Please see below an article from J.P. Morgan which was published on 25/02 and received yesterday (28/02) afternoon and details their views on the Russia/Ukraine conflict and the potential wider impact this could have on the West:

The human toll of any conflict is devastating and events unfolding in Ukraine are deeply upsetting. This note seeks to answer the economic and market questions we are receiving.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see the below article from AJ Bell, examining the potential effects on wage growth from current inflationary pressure and the implications for stock market valuations – received yesterday – 27/02/2022

Calls from both the Bank of England’s governor, Andrew Bailey, and its chief economist, Huw Pill, for wage restraint do not sit easily alongside the current headline inflation figures. Nor does Unilever’s statement (10 Feb) that it raised prices by 4.9% in the fourth quarter of last year and has planned further hikes in 2022, thanks to expected input cost inflation of 3% to 4%.

A few small caps, notably own-brand cleaning products specialist McBride, loo roll maker Accrol and retailer Joules, had dished out profit warnings as they have proved unable to raise prices far or fast enough to compensate for rising costs.

But Unilever is the biggest so far, as it forecast a drop in profit margins of some 1.4 to 2.4 percentage points in 2022, down to 16% to 17%. Even though not all of this is down to higher raw material, freight and packaging costs, as the food-to-personal care giant continues to invest heavily in product development and marketing, it does beg the question of who is able to defend product margins in an inflationary environment if Unilever cannot? After all, it can call upon the power of brands such as Marmite, Hellmans, Dove and Magnum.

Investors must again therefore address three key questions:

Will workers demand – and get – meaty wage rises in response to their rising bills and expenses? Lowly unemployment numbers would suggest this is their time to strike (either figuratively or literally speaking).

If they are successful will that drive wider inflation and force central banks to raise interest rates further and faster than currently anticipated by markets?

Will rising wages, alongside freight, raw materials, packaging, start to take a bite out of corporate profit margins? And, if so, what does that mean for stock market valuations, especially at a time when interest rates are rising?

Vicious circle

Wage growth is cooling a little on both sides of the Atlantic, but the readings are still high by the standards of the (admittedly relative short) datasets that we have. In the UK, total pay rose by 4.8% year-on-year in the three months to December and US workers’ average hourly pay rose 5.7% year-on-year in January.

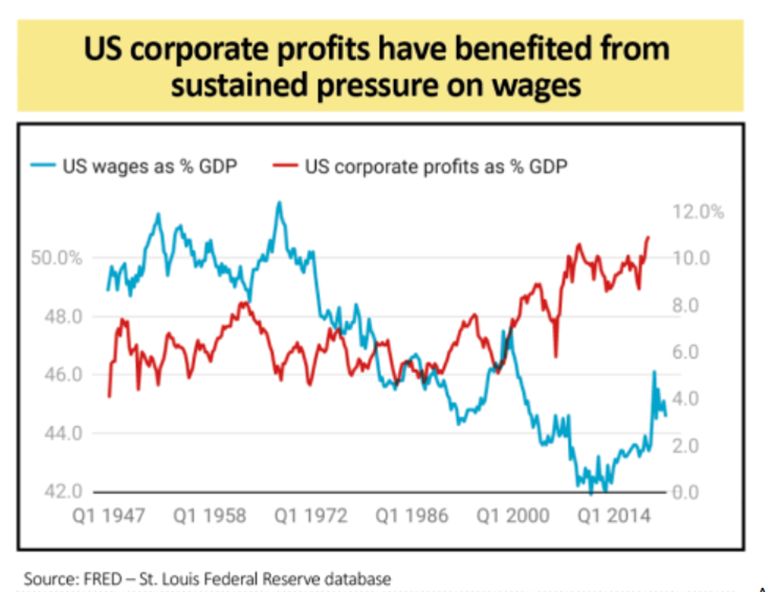

Low unemployment rates and high numbers of job vacancies relative to the numbers of those without work would suggest labour may just have the whip hand in any pay negotiations. Trades unionists and workers may be happy about that for political, philosophical and economic reasons as there can be little doubt that capital has had its wicked way with labour for much of the past four decades, and beyond.

Since 1947, Americans’ pay has fallen by more than four percentage points as a portion of GDP. American corporate profits have increased by around six percentage points over the same time frame.

