Please see below, an update from Blackfinch regarding their approach to investments going forward in 2022, received yesterday evening – 15/02/2022

Markets have been volatile so far this year as the prospect of higher-for-longer inflation and rising interest rates have weighed on investor sentiment. These risks have been most pronounced in company valuations, which last year reached historically high levels in certain stock market sectors.

In general, when interest rates rise, investors can look elsewhere for returns instead of buying richly valued shares. What we have seen in 2022 is a reversion to more normal valuations as investors rotate away from the returns potential available from ‘growth’ stocks into more traditional ‘value’ stocks trading at levels below what they are believed to be worth.

It’s important for us to review the fundamentals of the companies we invest in before making a significant switch into other areas of the stock market. For example, the US is typically known as a growth market due to its dominant technology sector. These companies are often high quality, with investors required to pay higher valuations based on more attractive prospects. Currently, large cap companies in the S&P 500 index are reporting earnings for the fourth quarter of 2021. For the earnings season to date, 356 companies have released updates, and aggregate sales growth year-over-year has been 16%. On the same basis, earnings have increased by an even bigger 27%. However, this year the S&P 500 has fallen almost 6% (for sterling-based investors). This disconnect between strong fundamentals, but declining stock prices is due to the deflation in valuations that has driven stock markets this year.

Looking at individual companies, even though earnings have been strong, stock prices have still declined. Apple, Microsoft and Alphabet announced results that beat expectations – Apple was the standout performer after generating $124bn of revenue in a single quarter – yet their share prices are all down so far this year. We still hold these companies in the portfolios through our S&P 500 index fund.

Although this has declined in 2022, we view the underlying fundamentals of the companies as highly attractive and have retained our exposure to this fund.

Our portfolios also hold quality-based strategies in Europe, such as Premier Miton European Opportunities and Liontrust Special Situations. In much of the same way as the US market has fallen, both funds are down so far this year. However, on a longer time horizon, both have delivered top quartile performance compared to other funds in their respective sectors. We believe that quality companies with competitive advantages and growth potential still offer investors attractive returns over a long-term holding period.

We also allocate assets to traditional value sectors to diversify our portfolios. The UK offers higher income from dividends when compared to other developed markets. However, although value sectors have outperformed this year, we have avoided changing our allocations to overweight. For example, with the price of crude oil rallying to an eight-year high, profitability in the Oil & Gas sector has been raised, and therefore the sector looks attractive in the short term. However, as we believe the Oil & Gas industry is in structural decline, we would not feel comfortable holding significant exposure to these assets over a longer period.

The risks of inflation and rising interest rates will, no doubt, have an impact on returns for investors this year. However, looking further ahead, we still view holding quality companies with attractive growth potential as the best drivers of long-term returns. We will continue to update you on our portfolio activity as the economic outlook progresses.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 15/02/2022.

US inflation hits highest level in 40 years

Stock market volatility continued last week as fears about tighter monetary policy and a Russian invasion of Ukraine weighed on investor sentiment.

In the US, the technology-heavy Nasdaq ended the week 2.2% lower and remained in correction territory, down 15% from its recent peak. The S&P 500 declined 1.8% after the latest inflation data showed US consumer prices surged in January to their highest level since 1982.

Strong corporate earnings boosted shares in Europe, with the STOXX 600 rising 1.6% and Germany’s Dax gaining 2.2%. The FTSE 100 added 1.9% after data showed the UK economy grew by 7.5% in 2021.

In China, the Shanghai Composite surged 3.0% after economists said the worst of the country’s regulatory crackdown was over.

Russia-Ukraine tensions rattle markets

Stocks started this week in the red as tensions grew between Russia and Ukraine. The FTSE 100 tumbled 1.7% on Monday (14 February) with travel stocks worst hit.

The STOXX 600 fell 1.8% and Germany’s Dax lost 2.0%. Oil prices hit their highest levels in more than seven years amid concerns an invasion of Ukraine could disrupt supplies and spark retaliatory sanctions on Russia.

US shares dropped sharply on news the US is closing its embassy in Kyiv and moving diplomats to Western Ukraine. The S&P 500 managed to largely recover from the sharp selloff and ended Monday 0.4% lower, with energy stocks suffering the largest falls.

The FTSE 100 was up 0.8% at the start of trading on Tuesday, as investors digested the latest labour market data from the Office for National Statistics. Unemployment fell slightly to 4.1% in the fourth quarter of 2021 from 4.3% in the third quarter, while inflation-adjusted regular pay (excluding bonuses) fell by 0.8% year-on-year.

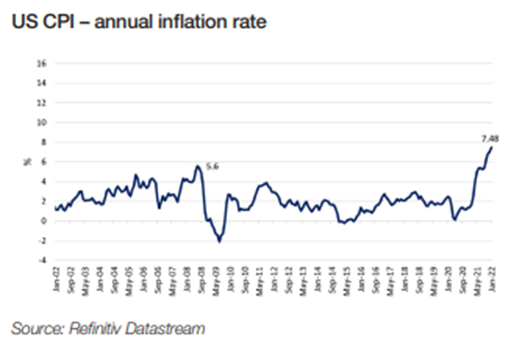

US consumer prices surge 7.5%

Soaring demand and lack of supply pushed US inflation to its highest level in 40 years in January. Consumer prices rose by 7.5% from a year earlier, and by a bigger-thanexpected 0.6% from the previous month, according to the Bureau of Labor Statistics.

Price rises for food, electricity and shelter were the largest contributors to the increase. Food prices rose by 0.9% month-on-month in January, following a 0.5% rise in December. Energy prices also rose by 0.9% in January. Core inflation, which strips out food and fuel, rose by 6.0% on an annual basis, driven by a 40.5% surge in the prices of used cars.

Concerns about inflation were evident in the University of Michigan’s preliminary gauge of consumer sentiment, which fell to its lowest level in more than a decade in early February. The index dropped to 61.7 from a final reading of 67.2 in January.

Richard Curtin, chief economist for the University of Michigan’s surveys of consumers, said the declines were driven by weakening personal financial prospects, with higher inflation spontaneously cited by one-third of all consumers. Nearly half expected declines in their inflation-adjusted incomes during the year ahead.

