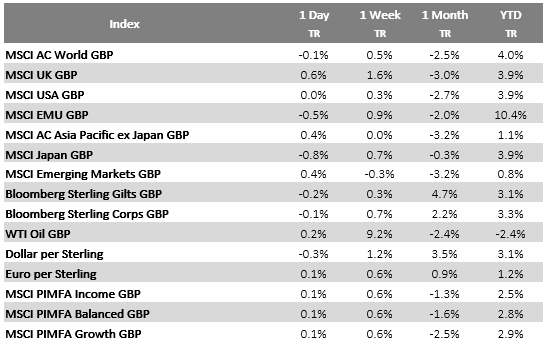

Please see below article received from Brooks Macdonald today 06/04/2023 which provides their views on recent global market events:

What has happened

Market sentiment worsened yesterday with additional data releases pointing towards weakness in economic growth. The ADP’s private payroll report came in far lower than market expectations, mirroring some of the softening labour market evidence from the job openings survey on Tuesday. US equities fell yesterday with technology shares underperforming despite rate expectations continuing to fall.

US economic data

After the ADP report set the scene for a risk-off day of equity market trading, the final PMI readings for March were released. There were some sizeable downgrades versus the flash estimates with both the services and composite readings disappointing. To cap off the weak day for data, the US ISM services index came in lower than estimates with declines within the employment and new order subcomponents compared to the previous month. These data releases cemented the market’s view that it was no more than a coin toss as to whether the Fed will raise interest rates by 25bps at their May meeting. Given the focus on employment readings in recent days this sets the market up for the US jobs report which is released tomorrow despite most markets being closed for Good Friday.

US employment report

In terms of what to expect from the jobs report, the consensus expectation is for 240k new jobs to have been created in March, down from the 311k seen in February. The unemployment is expected to remain steady at 3.6% and average hourly earnings are expected to tick down on a year-on-year basis from 4.6% to 4.3%. With the softer employment numbers recently, a major question will be whether this has impacted wage inflation or the average length of the working week (which is expected to remain steady at 34.5 hours).

What does Brooks Macdonald think

Despite employment remaining tight compared to historical averages, investors are starting to consider whether we may be seeing a pivot in labour market strength. The US employment report is therefore crucially important as it could confirm the recent trends in business demand for new workers. Investors will have until Monday in the US, and Tuesday in the UK, to conclude whether the report provides further impetus to the decline in equity markets this week.

Please check out blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below Markets in a Minute article received from Brewin Dolphin yesterday evening, which provides a global market update.

All major indices finished last week in the green as rising oil prices helped to boost energy stocks, while fears of financial instability eased.

In Europe, the Stoxx 600 gained 4.0% and Germany’s Dax added 4.5% after eurozone inflation eased to 6.9% year-on[1]year in March, down from 8.5% in February. The UK’s FTSE 100 rose 3.1% after fourth quarter gross domestic product (GDP) figures were revised upwards.

Over in the US, the Dow added 3.2% and the Nasdaq rose by 3.4% in a week that saw the Federal Reserve’s preferred inflation gauge rise by a less-than-expected 0.3% in February.

China’s Shanghai Composite edged up 0.2% and the Hang Seng gained 2.4% after premier Li Qiang said China would work to expand its domestic market, improve the business environment, and prevent financial systemic risks.

Markets mixed as global oil output cut

Markets closed with mixed results on Monday (3 April) following a decision by the Organisation of Petroleum Exporting Countries (OPEC+) to cut oil output by more than one million barrels per day. The move could harm efforts to cool global inflation, and has raised new concerns about a further US interest rate hike in May.

The pan-European Stoxx 600 ended the day down 0.1%, whereas the UK’s FTSE 100 gained 0.5%. Energy stocks performed particularly well, with Shell and BP adding 4.5% and 4.3%, respectively. In the US, the Dow gained 1.0% and the S&P 500 rose by 0.4%.

In economic news, the Institute for Supply Management’s manufacturing purchasing managers’ index slipped by more than expected in March to 46.3, the lowest level in nearly three years, as new orders declined.

US core inflation cools

Last week saw the release of the closely watched US core personal consumption expenditure (PCE) index – the Federal Reserve’s preferred measure of inflation. Core PCE, which excludes food and energy, rose by a lower-than-expected 0.3% in February, an improvement on the 0.5% increase seen in January. On an annual basis, core PCE increased by 4.6%, down slightly from 4.7% in January.

Headline PCE, which includes food and energy, grew by 0.3% month-on-month and 5.0% year-on-year, compared to 0.6% and 5.3%, respectively, in January. Food prices rose by 0.2%, goods prices by 0.2% and services by 0.3% month-on-month, while energy prices declined by 0.4%.

