Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

Markets bounced on Monday, but only partly unwinding the bigger falls from Friday. For the US S&P500 and the pan-European STOXX600, both equity indices still closed yesterday below where they had closed last Thursday. Furthermore, not all stocks saw a bounce – of particular note, US ‘Magnificent Seven’ megacap tech stock Amazon, which fell -8.27% on Friday, dropped a further -1.44% yesterday (all in local currency price return terms).

US dollar resumes its slide

The US dollar fell again yesterday, with the DXY index (which tracks the dollar against a basket of major global currencies) down for the second day in row. For context, while the DXY index had a relatively good July, its best month since last year, that was only on the back of the dollar suffering its weakest calendar 1H performance since 1973. Trying to make sense of the moves, some market watchers are suggesting that dollar weakness this year is in part reflecting ebbing investor confidence in owning US assets given US President Trump’s tariff policy consequences in particular.

Trade tariff escalation

US President Trump threatened higher trade tariffs again India yesterday, saying that he would be “substantially raising” tariffs on India’s goods coming into the US because of India’s continued willingness to buy oil from Russia. That would be over and above the 25% tariff rate on India announced last week. India’s stock market has been weak recently, arguably reflecting a marked recent deterioration in US-India relations. Highlighting the war of words, Trump said last week that if India maintains its close ties with Russia, then “they can take their dead economies down together”.

What does Brooks Macdonald think

According to data complied by the ‘Washington Service’ research company and reported by Bloomberg, only 151 US S&P500 constituent company executive insiders bought their own shares in July, the fewest in a month since 2018. Furthermore, the ratio of insiders’ buying-to-selling was the lowest in a year. While it is important not to try to read too much into one month’s data, a cautious stance among those that likely know their businesses best might be signalling concerns around either relatively high valuations and/or slower economic growth expected ahead.

Please check in again with us soon for further relevant content and market news.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 04/08/2025

Busy going nowhere

This week has been one of the most information-heavy in recent memory, with significant implications for global markets. Equity markets began positively but turned negative, particularly in Europe. US indices fared better, buoyed by the Magnificent Seven tech giants, though Friday’s ISM manufacturing survey revealed unexpected weakness, dragging domestic stocks lower.

Bond yields fluctuated, ultimately falling sharply, while the dollar strengthened through most of the week before retreating post-ISM data. Currency movements amplified US equity outperformance until Friday’s reversal. In sterling terms, France’s CAC40 fell 3.4%, while the Nasdaq 100 rose 0.7%. Gold weakened slightly, and commodities ended the week poorly.

Markets have shifted to a risk-off stance, with defensive global quality stocks—especially tech—attracting attention. The week’s agenda was packed: trade negotiations ahead of Trump’s tariff deadline, central bank meetings, GDP and inflation data, confidence indicators, employment reports, China policy updates, and Q2 earnings from major firms.

The EU-US trade deal initially appeared constructive, mirroring Japan’s agreement. However, discrepancies—particularly around pharmaceuticals—surfaced, casting doubt. European equities, notably autos, rallied briefly before faltering. Macron’s criticism of the Commission further undermined confidence.

GDP data disappointed, with the Eurozone posting just +0.1% q/q growth. The Euro weakened significantly. Some countries portrayed trade outcomes as victories, though Mexico and China secured extended negotiations due to their leverage. Trump’s approval on economic handling has declined, prompting aggressive tariff hikes on Canada and Switzerland. The UK, by contrast, emerged relatively unscathed.

While tariffs are unpopular, they may aid US fiscal sustainability. Investors remain concerned about the deficit, evidenced by rising bond risk premia. The Treasury’s funding plans were announced, but the timing of tariff shocks—amid a fragile labour market—poses challenges.

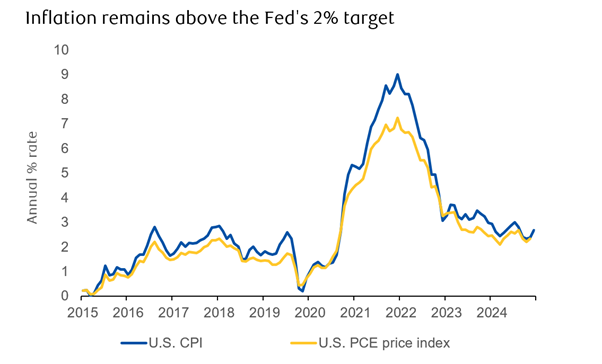

The Fed held rates steady, acknowledging contained inflation but warning of future rises due to tariffs. Labour market data showed weak job growth but strong wage increases, suggesting supply constraints. Trump’s renewed attacks on Fed Chair Powell added to market tension, pushing yields higher.

