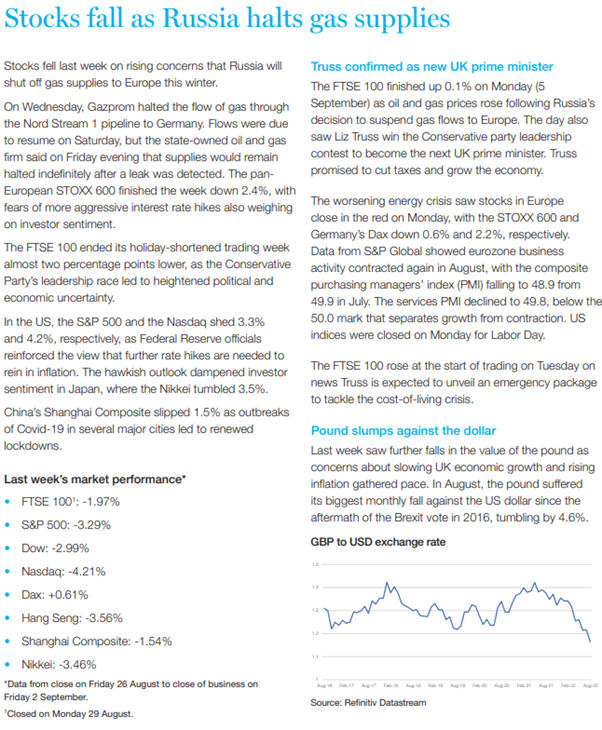

Please see this weeks Brewin Dolphin’s Markets in a Minute update:

Please continue to check back for our regular blog posts.

Andrew Lloyd DipPFS

07/09/2022

Please see this weeks Brewin Dolphin’s Markets in a Minute update:

Please continue to check back for our regular blog posts.

Andrew Lloyd DipPFS

07/09/2022

Please find below, an insight into Liz Truss becoming PM received from Brewin Dolphin yesterday evening – 05/09/2022

Following the news that Liz Truss will become the next prime minister of the United Kingdom, Guy Foster, our Chief Strategist, looks at what this means for investors.

Despite not being the favoured candidate among Conservative MPs, Liz Truss has been the frontrunner since the contest was put to the party membership as a straight choice between the foreign secretary and the former chancellor, Rishi Sunak.

The two candidates have been campaigning at hustings events for the last five weeks, with the debate frequently becoming fractious between the two.

Both had talked of their ambitions for growth based on lower taxes.

However, there were some clear dividing lines, particularly with their proposed approaches for managing the cost[1]of-living crisis. Truss has argued for tax cuts immediately while Sunak prioritised curbing inflation first. Both would have needed to adjust their plans in light of the latest increases in gas prices and the prospect of real social unrest this winter.

All incoming prime ministers presumably have a pretty full inbox when they arrive, but this seems particularly the case this time around. As a result, much attention has been focused on the candidates’ statements around the financial support they would offer if they became prime minister.

Truss had said she would hold an emergency budget in September, but that has subsequently been relabelled as a fiscal event where she is nonetheless expected to deliver some of her core tax commitments.

Tax cuts?

There have been a number of tax cut proposals floated over the course of the campaign. Two of the most notable include reversing her rival’s increases to national insurance (the health and social care levy) that was introduced in April, and cancelling the planned increase in corporation tax to 25% that had been due to come in from April 2023.

Alongside those, there have also been pledges to cut fuel duty and suspend the green energy levy, as well as less specific plans to support people with energy costs through the winter. These suggestions are all designed to put more money back in people’s pockets.

None of these pledges will come cheap; the first two alone are forecast to cost almost £28bn by 2023-241.

Truss also considers that the tax system would be fairer if households were treated as a single tax entity; this would reduce the tax burden on those providing unpaid care, but might incentivise people to leave low paying jobs.

Of course, we will have to wait and see what changes the new prime minister chooses to make once she has her feet under the desk – the economic choices that need to be made may seem less palatable than when discussed on the hustings.

