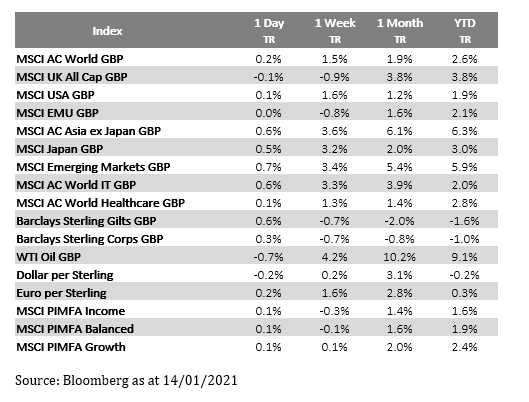

Please see below update received from Brooks MacDonald earlier today, which analyses global market performance over the past few days.

What has happened

With US markets closed yesterday, equity moves were fairly small and we saw more of a consolidation than any momentum one way or another. That said, European and Asian markets did gain ground with the latter helped by the strong Chinese GDP data at the start of the week.

Yellen’s confirmation hearing

Later today, Janet Yellen, former Fed Chair will set out her plan to the Senate finance committee ahead of her confirmation as Treasury secretary. The prepared remarks have already been leaked and the highest profile phrase is that ‘the smartest thing we can do is act big’. Yellen is expected to reiterate the need for fiscal spending saying that the downturn in the economy could lead to a ‘longer, more painful recession’ if stimulus bills such as that proposed by President-elect Biden falter. The first test for the new President will be the passing of $1.9 trillion of relief measures which may prove challenging given the tiniest of working majorities in the Senate. There will inevitably be questions about the longer-term funding of the deficit created by these measures and the interactions between the Fed and Treasury given Yellen’s former role.

COVID Update

Cases remain elevated across Europe but there are signs that the tougher restrictions are starting to work with Italy seeing its daily cases fall below 10,000 for the first time this year and the UK dipping below 40,000 as Lockdown 3.0 takes effect. Germany is also expected to extend its lockdown further due to concerns over the new variants after being in heightened restrictions for several months. On the vaccine there continue to be impressive numbers out of the UK which is one of the fastest moving of the major economies. The EU are also seeking 70% of the bloc’s population to have had the vaccine by the summer so signs of momentum, or at least ambition, building. In less positive news, California’s state epidemiologist has recommended the pause of the rollout of the Moderna vaccine after severe allergic reactions.

What does Brooks Macdonald think

Yesterday saw a brief lull in market activity after an eventful start to 2021, with central bank meetings, politics and earnings this is unlikely to last too long. Against this backdrop the vaccine rollout has begun in earnest which means that with each passing day the economic risk of reopening marginally reduces. Of course, the question for governments will be what proportion of the population needs to be vaccinated before the risk of the virus is ‘acceptable’, expect this to be a major debate in Q2 2021.

Please check in again with us soon for further relevant content and news.

Please see article below from J.P. Morgan received this morning – 18/01/2021

When will the vaccines allow for a sustained economic recovery?

15-01-2021

For months, the question on everyone’s lips has been, ‘When can we start getting back to normal?’ The short answer is, ‘When the vulnerable have been vaccinated and the healthcare systems are comfortably coping with Covid-19 cases’. The more complete answer is a little more complex. Protecting the vulnerable will facilitate the process of a sustainable reopening but caution will still be required until a broader group are vaccinated, and the timetable will differ around the world. Our base case for major developed economies is that the process of sustainable reopening begins in the spring, and in the latter months of the year we see a meaningful bounce in economic activity as pent-up demand is unleashed.

The charts in this report will be updated twice a week in our tracker for readers to follow the progress of the vaccine rollout.

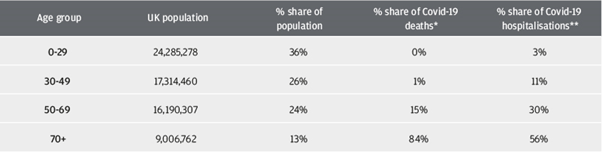

Vaccinating the vulnerable should drastically reduce mortality and hospitalisations from Covid-19

Governments around the world are adopting strategies to vaccinate the most vulnerable first, which should reduce mortality from the virus but also ease the burden on healthcare services. This approach makes sense given Covid-19 causes a disproportionate level of deaths and hospitalisations among older cohorts. In the UK, there are nine million people aged over 70, accounting for 13% of the total population, but 84% of the total Covid-19 deaths and over 50% of total hospitalisations (Exhibit 1).

Exhibit 1: Demographics and Covid-19 in the UK

Source: Office for National Statistics, British Medical Journal, J.P. Morgan Asset Management. *Based on deaths in England and Wales where Covid-19 is mentioned on the death certificate. **Based on an analysis of the first wave published in the British Medical Journal. Data as of 14 January 2021.

Throughout the Covid-19 pandemic we have seen how the health and economic crises have been inextricably linked. If vaccinating the vulnerable significantly reduces the number of new hospital admissions, then governments will feel more comfortable about relaxing restrictions, allowing economic activity to begin normalising.