Despite European struggles, US indices benefited from strong Q2 tech earnings. Apple’s rebound in China underscored the region’s importance. Nvidia’s results are awaited later in August.

Bills and bonds

In summary, while Q2’s policy upheavals have settled somewhat, August may bring renewed volatility. Tariff-driven price rises in the US feel imminent, and markets are increasingly uncertain about a smooth resolution.

The surge in government debt issuance has long been a focal point for asset strategists and portfolio managers. This week, the US Treasury outlined its financing plans, revealing that despite a projected $1.98 trillion rise in debt to $37.2 trillion by year-end (per the CBO), the bulk of this will be financed through short-term Treasury Bills (T-bills).

Why the preference for short-term debt? The Treasury faces a delicate balancing act: attracting investors without overburdening future cash flows. In uncertain times, T-bills—essentially short-term cash equivalents—are more appealing due to their lower capital risk. Demand for longer-dated bonds has weakened, prompting both current Treasury Secretary Scott Bessent and his predecessor Janet Yellen to favour short-term issuance.

This shift reflects investor sentiment. Since 2021, preferences have tilted toward liquidity, though there are signs of easing aversion to maturities up to five years. For the Treasury, this means lower interest costs in the near term. The term premium—the excess return investors demand for holding longer maturities—has narrowed slightly, reinforcing the appeal of short-term funding.

However, this strategy carries risks. Short-term debt is more sensitive to interest rate fluctuations. A shock to price stability or supply could drive rates higher, immediately increasing borrowing costs. With Trump’s second-term policies continuing to disrupt supply and pressure inflation, the risk is non-trivial.

Critics argue that the growing reliance on T-bills increases financial fragility. Bloomberg’s Simon White notes that the US debt maturity profile is now more vulnerable to rate hikes. While short-term debt still comprises only 20% of total issuance—broadly in line with historical norms—the rising debt-to-GDP ratio limits fiscal flexibility unless maturities are extended.

An additional concern is the quasi-monetisation of debt. Michael Howell of CrossBorder Capital suggests that increased T-bill issuance may be indirectly funded by the Fed, via commercial banks’ large cash reserves—remnants of pandemic-era stimulus. Regulatory inconsistencies have discouraged banks from holding T-bills, but reforms proposed by Bessent could redirect this liquidity.

If the Treasury taps this reservoir, it could fund more spending than forecasted—potentially stoking inflation. The Fed, already under political pressure, would face a difficult choice: tighten policy or risk its independence.

In sum, while short-term financing offers immediate savings, it leaves both policymakers and investors more exposed to future shocks.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see the below article from EPIC Investment Partners, analysing the latest interest rate decision by the Federal Reserve. Received today – 01/08/2025

The Federal Reserve’s decision on July 30, 2025, to maintain the federal funds rate at 4.25%–4.50% revealed deep divisions marked by a rare double dissent. Governors Christopher J. Waller and Michelle W. Bowman argued for an immediate 25-basis-point rate cut, reflecting sharp disagreements over tariff impacts and labour market conditions.

Chair Jerome Powell and the majority consider recent tariff-induced inflation as potentially temporary, cautioning against premature easing that could undermine price stability. Powell cited the stable 4.1% unemployment rate as evidence of labour market resilience, supporting the Fed’s restrictive policy stance.

Yet, recent labour data paints a more nuanced picture. July’s ADP payroll report showed private-sector employment increased by 104,000, surpassing forecasts but indicating a slowdown. Notably, small businesses added only 12,000 jobs, highlighting ongoing vulnerability due to high borrowing costs and tariff-driven price pressures.

Governor Waller emphasised underlying fragility, asserting the labour market is approaching “stall speed.” He warned that superficial job growth numbers obscure deeper economic weaknesses.

Governor Bowman’s dissent highlights additional concerns, particularly within smaller community banks serving small businesses. Bowman argues that tariff disruptions, initially viewed as temporary, are now causing sustained economic distress, justifying immediate action by the Fed.

This mix of moderate employment growth and rising inflation poses a policy challenge. Tariffs raise the risk of stagflation—higher prices coupled with slower growth. Powell’s cautious approach prioritises inflation control, but dissenters argue continued restrictive policy could unnecessarily deepen economic slowdown risks.

