Please see below article received from Blackfinch this morning, which provides a detailed global market update for February 2024.

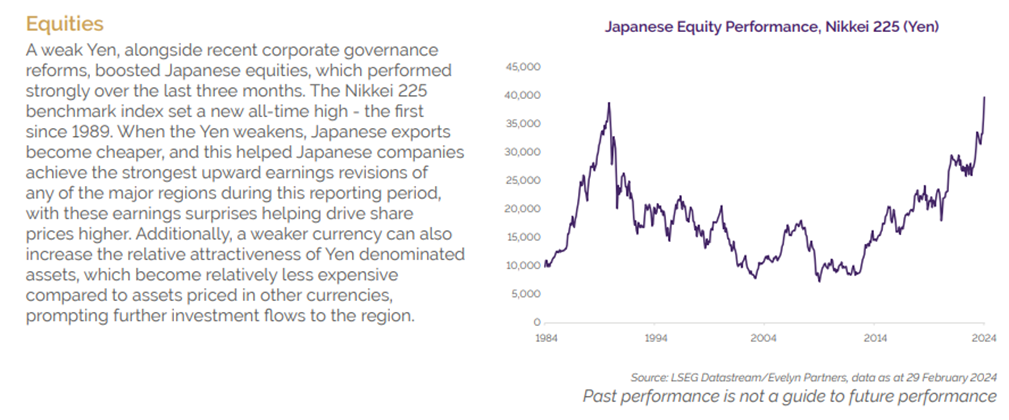

February was a record-breaking month for equity market returns, with several regional indices hitting all-time highs. The key stories were in the US and Japan, with US returns driven by the darling of the Artificial Intelligence (AI) world, Nvidia, boosting sentiment across the market. Japan boasted an impressive corporate earnings season, as well as stark improvements in corporate governance, which helped Japan’s largest index burst through the ceiling set at the end of 1989, when Tokyo real estate was the most valuable on the planet. On the economic front, the UK officially moved into its long-expected technical recession, which sparked some concern for domestic investors. Disappointing inflation data in the US was

largely shrugged off in equity markets by the sheer excitement of AI, as well as the US economy continuing its strong economic growth trend.

Bank of England hints that interest rate cuts are coming…

but not quite yet

• The UK officially moved into a technical recession – defined as two

consecutive quarters of falling national output – at the end of 2023.

The Office for National Statistics (ONS) reported that UK gross domestic

product (GDP) declined by a larger-than-expected 0.3% in the fourth

quarter, following a fall of 0.1% in the third quarter. Although this caused

some concern for local investors, Bank of England (BoE) Governor Andrew

Bailey said he expects this recession will be “shallow” and short-lived.

• UK consumer price index (CPI) inflation remained at 4% in January.

Economists had expected a small increase to 4.2%, meaning it was a softer

reading than predicted and reaffirmed hopes of meeting the BoE’s 2% target.

• The BoE’s decision to maintain interest rates at 5.25% in February, a 16-year high, was no surprise. However, the decision wasn’t unanimous, as varying Monetary Policy Committee (MPC) members voted in different directions, with some preferring to increase the rate by 0.25% and another member opting to reduce it by 0.25%.

• The ONS reported that annual growth in regular earnings, excluding

bonuses, was 6.2% in the fourth quarter of 2023, while pay rises, including

bonuses, reached 5.8%. Economists had expected 6.0% and 5.6%,

respectively. A strong jobs market and wage growth will likely make the

MPC apprehensive about cutting interest rates too soon.

China fighting an uphill battle to economic recovery

• China continued to fight deflationary pressures in January, adding to

uncertainty surrounding its economic outlook, with prices having fallen

at the fastest rate in 15 years. CPI inflation declined 0.8% year-on-year

for January, which marked the fourth straight month of declines and

the sharpest contraction since 2009, after the Global Financial Crisis.

The inflation rate was dragged down by falling food prices, which

dropped by 5.9% year-on-year.

• China did report some encouraging economic data in terms of increased

revenue. Revenue from tourism during the Lunar New Year holiday surged

47.3% year-on-year and surpassed 2019 levels. Domestic tourism spending

hit 632.7bn yuan (£69.7bn), according to government figures, thanks to a

domestic travel boom amid a longer-than-usual break.

• However, we are still seeing a continued trend that foreign direct investment (FDI) into China last year increased by the lowest amount since the early 1990s. China’s direct investment liabilities, a broad measure of FDI, rose by $33bn in 2023, down 81.7% from 2022, according to the State

Administration of Foreign Exchange.

US economy proves too strong for its own good, quashing hopes

of earlier interest rate cuts

• US CPI inflation declined to 3.1% in January, down from 3.4% in December,

but higher than the 2.9% reading economists expected. This was a

disappointing figure at the headline level.

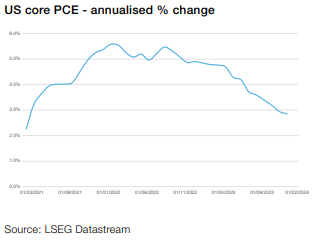

• However, the Personal Consumption Expenditures (PCE) index – the

preferred inflation measure of the Federal Reserve (Fed) – increased by

2.4% in the year to January, down from 2.6% in December. This would have

helped reassure the Fed that inflationary pressures were easing. The core

PCE index, excluding food and energy costs, showed prices rose 2.8% in

the year to January, down from 2.9% a month earlier.

