Please see below article received from Brewin Dolphin yesterday evening following the 2022 Autumn Statement.

Chancellor Jeremy Hunt has delivered his autumn statement, in which he set out plans to increase taxes and reduce spending in an effort to narrow the gap between the government’s income and outgoings

After his predecessor’s mini-budget in September triggered a slump in the pound and a sell-off in UK government bonds, this autumn statement was very much about reassuring the markets by demonstrating fiscal responsibility. The statement did not contain any nasty surprises, as many of the tax increases had been leaked in advance, and it was accompanied by growth forecasts from the Office for Budget Responsibility (OBR) – something that was noticeably missing from the mini-budget.

The raft of tax hikes included slashing the capital gains tax (CGT) exemption, dividend allowance and additional-rate income tax threshold, and extending the freeze on the personal allowance, higher-rate income tax threshold and inheritance tax (IHT) nil-rate band. Hunt also announced that public spending would rise by just 1% a year in real terms in the next parliament. The energy price cap will increase from April 2023, meaning the average household will see their bills rise from £2,500 to £3,000 a year.

Here, we highlight the key announcements, before giving Guy Foster’s view on the implications for UK economic growth and investors.

Capital gains tax

What has changed? The chancellor announced that the annual CGT exemption will be slashed from £12,300 in the current tax year to £6,000 in 2023/24 and £3,000 in 2024/25. Any profits (‘gains’) that exceed the exemption will be taxed at the existing rates of 20% for higher and additional-rate taxpayers and 10% for some basic-rate taxpayers (28% or 18% on gains from residential property).

What does it mean for investors? A higher-rate taxpayer who makes a capital gain of £20,000 in the 2023/24 tax year could face a CGT bill of £2,800, rising to £3,400 in 2024/25. This is a considerable increase from £1,540 currently. There are several ways to mitigate CGT, including investing in an ISA, making the most of the CGT exemption each tax year, and using losses to reduce your gain.

Dividend tax

What has changed? The annual dividend allowance – the amount of dividend income you do not have to pay tax on – will fall from £2,000 in the current tax year to £1,000 in 2023/24 and £500 in 2024/25. The rate of dividend tax will remain at 8.75% for basic-rate taxpayers, 33.75% for higher-rate taxpayers and 39.35% for additional-rate taxpayers.

What does it mean for investors? A higher-rate taxpayer who receives dividend income of £5,000 in the 2023/24 tax year could pay £1,350 in dividend tax, rising to £1,518.75 in 2024/25. This compares with £1,012.50 currently. Maximising your ISA allowance each year could become even more important, as any dividends you receive on investments held in an ISA are tax free. Some specialised investments may enable you to reduce dividend tax, but it’s important to seek advice on whether they are right for you.

Income tax thresholds

What has changed? The additional-rate income tax threshold will be lowered from £150,000 to £125,140 from April 2023. The personal allowance (the amount you can earn each year before you start paying income tax)

and the higher-rate income tax threshold have been frozen at their 2021/22 levels of £12,570 and £50,270, respectively, for an additional two years until 2028. Over a nine-year period from 2019/20, the personal allowance and higher-rate tax thresholds will have risen by just £70 and £270, respectively.

What does it mean for investors? Lowering the additional-rate income tax threshold will result in more people paying the 45% top rate of income tax. Someone earning £150,000 could face an income tax bill of £53,703 in 2023/24, up from £52,460 currently. Meanwhile, freezing the personal allowance and higher-rate tax threshold could see more people drifting into higher tax bands because of inflation. An individual who earned £50,000 in 2021, and whose income rises in line with actual and forecast consumer price index (CPI) inflation1 , could see their income tax bill rise from £7,486 to £15,825 by 2028.

One way to potentially reduce your income tax bill is to save into a pension. If your salary and/or bonus means you cross into a higher tax band, making a personal pension contribution could mean your adjusted net income falls to below the threshold and potentially avoids higher or additional-rate tax.

Inheritance tax nil-rate band

What has changed? The IHT nil-rate band and residence nil-rate band have also been frozen for another two years until 2028. The IHT nil-rate band has remained at £325,000 since 20092. Over this period, the average UK house price has surged by 77% from £154,006 to £273,135 in 2022, according to Nationwide3 . By 2028, families will have missed out on almost 20 years of inflation-linked increases. The residence nil-rate band – an additional allowance for those who pass on their main residence to children or grandchildren when they die – was last increased in April 2020 to its current level of £175,000.

What does it mean for investors? Freezing the thresholds could result in more families being caught in the IHT net. In the last decade alone, IHT receipts have rocketed from £2.9bn in 2011/12 to £6.1bn in 2021/224 . There are several ways to help mitigate IHT, particularly if you plan ahead.

Pension lifetime allowance

What has changed? Nothing. It was widely expected that the pension lifetime allowance – the total amount you can save into your pension before incurring tax charges – would also be frozen for another two years, but this did not happen. The existing freeze will therefore end in 2026, unless anything changes between now and then. The lifetime allowance rose in line with CPI inflation between 2018/19 and 2020/21, but has stayed at its current level of £1,073,100 since then. If it were to keep pace with actual and projected CPI1 , and therefore retain its value to individuals, the lifetime allowance would need to rise to £1,432,337 by 2026, according to our calculations.