Markets initially perceived Powell’s message as hawkish, resulting in modest stock declines and rising Treasury yields. Analysts remain divided, with Powell’s backers expecting tariff impacts to fade quickly, and dissenters seeing deeper vulnerabilities that require immediate easing.

Political factors complicate matters further. Waller and Bowman, appointed during the previous Trump administration, echo the President’s calls for lower interest rates, raising concerns about Fed independence as Powell’s term nears its May 2026 expiry.

Today’s nonfarm payroll release has significant implications. Weak numbers would bolster the dissenters’ argument for immediate easing, while stronger figures would validate Powell’s cautious “wait-and-see” stance.

As Governor Waller succinctly put it, “Waiting for undeniable weakness means waiting too long.” Today’s payroll data may be pivotal in shaping the Fed’s next move.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see the below article from EPIC Investment Partners detailing their discussions on the US economy. Received this morning 31/07/2025.

While the overall US consumer debt delinquency rate remains lower for upper-income households compared to other groups, a notable and concerning trend has emerged: delinquencies across all loan products for households earning over $150,000 per year have more than doubled since 2023. This is a significantly sharper increase than for middle- or lower-income households, suggesting that even those with substantial earnings are beginning to feel the pinch of economic shifts. Despite this acceleration, the actual delinquency rate for this group remains relatively low at around 0.34%, but the rapid upward trajectory is a red flag, indicating that a broader segment of the population might be struggling with rising costs and potentially stagnant real wage growth.

This strain on upper-income consumers comes at a time when consumer spending, which accounts for roughly two-thirds of US GDP, has seen its tamest growth in consecutive quarters since the pandemic. In the second quarter of 2025, consumer spending rose by a modest 1.4%, a deceleration from previous periods. While the overall US GDP did rebound to a 3.0% annual rate in Q2 2025 after a Q1 contraction, this was significantly influenced by a decrease in imports and an acceleration in consumer spending on durable goods and services. However, a deeper look reveals that “real final sales to private domestic purchasers” – a measure stripping out trade and government spending – increased by a more subdued 1.2% in Q2, down from 1.9% in Q1.

This subdued consumer spending growth, coupled with the rising delinquencies among higher earners, points to a potential underlying fragility in the US economy. While overall job growth has continued and consumer confidence saw a slight improvement in June, there are signals of caution. The deceleration in personal consumption expenditures and the increasing financial strain on a segment of the usually more resilient upper-income bracket suggest that consumers may be reaching a breaking point after a sustained period of high spending and rising debt. This could lead to a further slowdown in the vital consumer spending engine, impacting future GDP growth, and prompting a re-evaluation of the economic outlook.

Separately, as expected, the FOMC maintained the fed funds rate target range at 4.25-4.50% yesterday. The decision was not unanimous, with two members, Waller and Bowman, dissenting in favour of a 25bps cut, suggesting a growing dovish sentiment within the committee. Futures markets are forecasting one rate cut this year, amid a cooling labour market and restrictive current rates. However, these anticipated cuts could be delayed into 2026. We await the Fed’s favoured PCE readings, and the personal income and spending figures this afternoon.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 29/07/2025.

Japan and the EU secure U.S. trade deals

Guy Foster, Chief Strategist, discusses newly announced trade deals between the U.S. and Japan and the European Union. Plus, our Head of Market Analysis, Janet Mui, analyses the European Central Bank’s latest interest rate decision, and the prospect of further cuts.

Key highlights

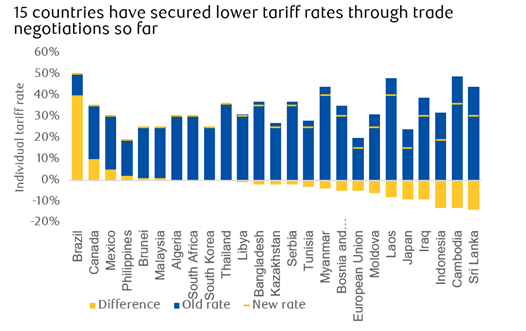

Japan and EU secure U.S. tariff deals: Japan and the European Union have successfully negotiated a 15% tariff rate with the U.S. The deals include cars, which is an improvement on the Trump administration’s previously announced 25% global auto tariff.

Will the Federal Reserve hold interest rates? The central bank is expected to maintain its federal funds rate at 4.25% to 4.5% this week as the U.S. economy and inflation have been holding up.

Eurozone outlook remains uncertain: The European Central Bank held its deposit rate at 2%, as expected. However, the future direction of interest rates will depend on how the tariff drama between the U.S. and European Union plays out.