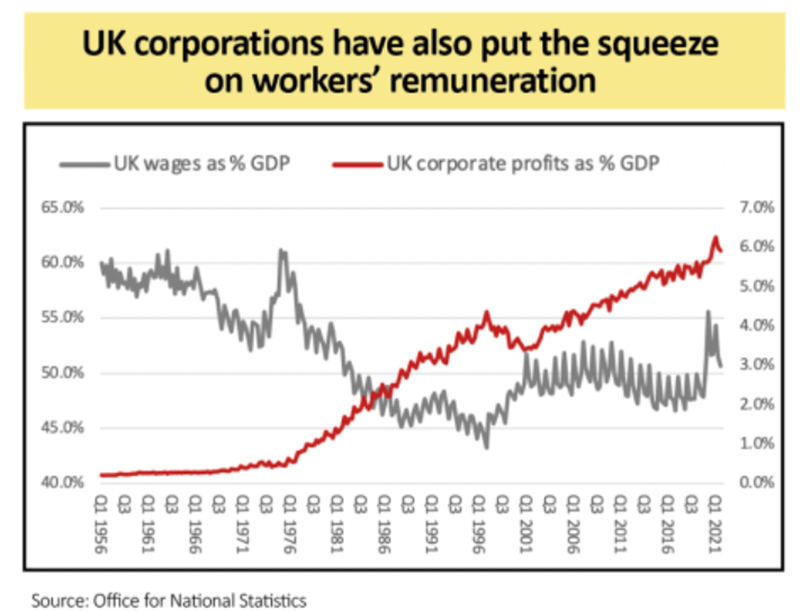

A similar trend can be seen in the UK, where the data goes back to 1955. Since then, labour’s take-home slice of the economy has dropped by almost ten percentage points, while corporations have increased theirs by the thick end of six points.

Margin call

Investors could therefore be forgiven for wondering what may happen next. After all, corporate profits stand at, or close to, a record high as a percentage of GDP in both the US and UK.

Any margin pressure could therefore restrict profit growth (and that is before UK-based firms face a jump in corporation tax to 25% from 19% from April 2023). And the combination of higher interest rates and slower profit growth is not an ideal one, especially in the US stock market, where valuations are at or near all-time peaks, based on market-cap-to-GDP and the Shiller cyclically adjusted price earnings CAPE ratio.

Yet all may not be lost for three reasons. Higher pay could help consumers’ keep spending. Companies report sales and profits in nominal, not real, inflation-adjusted terms. Sales up, costs up can still mean profits up, which is why stocks and shares are seen as offering a better hedge against inflation than say bonds.

Granted, some companies and industries may be better suited to coping with inflation than others. Areas where demand is relatively price inelastic, or insensitive, are one – they include oil and tobacco. Industries where demand growth outstrips supply growth (and it takes time to create fresh supply) are another – and that could include mining, especially as central banks cannot print copper, gold or cobalt.

And consumer staples or luxury goods companies with brands can be better placed than most to raise prices thanks to the customer loyalty and pricing power they confer. Luckily, the FTSE 100 has quite a few of those.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

As you would expect volatility has been particularly high recently as we try to transition back to normal with our economies, with Central Banks and Governments policy changes, particularly in the UK and the US. This volatility has been increased further by the Russia/Ukraine conflict as you will have heard in the news. Thankfully most portfolios don’t have much of an exposure to Russia.

Over the last few days we have started to receive notifications of 10% or more drops in portfolio values for clients in the higher risk ‘unsmoothed’ funds and portfolios. This is to be expected.

PruFund Growth is a very well diversified multi asset fund with ‘smoothing’ and it lags both a falling and a rising market but it is not immune to volatility. Prudential updated us on PruFund late on Friday 25/02/2022. You would expect some impact on your PruFund Growth investments now – however the great news is as follows:

No Unit Price Adjustment downwards on PruFund Growth

The Expected Growth Rate (EGR) increases from 5.7% to 5.9% gross per annum

A technical fund surplus has been declared following an actuarial assessment and an increase in value of 1.25% will be applied to PruFund Growth today (Monday 28/02/2022)

The above increase in PruFund Growth EGR rates is applicable to Pru pension products and ISAs. Other products differ.

This EGR increase is really good news given the current challenges and backdrop of markets. Other ‘smoothed’ Pru funds did not fare as well and in particular the new PruFund Planet ESG range of funds had some downwards Unit Price Adjustments applied. As we have discussed, in my view this range of funds are too new to invest in for the majority of our clients.

However, the global impact of the conflict in Ukraine with the Russian invasion should not be under estimated. The whole world will feel the impact of this invasion and the necessary sanctions economically.

Markets are disconcertingly dispassionate about geopolitical events such as this invasion of Ukraine, and their focus is more likely to return to the actions of Central Banks and Governments.

My thoughts are with the Ukrainians, brave people fighting a courageous battle. I’m sure the majority of Russians, even their armed forces, don’t want to be in a conflict either. Hopefully there will be a resolution soon.

Please find below, an update on how Russia’s conflict with Ukraine will impact markets, received from Brewin Dolphin yesterday evening – 24/02/2022

As Russian forces invade Ukraine, Guy Foster, Brewin Dolphin’s Chief Strategist, analyses the impact on stock markets, the economy and investors.

Stock markets around the globe have slumped on news that Russia has launched a full-scale invasion of Ukraine. What are the implications for investors, and does this change the equity market outlook?

How have stock markets reacted?

Stock markets have taken today’s news badly because it represents the ebbing away of the potential for peaceful de-escalation. At the time of writing, the pan-European STOXX 600 is down 3.8% and Germany’s Dax has shed just over 5%, reflecting the country’s heavy reliance on Russian energy supplies. The commodity-heavy FTSE 100 has lost 3.2%, with surging oil prices helping to limit losses.

Today’s stock market sell off is a continuation of the heightened volatility we have seen in the first two months of the year. Escalating tensions in the weeks leading up to the invasion, coupled with the risk of rising inflation and interest rate hikes, have been weighing heavily on investor sentiment.

The major risk to stock markets right now is the increase in uncertainty. When uncertainty rises, the ‘risk premium’ increases. In other words, equity valuations fall as investors require higher potential returns to compensate for the higher perceived risks. There is also a risk of contagion to emerging markets more broadly.