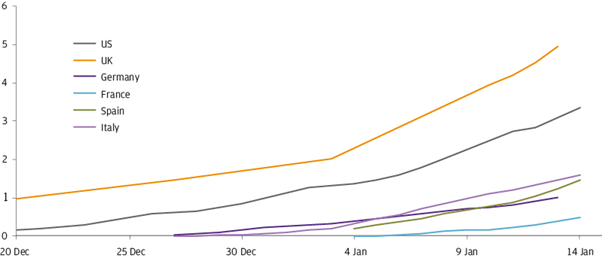

The pace of vaccine rollout is key

At the time of writing, the UK and US have made solid starts in vaccinating their populations, while the major European economies are off to a slower start (Exhibit 2).

Exhibit 2: Covid-19 vaccine rollout Cumulative doses administered per 100 people

Source: Our World in Data, J.P. Morgan Asset Management. Data as of 14 January 2021.

The UK government has announced an ambitious plan to offer vaccinations to its top four priority groups – amounting to 15 million people – by 15 February. These groups include those over the age of 70, frontline workers and those that are clinically vulnerable. The time between first and second dose of vaccines administered in the UK has been extended to 12 weeks to allow as many people as possible to receive at least the first dose, which the government’s advisers view as the best way to reduce mortality and the strain on the health system.

How feasible is it to vaccinate such a large group of people in such a short space of time? In the 2019-20 flu season, the UK vaccinated over 14 million people over a five-month period. The UK health system already has significant experience in vaccinating millions, but it needs to do it around five times as fast as normal. Several mass vaccination centres are planned around the country to meet this ambition, with some vaccinating 24/7. The government has expressed confidence that this will provide sufficient distributive capacity to allow it to meet its goal, and that distribution needs will be met by the supply of approved vaccines, of which the UK now has three.

We think the target is broadly achievable. Whether or not it is achieved exactly to the day is primarily a political concern, but the proposition of having the majority of the UK’s vulnerable with some protection by the beginning of March ought to be a game-changer (as Exhibit 1 suggests) and allow for a process of sustained economic recovery to begin in the second quarter.

The rollout in the US and EU is likely to continue to lag the UK, but both should still have vaccinated the most vulnerable in the first half of the year. Both the Pfizer and Moderna vaccines are approved in the US and the EU, and sufficient doses have been secured to vaccinate the vulnerable population.

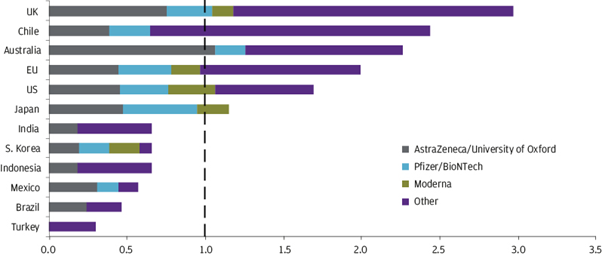

The EU, in particular, will benefit considerably if its regulators approve the AstraZeneca/University of Oxford vaccine in the coming weeks, since it has ordered doses to cover more than 40% of its population and this vaccine is logistically easier to handle (Exhibit 3).

Exhibit 3: Confirmed orders for vaccinations per head of population Complete vaccination courses per head of population

Source: Duke Global Health Innovation Center, World Bank, J.P. Morgan Asset Management. This chart shows the number of complete vaccination courses that a given country has confirmed orders for. Data as of 9 January 2021.

The success of the three pioneering Covid vaccines will have a huge impact in taming the pandemic, but there are also many other vaccine candidates that could be approved in the coming months that would bolster the world’s supply. Novavax and Johnson & Johnson (J&J) are two of 20 vaccine candidates currently in phase III trials, and have large orders confirmed.

However, it is clear that the vaccine rollout will be unequal. The deep pockets of developed governments have allowed them to secure vaccinations to more than cover their populations. Lower-income emerging market countries have order books that fall short of their populations, giving them less room for error in their rollout strategies. As a result, many will have to rely on the COVAX scheme – a consortium set up by the World Health Organisation and others to ensure that all countries have access to Covid-19 vaccines – and can expect a slower return to normality. COVAX has large orders for the AstraZeneca/University of Oxford and J&J vaccines.

One part of the emerging world is less reliant on vaccines for its economic recovery: North Asia. Through effective testing, contact tracing and strict border controls, the region has been able to recover quickly without the help of vaccines. For investors in emerging markets, this disparate outlook calls for a selective approach.

We are optimistic on the path of vaccine rollout, but mindful of tail risks

The rollout of vaccines in the developed world should allow economies to recover sharply in the second half of the year as normality returns and consumers are finally free to unleash their pent-up savings. We expect that the UK and US will have vaccinated over half their populations in the first half of the year, and the EU will reach that milestone during the summer.

The strong rebound in developed market activity should be supportive of risk assets, and in particular stocks that stand to benefit the most from a rotation from the Covid winners to those that lost out from the pandemic. Europe, the UK and the value style stand out in this respect. The emerging markets could also perform well in this environment, driven by continued strong economic performance in Asia and a gradual decline in the US dollar.

Of course, there remain risks. We are less concerned about the vaccine timetable slipping for logistical reasons, and think that plans could even be accelerated. Governments are under tremendous pressure to at least keep up with their neighbouring counterparts. And given the fiscal cost of maintaining economic restrictions, no expense will be spared in driving the rollout.