Eurozone inflation eases

The eurozone headline inflation rate slowed to 6.9% in March from 8.5% in February, according to figures released by Eurostat on Friday. This was lower than the 7.1% increase forecast by economists and represented the largest drop since 1991. The decline was largely driven by a reduction in energy costs, which helped to ease cost[1]of-living pressures. Annual energy inflation fell from 13.7% to -0.9%. In contrast, prices for tobacco, food and alcohol grew by 15.4% in March year-on-year.

Core consumer price growth, which excludes food and energy, grew to 5.7% from 5.6% in February, reaching an all-time high. This result, combined with unemployment remaining low at 6.6%, has added to expectations of further interest rate hikes by the European Central Bank. Investors are broadly expecting a 0.25 percentage point increase in May, with up to two more hikes of the same size in the summer.

UK house prices see highest fall since 2009

Here in the UK, house prices fell by 3.1% year-on-year in March, the largest decline since July 2009, according to figures from Nationwide. Prices fell by 0.8% month[1]on-month, the seventh-consecutive monthly decline. The average house price in the UK is now £257,122.

Separate data from the Bank of England showed the number of mortgage approvals increased to 43,500 in February, up from 39,600 in January. This was the first rise in six months. Meanwhile, net mortgage lending dropped from £2bn in January to £0.7bn in February, the lowest level since 2016 (excluding Covid).

Revised US and UK GDP figures released

Figures released by the Commerce Department last week showed the US economy grew by slightly less than expected in the fourth quarter of 2022. GDP grew at an annual pace of 2.6%, lower than the previous estimate of 2.7% and down from 3.2% in the third quarter. This was driven by downturns in exports, non-residential fixed investment, state and local government spending, and a decline in consumer spending to 1.0%.

Economists have predicted US GDP will grow by up to 3.2% in the first quarter of this year. On an annual basis, expectations are for growth of 0.3 percentage points to 1.2%. Sentiment has been dampened due to recent turmoil in the banking sector.

Meanwhile, revised figures from the Office for National Statistics showed the UK avoided a technical recession in the fourth quarter of last year as GDP grew by 0.1%. GDP in the third quarter showed a decline of 0.1%, a smaller contraction than initially thought. A technical recession is defined as two consecutive quarters of contraction.

Please check in again with us soon for further relevant content and market news.

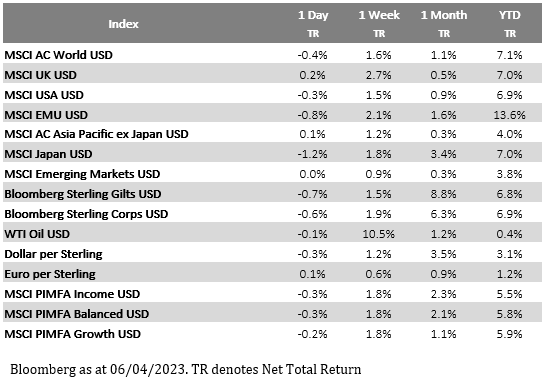

Please see the below article from Brooks Macdonald, providing a brief analysis of the past week’s economic and markets news. Received yesterday afternoon – 03/04/2023

Equities rallied on Friday as US and Eurozone inflation expectations came in below market expectations

Equity markets ended Q1 strongly on Friday, with the US index staging a late rally to cap off a positive week for markets as investors look to move past the banking turmoil of recent weeks. A significant driver of the risk on move was Friday’s softer-than-expected inflation data, which allowed bonds to rally after a tough week for the asset class.

On Friday the latest Core Personal Consumption Expenditure (PCE) inflation index was released, which came in at 0.3% month-on-month, lower than market expectations. The year-on-year reading of the US Federal Reserve’s (Fed) preferred inflation measure also missed expectations, coming in at 5%. Inflation expectations were somewhat of a mixed bag with the University of Michigan survey showing a fall in 1-year inflation expectations whilst those over 5 and 10 years rose. We also saw the Eurozone area inflation released which missed expectations after concerns had risen that European inflation would be stickier after the German release earlier in the week.