The reason why markets are so focused on the current conflict is that Russia is an important source of, and Ukraine is an important transit country for, oil. Supply disruption could lead to further increases in the price of oil, which could exacerbate already high inflation in Europe, resulting in continued market volatility.

What is the potential economic impact?

At this early stage, it is difficult to predict the economic impact.

First, we do not know what Russia’s ambitions are for Ukraine. It is also unclear how long the conflict could last, although the news coming through suggests Russian and Ukrainian military forces are balanced in number, and so the conflict is unlikely to be easily won either way.

Second, while sanctions could hold back Russia’s economic growth, Western leaders generally have a very limited range of sanctions that they are willing and able to deploy. Cutting off Russia from financial markets would only have an impact when it comes to seeking financing. Russia doesn’t need to do this while energy prices stay high.

Some have suggested barring Russia from the SWIFT communication system that facilitates international money transfers, but that would seem to impede payment for much-needed Russian gas supplies. In all likelihood, sanctions will focus on individuals and some Russian institutions; there will be great reluctance to threaten commodity supplies upon which Europe, in particular, is heavily dependent.

If sanctions did cause economic disruption in Russia, this is unlikely to have much of an impact on global growth, as Russia’s economy represents only around 1.8% of global gross domestic product. The much greater concern is the extent to which disruptions to oil supply could dampen economic growth more broadly.

What is the longer-term outlook?

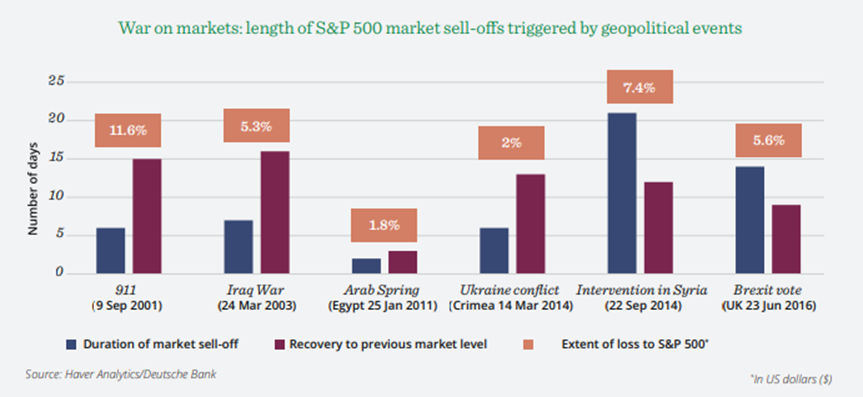

While events in Ukraine are extremely concerning, it is worth bearing in mind that from an investment perspective, steep declines in stock markets are not unusual, and they tend to be short lived. History shows us that equities have been resilient during periods of crisis in the past, such as the Cuban Missile Crisis, the Iraqi invasion of Kuwait, and 9/11. The impact of these events on the markets, and indeed the economy, were much more fleeting than their significance in modern history.

Stock markets tend to be disconcertingly dispassionate about political and human tragedy unless it has an overt economic impact. They also tend to anticipate geopolitical risks in advance, which means the onset of conflict can often be the moment that uncertainty peaks. So, while stock markets are likely to remain volatile in the short term, this may be more to do with ongoing concerns about inflation and interest rates. The longer-term outlook for the global economy and equities remains positive as the pandemic-related headwinds reduce, with job and wage gains becoming more common. The events in Russia will contribute to the overall framework we have for assessing the opportunities to grow wealth over the longer term.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please see article below from Quilter Investors received late yesterday afternoon – 23/02/2022

Markets tumble as unmarked Russian tanks rumble into Ukraine

Global equity markets recoiled late on Monday (21 February) following Russian President Vladimir Putin’s decision to send armoured divisions into Ukraine.

In the latest round of political brinkmanship in the Ukraine theatre, Mr Putin took advantage of Presidents Day, a federal holiday in the US, to announce on Russian television that the country now officially recognised the two breakaway regions of Donetsk and Luhansk in eastern Ukraine as independent entities.

The leaders of these breakaway regions subsequently appeared alongside Mr Putin in the Kremlin signing a decree recognising their independence. Later that day a number of conspicuously unmarked tanks were reported as rolling through the streets of Donetsk.

Russian markets were still trading when Mr Putin announced his decision following calls to the leaders of Germany and France. The rouble subsequently plummeted north of 3%, while Moscow’s dollar-denominated RTS index plunged more than 13% on Monday with the rouble-based MOEX Russian index suffering its worst day since the March 2014 Crimean annexation, down 10.5%. Elsewhere, the yield on Russian 10- year government bonds (known as OFZs) surged to 10.6% on Monday.

Meanwhile, western markets began to react to the heightened tension on Tuesday morning with oil prices pushing on toward $100 a barrel amid supply fears. After initial ‘softness’ western markets proved quite resilient as investors clearly anticipated limited sanctions at this early stage.

Asian markets fared worse, impacted by both the heightened geopolitical tensions and anxiety over fresh Chinese regulatory scrutiny.