Uncertainty around take-up is a hurdle for all countries, and surveys suggest a significant degree of scepticism for the Covid-19 vaccine in Europe. Experience in the UK suggests that as the vaccine rollout is proceeding, public confidence is growing, and many may feel increasingly confident of taking up the vaccine as time progresses.

The key risk is that the virus mutates to a new variant that makes the currently approved vaccines ineffective. There is also the risk that vaccine efficacy is lower than initially reported, either among the older population, or across the population from altering the time between first and second doses. Data from trials hasn’t been completely comprehensive in these areas. Many of these risks could be addressed – and rather than derailing the recovery completely, could just provide a setback while new formulations are found. However, we think it prudent for investors to maintain tail-risk protection such as through long-duration government bonds or dynamic fixed income and macro strategies.

A good update from J.P. Morgan with more positive news on the vaccine roll out.

Vaccinating the most vulnerable should drastically reduce mortality and hospitalisations from Covid-19. Hopefully, once the most vulnerable are vaccinated, governments will feel more comfortable about relaxing restrictions, allowing economic activity to begin normalising.

Please continue to check back for our latest blog posts and updates.

Please see below article received from AJ Bell yesterday evening, written by their Investment Director, Russ Mould. The commentary indicates a positive start to 2021 in relation to UK equity markets and predicts market performance for the year ahead.

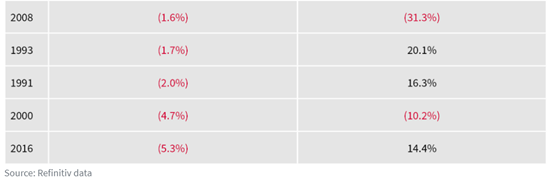

After a rotten showing in 2020, when the FTSE 100 ranked plumb last among major national indices on a local currency, total-return basis, the UK equity market is off to a flyer in 2021. Whether this is a simple case of every dog having its day or the start of a more fundamental turnaround will only become clear with the passage of time, but what is undeniable is that the FTSE 100 has just had its best start to a year in its history, using the capital return over the first five calendar days’ trading as a benchmark.

FTSE 100’s fast start looks promising for the rest of 2021, if history is any guide

“It is eye-catching to see how the FTSE 100 has generated positive capital returns on every occasion bar one when it has begun the year with an opening-week gain of 1% or more.”

The past is no guarantee for the future, as all advisers and clients know (and the numbers show that a bad start does not guarantee a bad overall outcome). Even so, it is eye-catching to see how the FTSE 100 has generated positive capital returns on every occasion bar one when it has begun the year with an opening-week gain of 1% or more. That exception was 1987 and even that year looked like plain sailing until October, although a nasty reckoning then followed with the Crash.

That episode shows that trouble can come when it is least expected and, as part of any risk-management review, advisers and clients will look at what can go wrong. There is a saying that “bull markets end when the money runs out” and, at the moment, there seems to be no shortage of cheap cash upon which financial markets can feast, as central banks continue to run ultra-loose monetary policy and governments around the world continue to provide fiscal support to their economies, racking up huge budget deficits in the process.

“Spotting misallocation of capital is important when it comes to market tops. In 1999–2000 and 2006–7, overpriced merger and acquisition deals had a role to play. So did a very active market for Initial Public Offerings (IPOs) and secondary sales of stock by either vendors or companies themselves.”

So perhaps advisers and clients need to start wondering where all of this money could go, or what could soak it up, to end the bull run. Spotting misallocation of capital is also key. In 1999–2000 and 2006–7, overpriced merger and acquisition deals had a role to play. So did a very active market for Initial Public Offerings (IPOs) and secondary sales of stock by either vendors or companies themselves. Many of those IPOs were in what turned out to be overpriced tech, media and telecoms stocks in 1999–2000, while miners and junior oil explorers, property stocks and financial investment vehicles took centre stage in 2006–7 (and more of the last-named in a moment), to eventual great cost to buyers of this new paper.

Some advisers’ and clients’ interest may therefore be piqued by the announcement of planned stock flotations by Moonpig, Foresight Group and Dr Martens at the start of 2021, even if the specifics of the individual companies will be left to their preferred UK equity managers to assess.

Functioning markets

In some ways, these new flotations could be a good sign.

They suggest that capital markets are working well and doing what they are supposed to do, which is provide capital that companies can use to invest and hire, create wealth and ultimately help the economy to grow.

Fund managers may also see them as a chance to buy into new, exciting stories that generate capital gains or welcome income over the long term for their clients, or at least offer the potential for a quick turn if a deal looks like it is going to be hot and the shares are going to spike.

However, a sudden flood of new market entrants might also be warning sign, on the grounds that you can have too much of a good thing.

“Not surprisingly given the circumstances, and especially last spring’s stock market rout, newcomers to the London market were relatively few and far between in 2020, although the pace did pick up in the second half and some deals, such as THG, proved to be absolute winners.”

Not surprisingly given the circumstances, and especially last spring’s stock market rout, newcomers to the London market were relatively few and far between in 2020, although the pace did pick up in the second half and some deals, such as THG, proved to be absolute winners.