It was a quiet week in the markets as investors began to head off for the summer, taking some liquidity with them. Earnings season hit full stride, and the reports were generally good, providing some support to indices.

The general backdrop was somewhat supportive, with additional trade deals announced at lower-than-expected tariff rates. Trade deals haven’t resulted in a pivot back to the low tariff environment that existed before President Trump returned to power, but they have reduced uncertainty about the future trading environment. This is evident in a reduction in the VIX Index of expected volatility to the lowest level since 14 February.

Japan and the EU secure U.S. tariff deals

A number of trade agreements were reached over the last week, with the European Union (EU) and Japan being the most significant.

Both deals saw a reduction in the baseline tariff rate to 15%; Japan’s tariff rate was 24% on ‘Liberation Day’, and the EU had been threatened with a 30% rate at one point. The deal includes cars, which represents a significant improvement on the 25% global auto tariff previously announced by the Trump administration. Pharmaceuticals should also be covered, mitigating the effects of more tariffs due to come on the sector.

Source: RBC Brewin Dolphin

The U.S. has prioritised making commitments to inward investment a part of the deals. The White House announced that Japan will invest $550bn in a range of U.S. strategic industries, with the U.S. apparently retaining 90% of the profits from those investments. On the face of it, that seems an intolerably bad deal for Japan, so we await more details on exactly how, or why, this would happen. The EU is understood to have committed to $600bn of inward investment into the U.S. and the purchase of $750bn worth of energy products.

Overall, more trade deals appear to have been achieved with lower tariff rates compared to those announced on ‘Liberation Day’. Obviously, this still represents a significant increase from pre-Inauguration Day levels, which could weigh on growth by driving higher inflation. Despite this, the markets seem to have responded positively.

With days to go until the new tariff rates come into effect, many countries still haven’t come to agreements with the U.S., and President Trump has been vague about what the new universal tariff rate might be.

Will the Federal Reserve hold interest rates?

The president has continued to needle Federal Reserve (Fed) Chairman Jay Powell while maintaining that he has no intention to replace Powell before his term as chair expires in 2026. But President Trump and members of his administration continue to be critical of Powell in relation to monetary and non-monetary matters. In doing so, they seem to be normalising the idea that the president should influence monetary policy.

The Fed will announce interest rates this week. It seems highly unlikely that there will be any change because the economy and inflation have been holding up. However, interest rates are still expected to fall later in the year as the economy gradually loses further steam.

Source: LSEG

Eurozone outlook remains uncertain

The European Central Bank (ECB) has held its deposit rate steady at 2%, which was widely expected. However, the future direction of interest rates is uncertain and will depend on how the tariff drama between the U.S. and EU plays out.

If the U.S. imposes a 15% tariff on the EU, as is currently being discussed, it may negate the need for further rate cuts by the ECB. Markets are currently pricing in a better-than-50%-chance of a rate cut between now and March, despite the trade deal (without which the economic outlook would be more precarious.)

The ECB’s latest bank lending survey shows strong residential mortgage demand, suggesting that this interest rate-sensitive sector may not need additional stimulus. Meanwhile, recent data has shown an uptick in new orders in the Eurozone.

Despite improved sentiment towards the Eurozone, the French economy is likely to weigh on the upside. France has the second-largest government budget deficit in the region and is facing a debt crisis. The government has announced a package of spending cuts, tax hikes, and reforms aimed at shrinking the deficit, but these measures are unlikely to be passed into law due to political opposition. The budget deficit is expected to remain unchanged over the next couple of years, and developments in France are a reminder that the upside for the Eurozone should be limited.

Overall, while the Eurozone has shown signs of improvement, the ongoing tariff drama and challenges in France mean the outlook remains uncertain.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

Yesterday saw US and European equity markets largely unwind their earlier intraday-gains as investors focused on negative ramifications from the US-European Union (EU) trade deal that was announced over the weekend. The share prices of German auto makers, which are especially sensitive to US trade access, reflected the evolving investment mood that the EU had struck a weak deal: Volkswagen shares, which had surged over +3% in the opening minutes of yesterday’s session, ended up closing more than -3.5% down by the end of the day (all in local currency terms).

US-EU trade deal criticised

As we noted in our Daily Investment Bulletin yesterday, the 15% tariff rate that will now apply to most EU trade going into the US is significantly higher than the average trade-weighted pre-existing US tariff rate of under 2%. While European Commission President von der Leyen had previously conceded the deal “was the best we could get”, yesterday saw French Prime Minister (PM) Bayrou label it “a dark day” and a “submission” for the EU, while Hungarian PM Orbán called von der Leyen a “featherweight” negotiator, adding “[US President] Trump ate von der Leyen for breakfast’.