In response to the moves, the US imposed immediate business sanctions on the breakaway regions but held off from imposing the agreed sanctions planned by the US and its European allies in the event of a full-scale invasion of the Ukraine. Even so, more US sanction were expected on Tuesday while Boris Johnson chaired a meeting of the UK’s emergency ‘Cobra’ committee to discuss UK sanctions against Russia.

Likely outcomes…

Coming as it does on the back of a slowly unfurling global energy crisis and record levels of western inflation, driven in no small part by soaring energy prices, Mr Putin’s gambit has succeeded in garnering the political attention he has always sought for his nation.

There now exists a broad spectrum of possible outcomes, each dependent on the Russian president’s next move. The sanctions announced so far entirely lack bite which may have emboldened Russia’s leader. However, the situation will quickly change with potentially harsh international sanctions set to be imposed against Russia in the event of a full invasion.

Even so, Russian boots are now that much closer to Ukraine – which Mr Putin on Monday described as ancient lands of Russia – ratcheting up tensions on the ground and internationally.

Energy worries

In theory, it seems unlikely that an escalation in the conflict will lead to Russia ‘turning off the gas’ to Europe as such exports broadly account for around a third of Russian GDP. But although Russia continued to supply energy to the West throughout the cold war years, the situation is quite different today. Russia is no longer a rickety soviet state dependent on western hard currency.

Mr Putin’s actions have already helped push operating profits for Russia’s primary player, Gazprom, to $90bn this year, more than four times what they were in 2019. Meanwhile, energy sector analysts estimate that (client penalties aside) a complete shutdown of gas piped to Europe might cost up to $230m a day in lost revenues for Gazprom at a time when Russia holds a huge war chest of some $630bn in central bank reserves.

While Russia could afford the lost revenue, the bigger price for Mr Putin might come from jeopardising projects like the Nord Stream 2 gas pipeline which, although completed in September, still requires certification by Germany and the EU – a process that was halted by German Chancellor Olaf Scholz on Tuesday following the recognition of Donetsk and Luhansk. Russia’s still fledgling supply contracts with China might also suffer if it proves to be an unreliable partner.

Whatever Mr Putin decides to do, he’ll need to move fast as Europe’s energy demand drops by 40% or so come spring, which means he loses the added leverage he currently enjoys.

Broader changes

Regardless of the eventual outcome, the latest escalation in the Ukraine suggests that NATO troop numbers in Europe will need to rise in Eastern Europe along with national defence spending budgets, which has potential tax implications down the line.

Meanwhile, it remains to be seen if the rising levels of geopolitical risk in markets cause central banks to re-think the pace of their planned hiking cycles to help support markets. Some analysts are already pricing in more restrained rate rises in Europe this year.

Mr Putin has chosen his opening well with western markets already straining against record inflation and the interest-rate rises that must now quell it. An energy price shock just as central banks are raising interest rates could derail investor sentiment and the outlook for energy-intensive companies in particular.

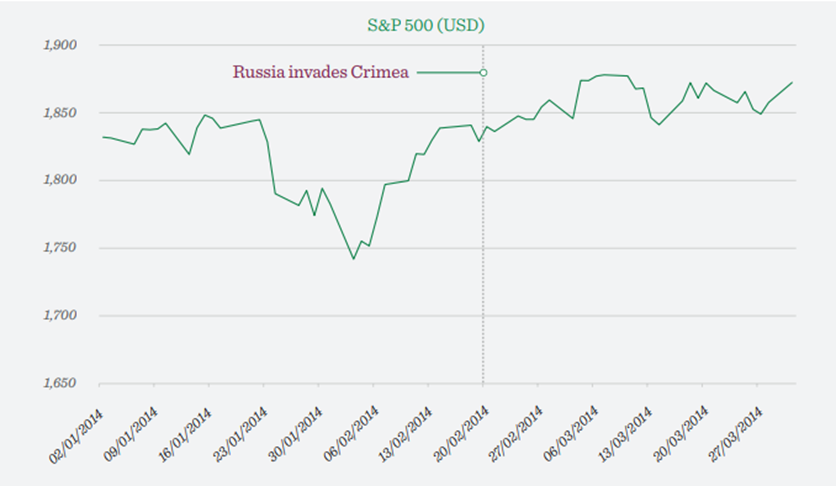

Although we expect to see the S&P Index re-testing the lows of 24 January, we suspect the disruption caused to equity markets will be relatively brief in line with history (see below). In the meantime, our portfolio managers are looking for opportunities to capitalise on the current volatility, possibly through derivative contracts, which can offer both investment gains and protection against market losses.

A history of conflict

Historically, western markets have always been relatively sanguine towards Russian territorial aggression. As the chart inset illustrates, when Russia annexed the Crimea from Ukraine in 2014, markets were quick to dismiss the interruption.

This time, the political, inflationary and energy supply consequences of further escalation are likely to result in a more pronounced response from markets but they will quickly re-price to the new norm, whatever that might happen to be.

As always, the key message for investors is not to get sucked in by the noise. Over the medium to long term, the broader landscape of company earnings and the strength of economic growth will far outweigh the importance of ‘conflict politics’ for investors. Currently, even including its huge energy bills, total trade with Russia accounts for just 1.5% of EU GDP and only 0.5% of US GDP.