What does it mean for investors ? The combination of long-term investment growth and high inflation could see more people inadvertently breaching the lifetime allowance and facing a hefty tax charge when they come to draw pension income.

Pension tax relief

What has changed? Nothing. There were rumours that the chancellor was considering scrapping higher rates of pension tax relief and moving to a single flat rate of 20%, but this did not come to fruition.

What does it mean for investors? Higher and additional-rate taxpayers can continue to benefit from tax relief of up to 40% and 45%, respectively (subject to limitations).

State pension

What has changed? The state pension will increase in line with inflation by 10.1% in April 2023.

What does it mean for investors? Those who qualify for the full state pension will receive an additional £870 in the 2023/24 tax year.

The economy

This autumn statement was accompanied by the OBR’s economic and fiscal outlook5 , which painted a gloomy picture of the UK economy. High inflation is expected to result in living standards declining by 7% in total over the two years to 2023/24, wiping out the previous eight years’ growth. The OBR warned that the squeeze on real incomes, rise in interest rates and fall in house prices would weigh on consumption and investment, tipping the economy into a recession lasting just over a year from the third quarter of 2022. GDP is forecast to fall by 1.4% in 2023 before rising by 1.3% in 2024 as energy prices and inflation drop.

While government borrowing is forecast to rise from £133.3bn, or 5.7% of GDP, last year to £177.0bn this year (7.1% of GDP), it should gradually fall to £69.2bn (2.4% of GDP) in 2027/28 as a result of tax rises and scaledback fiscal support. Similarly, underlying debt is projected to rise sharply from 84.3% of GDP last year to a 63-year high of 97.6% in 2025/26, but then fall modestly in the subsequent two years.

With such a wide range of measures being announced, Guy Foster, our Chief Strategist, shares his views on how they could affect the economy and investors.

Even without the extensive trailing of measures in the media, the tax hikes and spending cuts in this autumn statement were to be expected, coming in the shadow of former chancellor Kwasi Kwarteng’s widely criticised minibudget. Hunt would have been keen to avoid the market turmoil created by Kwarteng’s now-scrapped tax-cutting measures and, instead, demonstrate to the markets that the UK government is capable of making responsible spending and taxation decisions. Estimates of the size, or even the existence of, the fiscal black hole vary, but if markets lose faith in the government, it can lead to higher borrowing costs which ultimately hit consumer spending as interest rates rise.

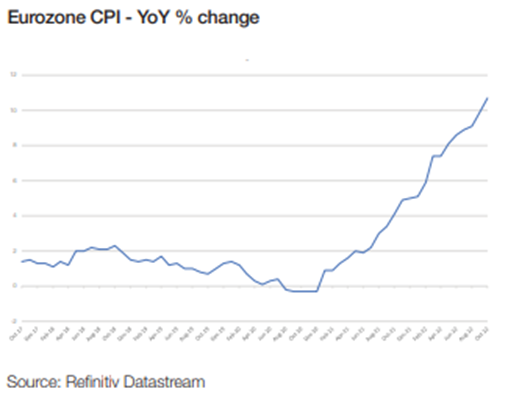

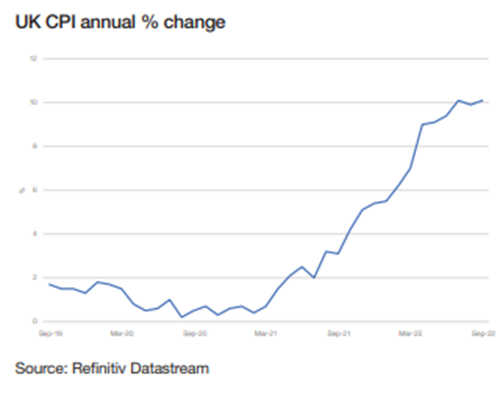

Higher taxes and lower spending should eventually help to bring down inflation, which rose to a 41-year high of 11.1% in October. This will, however, be of little consolation to households who face paying more tax at a time when wallets are already squeezed. Freezing tax thresholds draws more people into the income tax net, more assets into taxable estates for inheritance tax purposes, and diminishes the real value of the pension lifetime allowance.

The challenge for the chancellor has been to confront inflation without damaging the UK’s longer-term growth prospects. Like many developed economies, the UK has seen declining birth rates and rising life expectancy, which is a headwind for economic growth. It makes it harder to maintain a low tax base for a given level of public services, and makes achieving higher productivity more important than ever. Yet trying to increase productivity comes with many challenges: changes now may take a long time to bear fruit; determining how much benefit measures will yield is highly subjective; and there is invariably some sort of cost to such measures – either economic (i.e., investment in education) or political (i.e., immigration or planning reform).

Nonetheless, the announcements confirming funding for the Sizewell C nuclear power station and HS2 rail project, along with reforms to Solvency II insurance rules that aim to free up funding for infrastructure, were among the measures demonstrating that growth was an important part of the chancellor’s juggling act.

Please check in with us again soon for further relevant content and news.

Chloe

18/11/2022