The impact on investors

It’s important to remember that the performance of the UK economy is usually relatively muted in its impact on investment portfolios. Most large UK companies are not particularly exposed to the UK economy, being more multinational in nature. For the largest companies, their country of listing is almost a historical accident.

However, some companies do have a specific UK focus, particularly supermarkets and some other retailers as well as some financial companies.

As you move further down the size spectrum, many mid and smaller sized companies will be progressively more exposed to their local market. If investors believe UK consumers will find life hard (as they do) then they will value companies selling to those consumers a little less generously.

And there are additional effects too, as most UK investments will be affected to some extent by the outlook for the pound and interest rates.

In the run up to the result, the pound has been very weak.

That reflects the particular challenge the UK is facing in terms of soaring inflation, most notably from rising energy prices. The most dramatic weakness has been relative to the dollar, but that is a reflection of dollar strength as much as sterling weakness. Recently though, the pound has been underperforming the euro as well and that should be concerning for Truss, because the pound weakened as her likelihood of winning increased.

Similarly, government borrowing costs, which were rising as a result of the steeper trajectory of UK interest rates, seemed to rise faster as a Truss victory became more likely.

The new prime minister has successfully convinced the Conservative membership she is the right person for the job, but delivering on her promises will be difficult.

She has already been accused of designating the presentation of her economic plans as a fiscal event, rather than a budget, because that will avoid the need for the Office for Budget Responsibility (OBR) to scrutinise them. The markets, however, are passing judgement on them already.

The good news is that the pound’s weakness has been a benefit for the majority of UK companies who earn their revenue in foreign currencies. It has been a bigger benefit for overseas equities within client portfolios.

It does make holding longer-dated UK government bonds risky if, as Sunak has suggested, the UK were to lose the confidence of the markets. However, the chances of a default on a UK government bond are virtually nil because the central bank can print its own currency.

While shorter-dated government bonds anticipate future increases in interest rates and so are already providing a more attractive yield than is available in bank accounts, a quirk of the pandemic-era issuance means that, for many UK taxpayers, holding short-dated government bonds as a savings instrument is often hugely preferable to keeping cash in deposits.

The importance of the markets

The UK has a history of being unable to follow through on some policies because of the market’s reaction. One of the most notable examples was its withdrawal from the exchange rate mechanism, which ended up being economically advantageous for the economy.

Famously James Carville, economic advisor to Bill Clinton, once said: “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

The new prime minister will need to have a policy agenda which appeals to her MPs, their voters, and eventually the OBR, and is at least tolerable for the markets.

The implications for portfolios are that we could see further weakness in bonds and the pound until the market builds confidence in the new prime minister. We protect against the weak pound by holding overseas securities. Weaker bonds are a more immediate threat and so we are cautious on this part of the market. However, the weaker they become, the higher the yields they will offer for the future.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

David Purcell

6th September 2022

Please see below an article from Waverton Investment Management which was published and received earlier today (02/09/2022) and provides some insight on what to expect from a Liz Truss Government:

Tim Shipman, Chief Political Commentator at The Sunday Times, spoke to Waverton clients on the likely outcomes of the recent Conservative Party leadership vote.

It is expected that Liz Truss will prevail over Rishi Sunak when the results are announced on Monday 5 September, and Tim was able to talk with great insight about the possible implications of this change of leadership.

Liz Truss would be the fourth Prime Minister in six years, although she was initially felt to be an unlikely candidate to win the Conservative leadership by the media and her parliamentary peers, she is in fact an experienced candidate with a long track record in the cabinet. She does not fit the stereotype of Conservative leaders, having been raised in Scotland before moving to Leeds in a comparatively left-wing family. Indeed, her father is reported to be undecided as to whether he would vote for her, her mother though “probably will”. Her upbringing seems to have contributed to a relatively flinty character with a lot of backbone. She is quite self-contained and she has endured ups and downs in her political career already.