Please continue to check back for our latest blog posts and updates. Charlotte Clarke 24/02/2022

Please see below a special market update from Tatton Investment Management received yesterday – 22/02/2022.

Russia’s aggression towards Ukraine reached a new level overnight after Russia’s president Putin officially recognised the two self-proclaimed separatist ‘republics’ in Ukraine’s Donbas region. Most importantly, he ordered official troops to move in for what he declared to be ‘peacekeeping operations’. This has triggered the West to announce a stepping up of sanctions. Meanwhile Ukraine’s president Volodymyr Zelenskiy said Putin had merely “legalised” troops already present in the republics.

At the time of writing on Tuesday the media reaction to the escalation of the conflict has been more alarmed than that of stock and other asset markets. This ties in with what we published last week about historical observations of the impact of regional wars on stock markets. Price moves tend not to be particularly pronounced once hostilities have actually started. Indeed, downswings occurred when tensions were building up beforehand and hostilities have more often marked the beginning of a medium-term upswing in markets.

The explanation for this apparently uncaring market action is that economic activity beyond the area of conflict usually continues as before. However, in this specific instance, there is a risk of energy supply disruptions to the pan-European region in the form of Russian gas, or at least that energy prices will remain high for longer or rise higher than had been anticipated in 2022’s general economic recovery scenario. This would explain some of the recent weakness in stock markets as they had priced in further increases in the cost of gas and oil putting a dampener on the 2022 economic upswing.

We suspect that if Putin’s latest move had indeed constituted a full-on invasion of Ukraine – as some of the news media seemed to suggest – then the market reaction would not be as benign as it was this Tuesday morning, with only the price of oil and gas in Europe trading notably higher than yesterday.

The subdued market reaction tells us that there is a recognition or at least suspicion that with this latest move, Putin may have revealed his true goals/intentions in this conflict; namely, explicit control of the Russian speaking parts of the Donbas region after Russian supported separatists seized the area in 2014. A military protectorate may not be an outright annexation like the Crimea, but few would draw a distinction. This would be similar to the outcome of the 2008 conflict where Russia succeeded in turning the two Georgian regions of Abkhazia and South Ossetia into such military protectorates.

It also suggests that there is an assumption in markets that Putin has once again been successful in outmanoeuvring western interests and achieved his aim of extending Russia’s area of influence and control at an acceptable cost to his country. This assumption is based on previous indications by the Biden administration that they would not deem a move in the frozen conflict in the Donbas as a trigger for imposing the full force, of what would be very painful sanctions on Russia.

This relative market optimism is heartening, and some may even describe it as wishful thinking, given it is not at all certain that Putin will be content with what he has gained so far. Whether the US and European governments will indeed refrain from imposing significant sanctions and whether the Ukrainian government will accept Russia’s occupation of part of its rightful territory, rather than strike back is unclear. Its basis is the assumption of rational actors on both sides, which at a time when the pressures of the pandemic are easing should want to shy away from risking the economic recovery and contain the economic fallout to what is deemed an acceptable minimum.

Our view is that the above is a possible outcome, but that it is too early to expect this conflict to be beyond its peak. We recall that in the run up to Greece’s 2012 sovereign debt crisis there was also a widespread market expectation that political actors in Greece and the EU would act rationally from an economic point of view, and not let the situation deteriorate to the point where the Greek public no longer had access to their bank accounts. In the end, what was deemed unthinkable was allowed to happen in order to pave the way for a lasting resolution to the debt crisis.

We believe we are faced with a similar situation today, except that one of the main actors in the current conflict – President Putin – is much harder to gauge, even if it has to be said that up to now, in apparently achieving his aims he looks to have been clever and rational, rather than dogmatic or irrational.

As a result of the fluid situation, we are for the time being satisfied that our central investment position, aligned with a continued, albeit more gradual global recovery during 2022 remains sound in the prevailing political and market environment. However, should Russia aim for a significantly bigger landgrab than the already rebel occupied areas of the Donbas and/or the reaction of the Ukraine and the West’s sanctions become more severe, we will re-evaluate our investment portfolio positions. On the other hand, if Russia signals that they are content with what they have achieved, along the lines of ‘we believe our brothers and sisters in the Donbas are now save’ could trigger a genuine relief rally.

The situation remains fluid and uncertain, but as it currently stands, we are seeing an almost equal probability for our next move to be an increase in our pro-cyclical recovery position or a more defensive reduction in our overall risk exposure should the geopolitical situation deteriorate rather than improve from here.

Additional input from J P Morgan yesterday looked at the impact on markets of geopolitical events such as conflicts, war and 9/11. Generally, the impact was short term in nature and recovery typically quick.

In the circumstances you should remain invested and keep on regular monthly funding of pensions and investments. Be patient, look through the short term volatility and focus on your long term objectives.

My thoughts are for the innocent populations involved, hopefully we will still see a peaceful resolution. Steve Speed 23/02/2022

Please see Brooks Macdonald’s Weekly Market Commentary below published yesterday (21st February 2022):

Geopolitical risk continues to dominate the near-term investor narrative with the US describing a Russian invasion of Ukraine as imminent.

