Please see the below daily update on the markets from EPIC Investment Partners received this morning:

A single mathematics equation kicked off not one, but four multi-trillion-dollar industries that completely transformed how we think about risk.

The crazy part? This game-changing equation originated from some unlikely places – like studying how heat transfers, beating the casino at blackjack, and figuring out why microscopic particles jiggle around randomly (Brownian motion). An unlikely bunch ended up cracking the code on making fortunes from it too – physicists, mathematicians, and scientists rather than stock traders.

The earliest known options were bought around 600 BC by the Greek philosopher Thales of Miletus. He believed that the coming summer would yield a bumper crop of olives. To make money off this idea, he could have purchased olive presses, which, if you were right, would be in great demand, but he didn’t have enough money to buy the machines. So instead, he went to all the existing olive press owners and paid them a little bit of money to secure the option to rent their presses in the summer for a specified price. When the harvest came, Thales was right, there were so many olives that the price of renting a press skyrocketed. Thales paid the press owners their pre-agreed price, and then he rented out the machines at a higher rate and pocketed the difference. Thales had executed the first known call option.

In the late 1800s, French mathematician Louis Bachelier had to take a job at the Paris Stock Exchange to support his family. Observing the chaotic trading floor made him realize that stock prices follow a random walk, just like the erratic movement of particles in Brownian motion. Options can be an incredibly useful investing tool, but what Bachelier saw on the trading floor was chaos, especially when it came to the price of stock options. Even though they had been around for hundreds of years, no one had found a good way to price them. Traders would just bargain to come to an agreement about what the price should be. Applying physics principles, he derived the first formula for accurately pricing stock options.

Fast-forward to the 1970s, and economists finally built upon Bachelier’s work to create the legendary Black-Scholes(-Merton) equation for option pricing. This was adopted by Wall Street faster than you can say “get rich quick.” In fact, it was the quickest adoption of an academic concept in history – it enabled the explosion of multi-trillion-dollar markets for options, derivatives, securitized debt and more. Being able to find patterns of behaviour in this randomness spawned massive hedge funds, led by mathematicians and physicists, that were able to arbitrage the difference between Black-Scholes implied options prices and market prices of those very options. Ed Thorp’s (the pioneer of blackjack’s card counting methodology) Ridgeline and Princeton funds annualised over 20%, and Jim Simons’ Medallion fund made an incredible 66% per year for 30 years by using cutting-edge data science.

Modern-day managers have come full circle – from explaining the randomness and chaos to now finding the remaining predictable patterns within it to make money. However, the mathematics of Black-Scholes(-Merton) transformed our relationship with risk and volatility forever, even creating trillion-dollar industries out of thin air!

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see today’s Daily Investment Bulletin from Brooks Macdonald:

What has happened

The equity rebound that was in place for much of Tuesday’s trading session in global markets reversed into a net sell-off into the US close. Coming a bit out of the blue, as we have remarked earlier this week, as we close in on the long Easter weekend later this week, thinning trading volumes can at times contribute to increased volatility in asset markets, so this may have been a factor behind the late sell-off yesterday – that and perhaps some end-of-calendar-quarter repositioning might also have been in the mix. To be fair, it’s hard to pin the blame on the economic data that featured yesterday – in US focused-data, consumer confidence held more or less steady month-on-month, while durable goods data showed orders climbed above expectations. Elsewhere, in currency markets the drama over the last 24hrs has been around weakness in the Japanese Yen (JPY), which hit 34-year lows overnight (of 151.97 JPY to the US$) – the weakness was prompted by seen-as-dovish remarks from Bank of Japan (BoJ) member Tamura saying that the BoJ must proceed “slowly” towards normalising its ultra-loose policy. Finally, early morning data has showed that Australia’s inflation rate remained at +3.4% year-on-year in February for the third straight month against analyst expectations for a +3.5% gain.

US bridge collapse risks some inflationary supply-side shocks

In the early hours of Tuesday morning US time, a major bridge in Baltimore, Maryland collapsed after a container ship ‘Dali’, chartered by Danish shipping giant Maersk crashed into it. The Francis Scott Key Bridge, some 1.6 miles long, leads to the Port of Baltimore, the deepest harbour in Maryland’s Chesapeake Bay. It is the busiest US port for car shipments and is also the largest US port by volume for handling farm and construction machinery.