US Federal Reserve meets

Yesterday sees the US Federal Reserve (Fed), arguably the world’s most important central bank, kick off its latest two-day policy meeting. The Fed announcement on interest rates is due out 7pm UK-time tomorrow evening, with a press conference starting 7:30pm UK-time tomorrow. While no change in interest rates is expected (the Fed’s benchmark interest rate target range of 4.25-4.50% has been unchanged so far this year), markets will instead be on the lookout for any signalling around possible interest rate cuts later this year, not least given the huge pressure that Trump has put on Fed Chair Powell recently to cut interest rates.

What does Brooks Macdonald think

It is a big week for stock markets, with a lot riding on the latest US megacap technology results in particular. Microsoft and (Facebook parent company) Meta have results tomorrow, while Apple and Amazon results are on Thursday, all coming out after the US trading close on each day. High hopes for Artificial Intelligence has powered broader US and global equity index performance so far this year, but with the aforementioned four megacap tech stocks currently accounting for around a fifth of the market-capitalised weight of the US S&P500 equity index, there is significant near-term two-way performance risk.

Please check in again with us soon for further relevant content and market news.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 28/07/2025

The Meme Generation

We start the week with another boost from a trade deal. The European Union has emulated Japan in securing a nearly-uniform 15% tariff on goods exported to the US. The signed agreement included autos, pharmaceuticals and metals (with a quota) but this may have surprised Trump, and that might lead to interpretation difficulties later. Equity markets have greeted it cordially at the open.

Last week, UK economic data releases showed that June’s retail sales rose just 0.9%, failing to recover from May’s sharp drop. Consumer sentiment dipped slightly, and government borrowing widened to £20.7bn, above expectations. Households appear to be saving more, possibly in anticipation of the autumn budget. While this caution isn’t recessionary, it reflects a hesitant mood. Increased savings may be supporting UK equities and giving the Bank of England room to lower rates despite persistent inflation.

In the US, Donald Trump has intensified criticism of Fed Chair Jerome Powell, blaming him for economic weakness due to “high” interest rates. Although Trump lacks the power to remove Powell, he may use the Fed’s $3bn HQ renovation overrun as political leverage. Despite tensions, Trump recently visited the Fed and downplayed any desire to oust Powell—likely keeping him in place as a convenient scapegoat.

Japan’s Prime Minister Ishiba faces mounting pressure after his coalition lost its upper house majority. Despite securing a trade deal with the US—imposing a blanket 15% tariff on Japanese exports but sparing cars from a harsher 25% rate—his domestic support is waning. Japan also pledged $500bn to support US industry, with spending decisions left to the US government. The Bank of Japan responded by reaffirming its hawkish stance, nudging the Yen higher.

Meanwhile, the European Central Bank held rates at 2%, with President Christine Lagarde suggesting the economy is in a “good place.” Markets now believe the rate-cutting cycle may be over.

Back in the US, retail investors—dubbed the “meme generation”—are targeting stocks disliked by hedge funds, using social media to coordinate buying. This disrupts short-selling strategies and drives up borrowing costs for hedge funds. While reminiscent of 2021’s frenzy, today’s meme stock activity is powered by profits from earlier trades and cheap options. Despite past underperformance, some meme stocks have delivered outsized returns.

Ultimately, meme investing is more game than strategy—high-risk, emotionally driven, and not unlike the hedge fund tactics of the 1990s. Still, it’s proving effective for now.

Platinum Prices Rising

While gold remains the most closely watched precious metal, platinum and palladium have seen a sharp price rise over the past year. Gold’s recent gains are tied to geopolitical and monetary uncertainty, particularly under Trump’s presidency. But, over the past two decades, the story for platinum has focussed on its use as utility and industrial use.

Platinum is extremely stable and unreactive, even more so than gold. Historically, its high melting point made it difficult to work with, delaying its widespread use in jewellery until the 20th century. Its real breakthrough came in the 1980s, when it became essential in catalytic converters to reduce vehicle emissions. Palladium followed a similar path, eventually surpassing gold in price at times due to its efficiency in catalysis.