Equity market volatility continued on Friday as Ukraine risks ratcheted up and geopolitical uncertainty looks set to continue well into this week. Markets are fixated on the geopolitical risk within Ukraine, particularly as it could have, alongside severe human cost, a significant impact on inflationary pressures in continental Europe and the rest of the world. The imminence of US warnings over a Russian invasion of Ukraine gathered pace over the weekend with President Biden saying that significant volumes of intelligence pointed to the invasion starting in a matter of days.

The US and Russia are set to commence high level talks this week after a more constructive call between President Putin and President Macron.

A phone call yesterday between President Macron and President Putin sounded constructive, with both parties agreeing that a diplomatic solution to tensions in Ukraine was preferable. That said, the last set of calls between France and Russia established a Russian commitment to withdraw troops after the ongoing exercises in Belarus which appears to have now been reversed. The US and Russia have in principle agreed to a summit between the leaders but the US has said that such a summit would be conditional on Russia not invading Ukraine in the interim. The content for discussion at the summit will be set between the US secretary of state and Russia’s foreign minister on Thursday, with the implication that the high-level talks will talk place on Friday at the earliest. This likely sets the stage for another week of uncertainty as energy markets attempt to price in a binary outcome.

This week sees the publication of the Federal Reserve’s preferred measure of inflation as well as surveys testing the health of US consumption.

Meanwhile financial markets are also trying to assess the strength of the US economy and whether momentum is sufficiently strong to offset the demand destruction that would be caused by an aggressive tightening of US monetary policy. This week we have the US’s preferred inflation measure, Personal Consumption Expenditures (PCE), released on Friday which will add to the debate over whether the Federal Reserve will raise by 25 or 50bps in March. However, we will be paying as much attention to durable goods orders for a view of current demand for capital outlays and to consumer confidence and sentiment numbers that will help explain the consumer reaction to the inflation pressures of recent months.

Adding Ukraine tensions to a market outlook, which is already wrestling with several inflation and interest rate narratives, sets up a volatile backdrop. This week will give investors a preview of consumer demand in the US which will be an essential consideration for how the economy will react to a more aggressive Federal Reserve hiking cycle. The bond market is currently implying six rate hikes in 2022 – whether that has a major impact on GDP will be highly dependent on US consumption.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Cash savings have suffered death by a thousand rate cuts over the last decade, but the cash paradox is that even though rates are now on the up, things look like they will get even tougher for savers. That’s because elevated inflation is going to eat up any gains from higher interest rates on cash and will take an extra pound of flesh for its trouble too. Please see below article received from AJ Bell yesterday for further detail on this.