China’s Alibaba scraps logistics unit IPO

Chinese tech giant Alibaba announced on Tuesday that it was scrapping the planned US $1bn+ IPO of its Cainiao smart logistics unit (planned for the Hong Kong stock exchange), with the company citing “challenging IPO market conditions”. Alibaba’s shares are down around 18% over the past year. Reflecting deteriorating market conditions in China, with economic headwinds and hitherto regulatory uncertainty, Alibaba chairman Tsai described the market as “pretty depressed”.

What does Brooks Macdonald think

The US bridge collapse in Baltimore will likely have economic implications that serve as a reminder of supply-chain inflation risks. With global seaborne trade having to divert to other ports along the US eastern seaboard, the expected added cost impact is likely to ultimately feed through into higher prices to the US consumer, as businesses look to recoup increased transportation costs. As a result, at the edges it might show up in US inflation data in the coming months – while important to keep the size impact in perspective, it is nonetheless an additional incremental factor to add into the broader inflation mix for both markets and policymakers to reflect on.

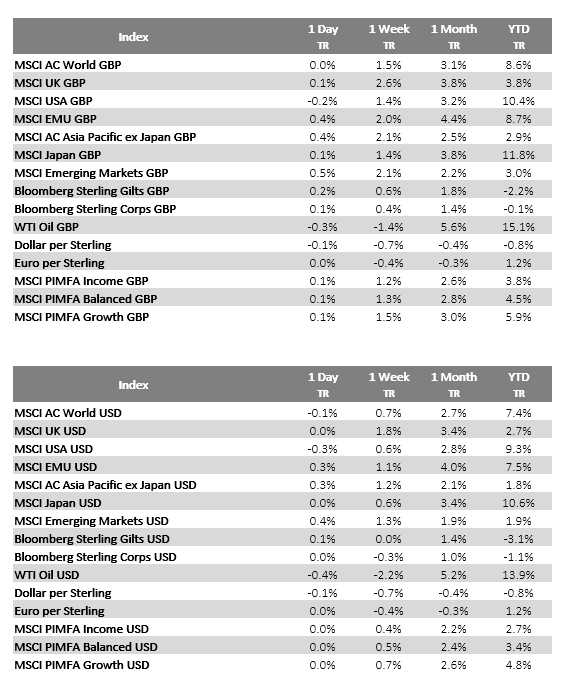

Bloomberg as at 27/03/2024. TR denotes Net Total Return.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see this week’s Markets in a Minute update from Brewin Dolphin, which was received yesterday evening:

Guy Foster, Chief Strategist, discusses recent dovish interest rate announcements from central banks, while Janet Mui, Head of Market Analysis, analyses purchasing manager indices data from Europe and the U.S.

Last week was big for central bank meetings. Although it saw the Bank of Japan (BoJ) raise interest rates for the first time in 17 years, the week was really characterised by dovishness from the central banks.

Interest rates rise in the East

European investors woke up to the BoJ’s decision last Tuesday morning. Money markets considered it touch and go whether it would hike or not, while consensus forecasts were firmly for the BoJ to keep rates in negative territory. However, news at the end of last week on the outcomes of the “Shunto” wage negotiations made the case for tightening much stronger. The Shunto translates to the spring wage offensive and represents a set season for wage negotiations, so if workers ended up striking together, their employers would not lose market share to peers. RENGO, the Japanese equivalent of the Trade Union Congress (TUC), announced last week that settlements achieved so far were above 5%; they were well below 4% last year. So, inflation by this measure remains strong in Japan.

Other measures seem less conclusive. Most obviously, Thursday’s inflation report would have encouraged the BoJ to tread slowly. Although headline inflation rose over the last year, that was mainly to do with fuel subsidies from last year dropping out of the numbers. The latest monthly inflation prints have been soft. The best measure, seasonally adjusted monthly moves in the core inflation rate, has been too low for the BoJ to hit its inflation target for the last four months. So, although the BoJ did technically surprise the market with an interest rate increase, its rhetoric was cautious enough to leave the outlook for further rate increases wide open. More people are talking about this being a one and done rate hike from the BoJ, although the money market still expects another two hikes this year.