OPEC+ announced over the weekend that they were set to cut oil production by 1 million barrels-a-day

Over the weekend the OPEC+ group of oil exporting countries unexpectedly announced that they would cut oil output starting in May. The cut is set to exceed 1 million barrels a day with Saudi Arabia alone cutting 500,000 barrels a day. OPEC+ agreed to allow Russia to keep production unchanged as it struggles to finance the ongoing war in Ukraine. The White House strongly opposed this latest cut, citing its impact on consumers and its global inflationary impact. Global oil demand has been soft in Q1 of 2023 with oil prices falling each month of this year so far, as a result it is currently uncertain as to the equilibrium price for oil after the supply cuts. Falling oil prices have been a major driver of some of the disinflationary forces of the last 6 months and therefore policy makers will be concerned that the latest OPEC+ move may push back against their attempts to control inflation.

The risk of higher energy prices over the coming months will concern governments and central banks

Oil prices have started the week sharply higher with US equity market futures pointing to a lower start to US trading after the late rally on Friday. Lower energy prices have undoubtedly played into the lower 1-year consumer inflation expectation numbers released on Friday. Policy makers will be very conscious of the risks that a new surge in energy prices will represent and this will give further impetus to central banks to retain a hawkish narrative.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, a ‘Monday Digest’ from Tatton Investment Management discussing the key economic news from the past week. Received this morning – 03/04/2023:

March ran the whole gamut of emotions for investors, but for the average UK investor holding globally diversified risk profiled portfolios, Q1 still ended above where it began, even if the journey was rather bumpy. Bank run fears that caused so much March angst and downward volatility quickly abated, allowing markets to mostly recover into positive territory. However, just because stock markets have proved relatively resilient this time, we should not assume the episode will pass without further consequences. The global financial system’s ‘immune system’ becomes weaker after each attack, and right now the global economy is vulnerable and busy fighting off the ravages of inflation.

That said, the recovery rally in stock markets has told us that market liquidity remains reasonably healthy. It also appears that end-of-quarter rebalancing provoked some rather reluctant buying back of equities to cover underweight positions. Both government and corporate bond markets were eerily subdued as last week drew to a close. The week ahead could be fairly quiet too, and ahead of the Easter holidays, most of us would welcome that.

Banking scare meets inflation pressures

The banking sector is still scrambling to deal with the fallout from Credit Suisse’s forced sale and Additional Tier 1 (AT1) bond write-off. Credit conditions have become very challenging since several US regional banks collapsed, with lenders trying to reduce their risk exposure by handing out fewer loans. However, US bank failures, and subsequent turmoil in the financial system, have helped ease underlying concerns about the extent of further interest rate rises.

With the financial system effectively taking over tightening from the US Federal Reserve (Fed), markets now assume that policy rates may not need to rise much from here. Indeed, investors have built in expectations that rates will fall by the end of the year. However, given that corporate credit has two components – the ‘risk free’ rate of government bonds and the credit spread – this has eased conditions for companies with higher credit ratings, but worsened them for those with lower ratings.

The cost of both long-term and short-term borrowing has increased dramatically, and all maturities of borrowing are now well above the ten-year historic cost of corporate borrowing. Many companies will have no choice to refinance some borrowing, but most will also choose to cut back spending elsewhere. In essence, the US economy (and indeed the wider global economy) is going through a deleveraging process – which usually leads to lower growth prospects. That might not be such a bad thing for long-term stability, but lower growth means weaker credit metrics for many companies, particularly those at the lower end. We welcome the recent calm, but weaker credits are surely still in for a rough ride.

Is the microchip market heating up again?

The semiconductor industry has bounced between supply-demand extremes of late – and has experienced the ‘bullwhip effect’ post-pandemic. From its peak in late December 2021 to its early October 2022 trough, the Philadelphia Semiconductor Index (SOX) fell 47%, significantly sharper than the 26% fall in the wider US stock market. But since the end of last year, chipmakers have been on a roll. Cyclical adjustments are no doubt part of the story, but the current trend kicked-off with a sharp rally in early November. This was around the time OpenAI released the prototype of its ChatGPT program for general use. The chatbot’s ability to write detailed, knowledgeable and readable content on any given topic has gathered a lot of attention in the media. It also dramatically pushed up the estimated valuation of OpenAI and similar companies, as well as driving substantial investment toward artificial intelligence (AI) in general.

The fact that big tech companies are investing heavily in AI and advanced computing techniques is nothing new, so in itself the release of a new chatbot should not drastically increase demand for chips. Optically, though, it is a huge boost for the tech industry. For the last few years, those in the know have been critical of stagnation in the industry – not in terms of revenue, but in terms of genuinely transformative innovation. The accusation has been that many of the biggest players had effectively run out of new ideas and investor attention has waned as a result. The visibility of innovations like ChatGPT is therefore extremely valuable from an investment perspective, as it reaffirms the industry’s long-term growth prospects.