UK GDP rebounds from pandemic slump

UK gross domestic product (GDP) grew by a betterthan-expected 1.0% in the final quarter of 2021 as the hit from Omicron proved to be smaller than feared. GDP slipped by 0.2% in December, after growing by 0.7% the month before, as people worked from home and avoided Christmas socialising, according to the Office for National Statistics. This was better than the 0.6% contraction expected in a Reuters poll.

For 2021 as a whole, GDP grew by 7.5%, marking the biggest annual rise since 1941 and rebounding from the 9.4% plunge in 2020. However, economists are predicting slower growth in 2022 as rising inflation and soaring energy prices put further strain on households. The Bank of England recently cut its GDP growth forecast for 2022 to 3.75% from 5.0%.

Europe lowers growth forecast

The European Commission also lowered its outlook for economic growth in the eurozone to 4.0% in 2022 and 2.7% in 2023, down from 4.3% and 2.4% previously. European economic commissioner Paolo Gentiloni said multiple headwinds had chilled Europe’s economy this winter, including Omicron, soaring energy prices, and persistent supply chain disruptions. “With these headwinds expected to fade progressively, we project growth to pick up speed again already this spring,” he added.

Inflation is expected to reach 3.5% this year, higher than the European Commission’s November forecast of 2.2% and well above the European Central Bank’s 2.0% target. Next year, inflation is forecast to ease to 1.7%.

“Price pressures are likely to remain strong until the summer, after which inflation is projected to decline as growth in energy prices moderates and supply bottlenecks ease. However, uncertainty and risks remain high,” Gentiloni said.

China services activity slows

Activity in China’s services sector grew at the slowest pace in five months in January as the government introduced measures to contain localised cases of Covid-19. The Caixin / Markit services purchasing managers’ index fell from 53.1 in December to 51.4 in January – the lowest since August, although still above the 50-point mark that separates growth from contraction. Input costs rose at a sharper rate in January from the previous month, and confidence about the year ahead slipped to a 16-month low.

The data has increased expectations that China’s policymakers will introduce further support for the economy this year, rather than moving towards the more hawkish stance adopted by central banks in the West.

Please continue to check back for our latest blog posts and updates.

Please see Brooks Macdonald’s latest Weekly Market Commentary below:

Inflationary pressures clash with the risk of a Ukraine conflict, creating volatility in the bond market

Worsening geopolitical headlines late in the US trading session on Friday caused sentiment to plunge. Bond investors, in particular, were struggling to balance the US inflation/interest rate picture, which has driven yields higher, with the Ukraine crisis which could trigger a flight to quality. At the moment, the flight to quality trade is winning out with the US 10-year Treasury yield back to 1.9% after hitting 2% last week.

Late in the Friday trading session, the US warned of an imminent attack from Russia on Ukraine, with detailed invasion plans pointing to a military incursion starting on Wednesday. The immediate reaction to this news was a rapid fall in risk assets, a rally in government bond yields and a spike higher in the oil price. European equities are playing catch up this morning with European indices ranging from 2-3% down as risk appetite indiscriminately affects equity market sectors. Over the course of the weekend there was no further escalation however the market is now expecting an imminent breakout either to the upside or downside. With the US and NATO allies ready to deploy punitive sanctions, and the real human cost from a conflict, the stakes are undoubtedly high over the next week.

Central bankers fine tune their guidance with the major central bank meetings out of the way for February

Before the Ukraine headlines late on Friday, the main event of last week was the US Consumer Price Index release which showed a headline inflation rate of 7.5% year-on-year. Federal Reserve (Fed) speakers drove much of the market narrative pre and post the release, with President Bullard garnering particular attention for his discussion of the possibility of an inter meeting hike, which was later talked down by other governors. The European Central Bank (ECB) meanwhile tried to calm bond market nerves around an imminent tightening in Euro Area monetary policy, with President Lagarde keen to stress that the ECB had little appetite for a widening of peripheral European sovereign bond yields.

The minutes from the latest Federal Reserve meeting will be released this week and all eyes will be on a series of high profile central bank speakers

With the minutes from the Fed’s latest meeting being released and a series of high-profile central bankers speaking, this week will likely be dominated by central bank speak, particularly as the banks need to incorporate geopolitical risks into their forecasts and guidance.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below article received from Tatton Investment Management on Friday evening, which provides a detailed update on markets and global economies.

Stock markets around the world continued their volatile trading pattern over the past week, although compared with January, trending slightly up rather than down. Bond markets, on the other hand, continued to retreat as yields continued to rise. This type of market action has now become characteristic for capital markets this year, as they experience their very own climate change, now that the coronavirus appears to have lost its lethal impact on the majority of the population.

We have written at length about the U-turn of the central banks, which have swung from downplaying (if not ignoring) inflationary pressures to seemingly becoming more concerned about fighting inflation than ensuring the continued wellbeing of the economy. This week continued very much in the same vein, but several new data points are beginning to offer more clues into the direction of travel beyond central bank action.

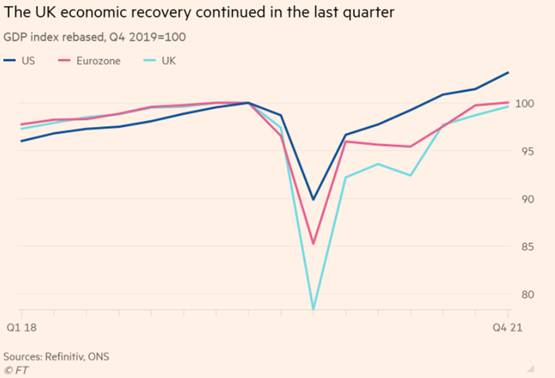

In the UK, GDP growth of 7.5% was reported for 2021, which put the economy roughly back to where we were before the pandemic started back, this time two years ago. The chart below illustrates how the V-shaped recovery has not only taken place in the UK, but also Europe, while the US is the outlier that has surpassed the starting level. As we know, this was substantially achieved by larger and less targeted handouts by the US government that resulted in a significant consumer demand boost. The increased levels of inflation are, to a large extent, the undesired side effect of this necessary, but hard to fine-tune, bridging support for the affected population.