Economic activity edging higher

The most hawkish news for Japan came from Thursday’s purchasing managers indices (PMI). It showed the third consecutive expansion in activity overall, with services growing at the fastest pace in ten months, while the contraction in manufacturing was at its least severe since November. These data suggest demand is holding up in the economy. They also suggest that inflationary pressures remain, as output prices rose in both the manufacturing and services sectors, with higher raw material, fuel, transport, and staff costs being cited as the factors behind the increase.

Although the survey results suggest the above factors might be driving up Japanese prices, the fact that they are not evident in consumer price indices (CPI) suggests they could also be weighing on margins.

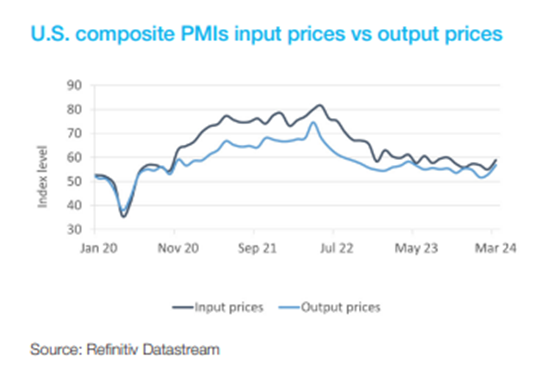

By contrast, the U.S. equivalent survey cited increased pricing power alongside “a steepening rise in costs”. This qualitative observation may tell us more about the disposition of the report author than the underlying economy, however, references to pricing power were notably absent from other regions.

U.S. interest rates left unchanged

The Federal Reserve left interest rate policy unchanged on Wednesday. It acknowledged that the economy is doing better than anticipated, easing its growth and inflation forecasts for the year. But the Fed also left unchanged its expectation of three interest rate cuts. That was a slight surprise as CPI data has run hot and the consumer remains resilient. This doesn’t seem to have changed the outlook for rates much, but it has stalled the upward march of year-end U.S. interest rate expectations that have been underway since mid-January.

With Japan raising rates and the U.S. expecting to cut rates, you could be forgiven for expecting the yen to strengthen. It rallied a little in response to the Fed’s meeting, but overall ended the week lower. The reason for this is that while Japanese rates rose last week, the increase was marginal. The more important driver of the exchange rate is where each respective currency’s interest rates will be in the future, and in relative terms, U.S. expected rates have been rising relative to Japanese expected rates (Japanese rates rising less than expected, but U.S. interest rates being cut by less than expected).

The outlook for liquidity

A big focus for the year will be on the timing of the Fed’s exit from quantitative tightening (QT). It sounds from Fed speakers as if this could be announced at its next meeting. This could be a positive story for markets because QT was assumed to be a factor that would weigh on investor demand by reducing liquidity that might otherwise find its way into equity and bond markets. In fact, equity markets have performed admirably while quantitative tightening has been going on, and liquidity watchers put this down to the reduced use of the Federal Reserve’s repo facility.

Repo means repurchase agreement, and it allows an asset owner to raise short-term liquidity by selling an asset, such as a government bond, to another investor whilst agreeing to buy it back at a future date and price. In this way, it turns assets into liquid cash.

Reverse repo, as you might expect, is the opposite; specifically, it involves a central bank such as the Federal Reserve selling securities into the financial system but agreeing to buy them back later. For the duration of the agreement, the Fed will have taken the proceeds out of circulation. So, increasing use of reverse repo is a way of tightening monetary policy and vice versa. The reverse repo facility has been declining as banks have used it less, bolstering their own reserves and offsetting the impact from quantitative tightening. But that decline will need to slow, stop, or even reverse at some stage, which will have an impact on liquidity. The Fed is looking at how this can be coordinated with the more stimulative impact of reduced quantitative tightening.

Markets were strong last week as the Fed reiterated its three-cut guidance, but they have been strong in previous weeks even when that has seemed in doubt. This loose liquidity environment has been one of the explanations, and as the Fed experiments with the winding down of QT and less liquidity is released from the reverse repurchase facility, there will likely be some wobbles in the market. A particular sector to watch will be the U.S. regional banking sector because any shortfall in liquidity is likely to be reflected in declining bank reserves and a return of solvency worries due to the bond assets these banks hold, which currently stand at a loss.