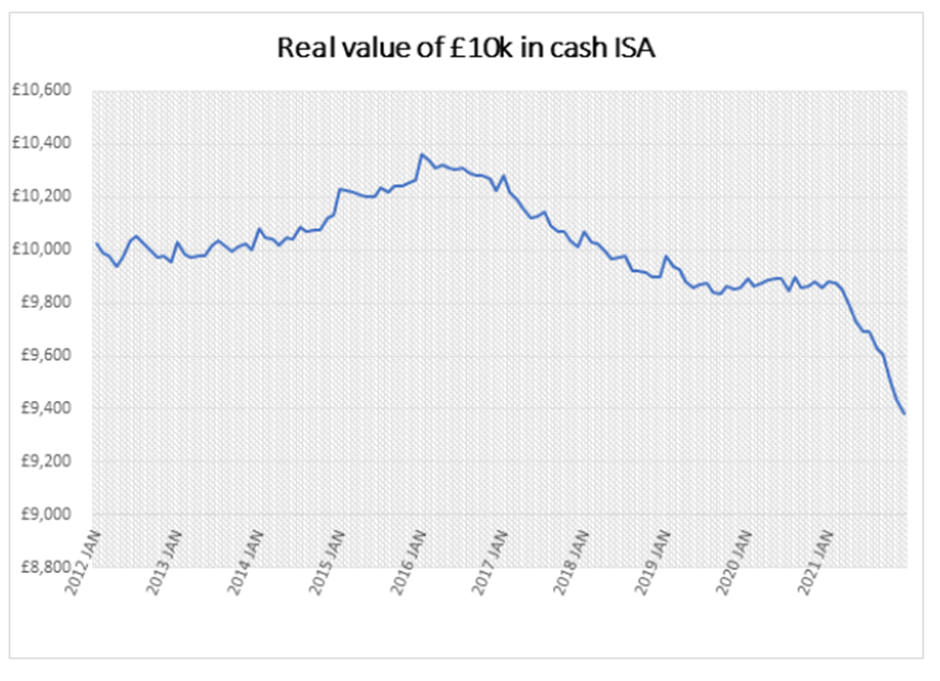

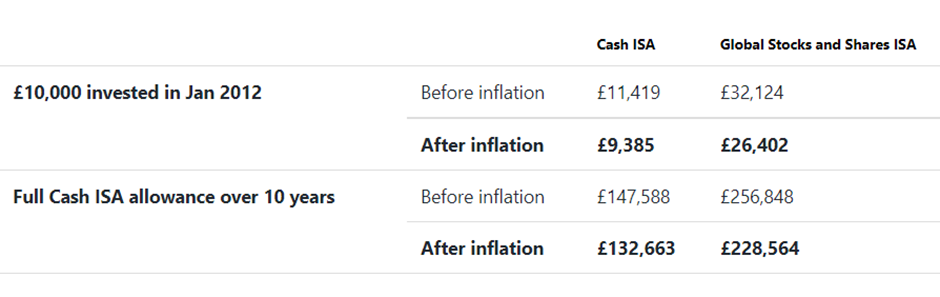

£10,000 invested ten years ago would now be worth just £9,385 today, after inflation is taken into account. This lost decade for cash savers has of course been caused by ultra-loose monetary policy, though inflation has remained largely contained. What is alarming is that in the next twelve months alone, Cash ISA savers face a similar loss in buying power to the one they have experienced over the last decade. £10,000 saved into the average Cash ISA today could be worth just £9,600 this time next year, based on the latest Bank of England forecasts for interest rates and inflation, and the current margin between base rate and ISA rates.

So despite interest rates falling to rock bottom over the last ten years, worse may yet be in store for cash savers. Longer term, higher rates should be positive for Cash ISA savers, if inflation tails off in the way the Bank of England expects. If it doesn’t, the last ten years of slow and steady inflationary erosion could end up looking like a walk in the park.

Those who shop around will likely be able to improve their lot, slightly. The current best buy ISA is offering 0.6% per annum, according to Moneyfacts, which compares to 0.34% for the average Cash ISA. As interest rates rise, the wedge between the most competitive and least competitive Cash ISAs can be expected to grow, as some banks attempt to attract new customers by bumping up their rate, while others try too eek out some extra profits by keeping rates low until savers start voting with their feet.

Meanwhile Stocks and Shares ISA investors have been big winners from the last ten years. £10,000 invested in the average global stock market fund within an ISA would now be worth £26,402 after inflation is taken into account. Over any ten year period, the odds are heavily stacked in favour of a stock investor compared to a cash saver. But the loose monetary policy of the last decade has helped exacerbate that trend. Looking forward, tightening monetary policy may well prove to be a false friend to cash savers, if accompanied by sustained inflationary pressures. High inflation isn’t exactly good news for shares either, but companies can at least offset increasing costs by pushing price rises onto consumers. Investing in shares therefore looks like the best way to beat inflation over the long term.

The FCA’s latest strategic focus on encouraging those with high levels of cash saving to invest for the longer term is therefore well-timed. The regulator reckons that 8.6 million consumers hold over £10,000 of investible assets as cash. HMRC data shows that £443 billion was put into Cash ISAs between 2010 and 2020, compared with £206 billion invested into Stocks and Shares ISAs over the same period. Clearly low interest rates have not hugely deterred Cash ISA savers to date, but the return of high inflation means poor cash rates will really start to bite, and will likely push savers up the risk spectrum in search of inflation-busting returns. Those who are thinking of taking on more risk by investing in the stock market might consider doing so through a monthly savings plan, which will make for a smoother ride.

The lost decade for cash in numbers

Since January 2012, the average interest rate paid on Cash ISA balances has sunk from 2.5% to a record low of 0.3%. A combination of low interest rates and bank funding schemes like Funding for Lending and the Term Funding Scheme have seen cash rates drop to almost zero. Inflation has been relatively benign over this period, averaging 2%, directly in line with the Bank of England’s target. Even so, £10,000 invested in a Cash ISA ten years ago would be worth £9,385 in real terms today.

By contrast the average Global Stocks and Shares ISA (invested in the IA Global fund sector average) has turned £10,000 invested into £26,402 over the same period, after adjusting for inflation. If you had saved your full Cash ISA allowance over these ten years, equivalent to £142,220 of contributions, that would now be worth £132,663 in real terms, if saved in the average Cash ISA. If invested in the average Global Stocks and Shares ISA instead, it would be now worth £228,564, after adjusting for inflation.

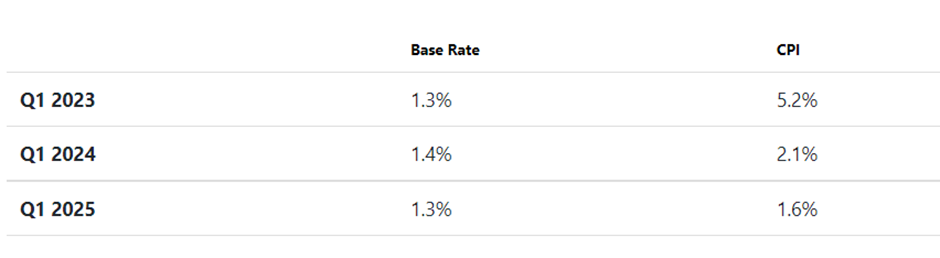

Looking forward, the market is expecting rates to rise, and the Bank of England is forecasting that inflation will fall away next year. The latest forecast from the Bank is shown in the table below. The rate of interest paid on the average Cash ISA currently stands 0.09% above the Bank of England base rate, so assuming that margin holds, and the Bank’s forecasts are accurate, that would mean £10,000 saved in the average Cash ISA today would be worth around £9,600 this time next year*. Beyond that, the Bank expects inflation to moderate, but interest rate hikes are expected to tail off too. Of course, the Bank has repeatedly underestimated inflationary pressures of late, and if elevated inflation sticks around for longer, that could be even more ruinous for cash savings.

