Please see the below article from Cantab Asset Management received late last night:

Cantab Market Update – Recent Volatility

Market conditions at the start of the year have continued to be challenging for investors, with many indices posting drops year-to-date.

We have been preparing portfolios to withstand heightened volatility for some time. Rising fears around potential conflict in Europe are concerning both on a human level and with respect to the potential economic consequences. Should tensions continue to escalate, we would expect short-term market reaction.

Although it is difficult to watch values drop, we encourage investors to remain focused on their long-term objectives. We are confident that despite geopolitical tensions and challenging market conditions, there remain many outstanding companies delivering growth and opportunities.

High growth companies drove significant outperformance in the immediate market recovery following the pandemic drop in March 2020, but values have struggled in 2021 and thus far in 2022. Part of this pullback is likely attributable to a tempering of the optimism around the future for high-growth companies (particularly in the Technology sector).

Concerns over rising interest rates to tackle inflation, which is looking less ‘transitory’ than Central Banks had initially articulated, have added to the headwinds and 2022 has seen wider market corrections alongside rotations between styles.

The current market weakness does not come as a surprise following strong performance in recent years, as investors grapple with a new stage in the economic cycle. We continue to have conviction in our chosen investments and believe that short-term periods of volatility can provide opportunities for active managers as well as challenges. We discussed this topic in more depth in our recent briefing note, ‘Active Management and the Bright Side of Volatility’, which can be found here:

Active Management and the Bright Side of Volatility

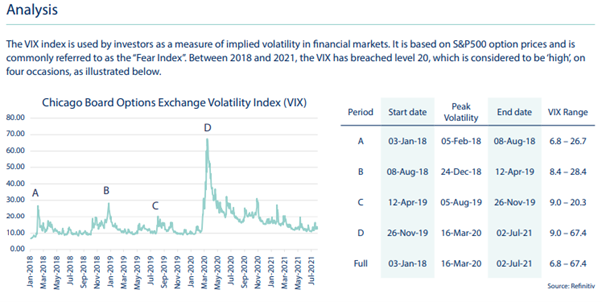

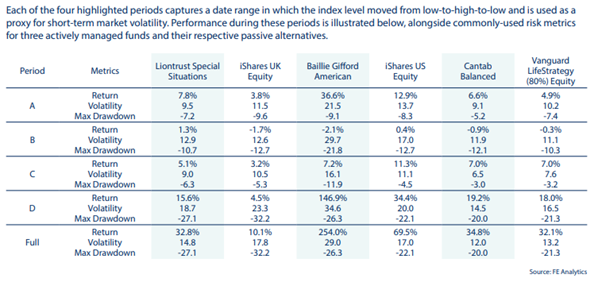

The last decade has seen significant asset price appreciation, accommodated by expansionary monetary policy. Alongside this,

periods of uncertainty have led to spikes in volatility. Whilst recent levels of Quantitative Easing are unprecedented in historical terms,

volatility and market corrections are not. This note considers the relationship between active management and market volatility in

the context of achieving strong long-term performance.

The main takeaways from the following analysis are:

- The actively managed funds tended to exhibit higher volatility than their passive peers

- Over each period of heightened volatility, the actively managed funds tended to outperform their passive peers

- Over the full period, the actively managed funds all materially outperformed their passive peers

- Despite higher levels of volatility, the actively managed funds tended to prove more resilient than their passive peers from a maximum drawdown perspective. This demonstrates one challenge associated with relying on volatility alone as a measure of risk – it captures upside as well as downside movements

- Similar results were obtained when comparing the actively managed Cantab multi-asset portfolio to a passive peer

Summary

These findings may or may not be representative of the entire active universe of funds; to test them is beyond the scope of this analysis. What is clear however, is that within the universe of actively managed funds, there are options that provide significant outperformance on a risk–adjusted basis during periods of heightened volatility. It is our role as advisors to identify and monitor these.

When applying the same analysis to the actively managed Cantab multi-asset portfolio, not only did the portfolio outperform its passive equivalent over the full period but also achieved relatively similar volatility and max drawdown metrics overall. The analysis also found that after a material peak-to-trough movement, the actively managed Cantab portfolio recovered considerably faster to previous highs when compared to the passive equivalent.

The results from the analysis not only highlight the importance of taking a long-term view, but also demonstrate that there are two sides to volatility: downside and upside. Volatility is usually calculated using variance or standard deviation, by summing the square of the deviation of returns from the mean return and dividing by the number of observations in the data set. By definition, upside and downside deviations are treated equally. Whilst higher volatility implies higher risk, due to less predictability of asset pricing, investors are typically in favour of upside volatility in practice. By pursuing a passive strategy, investors avoid the downside risk of underperforming a benchmark index; unfortunately, they also miss out on the upside potential of outperformance.

Periods of short-term volatility have been common throughout history and will continue to be common in the future. However, during such periods, investors tend to focus on the negative side of volatility rather than directing their focus to the bright side of volatility that is offered by good active management.

Our Comment

As always, our comment regarding the recent volatility is to remain calm and don’t panic. The markets will stabilise in time.

Volatility is a normal part and a key function of how markets work.

It creates great investment opportunities when buying assets.

Keep checking back for our regular blog updates which cover a range of topics and market updates.

Andrew Lloyd DipPFS

28/01/2022