The UK hawks take flight

The final (major) central bank reporting last week was the Bank of England (BoE). Again, there was no surprise about its decision to leave interest rates unchanged, but what did stand out was the change in voting, where two hawks had previously voted to raise interest rates but this time aligned with the majority to keep them on hold. Unlike in other regions, inflation has been declining slightly faster than expected in the UK. Much of this relates to the delayed impact of the utility bills cap, which meant that inflation seemed slower to take off, before being sharper, and lingering longer, after which it is now declining faster once more. Indeed, inflation is expected to drop to, or even below, the BoE’s target in the next couple of months as high monthly increases from a year ago drop out of the latest figures. But it is not expected to last, and despite the downside surprise to UK inflation last week, when looking beneath the surface, those indicators of persistent inflationary pressure remain. The median price increase, having been stable but still marginally too high for the last few months, lurched upward this month.

Some of this lingering inflationary pressure is good news. It reflects the resilience of the UK economy and the fact that the UK seems to be emerging from a cyclical downtrend, as reflected in the PMIs. In addition, as we discussed last week, the housing sector is improving both in terms of demand and construction activity. And, of course, there has been a two, soon to be four, percentage point reduction in tax on a substantial portion of the income for people with a high propensity to spend.

But some of the persistent inflationary pressure is down to a lack of productive capacity, partly explained by a high rate of economic inactivity, which itself is driven by an increase in long-term sickness. No doubt this will be one of the key dividing lines for policy going into the next election.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below an article from EPIC Partners providing their daily round-up on markets, which was received late this morning (26/03/2024):

At the China Development Forum, the IMF’s Managing Director Kristalina Georgieva said she believes the world’s second-largest economy faces “a fork in the road”, whether to stick to its tried and tested policies that have worked in the past to a lesser or greater degree, or push for high-quality growth.

Georgieva added that: “With a comprehensive package of pro-market reforms, China could grow considerably faster than a status quo scenario”. The IMF believe these pro-market reforms could unleash a 20% expansion of the real economy over the next 15 years, which in today’s terms would equate to adding USD3.5tn to the Chinese economy. The IMF also upgraded its estimate that China’s economy will grow 4.6% in 2024, 0.4% point higher than its last forecast in October, and 0.4% below China’s own forecast.

However, Georgieva also warned that China had pressing near-term challenges, including transitioning the property sector on to a more sustainable footing and reducing local government debt. In order for this to happen China needs to take “decisive steps” to complete unfinished housing stranded by bankrupt developers and to reduce risks from local government debt she said. In doing so, China could “accelerate the solution to the current property sector problems and lift up consumer and investor confidence”. She went on to say that: “A key feature of high-quality growth will need to be higher reliance on domestic consumption”, adding that this “depends on boosting the spending power of individuals and families”.

Finally, as we approach Easter, the price of your Easter eggs next year might be a lot higher than the ones you bought this year. Cocoa futures are up 50% this month alone and have more than doubled since the turn of the year. The combination of aging trees, diseases, bad weather and demand has combined to create the largest shortfall seen in the cocoa market in more than sixty years.

On Monday, cocoa futures closed at nearly $10,000 a ton, up 8% from Friday’s close, up 250% in the last few months, making it more expensive than copper.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below article received from Tatton this morning, which provides a positive update on global markets.

Overview: Stick to the Plan

Brighter days for markets; returns were strong across the board last week, thanks to central bank messaging.

The Bank of England (BoE) “has done its job” according to Governor Bailey, and “we are not seeing a lot of sticky persistence” in inflation. Markets are pricing cuts in July, with rates settling at 3.5% in 24 months. If the BoE moves rates in line with economic activity, though, it would mean rates between 3% and 3.5% in around 18 months on our calculations.

The hawkish Monetary Policy Committee members are less hawkish now that inflationary behaviour has dissipated. Recent data shows more money is being spent, but the rise is slow. It vindicates the BoE’s wait-and-see approach. Comments suggest MPC members now fear low growth more than inflation, which could mean a rate cut in May if April inflation is lower than 2%, as expected.

