Please see the below article from Tatton Investment Management detailing their views on global economic news from the past week.

Overview: Summer markets lukewarm on good news

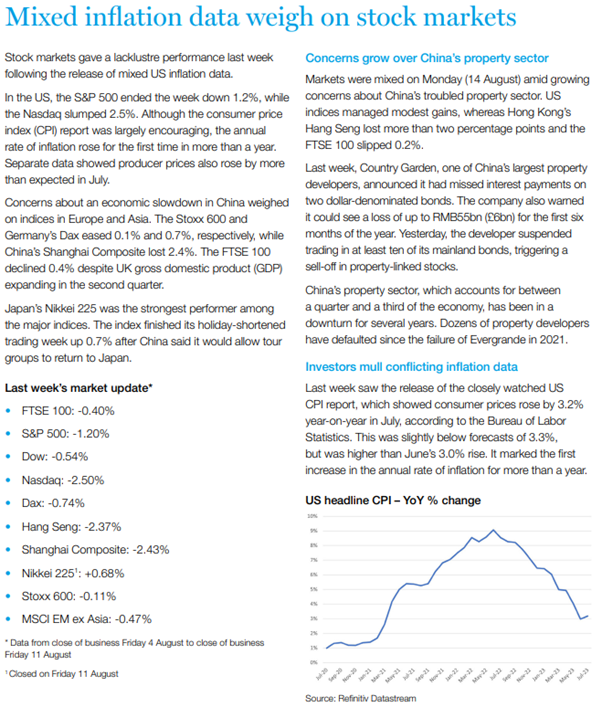

On the face of it, last week contained many of the positive headlines market optimists had been waiting for, but the response to those headlines received was tepid at best. On Thursday, the US Bureau of Labor Statistics released its consumer price index (CPI) inflation data for July, and it was relatively benign. In particular, the core CPI measure (with food and energy taken out) was +0.16% for the month, the same as in June. For the two months, annualised core CPI is now running below 2%, at +1.92%. Commentators reiterated the June narrative: that the US Federal Reserve (Fed) will be able to stop raising rates and then begin cutting next year. In the bond market, the 10-year yield went from 3.95% as the CPI data was published to 4.10% by the close on Thursday. Meanwhile, the S&P500 was pretty much unchanged. So, for equities and bonds, what was once a bullish driver has become less so now, and corroborative data is not new information.

Back at home, the Royal Institute of Chartered Surveyor’s report on the housing market continued to flag the prospect of further house price falls which, in earlier years, would be a harbinger of very difficult economic times. Yet the UK economy put in yet another quarter of growth, albeit anaemic, at +0.2%. The really surprising aspect was that July manufacturing and construction output was very strong at +2.4% and +1.6% month-on-month, respectively. That echoed the construction purchasing managers’ index (PMI) from last week, which showed a totally surprising shift into growth territory at 51.7 (50 marks the divide between contraction and expansion). Perhaps unsurprisingly, bond yields shifted sharply higher on Friday after the data, with the 10-year testing 4.5% and the two-year back at 5%. Neither has yet broken beyond the highs of the past month, however.

August is generally a quiet month, with holidays the priority for many. In recent years, it has felt more like business-as-usual, but market liquidity can still be somewhat reduced and, if news is really important, can lead to sharp dislocations. So far this month, the stories are not unimportant, but neither are they earth shattering, and while volatility has picked up, remains way down from last year and even the first half of this year.

China’s growing pains continue

China’s economy has sputtered again. CPI inflation fell 0.3% year-on-year in July. Producer prices were even lower, falling 4.4%. That might sound like a strange thing to complain about, given the West’s ongoing battle with high inflation; but China did not experience the same wave of post-pandemic inflation, and now deflation is a bad sign for the world’s second-largest economy. It shows weakness in consumer demand, which will likely mean slower growth down the line. Moreover, businesses competing with Chinese exporters are losing pricing power, while suppliers of commodities to China are experiencing a sharp slackening in demand. Thus, weak growth in China may be transferring to the rest of the world.

As we wrote recently about China, its economic problems have never been about lacking potential. The question is whether the government is willing or able to unlock it, and as yet that question remains unanswered. At the end of July, Beijing called for strong countercyclical measures to arrest a recent decline, but as (by now) usual, the details on what this means are lacking. Policymakers want to boost short-term growth, but are unwilling to loosen their grip on the private sector to do so.

China still has potential for a near-term rebound. But for foreign investors, the longer term returns on Chinese assets are hard to assess. Even though economic growth will come through, there is no guarantee this will translate into enough profit to justify investment, thanks to the unpredictability of central government. There are growth opportunities in China; Beijing only needs to decide if they are in its interest.

Is US earnings supremacy on the wane?

American companies are leading the way again this year, with 12.8% year-to-date returns as of the end of July. With the benefit of hindsight going back a decade, there are few better bets any international investor could have made than the US and its tech giants. Over the 20 years from 1989 to 2019, the S&P delivered an average real (inflation-adjusted) return of 5.5% a year excluding dividends.

However, a June discussion paper written by US central bank staff for the Federal Reserve Board of Governors in Washington argues that much of the growth in the value of US investments is explainable by different, more straightforward factors. The paper posits that exceptional US stock market performance over the last three decades was a consequence of changes to tax and interest rates. Moreover, it is very hard to see either of these trends continuing into the next decade or beyond. Short-term government interest rates have already increased from around 0% at the start of 2022 to above 5%, and markets expect these to come down over the next year or so. But as we have noted before, the economic environment – and particularly labour relations – mean we should not expect a quick return to the pre-pandemic norm of low inflation and growth.

Tax rates are a similar story. Effective taxation is already as low as it has been since corporate taxes were introduced, and the historically high levels of government debt are coinciding with an historically small tax base.

Equity prices change because of earnings growth and the rate investors are willing to pay for those expected earnings. Essentially, long-term US performance from here could be capped given that valuations are no lower than the average, an average based on net income growth which has had exceptional factors since 1989. It is possible that investors could show an even stronger bias for American assets, and accept a lower return because they feel US equities are less risky than other countries. This is not unthinkable but, in the current environment, it is hard to see the US outperforming to the level it has before.

Please check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

14/08/2023