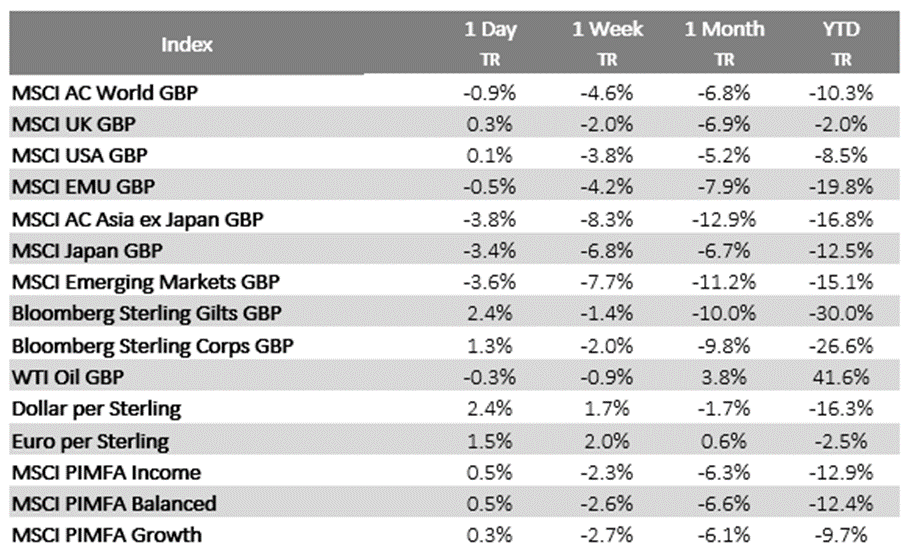

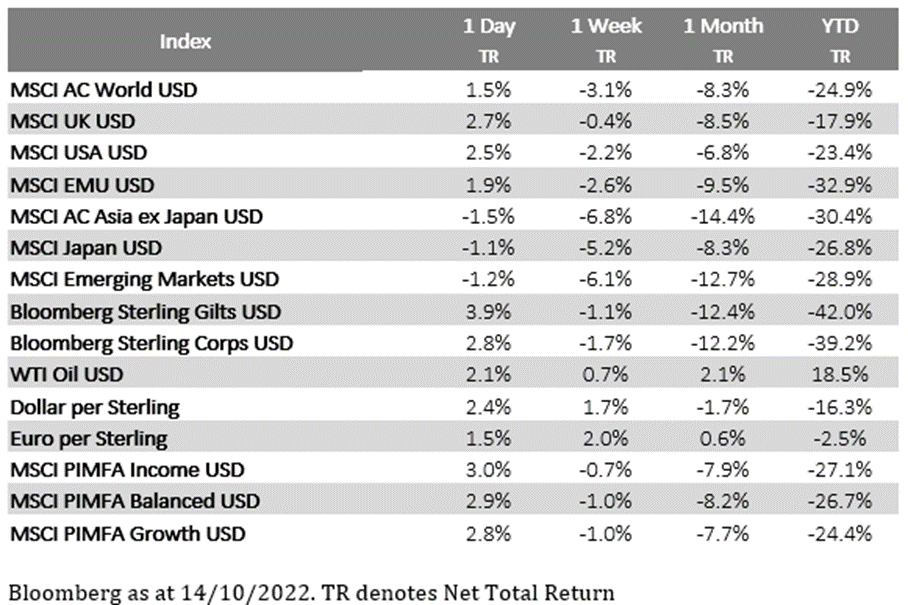

Please see the below article from Brewin Dolphin, highlighting the economic impact of the government U-turn on freezing corporation tax, and the effect this is having on markets. Received late Friday afternoon – 14/10/2022.

Prime minister Liz Truss has reversed the decision to scrap the planned rise in corporation tax. Guy Foster, our Chief Strategist, discusses the impact this could have on financial markets.

Prime minister Liz Truss has announced a second major mini-budget U-turn and the departure of chancellor Kwasi Kwarteng following weeks of market and economic turmoil.