The ECB could join in, after telling us that “rate cuts are coming”. Manufacturing confidence is low, and Switzerland cut rates during the week, supporting the notion of an ECB cut. The Bank of Japan actually raised rates, but markets acted like they cut (see article below). There was weakness in China – the heart of global disinflation – which led to falling Chinese bond yields and possible policy giveaways from Beijing.

The Federal Reserve said it was still expecting to cut rates, despite US inflation picking up. There is a growing confidence that the US economy is balanced, despite continued economic strength. But strength is a complication for chairman Powell’s plan. The Fed expects 2.1% real growth and 2.4% inflation in 2024, but things will have to slow from here to achieve that – and current activity is rising.

Central banks feel vindicated in sticking to their plans: inflation is down and activity is not too bad. For the Fed specifically, this might be overconfidence, but that will be good for company profits in the short-term. Our only worry is that, if inflation does move higher, the nice rate cut narrative might shift suddenly.

Japan’s rates are go – and markets up with them

The Bank of Japan (BoJ) raised interest rates for the first time in 17 years last week. The hike, from -0.1% to a range between 0% and +0.1% might seem tiny, but it is big and symbolic for the Japanese. The BoJ becomes the last central bank to end negative rates, curtailing the era of no payouts for Japanese depositors.

Markets reacted unintuitively. The value of the yen fell sharply, the currency now at ¥151 on the dollar. Bond yields also fell, with Japanese 10-year yields now well below the 1% peak from October. Equities rallied too, and the Nikkei 225 up over 20% year-to-date. All of these are the reverse of what you would expect when Japan’s monetary policy is finally tightening.

Markets acted like the BoJ cut rates instead of hiked them, because the decision came with dovish signals. Japanese inflation is now barely above the bank’s 2% target and trending down, so BoJ governor Kazuo Ueda has said borrowing costs will not go up sharply. Market positivity – which pushed the Nikkei past its 1989 asset bubble peak only last month – should help stave off a return to deflation.

Japan’s goods, services and labour are extremely competitive after decades of stagnation. There have been corporate structural changes in the last decade which will help take advantage of that too – resulting in the biggest wage increase since 1992. Structural changes, the third arrow of the late Prime Minister Shinzo Abe’s “Abenomics”, have finally hit home. This will likely mean stronger inflation and nominal growth, even if still low compared to the world.

Thankfully, the BoJ is keeping rates low relative to the expected growth, with real (inflation-adjusted) rates still negative. It refuses to do much in the face of inflation, and Japan’s economy should benefit.

Neom and the Saudi Line

Saudi Arabia wants to create the future of sustainable living in Neom, a futuristic megacity featuring “The Line”, a linear ‘smart city’ with no cars or fossil fuels. There is understandable cynicism in the West, considering the country is the world’s largest oil exporter and currently imports 80% of its food. Critics have called it “greenwashing” or purely PR, similar to Saudis’ extensive sports investments.

But at a top estimated cost of $1 trillion ($500bn on the low end), Neom would be by far the most expensive publicity stunt in history. There are more cost effective ways of improving image that Riyadh is already pursuing – like forcing international companies to set up Saudi headquarters or joint ventures in exchange for government deals. Many big names have already done so, and more are sure to follow.

The huge sums and coordinated policies tell us Crown Prince Mohammed bin Salman is serious about diversifying the Kingdom away from oil exports. It obviously has an interest in promoting oil, but the nation’s long-term interests are to no longer rely on the industry.

Part of the ‘Saudi Vision 2030’ campaign is about aligning Saudi Arabia – which has a higher GDP per capita than several European nations – with global economic and financial institutions. Its links to the global economy are currently one-track, and there are opportunities in diversifying them.

That requires upfront capital, and Riyadh is certainly willing to spend it. Not only might the Kingdom’s massive reserves be put to work for global companies, but the domestic stock market – including the world’s most profitable company Saudi Aramco – might be opened up too. It means a reallocation of capital towards newer, hopefully productive, areas. Opportunities are there, but risks of congestion and misallocation are too.

Please check in with us again soon for further relevant content and market news.