However, their industrial use has also capped their price potential. Demand for platinum jewellery has declined over the past 15 years, and catalytic converters are now widely recycled—25% of platinum supply comes from recycled sources. The global shift to electric vehicles has further reduced demand, leading to falling mine investment and production. South Africa, which holds 88% of known platinum group metal reserves, saw a 7.7% drop in output in April 2025 and nearly 12,000 job losses in the sector.

Since 2022, platinum has faced a persistent supply deficit, projected to continue for at least five years. China remains the largest consumer, with industrial demand falling but jewellery and investment demand rising. Platinum is increasingly seen as a cheaper alternative to gold, especially after Trump’s metal tariffs prompted stockpiling in Chinese warehouses.

Recent data shows a slight dip in Chinese imports, suggesting inventory building may have peaked. Jewellery demand will be key to sustaining the rally. If consumer interest doesn’t match jewellers’ optimism, prices could fall by 20–30%. Yet, if just 1% of China-HK gold jewellery demand shifts to platinum, it could tighten global supply by over 2%.

With property investment out of favour in China and liquidity looking for a home, platinum—historically undervalued—may be poised for further gains.

The Oracle of Trading Platform Kalshi

Prediction markets are gaining traction in the U.S., with Kalshi recently raising $185 million at a $2 billion valuation, and rival Polymarket reportedly seeking $200 million. These platforms surged in popularity during the 2024 U.S. election and, following the Trump administration’s decision to drop legal actions against them, are poised to become a fixture in American finance.

Prediction markets allow users to trade contracts on the outcomes of real-world events. Though similar to betting, U.S. platforms like Kalshi and Polymarket argue their contracts are financial instruments, not wagers. U.S. firms can now claim regulatory ‘legitimacy’ —Kalshi is CFTC-approved, while Polymarket operates in a legal grey area.

These platforms use blockchain technology, with Polymarket accepting only cryptocurrency. Advocates say prediction markets offer a new asset class and powerful forecasting tools. The theory is that market prices reflect the collective probability of an event occurring, aggregating information more effectively than any individual could.

For investors, prediction contracts offer a direct way to hedge or speculate on specific events—such as geopolitical developments—without relying on indirect instruments like futures. For example, Polymarket allowed users to bet on the likelihood of Iran closing the Strait of Hormuz.

Despite their growth, legal uncertainty looms. Kalshi is being sued by several U.S. states that view it as a gambling platform. Polymarket, fined in 2022 for operating without a license, was raided by the FBI in 2024. However, the Trump administration has since dropped investigations into both firms, aligning with its broader deregulatory stance, including toward crypto.

This regulatory leniency has allowed prediction markets to expand rapidly. Kalshi contracts are now available on Robinhood, and some investors liken the sector’s potential to early-stage crypto. Yet risks remain. Prediction markets often suffer from low liquidity, making prices volatile and susceptible to manipulation. Prices can become self-reinforcing signals, creating feedback loops and undermining their reliability as forecasting tools. If widely adopted in financial hedging, these distortions could pose systemic risks.

Supporters argue that deeper markets will resolve these issues and democratize access to information. But with little oversight, prediction markets are entering a “wild west” phase—one that could end in innovation or casualties, as history has shown with other unregulated financial frontiers.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see the below article from EPIC Investment Partners detailing their discussions on the macro environment for trade, including the ongoing Trump Tariff saga. Received this afternoon 24/07/2025.

Global equities rose yesterday, as traders rode a wave of optimism following signs that the US is back in deal-making mode. Hot on the heels of a pact with Japan announced on Tuesday, markets are now buzzing with talk of similar moves with Europe and South Korea. The Stoxx 600 climbed 0.7%, while the S&P 500 and the MSCI World reached record highs. Risk-on is back, and traders are betting Washington’s bark may prove louder than its bite when it comes to tariffs.

But, behind the rally, not everyone is cheering.

President Trump’s Japan deal is being hailed by the White House as a model for others: a 15% tariff cap, sweetened by Tokyo’s promise of a $550 billion investment fund targeting US projects. Trump declared Japan’s markets “OPEN” for the first time ever. But, at home the backlash is growing. Critics say the deal hands Japan a free pass on autos — the very sector driving America’s trade gap with Tokyo — and risks undermining domestic manufacturing just as tariff pressure was starting to bite.

“Any deal that charges a lower tariff on Japanese imports with zero US content than on North American-built vehicles with high US content is a bad deal,” said Matt Blunt of the American Automotive Policy Council, voicing what many in Detroit are now thinking.