While it is unsurprising ChatGPT prompted a rally in chipmaker stocks, it is equally unsurprising this occurred while government bond yields were stabilising and investors were getting excited about the prospect of looser monetary policy. Certainly, the political appetite for public policy involvement in the tech sector has grown dramatically as tech has become synonymous with society’s security. Moreover, we already have seen high profile calls for tighter AI regulation or even pausing its development, including an open letter signed by Elon Musk and Steve Wozniak, among others. This is a battle set to run and run and as a result, investing into chipmakers at these sky-high levels may prove the sole preserve of tech optimists.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

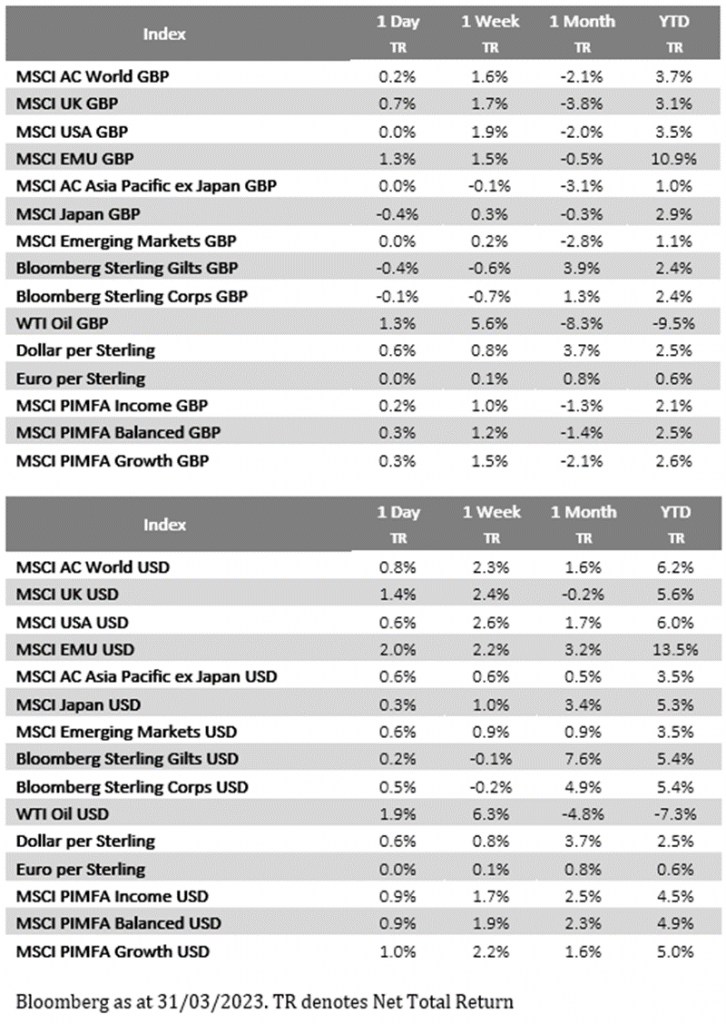

Please see the below article from Brooks Macdonald providing their latest Investment Bulletin received this afternoon 31/03/2023.

What has happened

Equities rose yet again yesterday with European equities seeing some outperformance as the market caught up with US gains late on Wednesday. European bonds came under pressure after the German inflation release showed an acceleration in price pressures with the year-on-year CPI print coming in at 7.8% versus 7.5% expected. This led German bund yields to rise across the yield curve with other European bonds following the move in the benchmark Eurozone sovereign.

Federal Reserve Speakers

Yesterday saw another set of speeches from Fed members as the conference roster continues now the Fed meeting is out of the way. President Collins sounded hawkish despite the recent banking issues, saying that ‘inflation remains too high, and recent indicators reinforce my view that there is more work to do.’ President Kashkari meanwhile focused on some of the concerns around banking sector liquidity but added that ‘the services part of the economy has not yet slowed down and … wage growth is still growing faster than what is consistent with our 2% inflation target.’ Lastly President Barkin reminded markets that the Fed was considering a 50bp interest rate hike last week until just before the SVB failure, and that ‘if inflation persists, we can react by raising rates further.’ As bond and equity markets calm in the aftermath of March’s banking troubles, Fed speakers appear more comfortable actively weighing up financial stability and inflation risks in full view of the market.

Inflation data

Today attention will move to the US PCE inflation data which is expected to show core PCE expanding by 0.4% month-on-month compared to 0.57% in January. Economists are also forecasting a fall in personal income and personal consumption after a very robust level of growth in January. With the PCE data coming out after the release of the CPI and PPI prints the market has a reasonable steer on the overall level of inflationary pressure and therefore the consumer demand numbers could be equally important.