The latest monthly inflation data for the US was therefore keenly awaited and, when it came in higher than hoped at (also) 7.5%, US stocks sold off as they quickly priced in that the US Fed will tighten and raise rates even faster than previously anticipated. Looking at the granular inflation data though, the strong market reaction felt counterintuitive, given all the major inflation-driving components of last year had continued to decline in their contribution, especially durable goods (the things we were most keen to order during the pandemic). What may have caused the negative surprise is that inflation appeared to have started ‘leaking into’ areas broadly unaffected by supply chain issues, and which are seen as more ‘sticky’ (not tending to reverse prices easily), especially the services sector.

On the other hand, there was some good news from the data on wage rises. While overall US wage growth has picked up to an uncomfortable 5%, this is very much concentrated among the very lowest earners. While this means wage growth is not sustained across the whole of the labour market, it also suggests the forces of capitalism are currently addressing the problem of inequality that has become such a divisive force – not just for American society.

Given bond yields are now broadly back to where they stood before the pandemic, equities have not in fact performed too badly so far this month. It appears markets are getting their collective heads around the ‘investment climate change’, and one could argue that by now quite a lot of rising yield headwind has been priced in without causing the substantial ‘damage’ the doomsayers had predicted.

This may be, because the inflation headlines this week were flanked by more positive data from the real economy, which would also explain why implicit long-term growth expectations as expressed by certain parts of the bond markets (ten-year yields, ten-year forward) communicated increasing optimism as they did not mirror the negative vibes from the flattening of the yield curve as they usually do, but went the other way.

To this end, January monetary data from China indicated that the leadership there had once again opened the credit stimulus taps – which has in the past resulted in growth stimulus spilling over into the rest of the global economy. On the trade side, volumes improved in the stream of goods with China which should reduce supply chain issues and stimulate the Eurozone economy.

In the wider world of emerging markets, we may see similar central bank loosening tendencies as in China, given they have already been in a tightening cycle since early last year and are therefore far more likely at the end of it compared to western central banks. This would add to China’s demand stimulus and bring positive growth impulses to global trade (we touch on this in this week’s article on commodities).

In Europe and the UK, strong 2021 growth came about despite significant reductions in inventories. This means that the rebuilding of those inventories in 2022 should carry some of the 2021 demand boost into GDP growth this year. Most surprising, perhaps, was data showing that despite all post-Brexit trade regulation frictions, the trade volumes between continental Europe and the UK are returning to pre-Brexit levels. As observed in the past, when Europe’s economy does well from resurgent global demand, so does the UK and, with the trade linkage seemingly healing, this is good news for domestic growth prospects.

Of course, not all is well and there are plenty of dark clouds still on the horizon, be they the cost-of-living challenge from energy prices reducing aggregate consumer demand, or Russia’s President Putin still threatening to extend the fossil fuel shortage that is now the main driver of inflation. However, the overall mix of data this week provided positive evidence that the current economic slowdown may not be as deep-seated as feared, and that capital markets appear to expect subsiding inflationary pressures will also lower the pressures on central banks to tighten too fast and too soon. The Bank of England’s chief economist’s remarks this week to that end were positively received.

Judging from the significant relative moves between different sectors and investment styles like Growth and Value, the message of change in the investment climate appears to be getting through. Positive returns may no longer be as readily available across all asset classes, sectors and styles, but for those who analyse, search and skilfully anticipate the progress of this uncharted post-pandemic economic cycle, there should be ample opportunities (For more, please read our article on the dynamics of small cap equities).

We endeavour to publish relevant content and news on a regular basis, so please check in again with us soon.

Please see below an article published by Invesco on Wednesday (09/02/2022) and received yesterday (10/02) afternoon detailing their current views on Central Bank’s policy changes:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please find below, the Daily Investment Bulletin update received from Brooks Macdonald this afternoon – 10/02/2022

What has happened

Risk appetite surged yesterday with a broad rally across most major sectors as central bank speak pushed back against the market’s aggressive interest rate pricing. Technology has been a particular beneficiary of this rally and yesterday’s session is another sign that the fate of the sector is showing signs of decoupling away from the grind higher in US bond yields.

Central bank speak

After the comments from Bank of France President Villeroy on Monday, suggesting that monetary tightening expectations in the market may have gone too far, bond markets began to stabilise after a choppy few days. Yesterday we heard from Fed voting member Mester of the Cleveland Fed, Mester said that she didn’t see a compelling reason to raise rates by 50bps when lift off occurs (widely expected to be in the March meeting). In the UK, the Bank of England’s Chief Economist, who pushed back against market pricing at the end of last year, said that ‘I worry that taking unusually large policy steps may validate a market narrative that bank policy is either foot-to-the-floor on the accelerator or foot-to-the-floor with the brake.’ European bond markets reacted positively, with German bunds finally ending their run of 11 consecutive days of yield rises.

US CPI

Today sees the week’s main event, the latest US inflation numbers. Most central banks have stressed the humility required around forward guidance given the uncertainties around inflation and growth for the rest of this year. Today’s CPI number will be closely watched to see if the month-on-month path of inflation is starting to slow. Consensus is expecting US CPI to increase by 0.5% over the last month (reaching 7.3% year-on-year) and for US Core CPI to also rise by 0.5% over the month and 5.9% over the last year. Both Core and headline CPI grew by 0.6% in December so if the consensus is achieved, this would show a slowing of the inflation rate. There is room for caution however, 0.5% month-on-month inflation is still a hefty increase and there may be signs of distortion due to the Omicron variant.

What does Brooks Macdonald think?