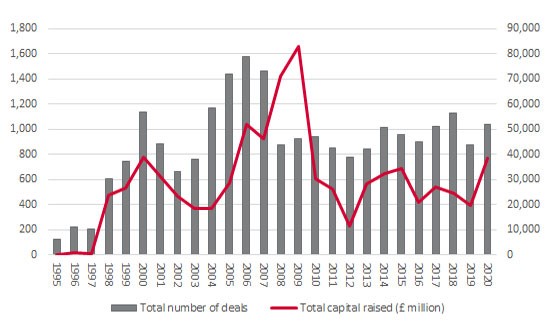

Overall, the number of new issues and IPOs in London last year was the second-lowest since 2009 and the end of the Great Financial Crisis, according to data from the London Stock Exchange (only 2019 was lower).

New issue activity has been relatively quiet in the UK for some time

Source: London Stock Exchange

Over £7 billion was raised by primary offerings, the highest figure since 2017, and that exceeded the sums generated by market newbies in 2009, 2012, 2015, 2018 and 2019.

And with only a select number of names announcing plans for an IPO so far in 2021, it is too early to be pressing the panic button about a deluge of new issues swamping investors and snuffing out the UK market’s attempt to forge a sustained bull run.

The £7.3 billion raised in 2020 came nowhere near the £31 billion of 2006 and £27 billion of 2007, right before trouble hit and the bear market began, or the £18.7 billion peak of the prior cycle in 2000.

Warming up

But advisers and clients need to be on their guard. The US market has shown signs of an overheated new offerings market, especially given the post-listing surges in names such as Airbnb and DoorDash, the coming to market and the lofty valuations at which many new entrants have gone public and the torrent of Special Purpose Acquisition Companies (SPACs) that have listed, in a manner that is eerily reminiscent of 2006–7 on both sides of the Atlantic.

“The US market has shown signs of an overheated new offerings market. The UK is showing no real signs of any of those, which is reassuring, although advisers and clients will also want to keep an eye on secondary offerings too, since they can also soak up cash that could otherwise be deployed elsewhere.”

The UK is showing no real signs of any of those, which is reassuring, although advisers and clients will also want to keep an eye on secondary offerings too, since they can also soak up cash that could otherwise be deployed elsewhere.

Over 950 secondary deals, including rights issues, placings for cash, open offers, subscriptions and further issues took place in 2020, perhaps understandably as many companies tapped their shareholders for fresh liquidity to help see them through the pandemic and the subsequent recession. London-listed and quoted firms raised over £31 billion, the highest figure since 2008–9 when companies were again in cash-raising, crisis-management mode.

Secondary issuance began to pick up in 2020 as many firms scrambled for cash

Source: London Stock Exchange

That meant the total cash raised across primary and secondary deals reached nearly £39 billion, again the highest mark since 2009. Couple that with hefty cuts to dividend payments and a collapse in share buyback activity and it is no surprise that the UK stock market’s headline indices struggled to make headway in 2020.

Total UK equity issuance picked up in 2020 just as dividends and buyback activity fell

Source: London Stock Exchange

Watch the flow

Dividend payments are expected to rebound this year and buyback activity could conceivably start to pick up, too, should the global economy really begin to gain traction in the wake of vaccination programmes.

This remains far from certain, however, and advisers and clients do need to be on their guard in case the steady flow of new deals becomes a flood, especially if deal quality starts to flag and certain hot or popular sectors witness very high levels of activity. This is not a problem in the UK, as Foresight Group, Dr Martens and Moonpig all come from different sectors and industries, but advisers and clients might like to make sure that their chosen fund managers bear in mind Warren Buffett’s warning, should copycat deals start to proliferate:

“First come the innovators, who see opportunities that others don’t. Then come the imitators who copy what the innovators have done. And then come the idiots, whose avarice undoes the very innovations they are trying to use to get rich.”

We will continue to publish relevant market analysis and news, so please check in again with us soon.

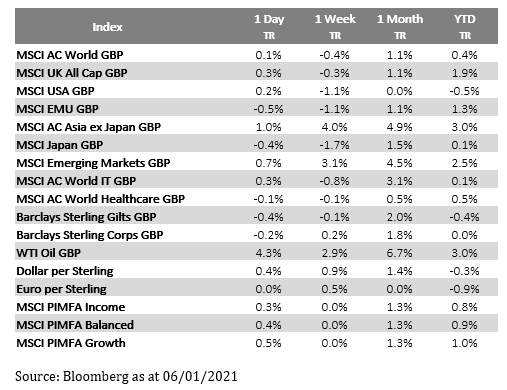

Please see below Daily Investment Bulletin received from Brooks MacDonald earlier this afternoon. The update provides analysis on the fall and rise of bond markets in response to political developments in the US and Italy over the past few days.

What has happened

Equity markets retained a constructive tone yesterday, but it was really bond markets that did the most travelling. Initially US Treasury bond yields fell as markets continued to digest the series of Fed governors who reassured bond investors that they would remain accommodative for the foreseeable future. Overnight however, Bloomberg reported that President-elect Biden’s administration would be seeking a bi-partisan $2 trillion bill which led the decline in yields to reverse. The interplay of the nascent economic recovery, fiscal stimulus and monetary stimulus will be a key theme of 2021.

Italian politics

As widely expected, Matteo Renzi announced yesterday that his party, Italy Alive, was quitting the government’s coalition. Matteo Renzi previously was Prime Minister as well as leader of Democratic Party however his new party has far fewer seats in Parliament. Those few seats are still enough to topple the delicate coalition, but investors are currently expecting an election to be avoided. Prime Minister Conte may now resign, or a vote of confidence may be called, regardless Conte will first seek to build a new coalition amongst the parties. Should this fail we may see a change of Prime Minister or a technocratic administration as an interim measure. Hope that Italy could avoid the destabilisation of fresh elections helped support Italian government bonds after a difficult start to the week.