It is hard to know exactly what her plans are, assuming that she wins, but there are a few policies that she has put forward; it is expected that there will be no new taxes and that she will symbolically reverse the national insurance rise. She has also said that there will be no energy rationing – which went against the expectations of some of the other members of her party. She is expected to look at cutting business rates and potentially provide additional support to small businesses, many of whom are suffering with the current high cost of energy. A temporary cut to VAT is also being discussed – which they are said to believe will help to limit inflation. There is a non-zero chance that once in office the next prime minister will declare that the situation is far worse than expected and follow a different path to the one on which they ran.

There is little doubt in Whitehall that the next 18 months are going to be tough, the Brexit issues rumble on, as they did for Johnson, and there is elevated inflation as in the 1970s. Thankfully, for now, the labour market remains strong, though that is not a given. There is talk that there might be a more front-and-centre approach to dealing with the cost-of-living crisis (as with the Covid pandemic), with regular briefings and a task force. There is also talk of having a Cost-of-Living Minister.

While there will be some work on the leveling up program, the first few weeks are likely to be dominated by the economy. An emergency budget is expected on 21 September, right before the Labour Party conference. Despite how serious the problems caused by the cost of energy may prove to be this winter, the political process is probably too slow to react in time with new measures. One solution is to adjust the value of the payments that are expected to go out this autumn. Alternatively help could be directed via Universal Credit. Estimates suggest that she will need to borrow significantly further to fund her economic plans.

The timing of the emergency budget means the Labour Party are left in an interesting position. They were reportedly caught off guard by the rise of Truss, though are able to challenge her ideologically. Their plan was to cleanse the Labour Party’s image, introduce Starmer to the public and provide coherent resistance to the government, as they slowly start to look like a serious government in waiting. Starmer is struggling to cut through with the public but is expected to make an important speech at the end of September. Truss can probably expect a bounce before the polls settle to a new equilibrium.

The appointment Liz Truss would be most likely to make is that of Kwasi Kwarteng to Chancellor of the Exchequer. Suella Braverman is leading the race to be Home Secretary and James Cleverly is frontrunner to be Foreign Secretary. It is expected that Iain Duncan-Smith will play a more prominent role again, as will the Thatcherite John Redwood most likely in the Treasury, where he may well be joined by Jacob Rees-Mogg. Perhaps the two most watched of her colleagues will be Rishi Sunak, who is expected to turn down a cabinet job should he be offered one and has said that he intends to remain as a backbencher (though he has not convinced everyone that this is his long-term plan), and Boris Johnson, who is likely to find that his every word is pored over on all fronts.

A trip to Ukraine is likely to be first on the travel agenda, as Truss seeks to provide continuity from Johnson’s stance. She is also believed to be very keen to visit the White House, though the Biden administration is reportedly less excited at this prospect. It may be that a trip to Dublin to discuss the Northern Ireland border would help pave the way to visiting Washington. Relations with Scotland are not good, but not likely to be any worse than under Johnson.

While we at Waverton acknowledge the importance of the new Prime Minister, as global investors the proportion of UK exposure is comparatively low within our portfolios. The Prime Minister can have a significant impact on the UK financial markets, particularly via changes in investor sentiment initially, but the global economic environment is often the larger factor. We will continue to monitor the potential impacts of the changes in Downing Street closely and are able to adjust our positions as the situation develops.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

02/09/2022

Please see today’s Daily Investment Bulletin from Brooks Macdonald received this morning:

What has happened

Both US and European equities fell on Wednesday, marking for both a fourth consecutive session of declines, and ending August at month lows. Mirroring equity falls, bond prices were also lower, as markets pushed bond yields higher on the expectation that central banks are increasingly in a corner over having to raise rates to tackle current energy-led inflation pressures. Also knocking sentiment overnight is the news of a new COVID lockdown in the Chinese city of Chengdu, making it the largest city to be locked down since Shanghai earlier in the year.

