Please see below, an article from Evelyn Partners discussing the recent Monetary Policy Committee interest rate decision and the implications for markets and the economy. Received yesterday evening – 03/08/2023

What happened?

The Bank of England delivered on the expectations of economists and markets with an increase of 25bps to the base rate at their meeting today. This represents the Bank’s 14th consecutive increase and takes the base rate to 5.25%, its highest in 15 years. The committee was split 3 ways on the vote, with 1-6-2 members voting for 0-25-50bps increases respectively.

What does it mean?

Today’s decision by the Bank of England was always likely to be close, if markets are our guide. Prior to the meeting, Overnight Index Swap markets had priced around a 1/3 chance that the Bank would go further and increase by 50bps. In the end the MPC’s hawks, who would have preferred such a move, were outvoted by the majority, including governor Andrew Bailey.

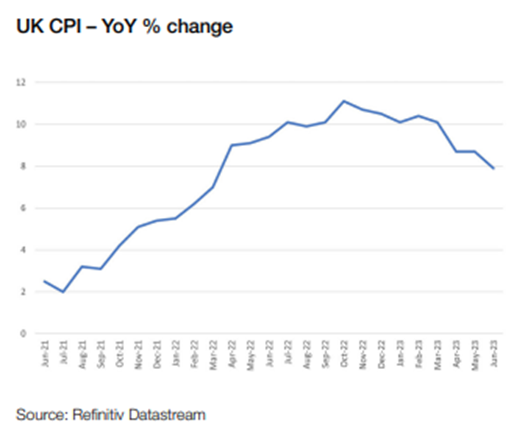

A key reason the bank will have decided against the larger increase will have been June’s inflation numbers, which finally revealed a downside surprise in headline inflation and, perhaps more importantly, the core (excluding volatile food and energy) print. The core figure came in at 6.9%, which will still high, was lower than July’s figure of 7.1%. The expectation is for inflation to continue to fall as lower energy prices continue to feed through to the bottom lines of balance sheets, both for businesses and individuals. This was reflected in the MPC’s own inflation forecasts, which fell from 5.1% to 4.9% in the fourth quarter of this year, although this was allied with an increase in its inflation expectations over the medium term.

The monetary policy report also included growth forecasts, which continued to make for pretty bleak reading, revealing a cut to forecasts to 0.5% per year for 2023 and 2024. On the upside, the Bank agrees with the consensus of economists in no longer forecasting a recession in the UK, but it does highlight the risk of one in 2024 and early 2025.

Previous guidance in the minutes released today was maintained: “if there were to be evidence of more persistent pressures, then further tightening in monetary policy would be required,”. There was an Important addition about rates being “sufficiently restrictive for sufficiently long” for inflation to get back to the Bank’s 2% target. That implies that interest rate cuts are perhaps further away than some had imagined.

The Bank provided no clues to the market today on its plans for reducing the size of its balance sheet, saying it will lay out these plans at its next meeting in September.

Bottom Line

Reaction to today’s 25bps increase by markets was dovish, as expectations of where rates will peak moved slightly lower, from 5.85% before the meeting to 5.75% afterwards, at the end of this year or beginning of next. This will be welcomed by mortgage holders, in the hope that increasing rate expectations may have peaked, along with the cost of mortgage deals in the market. The yield on the 10 year government gilt remained broadly unchanged on the announcement and looks attractive in our view, at 4.4%, as the Bank gets closer to the top.

Please continue to check our blog content for advice and planning news from us and leading investment management houses.

Alex Kitteringham

4th August 2023