Plans to scrap next year’s increase in corporation tax will no longer go ahead and the role of chancellor has now been filled by former health secretary Jeremy Hunt. Chris Philp is no longer chief secretary to the Treasury and has been replaced by Edward Argar, former paymaster general.

Background

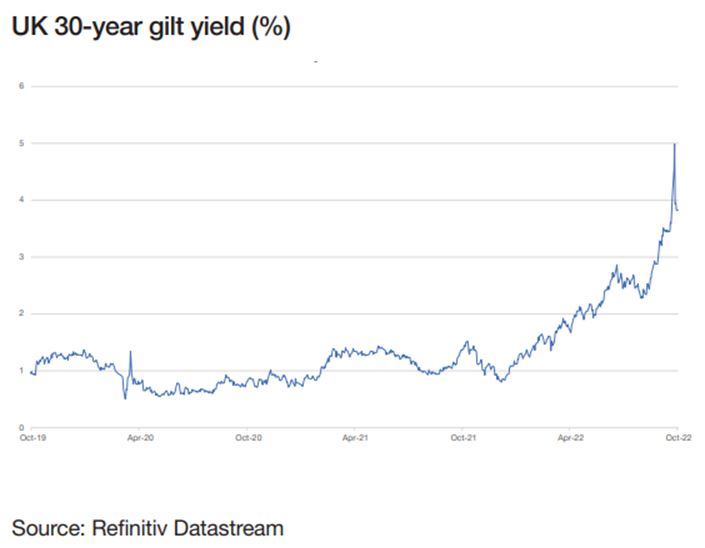

Today’s statement comes after the mini-budget on 23 September resulted in a steep decline in UK government bonds (gilts) and the pound, widespread stock market volatility, and lenders pulling mortgage deals from the market. The mini-budget included a much bigger package of tax cuts than had been expected, raising concerns about a surge in government borrowing and more aggressive interest rate hikes. According to the Institute for Fiscal Studies (IFS), the tax cuts would have cost the Treasury almost £45bn a year1 , contributing towards an £80bn increase in borrowing by 2026/27.

One of the biggest measures in the mini-budget was scrapping the planned increase in corporation tax from 19% to 25%. Today’s U-turn means the increase will now go ahead in April 2023, saving the government around £18bn a year, Truss said.

The government had already announced on 3 October that it was scrapping plans to axe additional-rate income tax. Removing the 45% tax rate would have cost about £2bn a year according to the government, or £6bn a year according to IFS estimates.

How are markets reacting?

Bond and share prices rose ahead of Truss’s statement as speculation about the corporation tax U-turn mounted. There were large swings in the value of the pound as traders digested the sacking and replacement of the UK chancellor.

The market’s reaction was somewhat tempered by the fact that a tax cut U-turn had been widely anticipated. Borrowing costs have, however, fallen this week as speculation continued to mount.

Today’s stock market rally came in the context of markets which were higher globally as the news was announced. This largely reflected a strong performance on Wall Street following the latest US inflation figures. Speculation about the return of the corporation tax hike did cause some volatility among companies with particularly significant UK operations, such as banks, housebuilders and some retailers, who are now facing higher tax bills.

What is the longer-term outlook?

Speculation about the U-turn had already seen UK borrowing costs fall and the new chancellor will be aware of the need to emphasise fiscal sustainability as many of his predecessors were too. It would not be surprising to see the return of self-imposed fiscal rules, which serve as guard rails to keep policy on track, and which give investors a sense of how policy will develop. These form part of the economic orthodoxy that had been shunned by this government, despite being seen as an essential policy signal by previous governments.

The latest period of turbulence could worry investors that one benign economic strategy can quickly be replaced by another they find more alarming. However, it should also reassure them that it demonstrates how the government of the day is accountable to its party, the electorate, and the Office for Budget Responsibility. An independent Bank of England will support the financial system without interfering with policy. And these institutional protections mean that change can be forced to retain the confidence of the markets. That is not true of all countries and should enable the UK to quickly regain investors’ confidence.

This is a turbulent time for the government, and we expect further changes to be announced today by our new chancellor.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

17th October