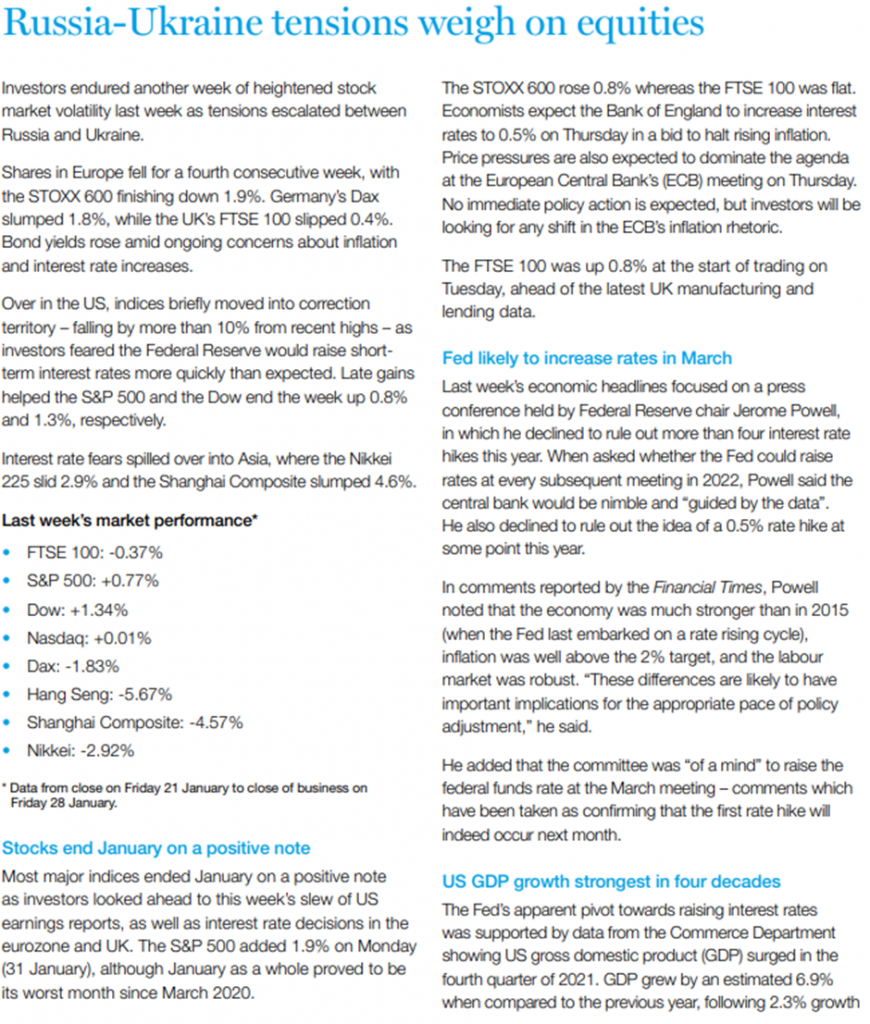

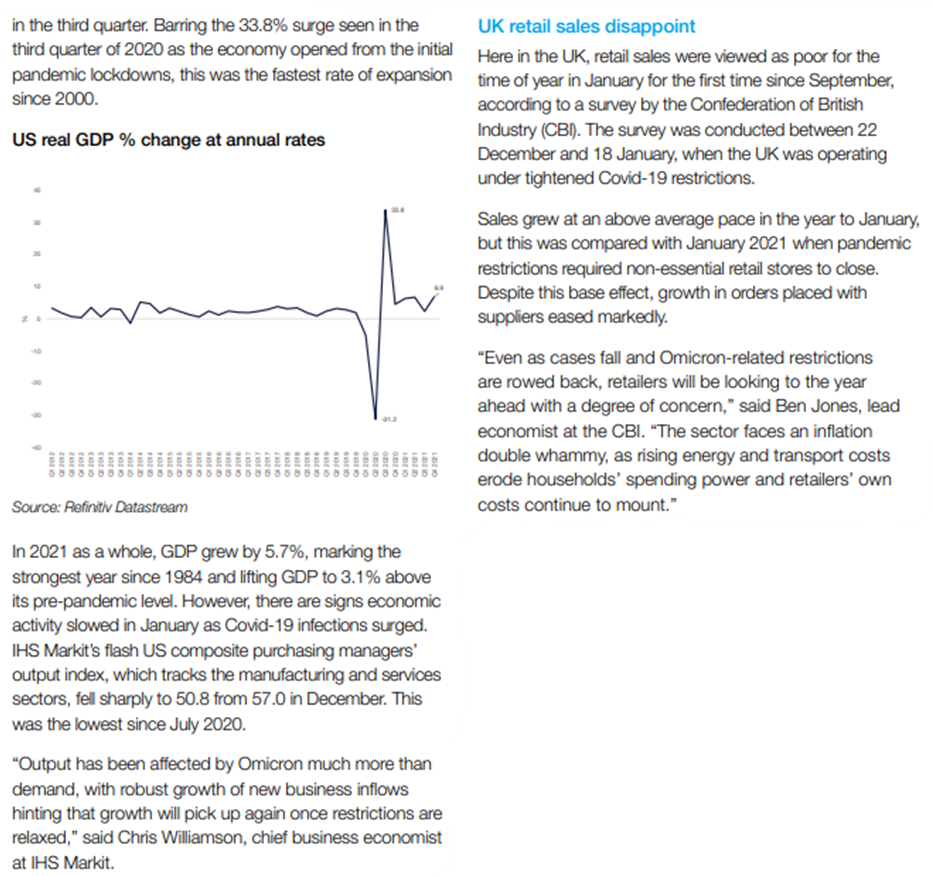

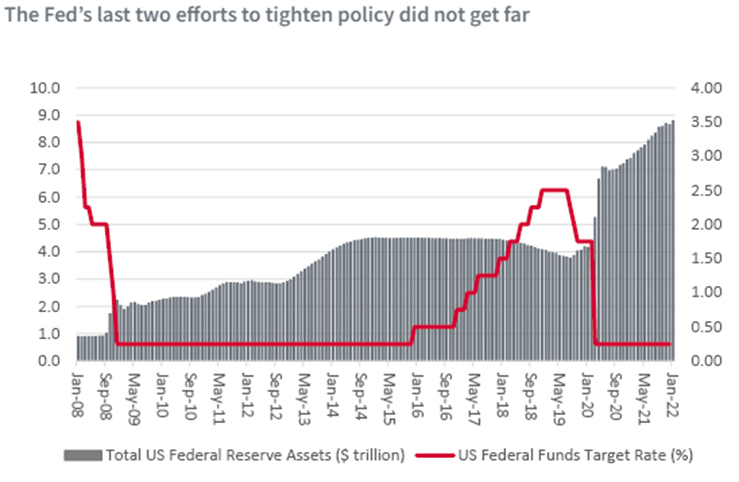

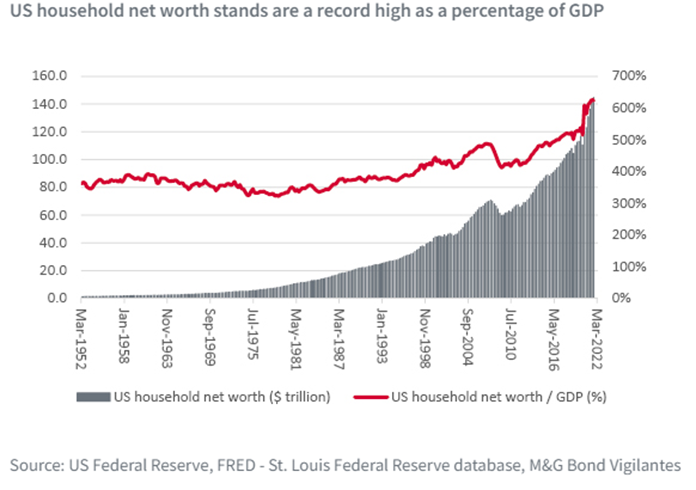

Please see below report received from BNY Mellon Investment Management yesterday afternoon, which sets out to explore some of the key drivers behind the persistent gender-investment gap from the perspective of those who currently invest, those who don’t, and the investment industry itself.

We set out to explore some of the key drivers behind the persistent gender-investment gap from the perspective of those who currently invest, those who don’t, and the investment industry itself.