Few are expecting a ‘turn’ in inflation data until April/May of this year when the month-on-month figures are expected to start moderating. Should we see inflation come in to the downside today, the current rally may gather further steam. That said, we should be very conscious of impacts from the Omicron variant distorting the information we can garner from one data release in isolation.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

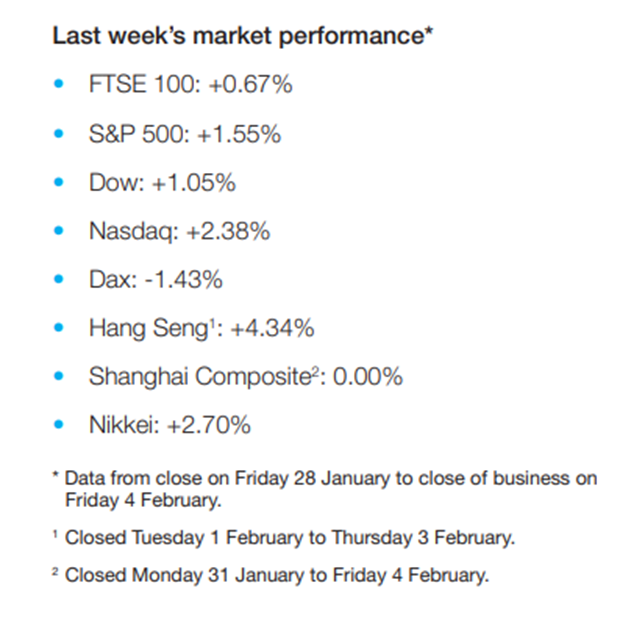

Please see below, Brewin Dolphin’s latest ‘Markets in a Minute’ update, examining last week’s global market performance – Received late yesterday afternoon – 08/02/2022

Stocks mixed as US earnings season ramps up

Equities were mixed last week as investors weighed mostly positive US earnings reports against the threat of rising interest rates.

The pan-European STOXX 600 fell 0.7% after European Central Bank (ECB) president Christine Lagarde declined to rule out an increase in interest rates this year. Germany’s Dax fell 1.4% and France’s CAC 40 slipped 0.2%. The UK’s FTSE 100 edged up 0.7%, despite the Bank of England’s (BoE) decision to hike the base interest rate for a second month in a row.

Over in the US, the S&P 500 finished a volatile week up 1.6% as investors digested fourth quarter earnings reports from big technology companies including Alphabet (Google’s parent), Amazon, and Meta (formerly Facebook). A surprise jump in US payrolls pushed the yield on the ten-year US Treasury note to its highest level since 2019.

China’s financial markets were closed last week for the Lunar New Year.

Tech selloff drives US stocks lower

US equities started this week in the red, with the S&P 500 and the Nasdaq down 0.4% and 0.6%, respectively, on Monday (7 February) following a selloff in big tech names. Investors are set to receive another batch of fourth quarter earnings in the coming days, including Disney, Pfizer and Coca-Cola. Meanwhile, the consumer price index, due on Thursday, is expected to add further weight to the case for hiking interest rates.

Germany’s Dax managed a 0.7% gain on Monday, despite data showing the country’s industrial output fell by 0.3% month-on-month in December, driven by supply chain bottlenecks and a decline in construction. In the UK, house prices rose 0.3% in January from the previous month, the slowest pace since June. Halifax said house price growth is expected to slow considerably over the next 12 months as households grapple with the cost-of-living crisis.

At the start of trading on Tuesday, the FTSE 100 was up around 0.6% as the latest BRC-KPMG survey showed total retail sales increased by 11.9% in January from a year ago.

BoE increases interest rate to 0.5%

Last week, the BoE’s monetary policy committee voted to increase the base interest rate by 25 basis points to 0.5%. This marked the first back-to-back rate hike since 2004. It came after data revealed UK inflation surged to a 30-year high in December amid rising energy costs and ongoing supply chain issues. The BoE also raised its inflation forecast to an April peak of 7.25%, which would be the highest since 1991.

The Bank warned that UK households would see their inflation-adjusted post-tax disposable income fall by 2% this year because of higher energy bills, taxes, and comparatively weak earnings. This would be the biggest fall ever recorded. Noting that higher costs would depress consumer spending and economic growth, the Bank cut its gross domestic product (GDP) growth forecast for 2022 from 5.0% to 3.75%.

The BoE’s report came shortly after Ofgem said households on default variable gas and electricity tariffs and those with prepayment meters would see their bills rise by around £700 in April, a 54% increase. In response, chancellor Rishi Sunak announced households would get £200 off energy bills in October, to be repaid over five years. Those in council tax bands A to D will also receive a £150 rebate.

ECB ‘much closer’ to inflation target

The odds of the ECB hiking interest rates this year have increased after Lagarde said the bank was “getting much closer” to hitting its target on inflation. Lagarde did not explicitly rule out increasing interest rates, but instead said there was consensus among ECB policymakers about the decision to keep rates unchanged.

“Compared with our expectations in December, risks to the inflation outlook are tilted to the upside, particularly in the near term,” Lagarde said.

She added: “We are all concerned to take the right steps at the right time, and I think there was also a concern and a determination around the table not to rush into a decision unless we had a proper and thorough assessment based on data and the analytical work that will take place in the next few weeks.”

Lagarde’s comments have been described as hawkish, and interpreted as signalling a shift to tightening monetary policy from March.

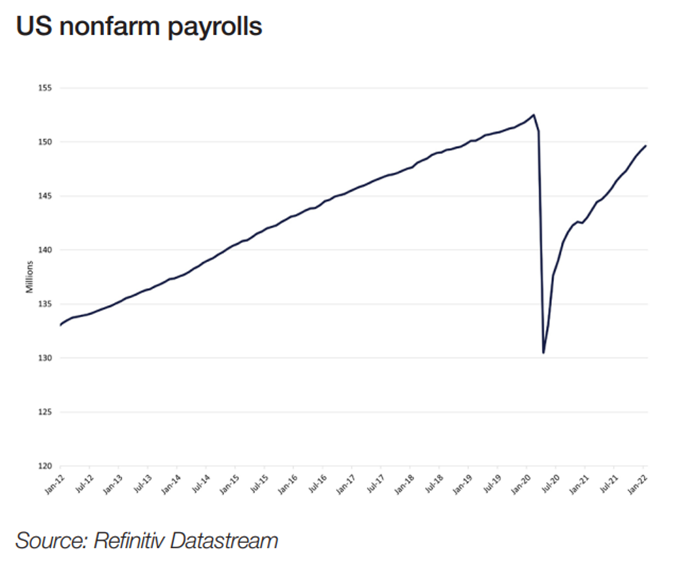

US payrolls beat estimates

US nonfarm payrolls jumped by 467,000 in January despite surging Omicron infections. This was well ahead of the 150,000 increase predicted in a Dow Jones poll, and came a week after the government warned the numbers could be low because of the pandemic.