What does Brooks Macdonald think

The PCE print will look at February’s data and therefore the Fed and market participants will find it difficult to extrapolate any data into the rest of 2023 given the turmoil of March. The PCE data will however give some indication of whether the economic strength and stickier inflation shown in other February data sets is also shown in the Fed’s preferred inflation measure.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

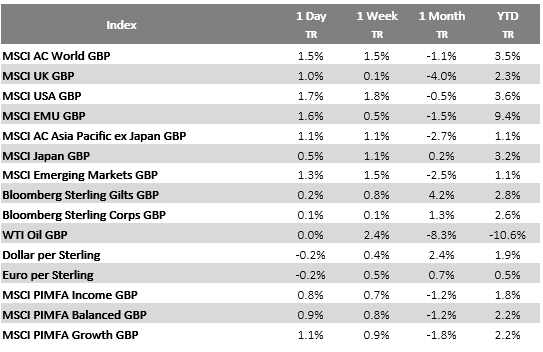

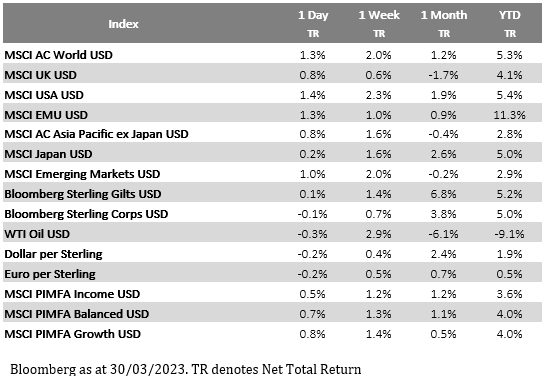

Please see below article received from Brooks Macdonald today 30/03/2023 which provides their views on recent global market events:

What has happened

Equity markets managed to retain their calm from earlier in the week yesterday and as risk appetite returned, US and European equity markets saw a broad rally. With yesterday’s rally, the US equity market has now closed above the level set before Silicon Valley Bank entered the newswires. US technology outperformed, with the sector set for a strong Q1 barring any major issues in the next few days.

Central Bank Speakers

Fed Speakers yesterday stuck to the data dependent script with Barr saying that the Fed would make a ‘meeting-by-meeting judgement on rates’ that would evolve as the data unfolded. The bond market began to settle down yesterday, pleased to hear the data dependent messaging reiterated and now the market expects just over 50bps of interest rate cuts after the terminal rate is reached at May’s meeting. The calm in the bond market reflects the fact that much of the post SVB rally in sovereign bonds has unwound over the last trading week. It was a similar message from the ECB yesterday as Kazmir stressed that members of the ECB governing council had ‘agreed we will not give guidance about May ECB policy meeting’ as the bank observes incoming data. Kazimir added that the ‘ECB shouldn’t back down on rates but maybe slow the pace.’

UK data

There was some stronger UK data yesterday as both consumer credit and mortgage approvals beat market expectations. Whilst consumer credit data could show a stretched consumer reliant on credit to meet the cost-of-living squeeze, the mortgage approvals are more unambiguously positive. The Bank of England’s Mann said that the UK economic outlook had improved given lower wholesale energy prices and the associated energy price caps. Of course, robust economic demand could put the Bank of England under pressure to hike rates further however it does push back against market expectations of a UK recession.

What does Brooks Macdonald think

A recession in the UK and Europe has been a consensus view amongst many investment strategists since the start of the year. Indeed, that expectation, combined with disinflationary data, helped equities to rise in January of this year as investors hoped that a short recession would help eliminate any demand-led inflationary pressure. The robust economic data globally pushes back against this recessionary expectation but at the same time risks inflation staying higher-for-longer which may necessitate more aggressive central bank action down the road to unanchor any increases in consumer inflation expectations.

Please check out blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below article received from Brewin Dolphin yesterday afternoon, which provides a cautiously optimistic market update despite high inflation and banking sector concerns.

Stock markets ended last week in the green as hopes of interest rate cuts outweighed recent concerns about the banking sector.

In the US, the S&P 500 and the Nasdaq added 1.4% and 1.7%, respectively, as the Federal Reserve hiked interest rates in line with expectations. The Fed’s ‘dot plot’ – a chart which summarises the central bank’s outlook for interest rates – suggested officials expect to stop raising rates after one more hike in May.

The FTSE 100 added 1.0% after UK retail sales recorded their largest monthly gain since October and business activity expanded for a second consecutive month, demonstrating resilience in the UK economy.

