Please see below article received from Tatton Investment Management this morning, which reflects on the market’s reaction to global banking issues over the past week.

Overview: Bank stress-testing in real-time

Following the run on Silicon Valley Bank (SVB), fear has spread. The nervousness of market participants over recently elevated stock and bond valuations found its focal point and so the stock index of the aggregate global bank sector had a very bad week. SVB has become the first sizeable victim of the steepest rise in rates since the 1970s, but its close affiliation with tech, healthcare and crypto is particularly notable. After seeing a near tripling of money deposited by start-up companies and their affiliates during the good times (namely the 2020/2021 tech and healthcare boom), those deposits were heavily drawn on recently when those same companies required funds to bridge the financial strains of these distinctively more challenging times.

Taking into account how much better capitalised and less credit risk exposed banks are today when compared to the run up to the GFC, they seemed an unlikely target and victim this time, but it turns out banking sector trust had never been fully rebuilt. Given SVB specific weakness was an outlier, with its losses from its long maturity government bonds wiping out its equity base, it was right that central banks stepped in to stop the self-enforcing avalanche of mistrust. That stock markets continued their highly volatile trading into the latter part of the week goes to show that once confidence is dented investor are more open to consider that there is the possibility for a much worse than the ‘steady as she goes’ scenario that could play out this year.

The lesson from the past few days is that the pain caused by the rises in rates is hitting small and micro-cap firms particularly hard, even if they are strictly speaking growth stocks whose valuations would otherwise benefit. But we should be heartened that this week proved central banks are reactive to issues of financial instability. The centre of the storm moved to Europe and particularly Switzerland as Credit Suisse came under pressure. The European Central Bank (ECB) still raised rates by 0.5% on Thursday as it had promised at its previous meeting, but President Christine Lagarde was notably reticent about offering any further indications of rate moves.

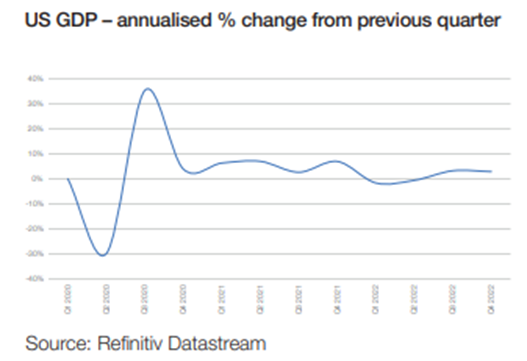

To top it all off, the market is now pricing in the strong likelihood that March will see an end to all the rate rises in the Western world, and that rates could be cut everywhere by year-end. This week, the Federal Reserve (Fed) and the Bank of England (BoE) meet. Despite the turmoil, markets on balance expect a 0.25% move from both. We have revised our views as well and see a 0.25% move in the US where data remains strong enough to justify it, but we expect the UK will not move. So, for the shorter term it appears that central banks’ objective to tighten financial condition to bring down inflation has suddenly been significantly accelerated through market action.

Is this a banking crisis? And if so, could it get as bad as last time?

What makes a crisis a crisis? Ernest Hemingway said bankruptcy happens “gradually, then suddenly”. Weaknesses build up over time, and wider economic circumstances add pressure on them. But for any given company, the full extent of its weaknesses is only revealed when things get so bad those weaknesses cannot stay hidden. The nature of banks means the financial system is more vulnerable than other sectors. Often the first bank failures in a downturn don’t precipitate a crisis but they do reduce the system’s overall willingness to tolerate risk. When the next set of bad news gets out, confidence plummets and financial problems spiral. We saw this a decade and a half ago with Bear Stearns and later Lehman Brothers. Cracks emerge slowly, but shattering happens all at once.

Over the last year, interest rates have risen at the fastest pace in a generation. Meanwhile, economic growth has slowed dramatically. That means higher capital costs with lower aggregate returns, a difficult environment for banks as a whole. When crypto hub FTX collapsed last year, we said this was a sign of the times – opaque high-risk investments being exposed – and that further casualties down the line were likely. That is exactly what happened with Silvergate Capital l, and then SVB.

The fact that troubles have spilt over to Credit Suisse is a sign that contagion is still very possible, though. Even if the US tech banks can fail in a relatively isolated fashion, a bank as big and important as Credit Suisse is a different matter. Moreover, European banks are much more tightly linked than US counterparts. If Credit Suisse had been allowed to collapse, shockwaves would have been felt far away, and weaknesses at other banks would certainly be exposed. The Swiss regulators’ decision to wipe out holders of Credit Suisse Coco bonds as part of the UBS ‘shot-gun’ marriage deal may still prove too much for the system, with a need to address the failout in some way. That being said, there are two key differences to the events of the global financial crisis. First, the policy response has been swift and decisive. In the US, the Biden administration effectively bailed out depositors of a bank considered too small to be systemically important, as soon as troubles began. Meanwhile, SNB provided billions in liquidity to Credit Suisse on the same day its stock sunk. The long-term merit of these moves is debatable; indeed, European lawmakers are reportedly angry about the US flouting bailout rules they helped create. But they undoubtedly make short-term financial contagion less likely. Second, crises spiral when unknown risks come to light, but most of the current risks exposed at Credit Suisse were already in the light, and known about for some time. We should not underplay the troubles that could spread from such a big institution, but it is important to note that many other banks will have already reduced their exposure to the investment bank.

We have no doubt that further problems – at different, as yet unknown banks – will become known in the weeks and months ahead. Such is the nature of a monetary tightening cycle. Those institutions that end up in trouble will be those with opaque or misleading balances of assets and liabilities. In that respect, we also expect financial hardship at some (probably recent entrant) private equity or private debt funds (private meaning not available to the general public and therefore not part of Tatton’s portfolios). It may be that such hardship catches only a very small number, and will be seen as idiosyncratic and containable as the demise of SVB, but it is something of which investors should be wary.

Please check in again with us shortly for further market updates and news.

Chloe

20/03/2023