US Politics

The major news story yesterday was the second impeachment of President Trump, a first in American history. The key question now is when the articles of impeachment will be reviewed by the Senate, commencing the trial. There is an active debate amongst Democrats over whether it is better to deal with the trial as the first order of business under a new White House or whether it is prudent to conclude other business first. There is certainly no urgency on the Senate trial given the trial will take place after President Trump leaves office however the political palatability of a delay is probably the key factor.

What does Brooks Macdonald think

With talk that President-elect Biden will seek a $2 trillion package, well ahead of expectations, cyclical equities are seeing another boost overnight and today. Today we hear from Fed Chair Powell who will be talking about the Fed’s policy framework. Investors will be scouring the speech for commitment to the mood music from recent Fed governor speeches which have sought to reassure markets that monetary accommodation is here to stay.

Please check in again with us soon for more relevant data and market analysis.

Please see below an interesting article received from Invesco earlier this afternoon, which provides an insight into the intricacies of the UK’s relationship with the EU following the long-awaited agreement of Brexit terms on Christmas Eve.

Almost four and a half years to the day since the Brexit referendum took place, the terms of the future relationship between the UK and the European Union were finally agreed on Christmas Eve. Having spent the final months of the year wrangling over provisions relating to the level playing field, governance and enforcement mechanisms, and fisheries, both sides proclaimed victory as the legal text on these issues was finally settled.

In Downing Street, Prime Minister Boris Johnson declared that the UK had delivered on the referendum verdict by taking back control of its borders, laws and waters, ending the jurisdiction of the European Court of Justice and gaining the freedom to set its own rules and standards. In Brussels, Commission President Ursula von der Leyen said the deal had safeguarded the integrity of the EU’s Single Market and the four freedoms of people, goods, services and capital, demonstrating that having left the EU the UK would no longer be able to enjoy the benefits of membership.

In reality, the verdict on which side was better able to secure its political priorities in the Agreement, and at what cost, will take many months, if not years, to reach. While agreeing a comprehensive trade deal in just ten months was a significant achievement for both sides, the full implications of the 1,246 pages of text and their impact on diverse business models on both sides of the Channel will only become clear over time: even the most obvious physical signs of separation – at the Dover-Calais border – have yet to manifest themselves given that haulier traffic has been much lower than normal during the early days of the year.

But what is clear is that, by avoiding a ‘no deal’ outcome, the UK and the EU have also avoided the risks of an acrimonious break up and blame game that could have soured relations between the two sides for years to come. Instead, they have a platform on which to build – should both sides choose to do so – in the coming years and decades.

Yet despite the last-minute Agreement, significant questions about the future relationship remain. What will be the key drivers of the UK-EU relationship in next years? Where will the main points of friction between the two sides emerge? Will the Agreement stand the test of time or require significant revision? Will, as President von der Leyen optimistically declared, both sides be able to “leave Brexit behind us”; or will the UK join Switzerland as a country outside the EU but in almost constant negotiation with its near neighbour?

It seems clear that on the UK side, the Agreement will not end the debate on Brexit. The Conservatives are already road testing messaging for the next election on the basis of an appeal to “keep Brexit done”, playing to concerns that Labour, should they regain power, would seek to forge a closer relationship with the EU in the future. Former Prime Minister David Cameron’s gambit to try to finally put the EU question to bed may instead have kept Pandora’s box wide open. Britain’s relationship with the EU looks set to continue to be a polarising issue in UK politics, and something that the devolved administrations will seek to play to their advantage in relations with Westminster. By comparison, the EU will be keen to leave Brexit, as a distinct problem to be solved, well behind it; but it will fuel the EU’s growing emphasis on strategic autonomy, requiring a delicate balance to be found between wanting to keep the UK within its area of influence while at the same time arguing for self-sufficiency in areas where it sees itself in competition with the UK.

One bellwether of this approach is likely to be the EU’s stance towards the UK on financial services. Despite the importance of financial services to the UK economy, and the cross-border integration of industry operations in Europe, the financial services section in the Agreement contains just eight articles, covering little of real substance. With the EU keeping the UK in suspense on a range of potential equivalence determinations, it remains to be seen whether the two sides will remain aligned on major regulatory issues such as sustainable finance, financial stability and protections for retail investors. The Governor of the Bank of England, Andrew Bailey, has argued that the UK cannot be an automatic rule-taker from the EU. But where might the UK seek to use its freedom to diverge to forge a separate path; and what would be the EU’s likely response?

Finally, in a world of increasing polarisation and renewed threats to international trade, market stability and security, will the lack of a framework for cooperation on foreign policy, security and defence cooperation in the Agreement significantly weaken the UK and EU’s ability to defend their interests on the international stage? How might actors such as Russia and China seek to exploit the UK’s exit from the EU; and will Europe’s collective influence in Washington now be weaker than before?

Although the UK and EU are now separate entities, they now have the opportunity to move forward together as allies in a productive and positive way. Please check in again with us soon.

Please see below Monday Market Update received from Blackfinch Group this morning, which reflects on how the market is reacting to current world events.