Please see today’s Daily Investment Bulletin from Brooks Macdonald:

What has happened

Dovish messages from central banks continued to led risk assets higher. In the US, the S&P 500 and the NASDAQ gained +0.32% and +0.20% respectively. The small-cap Russell 2000 index continue to outshine large-caps, surging by 1.14% to reach its highest point in nearly two years, while the Magnificent 7 suffered a decline of -0.43%, due to Apple’s notable drop of -4.09% following the initiation of an antitrust lawsuit. In contrast to the buoyancy seen in Western markets, Asian equities experienced a downturn, with Chinese stocks bearing the brunt of the losses. Hong Kong’s Hang Seng index fell by -2.16%, Hang Seng Tech index plummeted by -3.55%, and the Mainland Chinese CSI 300 index was down by -1.1%.

Bank of England holds rate steady

The Bank of England holds interest rate but the key takeaway from the policy decision meeting was that rate cuts might come sooner than expected. This change in sentiment comes as some hawkish BoE officials have retracted their previous support for rate hikes, and Governor Andrew Bailey has expressed a more sanguine view of the economic forecast. The markets are now pricing in a roughly 70% probability of a rate cut in June, with expectations fully set for a move by August. With headline inflation set to move below 2% from April, further calibration in the BoE’s policy message is likely in its May meeting when it will also publish updated forecasts. There are thoughts that May cut might be too soon because April inflation numbers will not be available until after the meeting. Nevertheless, Governor Bailey has suggested that inflation does not need to fall below 2% for the central bank to consider easing its policy.

What does Brooks Macdonald think

Bank of England’s messaging largely echoed what was communicated by the Fed earlier in the week. The persistently dovish tone from global central banks bodes well for risk assets, with the FTSE 100 index currently trading at the highest point since one year ago and edging close to the all-time-high level achieved in Feb 2023. This risk-on sentiment is also particularly beneficial for small and mid-cap stocks which have outperformed their larger counterparts for two consecutive days. It is important to highlight, however, that this wave of optimism did not extend to Chinese equities, which retreated today, as the negatives of domestic economic woes outweighed the positives of easy monetary policy.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, an update from Evelyn partners detailing the March inflation figures and Monetary Policy Committee meeting outcome. Received today – 21/03/2024

What happened?

The Bank of England (BoE) held the base rate at 5.25% at their meeting today. This was consistent with market expectations and marks the fifth consecutive meeting where rates have been held at this level.

There was, however, a notable shift in the committee votes, with nobody voting to increase interest rates. Eight members voted to hold the base rate at 5.25%, with Jonathan Haskel and Catherine Mann dropping their votes for higher interest rates, while Swati Dhingra continued to vote for a 25 basis point cut.

This follows February’s CPI print (released Wednesday), which came in slightly softer than expected at 3.4% year-on-year (vs consensus of 3.5%). Core CPI, which better reflects domestic price pressures, was reported at 4.5% year-on-year (vs consensus of 4.6%).

What does it mean?

As anticipated, the BoE held the base interest rate at 5.25%. But today’s change in votes signals that we are getting closer to interest rate cuts. Haskel and Mann, longstanding hawks, dropped their votes for higher rates, making this the first meeting since September 2021 with no votes for higher rates.

Moreover, the softer than expected February inflation print should give the monetary policy committee (MPC) more confidence that inflation is on the right track. CPI rose by 3.4% in the 12 months to February 2024, down from 4.0% in January. The largest downward contributions to the CPI annual rate came from food, and restaurants and cafes, while the largest upward contributions came from housing and household services, and motor fuels. Although the services component of CPI remains elevated at 6.1% year-on-year, and the MPC will want to see more progress on this measure before they commit to a rate cutting cycle.

On the growth side, the data is showing tentative signs that UK economic growth might be turning the corner. The UK composite PMI reading for March was 52.9, marking the third month in a row above 50 (50 signals expansion vs the previous month). This implies that the technical recession experienced in the second half of 2023 is now over.

Today’s meeting doesn’t seem to have materially changed the calculus for money market traders, although the probability of a June rate cut has increased to 70% from 50% at the start of this week. The market took the decision and communications as dovish, with sterling weaker against the US dollar and gilt yields falling across the curve.

Bottom Line

The BoE held interest rates at 5.25%, although today’s change in voting patterns signals that we are getting closer to a first interest rate cut. We continue to expect this will materialise around the middle of the year as inflation decelerates to the 2% mark.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, an article from Evelyn Partners explaining the implications for markets of the latest Federal Open Market Committee meeting and rate decision. Received last night – 20/03/2024

What happened?