If women invested at the same rate as men, there would be at least an extra:

$ 3.22 trillion of assets under management from private individuals today

$ 1.87 trillionof additional capital into Responsible Investment

We found that if women invested at the same rate as men, there would be at least an extra $3.22 trillion of assets under management from private individuals today. Perhaps more important, our research also reveals that women are more likely to make investments that have positive social and environmental impacts, meaning that there would be an influx of $1.87 trillion of additional capital into Responsible Investment if women invested at the same rate as men.

Three key barriers to higher levels of female participation in investing:

1. Confidence crisis

Globally, just 28% of women feel confident about investing some of their money.

2. Income hurdle

On average and globally, women think that they need $4,092 of disposable income each month – $50,000 per year – before [they can begin] investing some of their money.

3. High-risk investment myth

Almost half of women (45%) say that investing money in the stock market – either directly or in a fund – is too risky for them. Only 9% of women report that they have a high or very high level of risk tolerance when it comes to investing; 49% have a moderate risk tolerance; and 42% have low risk tolerance.

Women tend to feel less confident about investing than savings, property or pensions. In our report, we explore the reasons why more women aren’t investing and how the investment industry can evolve to support more inclusive investment.

1. Why women don’t invest

Women are less likely to invest than men. This gender-investment gap is a global issue, which limits women’s financial futures and their capacity to influence a better future for the planet. Over half of women believe that it’s important that more women invest to give them the choice to support companies and causes they agree with (53%) and to give them more influence over business and its environmental and social impact (52%).

In order to understand why women don’t invest at the same rate as men, and to explore what we in the industry can do to raise levels of female participation, we interviewed 8,000 men and women worldwide.

Our research reveals that the investment industry must tackle three key investment barriers to encourage more women to invest:

Engagement Crisis

The investment industry is failing to reach, appeal to, and engage women to the same degree as men. Globally, as few as one in 10 women feel they fully understand investing, and less than a third of women (28%) feel confident about investing some of their money.

With so few women comfortable investing any of their money, the urgent need for better communication and engagement is clear. Across key aspects of financial decision-making, investment is the area where the fewest women feel confident, compared to making decisions around savings, property and pensions.

Income Hurdle

On average and globally, women believe they need $4,092 of disposable income each month—almost $50,000 per year—before they would consider investing any of it. In the US, for example, on average women believe that they need over $6,000 of monthly disposable income—just over $72,000 per year—before they can start investing.

Clearly, this is unrealistic, especially given the fact that over a quarter of women (27%) describe their financial health as poor or very poor. For the investment industry, overcoming this misconception and explaining that only a small amount of money is needed to start investing should be a key focus.

Overcoming the income hurdle

Despite the widespread belief that you need large amounts of spare money to start investing, even a small investment habit of setting aside a few dollars each month can really pay off over time. For example, if you began 10 years ago investing $30 a month in the S&P 500 Index, your portfolio could be worth over $8,000 today, of which less than half would be money that you put in yourself.

2. How women investing can change the world

Higher levels of female participation in investment could not only have a huge impact on women’s lives but also on the world at large, as women are more likely to invest in causes that they believe in, such as protecting the environment.

What then could encourage more women to invest? Our study shows that women across the world are motivated by the impact that their investments could have. More than half of women (55%), for example, would invest (or invest more) if the impact of their investment aligned with their personal values, and 53% would invest (or invest more) if the investment fund had a clear goal or purpose for good. Two-thirds of women who currently invest (66%) try to invest in companies they like and that support their personal values.

This drive to align investments with values seems to be stronger among those with children: three-quarters of parents—both men and women—who currently invest say that they prefer to invest in companies that support their personal values, compared with 59% of adults who do not have children.

Responsible Investment (RI) means investing for a better future; a more sustainable, diverse, and equitable future. RI covers a spectrum of investing styles, including exclusionary screening, ESG integration, sustainable investing and impact investing. ESG integration is the systematic and explicit incorporation of ESG factors into financial analysis and investment decisions to better manage risks and improve returns. Impact investing goes a step beyond ESG investing. It is the practice of investing with the dual objective of generating a positive, measurable and intended social or environmental impact, as well as a financial return.

Investment Shift

The profile of those who invest is changing, and with it there is a shift in focus and values. Our data shows that older men – traditionally the “typical” investors targeted by the investment industry – are less focused on impact investing and aligning their investments with their values. While 69% of young women (aged 18–30) who currently invest select their investments based on their impact, this is true of only a third (33%) of older men (aged over 50). And more than seven in 10 women under 30 (71%) prefer to invest in companies that support their personal values, compared with 54% of men over 50.