UK COMMENTARY

Boris Johnson announced a third national lockdown, with households told to stay home until at least 22nd February.

Chancellor of the Exchequer Rishi Sunak unveiled a £4.6bn grants package to help businesses survive the new lockdown.

Retail footfall declined sharply after Christmas, according to market researcher Springboard. The number of recorded shoppers was down 23.2% week-on-week and 55.7% year-on-year.

British supermarkets enjoyed their busiest ever December, with shoppers spending £11.7bn on groceries over the month.

December saw seasonally adjusted Purchasing Managers’ Index (PMI) survey data for the manufacturing sector rise to a three-year high of 57.5, up from 55.6 in November.

Services sector PMI rose to 49.4 in December, up from 47.6 in November, but remained below the 50.0 breakeven mark, suggesting activity was still contracting.

PMI survey data for the construction sector eased slightly to 54.6, down from 54.7 in the previous month.

US COMMENTARY

The Democratic Party won both seats contested in the Senate run-off elections in the state of Georgia, securing control of the Senate due to the vice-president’s casting vote.

Protest groups stormed the buildings on Capitol Hill following Donald Trump’s speech outside the White House. The scenes shocked onlookers around the world, with more than 60 police officers injured and five people dead. However, the violent protests did not stop the certification of Joe Biden’s electoral victory.

The US economy shed 140,000 jobs in December, the first monthly decline since April.

Initial jobless claims data beat expectations, with the number of US citizens filing for first-time unemployment falling to 787,000, despite economists predicting a reading of 800,000.

ISM PMI manufacturing survey data defied market expectations and rose strongly to 60.7 in December, up from 57.5 in November.

ASIA COMMENTARY

In China, Caixin/Markit PMI survey data for the services sector fell to 56.0 in December, compared to the November reading of 57.8.

We will continue to source and publish relevant market analysis and news as we push through the UK’s 3rd national lockdown in the knowledge that we have 3 approved vaccines to be rolled out. Please check in again with us soon.

Please see below Daily Investment Bulletin received from Brooks MacDonald earlier today. The update provides market analysis and refers to developments in US politics and the Oxford/Astrazeneca vaccine roll-out.

What has happened

The two seats in the Georgia run-off elections look to be tipping in favour of the Democrats which will have wide ranging implications for the first two years of President-Elect Biden’s Administration. Markets were quick to interpret this with US index futures losing ground and Treasury yields rising.

Vaccine race hots up

We saw a swathe of forward-looking PMI data yesterday from across the world, much of this is pointing to more optimism ahead, but that optimism is largely focused on hopes around the vaccine. As the Oxford/Astrazeneca vaccine begins to be rolled out across the UK, the government announced that 1.3 million people had now been vaccinated and around 23% of those over 80. The wider the roll-out becomes the more political choices governments will have as immunity for those most at risk of hospitalisation or death will give hospitals capacity for any surges amongst less-at-risk populations.

Georgia run-off

Whilst there were concerns that we wouldn’t see a result for several days, with 98% of the vote counted it looks likely that both Democrat candidates will with their races. This brings the Senate to a 50-50 tie but Vice President-elect Harris will have the deciding vote and therefore will be able to edge a vote over the line should all Senators vote along party lines. This would give far more legislative options to President-elect Biden but legislation would need to be unanimously supported by Democrat Senators to pass so there will still be some consensus building required to pass laws. All short-term attention will be on US Fiscal Stimulus with, if the polls are confirmed, a larger package now on the table for Q1 2021 possibly including an infrastructure package alongside to provide a further boost. Of course the sting in the tail could be tax rises or increased regulation around healthcare or big technology, but the wafer thin working majority will moderate any of the more ambitious Democrat policies. With expectations of nearer term stimulus, the market expects the Federal Reserve to need to do marginally less in terms of monetary policy and as a result the 10 year US Treasury hit 1% for the first time in more than 9 months.

What does Brooks Macdonald think

Whilst the Senate looks likely to be split 50/50 with VP-Elect Harris’s vote tipping the balance, such a narrow working majority will inevitably reduce the risk of any highly divisive legislation passing the Upper Chamber. There is also the issue of the filibuster which, unless reformed, can effectively block legislation unless there are 60 Senators in favour of moving the bill along.

We will continue to publish news and market analysis throughout the third and hopefully, final, national UK lockdown. Please check in again with us shortly.

Please see below weekly market commentary from Brooks Macdonald received yesterday afternoon – 04/01/2021

Weekly Market Commentary | COVID-19 restrictions remain in the spotlight as 2021 begins

04 January 2021

Read detailed economic and market news from our in-house research team.

• Weekly Market Commentary

• COVID-19 updates

By Edward Park

• Risk sentiment was positive but muted as a Brexit deal and US Fiscal Stimulus both came over the line

• While vaccines improve the prospects for 2021, restrictions look set to tighten in the interim

• Georgia’s runoff elections tomorrow will determine the makeup of the Senate for the next two years

Risk sentiment was positive but muted as a Brexit deal and US Fiscal Stimulus both came over the line

There was a strong sense of Groundhog Day throughout December as the ‘will they won’t they’ pantomime played out over a Brexit deal and US Fiscal Stimulus. Ultimately, both of them were carried over the line but looking at the rather muted market reaction, investors were too exhausted to care once the result was known.