• Despite the positive PCE inflation news, the US jobs market appeared far

too strong for the Fed to consider cutting interest rates just yet. The US

Labor Department reported that employers added 353k new jobs in January taking the unemployment rate to 3.7%, still close to the 50-year low.

• The most disconcerting feature of the jobs report for the Fed was the

strength in worker pay, as average hourly earnings jumped by a surprisingly strong 0.6%. That was the fastest increase in two years, lifting the year-over-year increase to 4.5% from 4.3% in December. This is not the direction the Fed wants to see, as it views taming wages as a critical step in wrestling inflation down to its target.

Summary

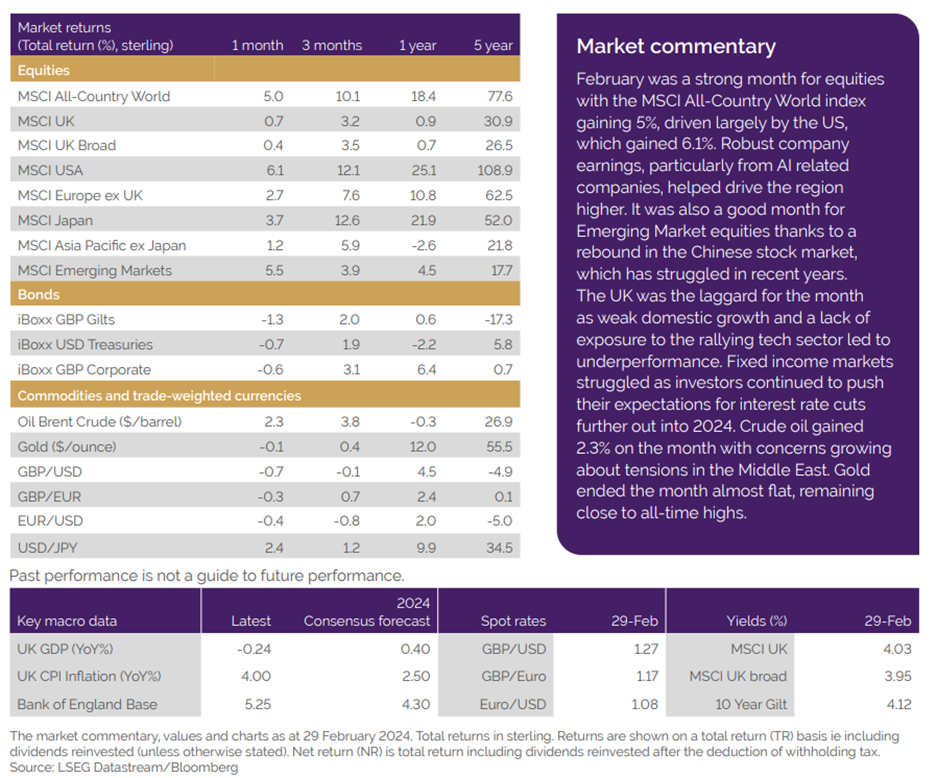

As mentioned, it paid dividends to be an equity investor in February. Although economic data across the globe was somewhat mixed, investors in Western markets were again swept up in the AI craze. China was the surprise package for the month, however, with indices rallying due to more targeted stimulus measures from the government. Despite this, Chinese equities remain at 20+ year lows against broader equities. The mood music in the region is still gloomy, as overseas investment expanded at the slowest pace in 30 years in 2023, although GDP did grow by 5%.

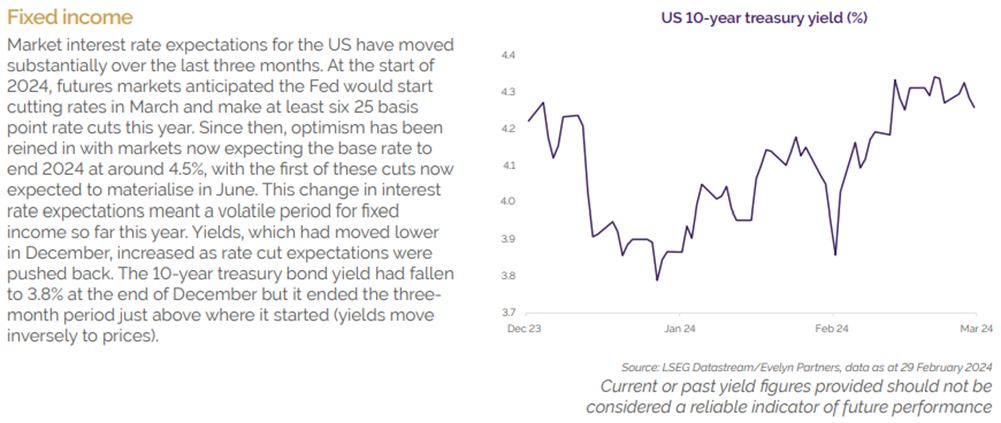

Turning to bonds, the outlook turned negative on rate cuts, with the yield on the ten-year UK government bond (gilt) rising from 3.79% at the start of February to 4.12% by the end of the month, and with the ten-year US Treasury yield increasing from 3.92% to finish the month paying 4.26%. The outlook for high-quality investment grade bonds continued to improve, as February saw over $150bn in new issuance in the US, a record-breaking amount.

Away from equities and bonds, property and infrastructure both fell in value for the month. These assets are particularly sensitive to shifts in interest rate expectations and fell victim to the conclusion from the market that interest rate cuts may not come as quickly as previously hoped, especially in the US.

Please check in again with us soon for further relevant content and market news.

Chloe

08/03/2024