The pan-European Stoxx 600 gained 0.9%, despite a sharp decline in banking stocks. Eurozone business activity was stronger than expected in March, driven by growth in the services sector.

In Asia, China’s Shanghai Composite edged up 0.5% and the Hang Seng climbed 2.0% as analysts predicted policymakers would maintain an accommodative monetary policy in light of the banking sector turmoil.

Investors cheered by Silicon Valley Bank deal

Stocks started this week in the green, with the FTSE 100, Stoxx 600 and S&P 500 gaining 0.9%, 1.1% and 0.2%, respectively, on Monday (27 March). Banking stocks, in particular, were boosted by news that First Citizens Bank had agreed to buy the deposits and loans of Silicon Valley Bank, the US regional bank which collapsed earlier in the month. There are hopes that the turmoil in the banking sector has now peaked.

In economic news, a survey by the Ifo Institute showed German business sentiment unexpectedly improved in March. The business climate index rose to 93.3 from 91.1 in February, marking the fifth-consecutive monthly increase.

Fed suggests rate hikes are nearing an end

Last week, the Federal Reserve pressed ahead with a quarter percentage point increase in interest rates – its ninth-consecutive rate hike since March 2022. As ever, investors were more interested in the Federal Open Market Committee’s (FOMC) post-meeting statement than the rate hike itself, which had been widely anticipated.

Unlike previous statements which referred to “ongoing increases” in interest rates to bring down inflation, this latest statement said that “some additional policy firming” may be appropriate. Projections indicated that a majority of officials expect only one further rate hike this year.

Fed chair Jerome Powell said the FOMC had considered a pause in rate hikes because of the troubles in the banking sector, but went ahead with the increase due to inflation data and the strength of the labour market. Powell also stated that rate cuts were not in the Fed’s base case for the remainder of 2023. However, futures markets are nonetheless pricing in a more than 90% chance that rates will end the year lower than the current Federal funds target rate of 4.75% to 5.0%, according to the CME FedWatch Tool.

BoE lifts UK base rate as inflation soars

The Bank of England (BoE) also increased interest rates by a quarter of a percentage point last week, marking its 11th consecutive rate hike. The increase has brought the base rate to 4.25%.

UK base interest rate

The BoE’s meeting came a day after figures from the Office for National Statistics (ONS) showed the rate of inflation unexpectedly accelerated in February to 10.4% year-on-year, up from 10.1% in January. Economists had been expecting the rate to decline to 9.9%. Prices of food and non-alcohol drink rose by 18.2%, the steepest pace in more than 45 years, as high energy costs and bad weather led to shortages of salads and vegetables.

Data indicates UK economic resilience

Other data released last week suggested the UK economy may be more resilient than previously thought, despite high inflation and borrowing costs. Retail sales volumes rose by 1.2% in February from the previous month, with sales returning to their pre-pandemic levels. The increase was well above the 0.5% rise forecast by analysts.

S&P Global’s flash UK purchasing managers’ index (PMI) showed business activity expanded for a second consecutive month in March. The main composite output index measured 52.2, down from February’s eight-month high of 53.1 but still comfortably above the 50.0 mark that separates growth from contraction. Manufacturing production decreased slightly, whereas services sector activity picked up for the second month running.

Chris Williamson, chief business economist at S&P Global Market Intelligence, said the UK economy looks to have returned to growth in the first quarter, and that the improvement in order book growth “adds to signs that a near-term recession has been avoided”.

Meanwhile, research company GfK’s consumer confidence index rose two points in March to -36. Within that, consumers were more positive about the general economic situation over the next 12 months. However, they were more pessimistic about their personal financial situation – a measure which Joe Staton, client strategy director at GfK, said “best reflects the financial pulse of the nation”.

Please check in again with us soon for further relevant content and news.

Please see the latest Weekly Market Commentary from Brooks Macdonald received this morning:

Banking fears characterised last week with concerns culminating in questions over Deutsche Bank’s creditworthiness

Despite the UBS and Credit Suisse deal, last week was characterised by high levels of banking sector volatility, culminating with fears over Deutsche Bank’s credit worthiness on Friday. Words from regulators and officials over the weekend have helped to calm market concerns setting a better backdrop for European financials this week.