While vaccines improve the prospects for 2021, restrictions look set to tighten in the interim

The brighter prospect for 2021 firmly lies with the vaccines and, in the UK, we now have the Oxford vaccine to add to the arsenal. The Oxford vaccine is important as, while it appears less effective than the Pfizer/Moderna mRNA options, it is cheaper and easier to handle, only requiring storage in a normal fridge. As the UK and other countries look to ramp up their inoculation efforts, the new viral variant has changed the dynamics for restrictions. Since the lockdown in March of 2020, the government has squeezed social activity and the hospitality industry with the intent of leaving room for the economy to stay largely open and schools to continue operating. The current Tier 4 restrictions, similar to Lockdown 2.0 in November, are seen as insufficient to curb the current variant and UK Prime Minister Johnson yesterday warned on the Andrew Marr show that restrictions were likely to get tougher. A return to a March 2020 lockdown will undoubtedly hit Q1 UK GDP, however markets may continue to look through this near-term uncertainty if they are confident that vaccines make this a temporary, though possibly deep, hit to economic activity.

Georgia’s runoff elections tomorrow will determine the makeup of the Senate for the next two years

Tomorrow sees the runoff elections in the state of Georgia which will ultimately determine the balance of power in the Senate with wide implications for President-Elect Biden’s legislative options for the next two years. It is worth noting that the Republicans currently have 50 seats to the Democrats’ 48, however if the two Georgia seats go blue then Vice President Harris will cast the deciding vote in the Senate, giving the Democrats the narrowest of working majorities. The most important near-term policy will be fiscal stimulus and the lie of the land post tomorrow will be a significant factor in determining how large or small any Q1 stimulus package is.

On Wednesday, we will see the joint session of Congress to formally count the electoral college votes for the next President. This is normally a formality but with several Republican senators saying they will challenge the result, expect some headlines even if the majority vote to move on and certify the result.

Please continue to check back for our latest updates and blog posts.

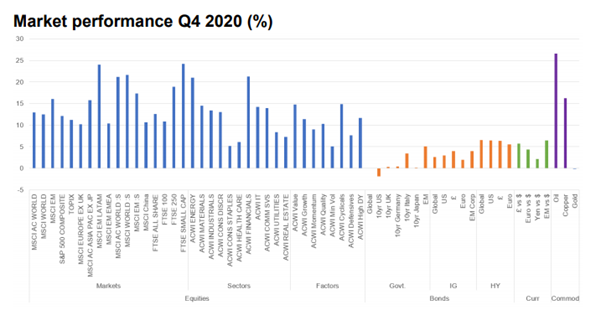

Please see below Invesco’s most recent Investment Intelligence update, received earlier this afternoon. The commentary provides analysis of market performance over the course of 2020 and reflects on influential global events.

Second and third waves of the coronavirus pandemic and their associated containment measures, progress on the vaccine front, US elections, Brexit and the monetary and fiscal backdrop were the main drivers of market performance during the fourth quarter. Investors chose largely to ignore the near-term negative economic consequences of a resurgence in virus cases in many parts of the world, notably the economic heavyweights of the US and Europe, preferring instead to focus on the much hoped for return to some sort of economic normality in 2021 that successful vaccine trials and their subsequent regulatory approvals and roll-out pointed to. As such it was hardly surprising to see that strongest performance during the quarter came from the most economically sensitive assets classes, such as equities, HY credit and commodities.

Global equities had a very strong quarter, dominated by a 11.5% gain in November, rising 12.9% overall with DM (12.5%) continuing to lag EM (16.1%). Within DM there wasn’t much to choose between the major markets, with the UK (12.6%) and US (12.2%) ahead of Japan (11.2%) and Europe ex UK (10.2%). Mid (FTSE 250 18.9%) and Small caps (FTSE Small Caps 24.2%) led the way in the UK, well ahead of large caps (FTSE 100 10.9%). Sector mix and £ strength weighed on the latter. EM continued to see wide divergences in regional performance, with Latin America (24%) well ahead of EMEA (10.4%). Small caps (21.1%) outperformed significantly with DM (21.6%) ahead of EM (17.3%), a reversal of what we saw in broader markets.

At a sector level there was a shift in market leadership during the quarter. Financials (21.3%) and Energy (21%), the two major sector laggards in the preceding quarters, topped the performance charts, even if that still left them at the bottom of the 2020 performance pile. Tech and techrelated sectors also outperformed, albeit only marginally so, with IT (14.2%) the best of them. Defensives struggled against a backdrop of improving economic sentiment, with Consumer Staples (5.2%) and HealthCare (6.1%) the main performance laggards.

On a factor basis, Value (14.8%) had its first quarterly outperformance against Growth (11.4%) for two years. Quality (10.3%) and Momentum (9%) lagged, while Minimum Volatility (5%) brought up the rear.

Globally government bond markets went nowhere (flat) for the second quarter in a row. 10yr yields were little changed for Bunds, Gilts and JGBs, but USTs saw yields 24bp higher (-1.9% TR) and contrasted with BTPs, which were down 35bp (3.4% TR) and hit all-time lows. EM Sovereign returns were the strongest of them all (5%) as yields fell 55bp.

