Please see the below article from Invesco, analysing the potential effects on equities and global markets from the possible outcomes of the developing situation in Ukraine. Received yesterday afternoon – 03/02/2022.

Russian financial markets have had a nasty ride of late as a result of yet more geopolitical intrigue. The MSCI Russia Index is off 26% from the peak in October 2021, while the ruble has slid 9.9% against the US dollar over the same period.

This retreat has occurred against a very favourable backdrop for Russian economic growth, earnings and the currency, with crude prices comfortably north of $80. Pain has been particularly concentrated in stocks that have heavy international ownership, typically growth companies, as opposed to large commodity companies, which are predominantly owned by domestic investors attracted to generous dividend yields.

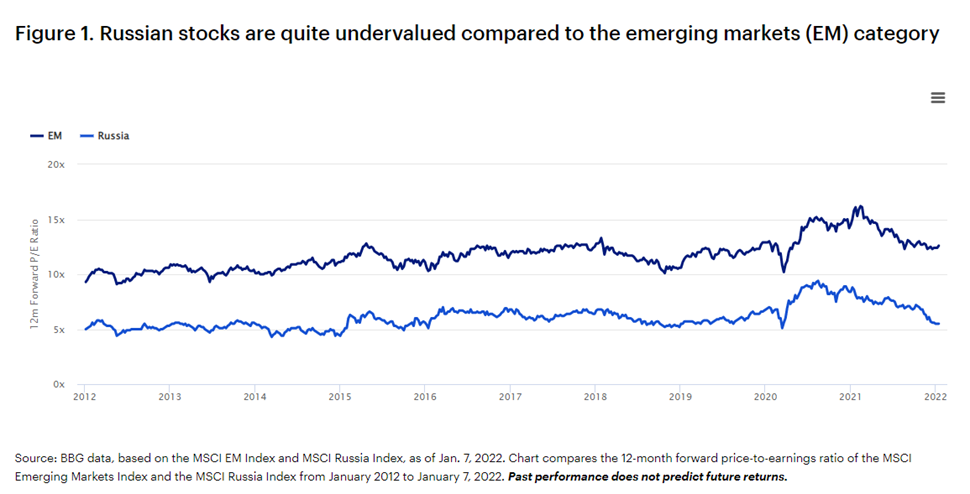

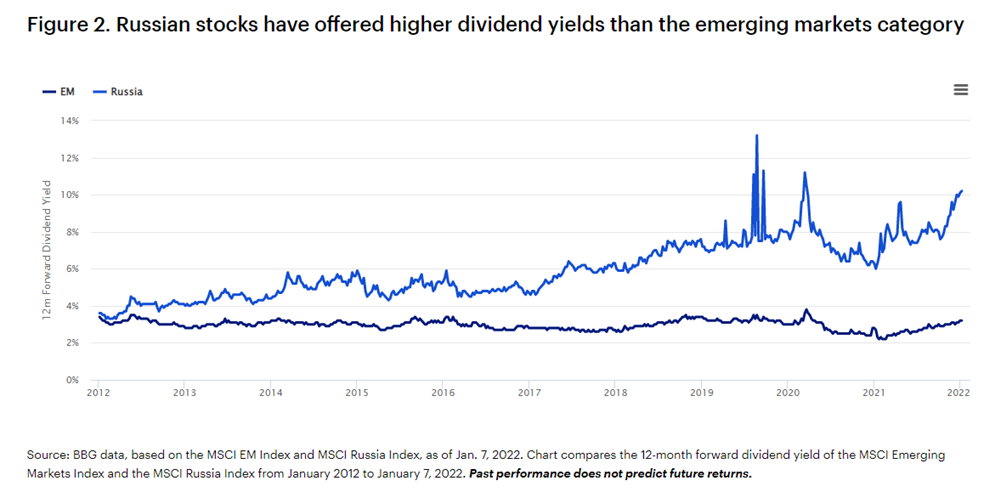

Today, Russian equities are broadly very cheap! (See Figure 1) The Russian equity bourse is trading at 6x its price-to-earnings (P/E) ratio for the trailing 12 months, clearly the least expensive of any significant bourse worldwide. The entire market, defined by the MSCI Russia Index, is also today offering a 7% dividend yields.

We would also note that Russia is that rare beast with fortress-like macroeconomic strength. It has built up a war chest of $631 billion international reserves, equivalent to 37% of gross domestic product (GDP), has a tremendous current account surplus (7% in 2021) and very low levels of public debt (19% of GDP).

Below, the Invesco Developing Markets team outlines our views on what the Kremlin wants, what the West can possibly concede, and four scenarios on how this could play out — two optimistic and two pessimistic.

It is noteworthy that the most adverse, and in our minds least likely, scenarios would have symmetric punitive implications for both Russian stocks and the entire global equity space — the world economy would likely fall into deep stagflation and equities worldwide would be hammered by massive inflation under the pessimistic scenarios.

Hence, we believe a bet on Russian stocks at these levels is not so different from a bet on the health of global equities more broadly.

What does Moscow really want?

Moscow has threatened a “military solution” to the Ukraine stalemate, in the advent of failed diplomatic efforts. This is backed up with the credible mobilisation of troops alongside the Russian border. In parallel, the Kremlin has presented an aggressive and perhaps deliberately unacceptable, list of demands to Western leaders and the NATO alliance.