The agreement is also raising alarm among protectionists who see it as a crack in the armour of Trump’s Section 232 tariffs — long considered the most durable shield for US industry. Unlimited auto imports at a 15% rate? Steel and parts, though, still taxed at 25% and 50%? For some, it looks like the goalposts are moving — and not in America’s favour.

Still, the administration insists its strategy is working — cutting deals, cracking open markets, and keeping rivals guessing. Next stop: Stockholm, where US and China officials are gearing up for round three of trade talks.

Buckle up — trade season’s not over yet.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 22/07/2025.

U.S. inflation remains contained

U.S. core inflation has only been modestly impacted by tariffs so far, rising marginally month-on-month in June.

Key highlights

Boost for cryptocurrencies: U.S. Congress passed legislation to regulate stablecoins, paving the way for the potential broader use of cryptocurrencies.

Tariff costs and consumer price increases: the full impact of tariffs will unfold slowly, making it much harder for consumers to associate their loss of disposable income with tariff increases.

Rumours continue around Federal Reserve Chair’s departure: frontrunners to replace Jerome Powell include President Trump’s economic adviser Kevin Hassett, and former Fed governor Kevin Warsh.

Boiling frogs by design or accident?

Last week was busy, with earnings season really kicking off. The banks posted good numbers, buoyed by a lot of trading-related volatility during the second quarter.

Japan’s upper house elections saw the ruling Liberal Democratic Party-led coalition lose control of the chamber. It is now in the minority in both chambers, making Prime Minister Shigeru Ishiba’s position particularly tenuous as Japanese households struggle with the return of inflation. The yen rose on an expectation that a future government would provide more support to households, in turn requiring more contractionary policy (higher interest rates) from the Bank of Japan.

Meanwhile, the United States Congress passed legislation to regulate stablecoins − a type of cryptocurrency whose value is pegged to an external reference, such as gold or fiat currencies (national currencies that are backed by the issuing government rather than commodities such as gold or silver). Stablecoins now have a clearer path to broader use in financial transactions.

The bill imposes federal or state oversight on U.S. dollar-linked tokens. Regulatory rules include a requirement for firms to fully back currency values with reserves in short-term government debt or equivalent products, bringing some perceived legitimacy to the crypto industry. It also brings demand for securities, which will help to finance increased government borrowing.

Supporters of the bill believe it could lead to cheaper, faster, and more business-related transactions. Critics, on the other hand, warn that the bill won’t do enough to protect consumers.

The development of the coins could have a macro-economic impact though, as it creates demand for bills that can support government borrowing, but it takes deposits away from the banking system, which could inhibit credit creation.

Have U.S. import tariff costs been passed on to consumers?

Investors have been scouring inflation reports for evidence that companies are passing on the costs of U.S. import tariffs by raising consumer prices. So far, tariff-driven inflation had been the dog that didn’t bark, but last week’s inflation report allowed another opportunity to check. Inflation picked up, but by less than expected. So, another month of no tariff inflation? Not quite.

Source: LSEG

Services prices were suppressed by travel prices (such as airfares and hotel prices) and housing (such as rent). But core goods inflation did pick up, and while the move was not very large, it was quite broad, covering several sectors that would instinctively suffer from import taxes (clothes, appliances, home wears).

This is really the first sign of these moves, and it reflects the fact that many months have passed between the first speculation about import tariffs and their eventual implementation, a process that even now hasn’t finished.

Is this an example of the kind of haphazard implementation that is characteristic of the Trump administration? Or is it a deliberate strategy?

Most economists assume that tariffs are a tax paid by consumers. The political risk is that consumers realise that too. That will be most obvious if you implement the tariffs and then prices go up. However, if you implement tariffs and then prices don’t noticeably rise, then it seems like the government has achieved an immaculate tax hike.

How can that happen? Firstly, you give some warning so that companies buy in a lot of inventory ahead of the tariff increase. Then you increase tariffs a bit, while deferring further increases.

It doesn’t hurt for there to be some ambiguity about what will happen, as happens if you dangle the prospect of trade deals, even though in practice hardly any such deals get done. Exporters don’t want to hike their prices and lose market share if tariffs might be cut again soon, so they suffer the tax themselves for a few months.

The upshot, therefore, is that importers have had the inventories and exporters have had the incentive to keep prices down for the time being, which has put some distance between the tariff announcement and the tariff impact. It means the impact will unfold gradually over time, rather than lurching higher, making it much harder for consumers (or, more accurately, voters) to associate their loss of disposable income with the tariff increase.