This week sees important US and European inflation readings including the US Federal Reserve’s preferred measure

While investors have been focusing on the banking sector risks in the short term, inflation will quickly return as a major driver of market sentiment. This week sees the release of the US Personal Consumption Expenditure (PCE) inflation numbers, the preferred measure of the US Federal Reserve. Core PCE is expected to have expanded by 0.4% on a month-on-month basis, keeping the year-on-year figure flat at 4.7%. Within the PCE release will be the US personal consumption and income lines which are both expected to decline after strong results in January. These barometers of consumer demand will also be supported by the releases of the Conference Board’s consumer confidence survey as well as the Michigan Sentiment survey. Europe will also see a fresh set of inflation data with Germany’s preliminary inflation readings released on Thursday before the Eurozone wide release on Friday. The market expects the annual rate of Eurozone Core Consumer Price Index (CPI) to pick up from 5.6% to 5.7%, pushing back against hopes of a rapidly falling inflation picture.

With the communication blackout concluded, Fed officials will now be able to comment on the volatility of the last few weeks

Throughout the banking turmoil of the last few weeks Fed speakers have largely been unable to comment given the pre-meeting communication blackout. This week sees a range of Fed speakers as they are now able to comment on not only the Fed’s 25bp hike last week but also the broader contagion risks in the banking sector. The market ended the week expecting only a 25% chance of a 25bp rate at the May meeting, with bond investors increasingly favouring the chances of no change at all. With 88bps of interest rate cuts priced in, how Fed speakers comment on this pricing will be an important bond market force this week.

With sentiment so fragile currently, it is perhaps no surprise that speculation and rumour around the health of major US and European banks can trigger such a strong risk-off response. Authorities and investors will be hoping however that the market can return to focusing on the fundamentals this week such as inflation and the state of the consumer, rather than another round of banking fears.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, an article from Tatton detailing the key news from markets around the globe over the past week. Received this morning – 27/03/2023

Swiss parochialism backfires

March continues to provide investors with the opposite of the ‘steady-as-she-goes’ environment of January and February. It appeared that global banking sector turmoil had eased after Swiss authorities officiated over a classic ‘shotgun’ marriage between Credit Suisse and UBS. Indeed, for a few days, stock markets and bond yields recovered somewhat, but the uneasy equilibrium was unbalanced once again after the US Federal Reserve (Fed) raised rates by another 0.25% to a range of 4.75%-5.0%.

Fed chair Jay Powell acknowledged the stresses on banks would likely tighten financial conditions, meaning the Fed may not need further rate rises to pursue its policy goals. Given it was aggressive monetary tightening that had weakened banks’ capital base, the obstinance of the rate decision saw focus return to other names in the banking sector. Germany’s Deutsche and Commerzbank came under renewed pressure, as well as some French and Italian banks.

No doubt much of the banking sector is suffering collateral damage from the central banks’ war against inflation over the past 12 months. But the manner in which the Swiss authorities hammered out the UBS takeover of Credit Suisse may well have amplified the returning weakness. The ‘rescue’ of Credit Suisse came at the expense of holders of its Additional Tier 1 (AT1) bonds (aka contingent convertible ‘CoCo’ bonds) which were written down to zero, while its equity shareholders (ranked below bond holders in the capital structure) were spared a similar fate. This preferential treatment of equity over bond holders is without precedent and deeply concerning. The principle is not that AT1 bond holders should be protected from loss, but that the capital structure as investors understand it must be upheld to re-establish trust in – and investor appetite for – the banking sector.

We should make clear that Tatton has no particular ‘skin in the game’ here. Our investment portfolios have minimal exposure directly to these issues, if any – and where we do, it is mostly through index tracker funds. The point is rather that instead of re-establishing trust among banking sector clients and investors, the Swiss authorities did the opposite, supposedly in the name of speed of action and financial stability. The aftermath still reverberates around markets, and we suspect last weekend’s actions have substantially eroded the Swiss banking sector’s international standing.

Banking sector rout squeezes the little guys

As noted last week, a rate rise cycle as dramatic as this one is bound to reveal cracks in the system. But no matter how much you mitigate systemic risks, each bank run increases the chances of another one. Almost every bank, no matter how well positioned, will take precautionary action as a consequence. Lenders will be more cautious, reducing capital available to corporations. As such, analysts suspect a general credit crunch in corporate America is now all but certain.

Storms are always worse for smaller boats, and small and micro-cap firms will be particularly hard hit. We are already seeing this play out, with investors pulling out of small businesses. In particular, positions in highly-leveraged companies have plummeted through March. Credit spreads – the premium companies have to pay for borrowing above those the government enjoys – are now expected to see their largest monthly increase since last September. Companies that rely on regional banks for funding will be very worried. According to Bloomberg, US commercial property owners will see nearly $400 billion of debt mature this year, requiring refinancing, with another $500 billion set to mature in 2024. With the financial and economic backdrop as it is, many could struggle to find banks willing to provide new loans. Those that secure refinancing will do so at sharply higher costs.