Eurozone inflation heaps pressure on ECB ahead of rate decision

Wednesday saw the flash estimate of Eurozone CPI for August, coming in at 9.1% Year on Year (YoY), a new record high, up from July’s 8.9% and ahead of the 9% estimate expected by the market. While energy prices were a predictably large component, core CPI (excluding food and energy) was 4.3% YoY, ahead of 4.1% expected. Services inflation rose 3.8% YoY. The data heaps more pressure on the ECB ahead of their next monetary policy meeting due next Thursday (8 September), with some ECB members in recent days seemingly opening the door to considering a larger 75bp move. In terms of what markets are expecting, overnight index swaps are now pricing in a 69bps hike for the next meeting, so closer to 75 than 50.

US dollar currency strength continues

The US dollar index (DXY) saw a third month in a row of gains in August, holding close to 20 year highs. The latest boost for the Dollar came on the back of a hawkish rebuke from Fed Chair Powell at Jackson Hole last week, as markets factored in higher US interest rates for longer. Of course, with currency pairs, the strength of the Dollar and the DXY index owes just as much to weakness in other currencies, including notably the Euro. Currency movements are often multi-faceted, but a key factor behind currency pairs this year has been energy. Versus relative US energy independence, Eurozone countries have been much more exposed to higher energy prices, forced to switch from buying previously relatively cheap Russian gas priced in Euros, to currently more expensive international LNG cargoes priced in US Dollars. Impacting broader terms of trade, this has fed into mounting Eurozone economic growth concerns, putting downward pressure on the Euro relative to the Dollar,

What does Brooks Macdonald think

A stronger outlook for US interest rates and the dollar continues to be a headwind for many countries globally, in particular, some emerging market economies. First, a stronger dollar and US interest rate outlook can impact and even reverse capital flows into emerging markets which are often reliant on foreign investor inflows in order to fund local government funding. Second, a stronger dollar can impact the relative cost of dollar denominated debt where emerging market economies have historically taken advantage of relatively low-cost dollar finance to support government financing.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

01/09/2022

Please see the below article from Blackfinch providing an overview of Technology Sector Stock performance, and their input on the future of the Global Technology Sector for investors. Received yesterday evening – 30/08/2022

Within the Blackfinch Asset Management Team, we are often asked for our views on the outlook for global technology stocks. The global technology sector is rich with forward thinking leaders and innovation in their respective fields. We’ve historically seen heavy investment into research and development (R&D), focused on launching unique and market-leading products that will generate substantial and sustainable positive cashflow well into the future.

Naturally, these companies are expected to grow their earnings and sales at a faster rate than the rest of market. As such, the shares of tech companies can look ‘expensive’ as they trade at a higher price-to-earnings (P/E) ratio than many of their less expensive or lower growth counterparts. Even with a higher-than average valuation, the long-term outlook for these tech companies can prove attractive if they continue the trend of strong expansion and ultimately share price growth.

Technology companies – particularly in the US – enjoyed significant share price growth at the onset of the COVID-19 pandemic. When the pandemic shook markets in March 2020, many companies were catapulted into the future, as they were forced to implement digital transformation across their business models. Market demand evolved almost overnight, the typical ‘office work environment’ became a thing of the past, and many tech companies offered an immediate, effective and efficient solution to the new challenges faced by consumers and businesses. While other sectors struggled, many of the largest tech companies reaped the reward of this market shift. For example, Amazon lapped up the heightened demand as their infrastructure could withstand this newfound supply pressure. Amazon enjoyed a near 38% increase in annual sales in 2020, and a subsequent 76% surge in its share price for the year.

This narrative of adaptation continued in 2021, when companies placed a greater emphasis on improved workforce transparency and flexibility. Firms needed their employees to reorientate and reskill to optimise their remote work outputs, and business leaders embraced advanced technology such as Artificial Intelligence. This activity was immediate and reactive, due to the unnatural impact the pandemic had on company cashflow.