The risk-on backdrop supported credit markets, where the higher risk HY market (6.5%) comfortably outperformed IG (2.6%). Yields (IG -26bp, HY -119bp) declined to all-time low levels, while spreads narrowed further too (IG -35bp, HY -149bp). Within IG returns were led by £ IG (3.9%) and in HY US HY (6.5%) just edged out £ HY (6.4%). Euro denominated credit lagged in both IG and HY. The lower the credit rating the better, with BBBs (3.4%) outperforming in IG and CCCs and below (11.9%) in HY.

Economic optimism and a weaker US$ boosted economically sensitive commodities, with Oil (26.6%) hitting its highest level since February, while Copper (16.2%) made an 8-year high. Gold (-0.1%) struggled as enthusiasm for the precious metal waned as ETF outflows picked up and real yields rose.

Another difficult quarter for the US$ with the US$ Index (-4.2%) having its worst quarter since 2017. It is now down -12.5% from its 2020 high and at its lowest level since early 2018. EM currencies (6.4%) led the way, closely followed by £ (5.7%), with sentiment towards the latter clearly boosted by the signing of a post-Brexit trade deal.

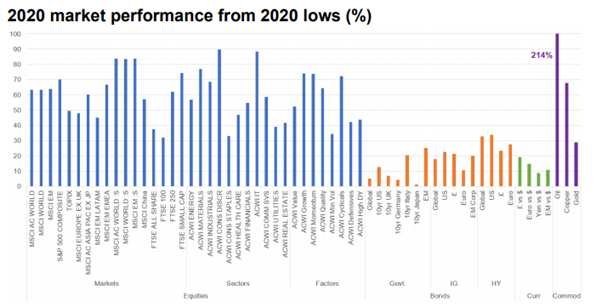

An extraordinary year featuring a strong start, a rapid virus induced collapse and then a remarkable rally off the March lows. The result was that most markets delivered positive returns for the year, with many ending at or close to their 2020 and in a number of cases all-time highs.

Standout performances in equity markets were US equities in DM and Asian equities in EM, led by China. At the sector level, IT and tech-related sectors, Consumer Discretionary and Comms Services, led the way, which underpinned strong performance from the Growth and Momentum factors.

An extraordinary year featuring a strong start, a rapid virus induced collapse and then a remarkable rally off the March lows. The result was that most markets delivered positive returns for the year, with many ending at or close to their 2020 and in a number of cases all-time highs.

Standout performances in equity markets were US equities in DM and Asian equities in EM, led by China. At the sector level, IT and tech-related sectors, Consumer Discretionary and Comms Services, led the way, which underpinned strong performance from the Growth and Momentum factors.

The potential approval of mulitple vaccines and the finality of Brexit may provide a more hopeful outlook for 2021. We will continue to publish relevant market data and news so please check in again with us soon.

You couldn’t have made it up. If anybody had tried to tell you in January this year what was going to happen, you would have thought they had completely lost it!

We are nearly at the end of 2020 and we have been through the mill. Covid 19 has had a severe impact on markets, economies, our health, and our wellbeing. We have not been able to live our lives normally.

Thankfully markets and economies have started to recover. China is in a better place than it was in January. Different sectors thrived, in particular, Technology. With c 75% of Technology businesses in the USA their markets have fared well with indices higher.

In November, with the Biden win and then the really good news on the Pfizer vaccine, markets recovered further. As you know we are now getting vaccinated in the UK in priority-order and we await further good news on the Oxford/Astra Zeneca vaccine.

This Oxford/Astra Zeneca vaccine will make a considerable difference as it’s easier to handle and distribute, and much lower cost. Not only is this good news in the UK, but also globally and for developing and emerging markets.

The only issue outstanding now, which I understand is nearly resolved, is Brexit. It looks like we are on the verge of doing a deal. Hopefully, by the time I relax at home later on, a deal will have been done. This will bring some certainty to the UK and the EU and we can get on with doing business.

How have we changed?

Personally, I think we have learnt a lot from this challenging year. As people and leaders, we now hopefully do a better job, with more of an understanding of the needs of our staff and clients, family and friends. Our culture in the business will have changed as we understand everybody’s needs better.

We now know, more than ever, that we need to work as a team and look after each other. A healthy culture is one that is diverse and inclusive. We need to nurture and grow our people.

In terms of investments, we have seen a significant shift to ESG (Environmental, Social and (corporate) Governance) investing. I think this will continue as Covid 19 has made us reflect on what is important, our health, looking after our environment and dealing with climate change.

The future?

Markets appear to have priced in a good recovery. With the vaccine roll out in the UK, we would expect volatility to continue and the economy to pick up in the second half of 2021. We still have a few headwinds. The end of furlough could see unemployment spike and zombie businesses could close.

To counter this, the pent-up demand of consumers will help, if the vaccine roll out is fast and efficient and people in the UK can return to their normal spending habits and make up for this year.

We also need to see the vaccine roll out globally so our amazing scientists and health care professionals can deal with any further mutation of the virus. Technology and further developments will help too.

I feel positive about the future. It’s been a tough year, but the outlook is brighter. Innovation and science will really help as we work hard to recover economies globally.

Thank you for reading our blogs. Hopefully, they help keep you informed in this fast-changing world we live in. If you have any specific questions, please get in touch.

Merry Christmas and a happy, healthy, and prosperous New Year!

Steve Speed

24/12/2020

Festive opening hours

24/12/2020 close at noon.

Return on 29/12/2020 for standard office hours on both 29/12 and 30/12.