The Labor Department report also contained sizeable revisions to data from the previous two months. December’s increase was lifted from 199,000 to 510,000, and November’s from 249,000 to 647,000. These changes brought the total for 2021 to just under 6.67 million, the biggest single-year gain in US history.

Earnings also rose sharply by 0.7% from the previous month and by 5.7% on an annual basis, providing further confirmation that inflation is accelerating. The unemployment rate edged higher to 4.0% from 3.9% in December. However, a broader measure of unemployment, which includes people who want to work but have given up searching and those working part-time because they cannot find full-time employment, dropped from 7.3% to 7.1%, the lowest since February 2020.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below this week’s market commentary from Brooks Macdonald received yesterday afternoon – 07/02/2022

Weekly Market Commentary | Thursday’s US data release the key event of the week

07 February 2022

By Edward Park

• Bond market moves and earnings releases spurred further volatility last week • This week’s US Consumer Price Index release will be closely watched for signs of sticky inflation within rental prices • With the European Central Bank’s hawkish tone last week, bond markets interpret the latest governor comments

Bond market moves and earnings releases spurred further volatility last week

Bond markets suffered further swings last week as investors had to price in a more hawkish European Central Bank and Bank of England on top of the large moves already seen in US rate markets. Idiosyncratic risk was also at the fore, with earnings creating volatility not only in the individual stocks but also in largely unconnected companies in the same sector.

This week’s US Consumer Price Index release will be closely watched for signs of sticky inflation within rental prices

Consumer Price Index (CPI) data is always important, however with the Federal Reserve (Fed) clearly data dependent, US CPI on Thursday is likely to be the main event of the week. This release could be particularly interesting as Core CPI is expected to slow moderately on a month-on-month basis, however the year-on-year number looks set to increase further, with analyst expectations at 5.9% on the core number and 7.3% on the headline1. In 2021, we saw a large number of upside beats to CPI and at times of transition, estimates are particularly prone to error. In terms of the factors driving the latest release, investors will be trying to sort through pandemic related distortions, supply chain issues and more durable inflation areas such as rents and owner equivalent rents. Rent/owner equivalent rents are closely watched by the Fed as a gauge of the stickiness of inflation across the economy so expect some focus on this.

With the European Central Bank’s hawkish tone last week, bond markets interpret the latest governor comments

Whilst major central bank meetings are now out of the way for the next few weeks, we will have a steady stream of speakers giving their personal views on the future path of policy. Over the weekend, ECB governor Knott suggested that the ECB could hike rates in Q4 of this year, followed by another hike in H1 2023 given his expectation that Euro Area inflation will remain stubbornly high throughout 2022. After last week’s ECB press conference and the more hawkish tilt, markets are already pricing in 50bps of hikes before the end of this year2, so markets are more aggressive than the ECB at the moment.

Bond markets still feel bruised from the rapid change in Fed policy seen over the last quarter and are keen to not be similarly wrong-footed by the ECB. Arguably, the backdrop in the Euro Area is very different to that in the US and Ukraine risks are a far greater factor in the current, elevated, headline CPI numbers. There has been a more constructive tone around Ukraine tensions in recent days. Whether this catalyses an agreement or not will be important for inflation and ECB policy.

Weekly updates like these from Brooks Macdonald help us keep up to date with what is happening within the markets.

Please continue to check back for our regular blog posts and updates.

Please see the below article from JP Morgan, received this morning:

Sustainability, which includes environmental, social and governance (ESG) considerations, has long been a focus for the European investment community, European governments and regulators. In recent years, the European Union (EU) has taken specific legislative actions to encourage the flow of capital towards a sustainable economy, including developing and enacting regulation related to sustainable finance.

The EU Sustainable Finance Disclosure Regulation (EU SFDR), which went into effect 10 March 2021, aims to increase transparency and standardisation within financial products with regards to their environmental and social characteristics and sustainable objectives.

The EU Taxonomy Regulation (EU TR), which went into effect 01 January 2022, provides an additional level of transparency to financial market participants by recognising and outlining six specific environmental objectives. The EU TR supports the EU’s goal of helping capital flow to sustainable finance and green projects.

An EU taxonomy specific to social objectives is currently being developed and a draft report was released by the social taxonomy subgroup of the EU Platform for Sustainable Finance in July 2021. We expect to learn more about the progress of the social taxonomy in the near term. Throughout this article we refer only to the EU TR related to environmental objectives.

It is important for investors to understand the scope of the EU TR. In-scope firms are not required to have binding commitments to make EU TR-aligned investments within their financial products; they are only required to disclose the degree to which their financial products commit to aligning with the EU TR. For example, zero alignment is permitted.

Taken all together, elements of the EU TR and the EU SFDR, along with ESG-related changes to the EU Market in Financial Instruments Directive (MiFID), introduce enhanced levels of ESG-related disclosures. Investors will see the most significant impact by mid-2022.

What is the EU Taxonomy Regulation (EU TR) and why is it important?

The EU TR is the EU classification system for environmentally sustainable economic activities. It translates the EU’s environmental objectives into a clear framework for investment purposes. The EU TR creates a common, standardised language, criteria and due diligence (quality assurance) process related to identifying economic activities that align to recognised environmental objectives.

The EU TR specifies six EU environmental objectives:

Climate change mitigation*

Climate change adaptation*

Sustainable use and protection of water and marine resources**

Transition to a circular economy**

Pollution prevention and control**

Protection and restoration of biodiversity and ecosystems**

*Level 2 standards confirmed as of 9 December 2021. **Level 2 standards under review.