The first half of 2022 saw several well-managed tech companies that fit the ‘growth’ profile experience a mass sell-off. In some cases, share prices were unfairly punished. However, this has created ample opportunities for active managers to pick up these typically ‘high valued’ names at a lower premium than in recent years.

In our view, this is an important year for these technology companies to adapt and innovate, with sustainability being a key theme. This can be achieved through many ways, such as embracing cloud computing to drive transformation, adapting their supply chains to account for future uncertainty, and focusing on reducing their environmental impact. The fundamentals of a technology company have become even more important for investment, which we explore below.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

31/08/2022

Please see below article received from Tatton Investment Management this morning, which provides a market update on Europe, the UK and the US.

Resolute Fed leaves markets in a delicate equilibrium

All eyes were on the annual Jackson Hole conference last week, where mildly hawkish US Federal Reserve (Fed) chair Jay Powell declared it “must keep at it until the job is done”, repeating his emphasis on controlling inflation and cooling wage demands. This has made investors nervous. Equities rallied last month on the back of improved valuation metrics, but bond market positivity was in large part down to expectations of a less hawkish stance. We suspect that this year’s downward stock market volatility has led to a delicate equilibrium between the negative impact on earnings and the positive reaction that could come from central banks. Should the Fed prove successful in engineering an inflation-busting slowdown in the labour market without an economic crash landing, there will be less upward pressure on bonds. ‘Delicate’ is the key word here.

Consumer and now also business confidence has taken a downturn, signalling a slowdown in growth, particularly in the US. But despite the gloom, profit margins have held up nicely across the Atlantic. In fact, recent data shows US corporate profit margins expanding to their best ever ‘book profit’ level in the second quarter of 2022. Cash flow is still remarkably strong, giving companies a buffer for the difficult times ahead. Particularly interesting is what this means for different investment styles. So called ‘growth’ stocks, like big tech companies, are usually heavily dependent on bond yields, as they are long-duration assets and therefore sensitive to assessments of long-term risk premia. But bond yields are clearly no longer the only driving factor behind these stocks. The biggest names – Amazon, Netflix, Microsoft and Apple, to name a few – have unquestionably come of age and are now by far the biggest players in their respective sectors. This means that their growth is not so much at the expense of old businesses, but rather a reflection of the market as a whole. Being exposed to the ups and downs of the economic cycle creates new dynamics and new avenues for growth and investment returns. For the discerning investor, this delicate equilibrium could be full of opportunities.

Strategies needed to mitigate Europe’s energy crisis

Closer to home, the UK was hit by the latest news of a near doubling of Ofgem’s energy price cap for the winter months. The arrival of a new prime minister must surely bring more government support for households. Even with government help, households will inevitably struggle, but businesses are under threat too. There is no price cap for businesses, meaning energy costs have increased several times over. Providing support for those businesses – particularly small and medium sized enterprises – is imperative in the months ahead. This is akin to the situation at the start of the pandemic: without help, small businesses will have to shed staff or face total collapse.

Heading into the winter, the energy outlook is harsh across all of Europe. Policymakers have discussed rationing and power outages at length, but there are no coordinated plans yet. In lieu of central edicts, the market is left to do its own energy rationing – as firms or consumers get priced out. Politicians have been quick to signal their support for households in all of this, but help for businesses has been less forthcoming. All across Europe, businesses face worsening conditions. Sales have already slowed somewhat, and inventories of goods have risen. Europe may already be in a recession and business sentiment surveys now firmly point toward contraction in the second half of 2022, while corporate debt is showing severe signs of stress. If politicians want to avoid a harsh economic winter, their options are limited. For now, it looks likely that Putin will keep using gas supply as a weapon in his hybrid warfare.