The Federal Open Market Committee voted unanimously to keep rates on hold at 5.5% (upper bound) at the conclusion of their meeting today. This was in line with market expectations and is the fifth consecutive meeting where rates have been held at the same level since the last increase in July 2023.

The Fed also today released its quarterly ‘dot plot’ which tells markets where committee members see interest rates going in the future. It showed no change from their December publication in terms of median rate expectations for the end of 2024 at 4.6%, suggesting 75bps of cuts from current levels. Importantly, it did show revised expectations for where rates will be at the end of 2025 at 3.9%, suggesting one less cut than their estimate in December.

What does it mean?

No change in rates at today’s meeting came as no surprise to financial markets, which were pricing the chances of a cut at less than 1% going into the meeting. There were no significant changes in the wording of the statement today, and the ‘dots’ revealed fewer rate cuts to come but with one taken from 2025, rather than 2024 as some analysts had been speculating. Officials also increased forecasts of where they see rates settling over the long term, increasing their median estimate from 2.5% to 2.6%.

Interest rate expectations have moved a long way since the Fed’s last meeting on the 31 January. Immediately following that meeting, futures markets were pricing in six interest rate cuts over the course of 2024, while their ‘dot plot’ (which was published in December) was suggesting there would be only three. Since then, markets have slowly fallen into line with Fed thinking, with the latest market estimation for the number of rate cuts this year also being three, immediately before today’s meeting. That was largely thanks to month-on-month core CPI inflation prints for both January and February coming in 10 basis points higher than market expectations – stickier than expected. Producer Price Index inflation readings (a price measure at the wholesale level) have also come in hotter than expected, leading to bond market inflation expectations to move from around 2.2% (CPI) annually for the next 5 years to around 2.4%. Interestingly, the Fed’s preferred measure of inflation, the PCE deflator was not stronger than expected, with the headline measure for January coming in at 2.4%. This inflationary backdrop led the Fed to increase their estimates today for PCE inflation to 2.6% from 2.4% by the end of the year.

On the growth side of the equation, payroll gains have been strong in January and February although unemployment ticked up to a 2 year high of 3.9%. Q1 GDP is tracking close to 2% after the remarkable strong 4% seen in the second half of last year – lower but still above the long run rate.

This varied economic backdrop led the committee to repeat the guidance in the previous statement that it doesn’t expect to cut rates “until it has gained greater confidence that inflation is moving sustainably toward 2%.”

Officials maintained the pace of quantitative tightening, with a maximum of $60 billion of Treasuries and $35 billion of mortgage-backed securities rolling off the balance sheet each month, and no guidance of any changes to this.

Bottom Line

There weren’t many surprises out of today’s Fed meeting, and therefore market expectations (and our own) for interest rates have not changed. The equity market hasn’t been put off its stride by the prior moderation in cut expectations in quite the same way that the bond market has, but with futures markets finally in line with the fed, we would expect one source of volatility, particularly for the bond market, to dissipate. Clearer visibility over cuts should be a more benign backdrop for positive performance from both equity and bond markets.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from EPIC Investment Partners providing their update based on the latest UK inflation data. Received this afternoon.

UK CPI has fallen to the lowest level since September 2021 as easing prices for food, hotels and restaurants helped offset an increase in fuel prices and household services. The Office for National Statistics (ONS) said CPI dropped to 3.4% in February, 0.1% below the market consensus and the 4% recorded previously. Core inflation, so excluding volatile food, energy, alcohol, and tobacco prices, came in at 4.5%yoy, also 0.1% below estimates, and the previous reading of 4.1%.

Following the release, Grant Fitzner, chief economist at the ONS, said: “Inflation eased in February to its lowest rate for nearly two-and-a-half years. Food prices were the main driver of the fall, with prices almost unchanged this year compared with a large rise last year, while restaurant and cafe price rises also slowed. These falls were only partially offset by price rises at the pump and a further increase in rental costs”.

However, the drop in inflation is unlikely to have a material impact on the Old Lady’s rate decision tomorrow. The market was already overwhelmingly looking for the BoE to hold rates at 5.25% for a fifth straight meeting. The central bank is likely to stick to the script, acknowledging the possibility that the of the next move could be lower, while remaining vague about the timing.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from Brewin Dolphin giving their overview of global markets. Received yesterday.