Broadly, an economic activity may be considered “environmentally sustainable” if it meets the following conditions:

Makes a substantial contribution to at least one of the EU’s six environmental objectives

Does not cause significant harm to any of the other EU environmental objectives to which it is not aligned

Meets prescribed minimum ESG safeguards

Meets the “technical screening criteria” set out by the EU TR

In addition, the EU TR mandates a series of disclosures that in-scope financial firms and financial products are required to make with regards to the degree to which their activities and/or investments are aligned to the EU TR.

Who is affected by the EU TR?

The EU TR affects all financial market participants in the EU. Asset managers and financial advisers need to disclose the degree to which they commit to being invested in taxonomy-aligned activities within their financial products. As a result:

Companies have clearer guidance on sustainable finance initiatives and regulation, which helps in strategic planning and raising capital for these projects.

Investment managers can design credible green products that meet the approved common standards.

Retail investors can better compare financial products based on EU TR-aligned activities.

Professional investors (portfolio managers) can better compare companies through improved disclosure of EU TR-aligned activities.

How does the EU TR apply to an investment portfolio?

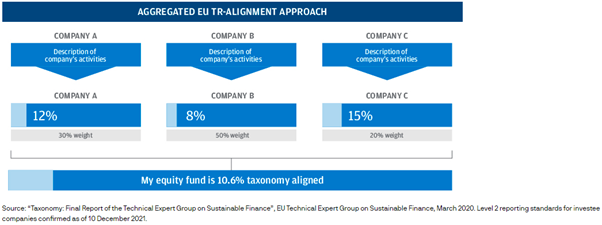

The disclosure of EU TR-aligned activities at the company level feeds up into disclosures of EU TR-aligned activities at the portfolio level. In-scope EU companies will be required to disclose the degree to which their economic activities align to the EU TR. Asset managers aggregate the company disclosures, incorporating all key conditions, so they can disclose the percentage of the fund that is aligned to the EU TR.

Aggregated EU TR-alignment approach

The quality, completeness and timeliness of the corresponding disclosures from investee companies is critical to ensuring the ability of asset managers to meet their own obligations under the EU TR. In time, the improved corporate disclosures will help portfolio managers better incorporate environmental considerations into investment decisions and portfolio construction.

How will the EU TR interact with the EU SFDR and other EU sustainable finance initiatives?

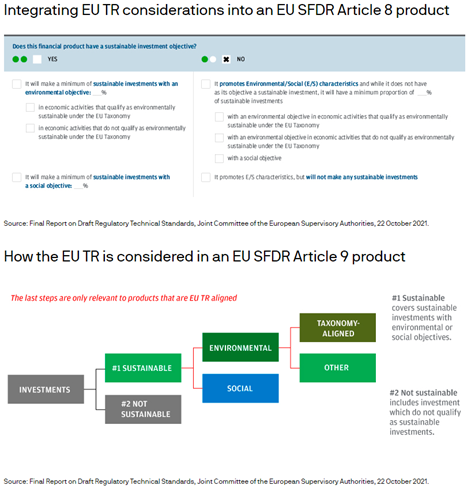

The EU TR is being integrated into the disclosure obligations set out by the EU SFDR. A firm is expected to reflect its minimum alignment to the EU TR alongside EU SFDR considerations. In addition, both Article 8 and Article 9 EU SFDR financial products need to disclose the degree to which they are committed to making sustainable investments, referencing both the EU SFDR and EU TR standards.

Under the EU SFDR, “sustainable investment” broadly means an investment in any economic activity that contributes to an environmental and/or social objective, provided that such investments do not significantly harm any of those objectives and that investee companies follow good governance practices.

Under the EU TR, a “sustainable investment” (being aligned to the EU TR) means specifically an investment in any economic activity that contributes to one of the six environmental objectives recognised by the regulation, on the condition that the investment meets the four-step due diligence standards outlined earlier.

The Article 8 and Article 9 disclosures will provide investors with a detailed understanding of the sustainable investment commitments of financial products via precontractual (ex-ante) disclosure obligations, such as a prospectus. Investors will also be able to see how financial products fared in terms of those commitments via periodic reporting (ex-post) disclosure obligations.

Several EU sustainable finance initiatives, in various stages of development, will likely incorporate elements of the EU TR, such as:

EU Non-Financial Reporting Directive (NFRD) and Corporate Sustainability Reporting Directive (CSRD)

Will there be a UK version of the EU TR?

The UK is planning to follow a hybrid, parallel model of regulation potentially incorporating:

The Task Force on Climate-Related Financial Disclosures recommendations for climate-related entity- and product-level disclosures that came into effect 1 January 2022

Possible Sustainable Disclosure Requirements (UK SDR) based on a discussion paper issued 3 November 2021

Possible Environmental Taxonomy Regulation, similar to the EU, expected at the end of 2022

The UK authorities have not yet decided whether they are planning to integrate ESG into their own legacy regulations.

What further developments related to the EU TR should investors look out for?

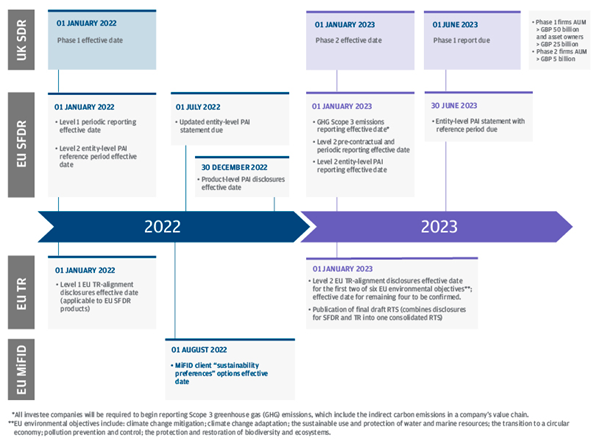

Integrating “sustainable preferences” within existing suitability rules defined by MiFID will be one of the next developments that will impact investors.

Recent EU rules regarding the integration of sustainability factors, risks and preferences into certain organisational requirements and operating conditions for investment firms, as outlined within MiFID, will also incorporate “sustainability preferences” within existing suitability rules. This is currently scheduled to take effect in August 2022, alongside other ESG-related changes affecting several EU regulatory frameworks including Undertakings for Collective Investment in Transferable Securities (UCITS) and the Alternative Investment Fund Managers Directive (AIFMD).