Business sentiment takes another battering

August’s sentiment surveys of consumers and businesses paint a rather unpleasant picture for the world economy. Consumers everywhere are not confident and have not been so for some months. This is particularly true in the EU, where confidence measures continue to languish near or at record lows. For the UK, July’s GfK consumer confidence survey hit a new record low of -44. Business confidence surveys, in the form of the Purchasing Managers’ Indices (PMIs), are even more timely than the consumer confidence data. Last week’s flash data for August across developed markets showed the ‘all-industry’ or composite PMI fall to 47.3. Relative to manufacturing, service industry confidence had been holding up relatively well in the first half of 2022, but the August service PMI data was notably weaker than expected. On the other hand, through the past month data sourced from actual activity has kept relatively robust. In Germany, consumer spending is holding up despite the constant depressing news flow. Importantly, jobs are still secure. Firms seldom make significant staff changes in the summer months, partly because doing so takes a lot of management effort.

Last week’s PMI data did not include China, as its data collectors do not publish flash estimates. Instead, they wait for the full release which will arrive in the first days of September. Last month, China’s service PMI data improved sharply and, given the flash PMI weakness of so many other areas, it will be hoped such resilience can be maintained. PMIs have been signalling a deteriorating environment for the past three months. That has worsened with this month’s output and new orders PMI data. As we emerge from a long hot summer, we are hoping employment remains resilient, but not as overly tight as it has been. Hopefully the future output data will signal a stabilisation of confidence for both consumers and businesses.

Please check in again with us soon for further relevant content and market news.

Chloe

30/08/2022

Please see below an article published by AJ Bell yesterday (25/08/2022) and received today (26/08/2022), which details Franklin Templeton’s Emerging Markets Team views on Emerging Markets:

1. Latin American markets rebounded in July, with Chile, Brazil and Peru among the leading performers, while Mexico and Colombia lagged. In Brazil, a smaller-than-expected increase in consumer prices in the first half of July, raised expectations of the start of a downward trend in inflation. Additionally, the labour market continued to recover with June unemployment falling to its lowest level since 2015. Although Mexico’s second-quarter GDP growth exceeded market expectations, investors expect to see easing growth in the second half of 2022 on the back of weaker US demand.

2.Earnings growth in emerging markets (EMs) for 2022 has been cut to -6% from +6% at the start of the year, based on consensus estimates. China has driven the reduction in EM earnings growth, with forecasts for 2022 declining to 4% growth from 14% over the same period. Analyst earnings revisions indicate further downward pressure on earnings forecasts is likely. The first half 2022 earnings season is expected to be weak, but the market has already discounted this scenario. Investors are likely to focus on guidance for 2023. Consensus expectations for next year call for 8% growth, relatively unchanged since the start of the year.

3. The US dollar trade-weighted index weakened modestly in July after reaching a cycle high in the month as investors discounted the timing of a peak in the US interest-rate cycle. The direction of the US dollar matters to EMs as it influences capital flows and the availability of liquidity. A strong US dollar tends to coincide with capital outflows and reduced liquidity availability in EMs, whereas a weak US dollar tends to coincide with capital inflows and the opposite trend for liquidity. As the US dollar strengthens and liquidity declines, companies with foreign currency debt find it harder to refinance foreign currency debt or raise new loans and vice versa. Expectations that the US Federal Reserve may be closer to the end than the start of its rate-hiking cycle have recently led the US dollar to weaken, leading to an improvement in liquidity conditions in EMs – foreign fund flows have increased into selected EMs, including India.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

26/08/2022

Please see below today’s Daily Investment Bulletin from Brooks Macdonald – received this morning – 25/08/2022

What has happened

Bond markets continued to price in higher central bank interest rates as fears over the European energy sector weigh on inflation expectations. Despite this bond volatility, equities managed to make gains yesterday with longer duration equities, such as technology, somewhat counterintuitively outperforming.

