Please see the below article from Brewin Dolphin commenting on the latest stock market movements. Received late yesterday 25/07/2023.

Stocks rise as UK inflation eases

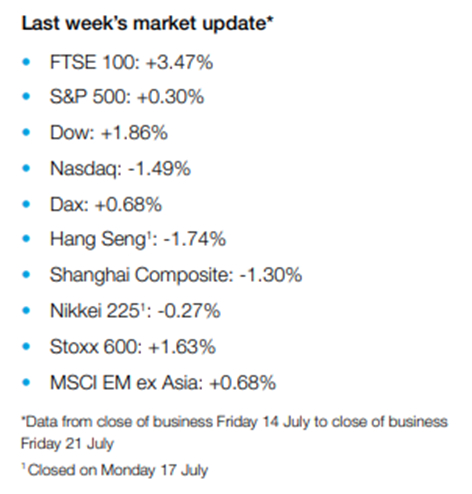

Most US and European indices rose last week as slowing inflation raised hopes that interest rate hikes could be nearing an end.

The FTSE 100 surged 3.5% as UK inflation eased more than expected, triggering a decline in the pound versus the dollar (around 70% of FTSE 100 company revenues come from overseas). The Stoxx 600 and Germany’s Dax climbed 1.6% and 0.7%, respectively, after two hawkish European central bankers appeared to moderate their stance on future rate hikes.

In the US, the Dow enjoyed its tenth consecutive day of gains on Friday – its longest winning streak since August 2017. The Dow ended the week up 1.9%, boosted by comments from Treasury secretary Janet Yellen that the risk of a US recession had fallen. Disappointing technology sector earnings weighed on the Nasdaq, which lost 1.5%. In Asia, the Shanghai Composite and the Hang Seng fell 1.3% and 1.7%, respectively, after figures showed China’s gross domestic product (GDP) grew by just 0.8% in the second quarter, down from the first quarter’s 2.2% expansion.

Investors shrug off weak PMIs

Stocks made small gains on Monday (24 July) as investors digested the latest purchasing managers’ indices (PMIs) for the US, eurozone and UK. The Dow extended its winning streak, advancing 0.5%, while the S&P 500 and the Nasdaq gained 0.4% and 0.2%, respectively. S&P Global’s flash PMI for the US showed business activity slowed to a five-month low in July, dragged down by weaker services sector growth. Manufacturing remained in contraction territory, but rose from 46.3 in June to a forecast-beating 49.0 in July (a reading below 50.0 indicates a contraction).

The Stoxx 600 and the FTSE 100 managed to shrug off weak PMIs to edge up 0.1% and 0.2%, respectively, on Monday. S&P Global’s flash PMI for the eurozone showed business output fell at the fastest rate for eight months in July. The services sub-index fell to 51.1, its lowest in six months, while the manufacturing output index plummeted to 42.9, the lowest in more than three years. S&P Global’s PMI for the UK was also disappointing, with manufacturing and services sector readings both coming in below expectations at 45.0 and 51.5, respectively.

Investors will now be looking ahead to the Federal Reserve’s two-day policy meeting on 25-26 July and the European Central Bank’s policy meeting on 27 July.

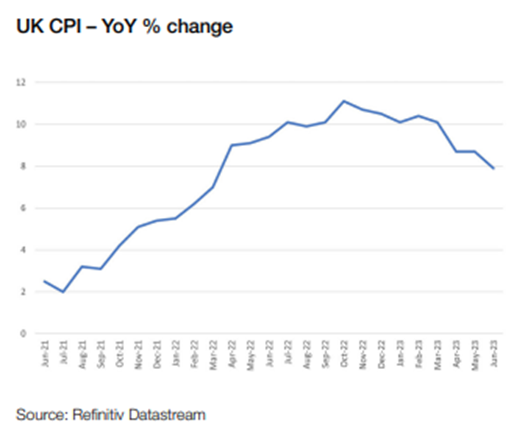

UK inflation rate falls to 7.9%

Last week saw the UK’s Office for National Statistics publish the closely watched consumer price index (CPI) report. The headline rate of inflation eased to 7.9% year[1]on-year in June, down from 8.7% in May and lower than expected. This was mainly driven by a 22.7% year-on[1]year decline in motor fuel prices. Food and drink inflation eased to 17.4% in June from 18.4% in May. Core inflation, which excludes energy, food, alcohol and tobacco, slowed to 6.9% in June after hitting a 30-year high of 7.1% in May.

The report has raised hopes that the Bank of England will be less aggressive when raising interest rates over the coming months. Markets now expect rates to peak at 5.8% this cycle, down from previous forecasts of 6.5%. The peak is expected to be reached in February 2024.

US retail sales rise modestly

In the US, retail sales rose by 0.2% in June from the previous month, while data for May was revised higher to show a 0.5% increase in sales. The data suggests sales have remained resilient despite interest rate hikes, although the rise was lower than the 0.5% increase forecast by economists in a Reuters poll. Online sales surged by 1.9%, the most in six months, whereas receipts at service stations and building material stores declined.

Core retail sales, which exclude automobiles, gasoline, building materials and food services, rose by a healthy 0.6% in June following an upwardly revised 0.5% increase in May. Core retail sales are an important indicator of consumer spending, which accounts for more than two[1]thirds of US GDP

Japan raises inflation forecast

Over in Japan, the government raised its inflation forecast for the current fiscal year to 2.6%, up from its January prediction of 1.7%. The announcement came a week before the Bank of Japan’s (BoJ) policy meeting on 27 July. Markets will be keen to see whether the revised forecast will result in the bank raising its own forecast and, in turn, tweaking its ultra-loose monetary policy. Latest figures show headline and core inflation both rose to 3.3% in June from 3.2% in May. Despite inflation persistently exceeding the 2% target, the BoJ has so far defended its stance. At the beginning of last week, governor Kazuo Ueda told a news conference that the BoJ would only change its yield curve control policy if there was a change in its inflation expectations.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

26/07/2023