Sustainability preferences allow clients (or potential clients) to determine whether they would like to consider sustainability in their investments, and to what extent, through a financial instrument with one of the following options:

Minimum proportion invested in environmentally sustainable investments as defined by the EU TR

Minimum proportion invested in sustainable investments as defined by the EU SFDR

Considers principal adverse impacts (PAI) on sustainability factors with qualitative or quantitative elements demonstrating that consideration

Additional amendments will incorporate key terms, such as “sustainability factors” and “sustainability risk”, and incorporate ESG considerations to align with the EU SFDR.

What is the timeline for implementing the EU TR?

The EU TR is effective 01 January 2022, when the Level 1 precontractual ex-ante disclosure standards are applied.

Subject to corresponding Level 2 standards of the EU TR being passed into EU law, the enhanced disclosure standards will be integrated into the disclosure templates set out by the EU SFDR effective 1 January 2023 (this date is subject to confirmation).

How will the EU TR benefit investors?

The impact of the EU TR is expected to be incremental over the coming years, rather than immediately transformative, particularly for non-professional investors.

As elements of the EU TR are integrated into the EU SFDR, investors will be able to gain additional detailed understanding of the minimum sustainable investment commitments of financial products and their alignment to the EU TR, both before making an investment and while invested in a particular product. In other words, investors will be able to better compare and monitor the sustainability commitments of financial products over time.

Ultimately, along with additional ESG-related changes to MiFID, investors will benefit from enhanced levels of ESG-related disclosures in financial products.

Keep checking back for our regular blog updates which cover a range of topics and market updates.

Please see the below article from Invesco, analysing the potential effects on equities and global markets from the possible outcomes of the developing situation in Ukraine. Received yesterday afternoon – 03/02/2022.

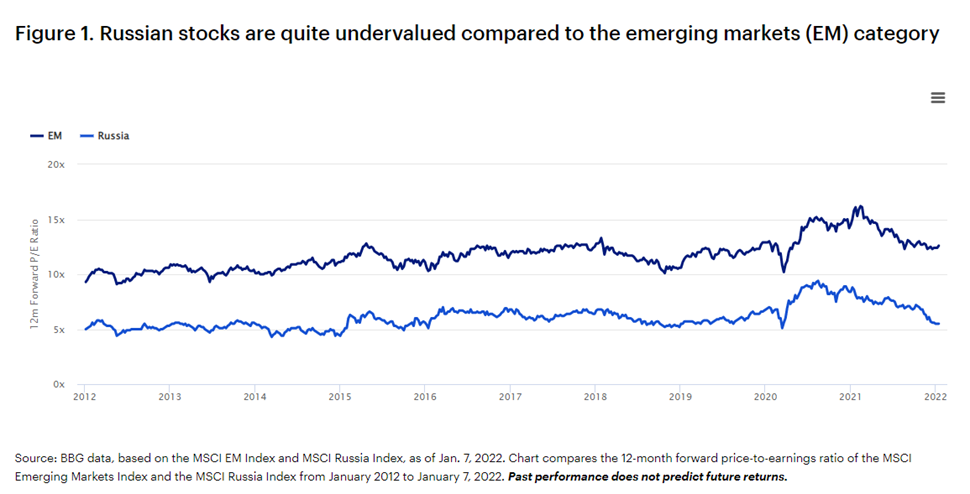

Russian financial markets have had a nasty ride of late as a result of yet more geopolitical intrigue. The MSCI Russia Index is off 26% from the peak in October 2021, while the ruble has slid 9.9% against the US dollar over the same period.

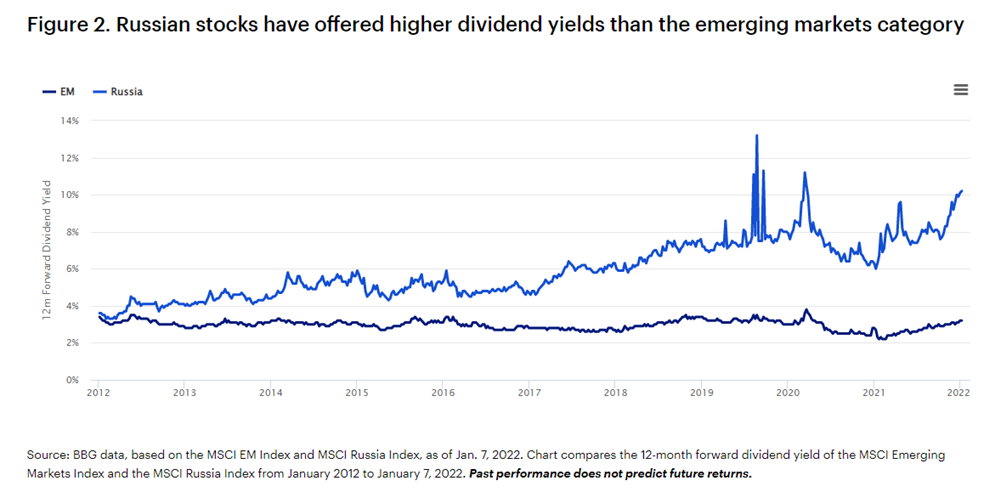

This retreat has occurred against a very favourable backdrop for Russian economic growth, earnings and the currency, with crude prices comfortably north of $80. Pain has been particularly concentrated in stocks that have heavy international ownership, typically growth companies, as opposed to large commodity companies, which are predominantly owned by domestic investors attracted to generous dividend yields.

Today, Russian equities are broadly very cheap! (See Figure 1) The Russian equity bourse is trading at 6x its price-to-earnings (P/E) ratio for the trailing 12 months, clearly the least expensive of any significant bourse worldwide. The entire market, defined by the MSCI Russia Index, is also today offering a 7% dividend yields.

We would also note that Russia is that rare beast with fortress-like macroeconomic strength. It has built up a war chest of $631 billion international reserves, equivalent to 37% of gross domestic product (GDP), has a tremendous current account surplus (7% in 2021) and very low levels of public debt (19% of GDP).