European energy

European natural gas futures continued their climb yesterday as investors look ahead to higher demand during the winter period. There has also been a growing concern that Russia may not reopen the Nord Stream 1 pipeline after three days of closure from 31st August. Recent rhetoric has also pointed to little appetite for Russia to seek a ceasefire in the Ukraine War, making it ever more likely that Ukraine War related supply side issues will continue well into 2023. Freeport LNG said yesterday that their natural gas terminal in Texas, which was shut down due to an explosion and fire, would not be reopened until November, later than energy markets had hoped. The latest rises in European energy prices quickly filtered into ECB rate expectations with the bond market now expecting 133bps of additional rate rises before the end of this year.

US politics

President Biden announced yesterday that the US would be providing student debt relief of up to $10,000 for graduates on an income of less than $125,000. Those receiving Federal aid would also be eligible for a larger payment. Federal student loan repayments are currently frozen and this pause will now be extended until the end of this year. This is very much a response to the cost-of-living squeeze in the US and while the US cost-of-living pressures are less pronounced than within Europe, the upcoming mid-term elections make proactive economic policy particularly politically attractive.

What does Brooks Macdonald think

Only a few months ago the Democrats looked likely to lose both the Senate and the House of Representatives in November. Recent legislative wins and targeted economic support, such as yesterday’s student loan programme, have put the Democrats odds on to retain the Senate and close to a 25% chance of retaining the House (which was always a distant prospect). Political cycles, and the global lack of appetite for austerity, mean many governments will be tempted to reach for accommodative fiscal policy at this time. Central banks are already wary of this risk however, in case it prompts even higher inflationary pressures.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Cyran Dorman

Trainee Paraplanner

25/08/2022

Please see this weeks Markets in a Minute update from Brewin Dolphin received late yesterday afternoon:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

24/08/2022

Please see below this week’s Weekly Market Commentary from Brooks Macdonald – received late yesterday afternoon – 22/08/2022

Weekly Market Commentary | Investors’ focus on inflation sees equities lose ground

22 August 2022

By Edward Park

The expected divergence between US and European inflation weighed on equities last week

US and European equities lost ground last week as investors focused on the near-term desire from central bankers to further reduce inflation expectations. This led bond markets to price in additional near-term rate rises which weighed on interest rate sensitive sectors such as technology.

This week’s annual Jackson Hole forum will see Fed Chair Powell address July’s US Consumer Price Index (CPI) downside surprise

This week’s macroeconomic focus will be the annual Jackson Hole economic symposium which takes place from Thursday until Sunday. The most important event within the forum will be Federal Reserve (Fed) Chair Jerome Powell’s speech on inflation and economic growth which takes place on Friday. The recent rise in equity markets, and more lacklustre week last week, has been closely correlated with the ebbs and flows of the market expectations around the evolution of Federal Reserve policy in the face of retreating inflationary pressures in the US. The US Fed is very much focused on further reducing consumer and corporate expectations around future inflation so there is unlikely to be a huge pivot in how the Fed refers to upcoming monetary policy. That said, Powell himself said that the committee were highly data dependent given the uncertain path of inflation. Therefore, with July’s CPI number suggesting that we may have seen peak US inflation, how Powell expects the committee to react to that data will be an important determinant of market sentiment over the coming weeks.

July’s European Central Bank (ECB) minutes, released on Thursday, are likely to show a central bank boxed in by inflation and poor growth prospects

The ECB meanwhile have an even trickier policy tightrope to walk with Europe experiencing economic pressures, energy price surges and stickier inflation. On Thursday, the ECB will release the minutes from their July meeting and the balancing of inflation and recessionary risks is likely to be the main debate between board members. The tail end of the week also sees flash Purchasing Managers’ Index (PMI) surveys of business activity as well as European consumer confidence gauges which have been particularly poor in recent months.

One of the main themes of last week was the expected divergence of economic growth, inflation and monetary policy between the US and Europe over the short-to-medium term. The latter part of this week may put this in stark contrast with the ECB minutes showing a central bank boxed in by inflation and Powell’s speech having more room for manoeuvre given the downside surprise to the latest US CPI reading.

Please continue to check back for our latest blog posts and updates.

Charlotte Clarke

23/08/2022