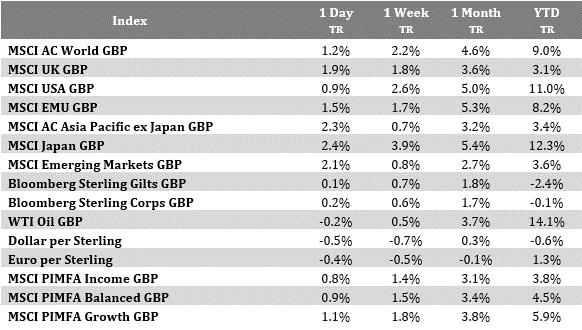

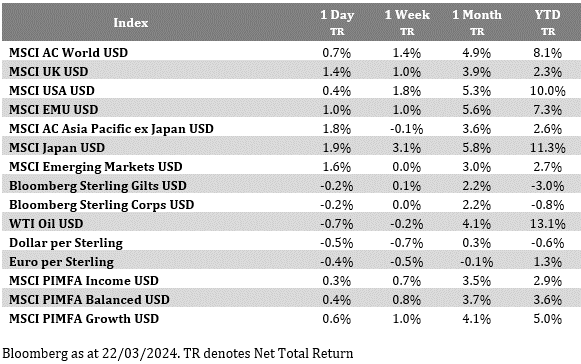

Please see today’s Daily Investment Bulletin from Brooks Macdonald:

What has happened

Dovish messages from central banks continued to led risk assets higher. In the US, the S&P 500 and the NASDAQ gained +0.32% and +0.20% respectively. The small-cap Russell 2000 index continue to outshine large-caps, surging by 1.14% to reach its highest point in nearly two years, while the Magnificent 7 suffered a decline of -0.43%, due to Apple’s notable drop of -4.09% following the initiation of an antitrust lawsuit. In contrast to the buoyancy seen in Western markets, Asian equities experienced a downturn, with Chinese stocks bearing the brunt of the losses. Hong Kong’s Hang Seng index fell by -2.16%, Hang Seng Tech index plummeted by -3.55%, and the Mainland Chinese CSI 300 index was down by -1.1%.

Bank of England holds rate steady

The Bank of England holds interest rate but the key takeaway from the policy decision meeting was that rate cuts might come sooner than expected. This change in sentiment comes as some hawkish BoE officials have retracted their previous support for rate hikes, and Governor Andrew Bailey has expressed a more sanguine view of the economic forecast. The markets are now pricing in a roughly 70% probability of a rate cut in June, with expectations fully set for a move by August. With headline inflation set to move below 2% from April, further calibration in the BoE’s policy message is likely in its May meeting when it will also publish updated forecasts. There are thoughts that May cut might be too soon because April inflation numbers will not be available until after the meeting. Nevertheless, Governor Bailey has suggested that inflation does not need to fall below 2% for the central bank to consider easing its policy.

What does Brooks Macdonald think

Bank of England’s messaging largely echoed what was communicated by the Fed earlier in the week. The persistently dovish tone from global central banks bodes well for risk assets, with the FTSE 100 index currently trading at the highest point since one year ago and edging close to the all-time-high level achieved in Feb 2023. This risk-on sentiment is also particularly beneficial for small and mid-cap stocks which have outperformed their larger counterparts for two consecutive days. It is important to highlight, however, that this wave of optimism did not extend to Chinese equities, which retreated today, as the negatives of domestic economic woes outweighed the positives of easy monetary policy.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

22/03/2024