Below, the Invesco Developing Markets team outlines our views on what the Kremlin wants, what the West can possibly concede, and four scenarios on how this could play out — two optimistic and two pessimistic.

It is noteworthy that the most adverse, and in our minds least likely, scenarios would have symmetric punitive implications for both Russian stocks and the entire global equity space — the world economy would likely fall into deep stagflation and equities worldwide would be hammered by massive inflation under the pessimistic scenarios.

Hence, we believe a bet on Russian stocks at these levels is not so different from a bet on the health of global equities more broadly.

What does Moscow really want?

Moscow has threatened a “military solution” to the Ukraine stalemate, in the advent of failed diplomatic efforts. This is backed up with the credible mobilisation of troops alongside the Russian border. In parallel, the Kremlin has presented an aggressive and perhaps deliberately unacceptable, list of demands to Western leaders and the NATO alliance.

So, what does President Putin really want? In our view there are two interwoven broader concerns for Russia: regional security and domestic political legitimacy.

Four waves of NATO enlargement have been widely perceived in Moscow to be in violation of the tacit promises that followed the dissolution of the Soviet Empire. The long-stalled inclusion of the Ukraine (and perhaps Georgia) in NATO is simply unacceptable from Moscow’s perspective.

Therefore, Moscow’s principal demand is for regional security – a permanent denial of NATO membership to Ukraine (and other former Soviet states) and explicit restraints on NATO military exercises, troops and military infrastructure in the region.

Second, Moscow finds the endless “colour revolutions” and regime change pressures, including recent pressures in Belarus and Kazakhstan, unacceptable. These have adverse implications for regional security and domestic legitimacy for the leadership in Moscow.

A visible retreat in support for the Putin administration has amplified these concerns since the painful economic malaise that followed isolation (and sanctions) during 2014-16.

Why now?

Russia perceives it is in a position of considerable strength here. Recent disturbances in neighbouring Belarus and Kazakhstan have reinforced motivations. The Ukraine is slipping into the status of a failed economic (and governance) state.

Washington and Brussels have neither the capacity, nor the charity, to bail out Kiev from its economic debts. The West also has no appetite for military confrontation over the Ukraine.

Talks of “devastating” further sanctions seem largely fictional given the painful self-inflicted repercussions this would have on the global economy and in particular Western Europe. In essence, reflexive financial sanctions are beyond fatigue.

A denial of Russian access to the SWIFT payments system is clearly off the table as it would result in the inability of other nations to pay for Russian energy. Such sanctions would likely immediately send the global economy into massive stagflation, with a painful and likely dramatic rise in energy prices and subsequent recession.

Additionally, it is worth noting that, unlike Iran, who suffered the fate of excommunication from SWIFT in 2012, Russia possesses the wherewithal to exact painful counter sanctions on Europe. It has the means to eventually replace SWIFT with their own System for Transfer of Financial Messages (SPFS), which would be relied upon for payments of Russian hydrocarbons.

More serious sanctions could target large Russian banks, but this too would risk unsettling commodity payments, as it did with aluminium in 2018. In the end, we believe the death knell to many of the “nuclear” sanctions proposed will be Europe’s increased dependence on Russian exports of oil and natural gas over the last decade. Russia now provides 46.8% of Europe’s natural gas imports, up from 30% 10 years prior.

The ubiquitous use of financial sanctions as the simple go-to US foreign policy tool could also erode US dollar privilege as the world’s reserve currency, a very critical element in US strategic power. Thus, Western leaders are left sailing between the Scylla and Charybdis.

Multiple scenarios

The world is too dynamic and we are too humble to pronounce any prescient judgment. (We would also point out that those less humble in pontification are often wrong and generally unaccountable!) But in our view, there are four scenarios:

Invasion/conflict escalation

Concessions

A grand deal

Stalemate.

Each of these four outcomes has multiple permutations.

Optimistic scenarios

The most optimistic scenario would be some sort of grand deal that would exchange Russian regional security (embellishment of the Minsk Accords, restraints on eastward NATO expansion, and tolerance for Russia’s historical sphere of influence) for Ukrainian sovereignty and broader collaboration (new nuclear and tactical arms agreements and global collaboration in areas of Russian influence, including the Near East, Central Asia, and sub-Saharan Africa).

Perhaps this would also involve re-embracing Russia (repealing sanctions over time) into the West, stunting its tilt toward China over the past decade. This would be an enormous diplomatic coup for the West in the real historical narrative, which is checking the rise of China.

Another hopeful scenario would be making acceptable concessions to Moscow in exchange for some respite in tensions. However, this would come up against domestic political constraints in the West — particularly in the United States.

President Biden is already tarnished from chaotic abandonment of Afghanistan and could be attacked as “weak” on autocrats. Appeasement also has historically toxic connotations across Western Europe, particularly in London.

Pessimistic scenarios

Stalemate and conflict are interwoven scenarios. Broadly, it seems to us that these are widely considered the high-probability scenarios in both policymaking circles and financial markets.

Conflict can take many forms, as recent cyber-attacks have demonstrated. And stalemate can also take many forms from benign to periodic, erratic escalation.

Invasion itself is not a straightforward and decisive outcome. Seizure of the entire state is highly unlikely, given the sheer volume of manpower necessary to occupy and resist uprise for a prolonged period.

The 100,000 men stationed north of Ukraine already represent roughly 10% of the combined active and reserve personnel of the Russian Armed Forces. A prolonged occupation would necessitate an increase in Russian defense spending; a figure that already accounted for nearly 15% of annual expenditure in 2020. Should oil revenues fall – a guarantee should Russia move forward with invasion, given almost 50% of exported oil went to OECD Europe – it will have no means to finance its occupation.

Investment implications

As we’ve articulated before, while it is important to understand the implications of geopolitical or macroeconomic events, we believe long-term investors are best served by avoiding short-term, tactical decision-making. Instead remaining focused on identifying companies with sustainable competitive advantages and real options that can manifest over time.

We believe these types of opportunities offer investors the greatest potential for compelling results over time.

Please continue to check back for a range of relevant news and blog content from us and from some of the world’s leading fund management houses.