So, what does President Putin really want? In our view there are two interwoven broader concerns for Russia: regional security and domestic political legitimacy.

Four waves of NATO enlargement have been widely perceived in Moscow to be in violation of the tacit promises that followed the dissolution of the Soviet Empire. The long-stalled inclusion of the Ukraine (and perhaps Georgia) in NATO is simply unacceptable from Moscow’s perspective.

Therefore, Moscow’s principal demand is for regional security – a permanent denial of NATO membership to Ukraine (and other former Soviet states) and explicit restraints on NATO military exercises, troops and military infrastructure in the region.

Second, Moscow finds the endless “colour revolutions” and regime change pressures, including recent pressures in Belarus and Kazakhstan, unacceptable. These have adverse implications for regional security and domestic legitimacy for the leadership in Moscow.

A visible retreat in support for the Putin administration has amplified these concerns since the painful economic malaise that followed isolation (and sanctions) during 2014-16.

Why now?

Russia perceives it is in a position of considerable strength here. Recent disturbances in neighbouring Belarus and Kazakhstan have reinforced motivations. The Ukraine is slipping into the status of a failed economic (and governance) state.

Washington and Brussels have neither the capacity, nor the charity, to bail out Kiev from its economic debts. The West also has no appetite for military confrontation over the Ukraine.

Talks of “devastating” further sanctions seem largely fictional given the painful self-inflicted repercussions this would have on the global economy and in particular Western Europe. In essence, reflexive financial sanctions are beyond fatigue.

A denial of Russian access to the SWIFT payments system is clearly off the table as it would result in the inability of other nations to pay for Russian energy. Such sanctions would likely immediately send the global economy into massive stagflation, with a painful and likely dramatic rise in energy prices and subsequent recession.

Additionally, it is worth noting that, unlike Iran, who suffered the fate of excommunication from SWIFT in 2012, Russia possesses the wherewithal to exact painful counter sanctions on Europe. It has the means to eventually replace SWIFT with their own System for Transfer of Financial Messages (SPFS), which would be relied upon for payments of Russian hydrocarbons.

More serious sanctions could target large Russian banks, but this too would risk unsettling commodity payments, as it did with aluminium in 2018. In the end, we believe the death knell to many of the “nuclear” sanctions proposed will be Europe’s increased dependence on Russian exports of oil and natural gas over the last decade. Russia now provides 46.8% of Europe’s natural gas imports, up from 30% 10 years prior.

The ubiquitous use of financial sanctions as the simple go-to US foreign policy tool could also erode US dollar privilege as the world’s reserve currency, a very critical element in US strategic power. Thus, Western leaders are left sailing between the Scylla and Charybdis.

Multiple scenarios

The world is too dynamic and we are too humble to pronounce any prescient judgment. (We would also point out that those less humble in pontification are often wrong and generally unaccountable!) But in our view, there are four scenarios:

- Invasion/conflict escalation

- Concessions

- A grand deal

- Stalemate.

Each of these four outcomes has multiple permutations.

Optimistic scenarios

The most optimistic scenario would be some sort of grand deal that would exchange Russian regional security (embellishment of the Minsk Accords, restraints on eastward NATO expansion, and tolerance for Russia’s historical sphere of influence) for Ukrainian sovereignty and broader collaboration (new nuclear and tactical arms agreements and global collaboration in areas of Russian influence, including the Near East, Central Asia, and sub-Saharan Africa).

Perhaps this would also involve re-embracing Russia (repealing sanctions over time) into the West, stunting its tilt toward China over the past decade. This would be an enormous diplomatic coup for the West in the real historical narrative, which is checking the rise of China.

Another hopeful scenario would be making acceptable concessions to Moscow in exchange for some respite in tensions. However, this would come up against domestic political constraints in the West — particularly in the United States.

President Biden is already tarnished from chaotic abandonment of Afghanistan and could be attacked as “weak” on autocrats. Appeasement also has historically toxic connotations across Western Europe, particularly in London.

Pessimistic scenarios

Stalemate and conflict are interwoven scenarios. Broadly, it seems to us that these are widely considered the high-probability scenarios in both policymaking circles and financial markets.

Conflict can take many forms, as recent cyber-attacks have demonstrated. And stalemate can also take many forms from benign to periodic, erratic escalation.

Invasion itself is not a straightforward and decisive outcome. Seizure of the entire state is highly unlikely, given the sheer volume of manpower necessary to occupy and resist uprise for a prolonged period.

The 100,000 men stationed north of Ukraine already represent roughly 10% of the combined active and reserve personnel of the Russian Armed Forces. A prolonged occupation would necessitate an increase in Russian defense spending; a figure that already accounted for nearly 15% of annual expenditure in 2020. Should oil revenues fall – a guarantee should Russia move forward with invasion, given almost 50% of exported oil went to OECD Europe – it will have no means to finance its occupation.

Investment implications

As we’ve articulated before, while it is important to understand the implications of geopolitical or macroeconomic events, we believe long-term investors are best served by avoiding short-term, tactical decision-making. Instead remaining focused on identifying companies with sustainable competitive advantages and real options that can manifest over time.

We believe these types of opportunities offer investors the greatest potential for compelling results over time.

Please continue to check back for a range of relevant news and blog content from us and from some of the world’s leading fund management houses.

Alex Kitteringham

03/02/2022