Please see below, an article from EPIC Investment Partners which analyses the latest inflation figures in the UK. Received today – 24/10/2025

September’s figures show that UK inflation remains stubbornly high at 3.8%, nearly double the Bank of England’s target. Not only does the prospect of further interest rate cuts display wilful disregard of the MPC’s 2% mandate, this inflation number is also understated.

The Consumer Price Index (‘CPI’) is used by governments to set inflation targets and adjust other measures such as state pensions and benefits. It also impacts interest rates, wages and other payments, and is intended to show how inflation affects household budgets. The CPI measures inflation by tracking the average change over time in the prices of a basket of goods and services purchased by a typical household. The Office of National Statistics collects prices for about 700 different items like food, energy, and clothing, to create a “shopping basket”. They then track the price changes of this basket over time to calculate inflation. However, this is a flawed measure of price rises as it excludes housing costs, unlike the more complete Retail Price Index (‘RPI’).

CPI is generally lower than RPI, an older measure that includes owner-occupier housing costs like mortgage interest payments and council tax. But does either measure provide a true reflection of the cost of living? My friend in the US has just sent his Microsoft Excel subscription renewal statement – an increase from $69.99 to $99.99. Those of us unfortunate enough to occasionally grace a supermarket, or fortunate enough to occasionally visit restaurants, can bear witness to exponential price increases that appear divorced from official CPI numbers. And, of course, there is taxation, which apart from excise duties and sales taxes that directly affect prices paid, are excluded from both indices. My American correspondent also points out that their CPI used for index linking excludes both food and energy!

Even compound inflation of 3.8% halves the purchasing power of a currency in 18 years, and a Pound will have lost 75% of its current purchasing power before my newly born grandson reaches the age of thirty-five. Now let’s look at the real erosion of what our currency will buy. Prices including owner occupiers’ housing costs, (CPIH) rose by 4.1% in the 12 months to August 2025, and of course this might not accurately reflect the inflation rate for individuals with different spending habits, such as a retired person with higher healthcare costs, or a family with young children. While necessary for a consistent measure, methods like “substitution bias” (which assumes consumers switch to cheaper alternatives when prices rise) can also lead to an underestimation of the impact of rising prices on specific goods.

As we can see, inflation is a complex topic, and different individuals may feel that their personal experience of rising prices is higher than the official CPI figure, particularly in specific sectors like housing or energy. However, these marginal differences do not seem to explain our individual perceptions of changes in the cost of living. Some basic arithmetic can help: if we focus on the underlying index of prices as opposed to individual annual increases, we might find an answer.

Following Covid, the annual CPI figure rose to high single digit percentages from which it has now fallen back to below 4%. However, this 4% figure is in addition to previous price rises. I will use a basic set of assumptions to make the point. A £100 product price, inflated by 4% rises to £104. However, if preceded by a several years of high levels of compounding inflation, 4% is multiplied by a much larger number. If we use the CPI to measure inflation, just over the past five years, prices as measured by the CPI are now over 28% higher than at the beginning of 2021. 4% inflation this year takes the price index from 128 to nearly 135, and so a further 7%, measured in 2021 prices. This figure sounds closer to what many seem to be experiencing, and by unhappy coincidence reflects some commentators’ estimates of real underlying inflation both here and in America.

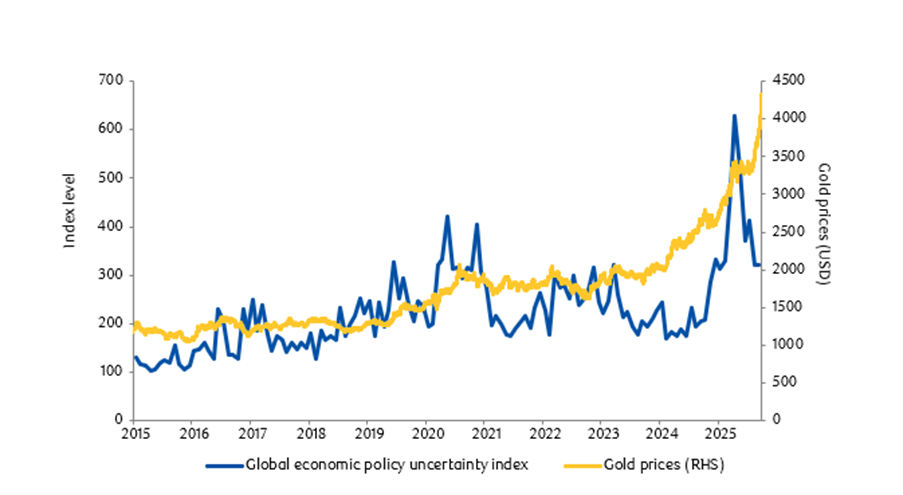

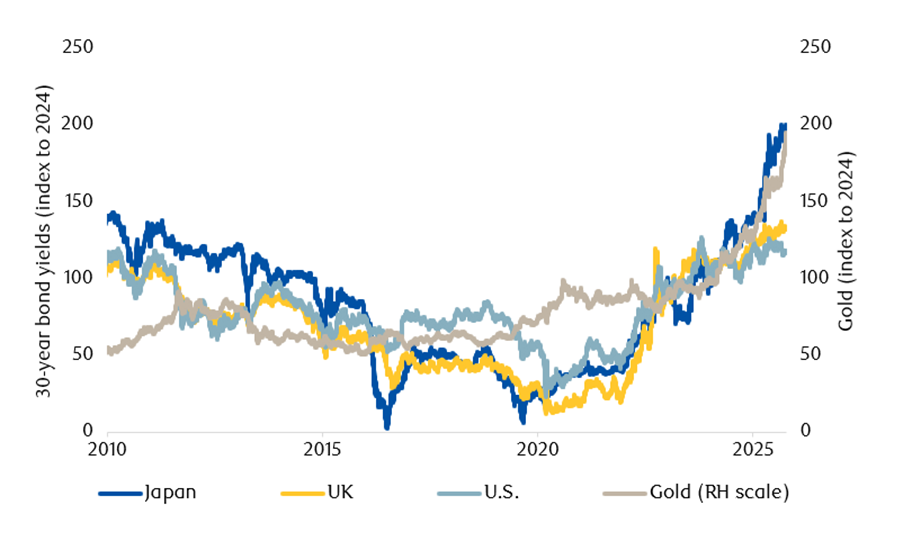

Whatever the arithmetic applied, strong signals being given by the commodities markets point towards fears of accelerating FIAT currency debasement. A return to 1970s inflation levels would see the Dollar lose a further 75% of its purchasing power in a decade – this in addition to the 95% erosion of the currency’s value since 1913.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Alex Kitteringham

24th October 2025