Please check in again with us shortly for further relevant content and news.

Please see below an article published by Invesco on Tuesday (15/02) and received yesterday afternoon, which covers their views on inflationary pressures and geopolitics and how these are impacting on markets:

As you can see from the above, inflationary pressures globally are having a big impact on markets and the Fed’s outlook and proposed rate hikes by Q2 2022 have also impacted on investor sentiment. Supply chain issues also remain an issue and this could potentially be further exposed by events in Russia and possible sanctions that could be imposed.

The good news is that Covid cases are declining, and global economies are starting to transition back to a form of normality. It also appears that inflation expectations may have peaked, watch this space!

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below, an article from Tatton Investment Management detailing how increasing tension on the border of Ukraine has affected global markets – received yesterday afternoon – 16/02/2022.

From our phone calls and conversations we have with adviser firms, we know portfolio investors are concerned that the fear of Russia invading Ukraine is driving, at least in part, the poor start to the year experienced by capital markets.

As laid out in recent editions of The Tatton Weekly, the cause of the current market volatility is not being caused by fears of Russia’s President Putin starting a European war, but is rooted in concerns that central banks may be moving too rapidly from monetary easing to tightening. Nevertheless, the two are loosely connected. Putin’s actions have left energy prices elevated for longer, which in turn keeps consumer price inflation elevated, which has arguably increased the pressure on central banks to act.

The current situation is undoubtedly worrying, and the political tensions are only exacerbating the most recent market weakness. Therefore, as we always do at a time of market-moving activity, we wanted to share our thoughts in a supplemental investment update. So, let’s begin by looking at what investors can learn from previous episodes of geopolitical stress.

Recent history has relatively few episodes of war and near-war that might be considered to have been of global significance. Surprise actions such as the Iraq invasion of Kuwait and 9/11 (in 1990 and 2001, respectively) had negative impacts only after the event. However, drawn-out episodes have seen market weakness in the lead-up to but not after the outbreak of conflict. Both US-Iraq wars marked the start of stock market rallies, as did the Cuban Missile Crisis.

On those occasions, there were several other factors – aside from geopolitical tensions – which had contributed to weakness beforehand. Moreover, we also cannot attribute market strength to a sense of resolution. Nonetheless, it demonstrates that markets are reasonably efficient around such events; they go through a gradual process of discounting risk ahead of the event, rather than having a sudden unexpected dislocation as war starts. Unless they seriously impact global growth, we should expect the impacts caused by the negative surprise to pass quite quickly. Using this fairly limited history as a guide, from the current position, there is potential market upside as well as a downside.

In other words, we think the past tells us that – on balance and in market terms – we should not be too worried about market returns if the worst happens. Nonetheless, it is important to try to assess whether the current situation is markedly different.

At this point, various markets have already priced in quite high levels of risk and consequence. This is particularly true of energy. Natural gas prices have been squeezed much higher this winter. Speculative buying has been a factor, but Russia’s actions in suppressing supply have almost certainly been the biggest driver. As we have noted before, Europe’s weak spot is its reliance on Russian energy, especially natural gas. The chart below shows that the gas supplies have been cut repeatedly, and do not seem to be related to the pandemic.

Russia still needs to sell its oil and gas and Europe remains its major customer. According to Russia’s central bank, total exports (not just energy) reached $489.8 billion in 2021. Of that, crude oil accounted for $110.2 billion, oil products for $68.7 billion, pipeline natural gas for $54.2 billion, while liquefied natural gas accounted for $7.6 billion (In sum 49% of all exports). While the rise in prices will be welcome in Moscow, it will gain little if Russia cannot sell the volumes needed.

Growth in Russia is forecast to slow down to 2.3% for this year, having reached 4.3% in 2021. These growth numbers may sound healthy enough but, given the rise in energy prices, they are in fact mediocre. The Russian Ruble would usually benefit substantially from rising energy prices but has already declined 5% since peaking against the US Dollar in October. Russian foreign currency debt credit spreads have widened, and local interest rates have risen sharply. Russia’s financing costs face an even worse outcome if war breaks out. Russia’s citizens are unhappy, and the prospect of a war that threatens to kill or injure many young Russians is likely to make them even less so. Given this economic backdrop, we suspect Putin’s posturing will remain just that. Should there be an actual armed conflict, Russia needs to be as short-lived and containable as possible.

Events can change dramatically from one day to the next, however, we believe that current markets have already priced in the risk of a worsening of the Ukraine conflict within the confines described above.

As we mentioned at the beginning, markets face a more substantial threat from policy tightening by central banks and governments. It may seem odd but if the Ukraine tension drags on or worsens, policymakers will feel less obliged to depress economic sentiment further.

Regular readers of our blogs will understand that markets are particularly volatile now and have been for a few months, mainly due to the policy changes from Central Banks and Governments.

In the circumstances we just need to remain invested, think about your long-term objectives and look through this short-term volatility.

If you are regularly monthly funding Pensions and Investments the volatility could help over the long-term too, ‘Pound Cost Averaging’ (see previous blogs).

Finally, Fund Managers use this volatility to buy good quality assets at the right price – ‘Active’ Fund Management.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from ourselves and leading investment houses.