Guy Foster, Chief Strategist, discusses improvement in the UK housing market and its effect on the wider economy, while Janet Mui, Head of Market Analysis, analyses the good and the bad news following fresh U.S. inflation data.

Hopes for seemingly enormous interest rate cuts during 2024 have been dissipating since the year began. Two months ago, investors thought U.S. interest rates would finish the year at just over 3.5%. Now that is just over 4.5%, implying there may be three interest rate cuts. But why the change in mood?

In short, inflation has remained stickier than expected. Last week’s U.S. consumer price index (CPI) print saw core inflation slightly above estimates for the second month in a row. Recent monthly readings have been consistent with a rate of core inflation of 4%, which is clearly too high.

Core CPI excludes the volatile food and energy prices that can make interpreting the data difficult. After this adjustment, shelter inflation makes up 45% of what is left. Some of the shelter data is very lagged in its impact because it relates to when tenancy agreements are renewed. Therefore, the Federal Reserve has discussed core services excluding shelter (so called super-core inflation) as a preferred measure. That rate also remains well above the Federal Reserve’s target rate.

On Thursday, producer price indices, which measure the prices of goods sold by their manufacturers, were also above estimates. This seems to fit the phenomenon that we have been highlighting over the last few months, that more companies are experiencing high services output prices.

A matter of ‘when’ rather than ‘if’?

All this sounds pretty concerning given the narrative for 2024 has been about interest rate cuts, and markets have certainly paused for breath. So far, though, investors still believe the question is ‘when’ rather than ‘if’ rates will be cut. Despite a full percentage point of cuts for this year being erased, long-term bond yields have risen by around 0.2%.

Theoretically, if you believe that companies are valued based upon bond yields with an acceptable equity risk premium, the stock exchange would be quite responsive to small changes in bond yields, but the evidence to support this is lacking.

Instead, the interaction between share prices and interest rates seems more likely to reflect the broader concept of liquidity, which so far this year remains reasonably abundant. The notable risk on this front would be if liquidity support for U.S. regional banks was to diminish, as we are now a year past the crisis.

U.S. retail sales accelerate in January

U.S. retail sales expanded at the fastest pace in five months during January, which could have given policy makers more inflationary fears to fret over. But this rebound reflected an improvement in the weather rather than a resurgence in animal spirits. Inclement weather caused a sharp decline in shopping trips during January and most of the recovery in February was driven by building materials and garden equipment, both of which are weather sensitive. U.S. goods demand therefore remains in the doldrums, with services having been the category of choice for consumers.

Chinese stocks bolstered by new growth target

Chinese stocks had a good week overall but were struggling for momentum by the end of it. The enthusiasm for these stocks has been bolstered by the idea that the newly announced growth target implies powerful stimulus must be coming.

Alas, it remains a trickle rather than a gush.

Despite property prices, which we learnt on Friday are continuing to decline, and bank loan growth, which decelerated to its slowest pace on record last month, the authorities have not been forthcoming with stimulus. Instead, China drained liquidity from the banking system during February and held interest rates steady.

The Chinese economy has shown some green shoots of recovery, with prices at last rising again in February after four months of deflation. It seems likely more stimulus through lower reserve requirement ratios and lower interest rates will eventually be unleashed.

UK GDP estimate turns positive in January

Green shoots are also evident in the UK. The January estimate of monthly gross domestic product (GDP) turned positive, which was implied by the already-released retail sales numbers for that month.

The recovery in the housing market continued as well, as last week’s Royal Institution of Chartered Surveyors (RICS) house price index would seem broadly consistent with house price growth of up to 5%. Demand for housing has recovered following a normalisation in borrowing costs. Most encouraging is that new sellers are entering the market as well, suggesting the recent uptick in prices is perceived to last. And it’s not just the secondary market for homes that is recovering.

More housing market activity also seems to be drawing a line under the fifteen-month housebuilding recession that the UK has suffered. More housing transactions are good for economic activity as they are labour intensive to build and even selling already existing homes triggers a chain of connected economic activity from financing to furnishing.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.