3. Building an inclusive investment industry

If it’s possible to raise the participation rate of women investing, it could increase their personal prosperity and could have a beneficial influence on environmental and social issues.

Making investing more accessible to women isn’t just about ensuring they have the right technology, but also inclusively equipping everyone with the knowledge, skills, and fostering the motivation to engage with investing. This requires a significant cultural shift within the industry—not only in the way that products are developed and marketed but also in the diversity of the investment industry itself.

We asked asset managers – representing nearly $60 trillion of assets under management – for their insights on the key challenges for gender-inclusive investment and for their thoughts on how the industry can change to encourage more women to invest. Their answers reveal the extent to which the investment industry is currently oriented toward male customers and help identify ways in which financial products and messaging could be reshaped to attract and engage more women.

An industry with men in mind

Currently, nearly nine in 10 asset managers (86%) admit that their default investment customer is a man, and three-quarters of asset managers (73%) state that their organization’s investment products are primarily aimed at men, suggesting that they focus on the benefits and features that generally appeal more to men than women.

As a result, potential female investors are met with language, imagery and messaging targeted mainly at a male customer. This often includes the use of high-risk metaphors, such as those used in extreme sports, and the concept of high performance and achievement as a shorthand for investment success.

The answer to engaging women in investment isn’t found in outdated gimmicks and doesn’t require, for example, the increased use of the color pink—rather, it’s about forming a connection by understanding what motivates women to invest and how they like to be communicated with.

If the industry can re-think the language around investing, there’s a significant opportunity to affect how much women invest: 37% of women said that if investment language were easier to understand, it would influence them to invest, or to invest more than they currently do. However, the key takeaway is that the language which describes financial products should not only be simpler, and avoid jargon, but also be more clearly aligned to women’s long-term goals and values.

As increasing health standards mean that today’s women need to plan for what might be a 100-year lifespan, women are motivated to invest by thinking of their long-term financial prosperity, independence, and the impact their investments can have. Products packaged to meet these needs and address these interests, clearly communicated in straightforward language, should go a long way to increasing women’s investment.

What Women Want: Investing in Independence

As discussed earlier in the report, women value responsible investing and investments aligned with their personal values. They are also motivated to invest by a range of other factors, with financial independence topping the list. The investment industry, therefore, has a key opportunity to appeal to women by focusing on messaging around financial independence.

Almost two-thirds of women (63%) believe that it’s important that more women invest to provide for themselves in retirement, and six in 10 women believe that it is important that more women invest in order to give themselves greater financial independence. This rises to eight in 10 women in India (80%) and the US (79%). Historically, the industry has marketed wealth products to women based on financial provision for their families; today, however, we find that investing in independence is more important than financing dependents. Motivators around retirement and independence are rated even more highly than growing a financial legacy for their family, for example (cited as important by 57% of women).

4. Changing investment, changing the world

The amount of wealth controlled by women globally is disproportionately small, but ever-growing and our research reveals that more women are looking to invest. This could bring benefits not only for those who invest but also for women everywhere, and for the world as a whole. However, women are being held back by lack of confidence, concerns about risk, and an industry oriented toward men.

It is up to us – the investment industry – to lead the change, by educating, inspiring, and including more women in all that we do. The traditional stereotype of the person who is interested in investing – the wealthy older man – is outdated and needs to be dismissed. Young women are interested in investing too, but they need to be empowered to do so. The face of investment is changing – and the industry needs to evolve too. Empowering women to invest can come about by bringing the world of investment to them – by providing the knowledge and skills they need and realigning the messaging to promote conversations both inside and outside of the industry that speak to their motivations, be they financial, societal, or both.

Responsible investing allows women to champion causes they believe in effectively by using their money to directly help reach social and environmental goals. A greater focus on this type of messaging and on the wider benefits of investing should help to attract more women.

Greater diversity within the industry should also help to achieve higher levels of female participation and ultimately investment; but in order for a meaningful industry shift to take place, both women and men will need to help drive change.

If we all work together, we can achieve the goal of making investment more inclusive, for the benefit of all.

The time to act is now. The investment industry needs to be more inclusive, find a better way to engage with women, make investing more accessible and close the gender-investment gap. Because more women investing will benefit everyone: society, the investment industry and the planet.

Please check in again with us soon for further relevant content and news.

Chloe

03/02/2022