Please see the below update from Brewin Dolphin received late last night:

Many global markets have fallen over the past week, thanks largely to a sell-off on Monday – the first trading day of the year. While many markets finished 2020 at all-time highs, uncertainty around the new Covid-19 variant, surging case numbers, and new lockdowns have dented optimism.

Hopes are now pinned on the mass vaccination programmes underway around the world.

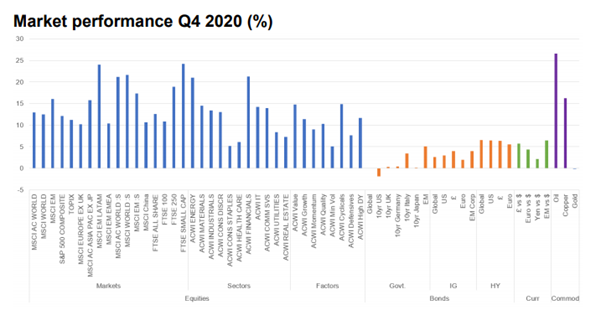

Despite the pandemic, 2020 ended up being a surprisingly good year for a number of markets. The S&P500 ended the year up by 16.3%, while the Nasdaq gained 44%. In the UK, however, the FTSE100 endured its worst year since the financial crisis, losing 14.3%. The UK’s blue-chip index is heavily weighted towards stocks that were hit hardest by the pandemic, including banks and energy companies. It also has very little exposure to the tech sector, which has had a stellar 12 months. Additionally, the FTSE100 has been hindered by a rising pound; since many companies in the index earn their revenue in US dollars, a strong pound reduces their earnings when converted into sterling.

The performance of other markets varied widely. Germany’s DAX index ended the year up 3.6%, which may not sound much but it did pass its previous record high.

France’s CAC 40 fell by around 7%, while Japan’s Nikkei gained 16%. In China, the CSI300 rose by 27% during 2020.

Last week’s markets performance*

- FTSE100: -0.46%

- S&P500: -0.70%

- Dow: +0.36%

- Nasdaq: -1.18%

- Dax: -0.25%

- Hang Seng: +3.4%

- Shanghai Composite: +3.66%

- Nikkei: -1.12%

*Data from close of business on Tuesday 29 December to close of business on Monday 4 January.

Equities in mixed start to new year

Global equity markets saw healthy gains on Monday as continued optimism about the vaccine rollout provided confidence.

However, the mood soured as the day wore on, and markets in Europe and the UK finished off their highs as it became clear that more lockdowns were imminent.

Relatively robust economic data out of China helped most Asian emerging markets at the start of the week.

In the region, the Shanghai Composite closed up by 0.86%, while Hong Kong’s Hang Seng gained 0.89%. South Korea’s KOSPI rose by 2.47% and Taiwan’s TSEC 50 gained 1.15%.

In Japan, however, the Nikkei lost 0.68%, as the government said that vaccinations may not start until February, despite surging cases.

In Europe, markets were up across the board. The German DAX eked out a 0.06% gain, while France’s CAC 40 rose 0.67% and the FTSE Mibtel in Italy rose 0.37%.

But it was the FTSE100 that outperformed on the day, rising by 1.72%, helped by a weak pound.

In the US, the mood was less upbeat, perhaps caused by news that the Covid-19 variant had arrived in New York, or perhaps the rumblings about more lockdowns in the UK and elsewhere had investors spooked.

Either way, US markets had their worst day since October, with the Dow losing 1.25% to close at 30,223.89, while the S&P500 fell by 1.48% to 3,700.65. The Nasdaq fell by 1.47% to close 12,698.45. It should be remembered the indices are still near their all-time highs.

New lockdowns announced or extended

Boris Johnson’s address to the nation on Monday night, in which he announced a strict national lockdown for England, set to last until at least mid February, has intensified the short-term headwinds now facing the market. Similar lockdowns have been announced around the UK, and also in Germany and Japan, with containment measures increasing in South Korea. Others are certain to follow.

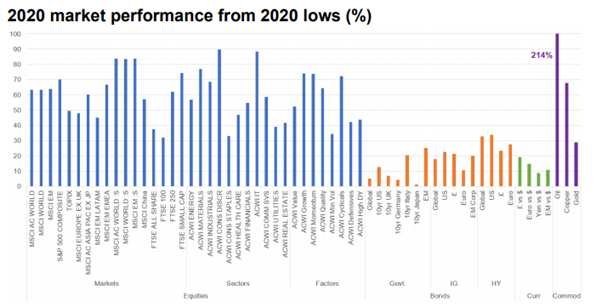

January is traditionally a tough month, and the current market wobble should be set in the context of the recent strong run. November 2020 was the best month for equities in 20 years, and December was also historically strong. It should be no surprise if the markets fall back in the near term. But fundamentals remain solid. There is a lot of money sitting on the sidelines waiting to be invested that has failed to find a home since the sell off last March. Only this time, we are at the beginning of a new business cycle and recovery, as opposed to last March, when we were at the tail end of an old cycle. So on a 12-month view, we remain positive.

Source: Refinitiv Datastream

UK economic data ends year on a high

The last business survey covering the UK’s manufacturing sector shows that factory activity was improving at the fastest rate in three years.

The IHS Markit/CIPS purchasing managers’ index rose to 57.5 in December from November’s 55.6. Any reading above 50 indicates activity is increasing. The rise was due largely to stockpiling by manufacturers ahead of the Brexit deadline, in case a deal was not reached. It may therefore drop back in the near-term as the lockdowns bite and activity reduces.

UK mortgage approvals are also booming, with 105,000 mortgages approved in November – the highest since 2007, before the credit crunch kicked in. Buyers are rushing to take advantage of the stamp-duty holiday announced by Chancellor Rishi Sunak, which expires in March. It is likely that activity will calm down in the summer.

Please continue to check back for more brief market views from a range of different fund managers. This should help you get a handle on the fast changing outlook.

Andrew Lloyd

06/01/2021

{kind=link}

{kind=link}

{kind=link}

{kind=link}