Imposing tariffs, like boiling frogs, is probably easier if you do it slowly. Has it made the policies popular? To an extent. The disapproval rate of President Trump and his policies on trade and inflation has stopped worsening since the ‘Liberation Day’ tariffs were partly deferred, although his policies haven’t actually become more popular.

However, what seems significant is that if the policies become embedded, it’s harder to see this, or a future administration removing them. As we’ve discussed before, the trajectory of the budget deficit makes it very hard for either party to give up revenue sources.

The chaotic implementation of tariffs – was it deliberate?

Source: Silver Bulletin

In that sense, the chaotic implementation of the tariffs may help to ensure their permanence. Was it deliberate? Probably not. But what seems more stage managed has been the repeated rumours, and subsequent guarded denials, that President Trump is preparing to fire Federal Reserve (the Fed) Chairman, Jerome Powell.

Last week, Trump met with congressional Republicans in a private meeting, at which he discussed the matter, even showing them a draft letter of termination. News of the meeting was leaked, the dollar fell, the yield curve steepened, and gold and bitcoin rose.

President Trump subsequently said he was probably not going to fire Powell after all, and added that former President Joe Biden had appointed Powell, a falsehood that is so obvious that it would immediately cast additional doubt on the topic. The market reaction was less severe than last time the topic was raised; prediction markets had already assumed a higher chance of it happening and, presumably, they will continue to do so. By repeatedly floating and walking back the idea, the market reaction, when it happens, will be less severe.

President Trump seems fixated on the fact that interest rates should be lower, despite inflation picking up recently. As a result, the shortlist for Powell’s replacement includes Kevin Hassett and Scott Bessent, both members of President Trump’s current economic team. Either would face challenges to being confirmed, as that would appear to undermine the independence of the Fed. More conventional alternatives would be former Fed governor Kevin Warsh or current governor Christopher Waller.

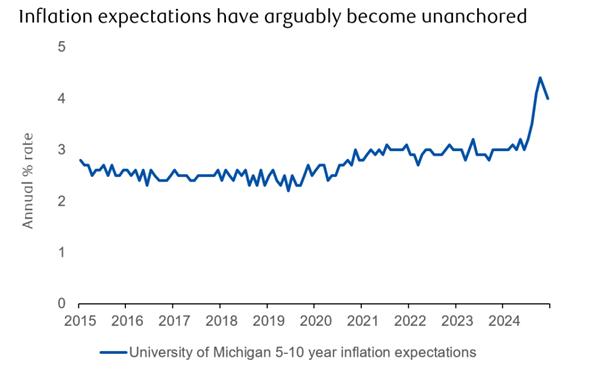

The frontrunners are Warsh and Hassett; but last week, Waller stated his view that interest rates should be cut at the next meeting on 30 July. His view is that the limited evidence of inflation from tariffs will be temporary (which seems likely) and that inflation expectations are unlikely to be unanchored (i.e. they’ve started to move unusually far away from their previous average). This last point is debateable as, by some measures, they have already become unanchored. It’s therefore pretty certain that rates will be held at that meeting.

Source: LSEG

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

The Government is pushing ahead with plans to include pensions within inheritance tax (IHT) from April 2027, but has made some adjustments to its implementation plans.

The move is expected to raise £1.5bn a year by 2029/30, with the average IHT burden expected to increase by £34,000.

The plans were confirmed by the Government on Monday (21 July). From April 6 2027, IHT will be applied on unused pension funds and death benefits.

Chancellor Rachel Reeves first unveiled the plans in the Autumn Statement 2024.

Adjustments

The Government has adjusted its original proposals following a consultation on the mechanics of implementation, which closed in January.

One such change is that personal representatives, rather pension scheme administrators, will be liable for reporting and paying any IHT due, and death in service benefits payable from a registered pension scheme will remain out of scope of IHT.

As part of the Autumn Budget 2024, the Government announced measures to reform IHT and “deliver a fairer, less economically distortive tax treatment of inherited wealth and assets, including this measure”.

Comment

Personally, I think Labour have got it wrong again on this one. They are penalising hard working people that have done the right thing and accumulated good pension assets for their retirement.

Having said that, for the majority of people funding pensions is still one of the best things to do to provide your retirement income, it’s tax efficient.

For a lot of married couples or for those in a Civil Partnership, you might not have an inheritance tax position unless your assets exceed £1 million, including your pension funds, from April 2027.

We can implement individual planning strategies as appropriate if you have an inheritance tax position now or in the future.

Generally, we caution against any knee jerk reaction to this legislative change. Consider your position, think long term, and take independent financial advice.