Those scarred by memories of 2008 will no doubt be alarmed by problems spreading higher up the credit chain. But we maintain our broad assessment from last week: this classic liquidity squeeze will cause problems for many, but systemic failure is highly unlikely. Policymakers are doing a good job of filling in the cracks before anything shatters. We welcome the relative calm of the past week, but further troubles are inevitable, potentially even for bigger players. We should have a safe landing in the end, but the rollercoaster is not finished yet.

UK inflation makes an unwelcome comeback

Last week’s announcement from the Office for National Statistics (ONS) that consumer prices index (CPI) inflation had crept up from 10.1% year-on-year in January to 10.4% in February came as an unwelcome surprise. Before this news, things were looking better for the UK economy, albeit only slightly. Falling fuel prices, easing global input costs and a small but consistent slide in monthly inflation had suggested ‘peak’ inflation was behind us, a view even endorsed by the Bank of England (BoE). But the latest inflation print poured cold water on hopes that the central bank might slow down or even suspend its interest rate rising cycle. Instead, the BoE increased its base rate by 0.25%, taking it to 4.25% in the 11th rise since December 2021.

Food, drink and clothing were the main culprits according to the ONS, with food and non-alcoholic drink prices rising 18% in February, the fastest pace in 45 years. This was despite food prices outside of the UK generally falling over the last few months, suggesting this particular problem is specifically British. Even disregarding the food element though, prices were still higher than expected. Core inflation – which strips out more volatile elements like food and fuel – came in at 6.2%, higher than January’s 5.8%. This is a measure the BoE pays close attention to, as it is an indicator of more persistent ‘stickier’ inflationary trends. Along those same lines, inflation in the services sector rose to 6.6% from 6.0% the month before, suggesting stronger-than-expected wage pressures. The BoE was concerned enough to raise the base rate to 4.25%. Since prices started soaring, policymakers’ biggest concern has been the threat of a wage-price spiral, where employees react to higher prices with higher wage demands, which in turn cause businesses to raise prices again.

However, the rise in food and clothing prices is notable. We think this is a sign companies – particularly supermarkets – are taking the opportunity to rebuild their profit margins, banking on the belief that consumers have become acclimatised to elevated inflation expectations, thanks to the prolonged period of rising prices. This may be good news for investors in supermarket shares, but less so for consumers and central bankers. If supermarkets tell us they’re doing well in their next trading reports, one might expect some pushback.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below an article from Evelyn Partners, which was published and received earlier today (23/03/2023) and covers their views on the Bank of England’s monetary policy decision to raise interest rates by 25bps:

What happened?

The Bank of England increased rates by 0.25% today at their March monetary policy meeting, which is in line with market and economic expectations. This takes the base rate to 4.25%, its highest level since 2008. The Monetary Policy Committee (MPC) voted 7-2 in favour of 25bps – 0bps respectively so policymakers continue to have diverse view on the best course for rates, although to a lesser extent than the 3-way split seen in December.

What does it mean?

When making their decision, committee members would have been weighing the fragility of the banking sector against the need to bring inflation back to target.

On one hand the recent turmoil in the banking sector, which began with collapse of Silicon Valley Bank (SVB), will remind central banks that things can break when monetary policy is rapidly tightened. Although contagion risks look to have receded for the time being, the BoE will need to tread carefully if they decide to further tighten monetary policy from here. The BoE recently acknowledged: ‘more sharp moves in asset prices could expose weakness in parts of Britain’s financial system’ in a letter to law makers.

On the other hand, yesterday’s CPI print showed that inflation re-accelerated in February with both headline and core CPI posting a gain of 1.1% and 1.2% respectively for the month. On top of this the labour market continues to remain tight putting pressure on wage growth which could further stoke inflation and cause it to become entrenched.

Moreover, recent UK economic data has been surprising on the upside: February’s PMI readings came in well above consensus with the composite figure reported at 53.0, consistent with a recovery in economic growth. Growth expectations are likely to get a boost as falling energy prices feed through to a reduction in household expenditures, boosting real incomes and stimulating the economy. A boost to growth could cause inflation to decelerate slower the than the BoE’s forecasts currently expect, which may cause monetary policy to remain tighter for longer in response.

In sum, today’s decision to increase the base rate indicates two things. First, the battle against inflation is not yet won. Second, the Bank is confident in its ability, and tools, to maintain financial stability.

Bottom Line

Today’s 25 basis point rate hike by the BoE signals there is still more work to be done to tame rampant inflation, as well as highlighting the banks need to remain cognisant of the risks over-tightening can pose to the economy.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.