Please see below article received from Brewin Dolphin yesterday evening, which provides a positive outlook on the UK economy and global markets.

The UK has been the subject of many headlines in recent weeks as journalists and politicians spar over the country’s economic performance. Ironically, this comes at a time when the economy is doing very little. We therefore felt it might be worth giving some consideration to the true state of the UK economy and what it means for investors.

Recession bound?

Traditionally, we measure economic strength by looking at the speed of growth (or shrinkage) in economic activity. The go-to measure here is gross domestic product (GDP). Faster GDP growth is assumed to be better, while two consecutive quarters of declining GDP is often considered a technical recession.

Speculation has been rife recently over whether the UK will enter a recession. If the economy shrank during the final quarter of 2022, then it would meet the technical definition of a recession because it had already contracted in the third quarter. Hence, there was great focus on the first estimate of growth for that period. As it transpired, it neither grew nor shrank, meaning that a recession has been averted for now. This splitting of hairs misses the point that the UK economy stagnated during 2022 and is in danger of doing the same during 2023.

Taking 2022 and 2023 as a whole, a recession could be avoided, or suffered, but the likelihood is that either way the economy will be a lethargic performer throughout. When we talk about the risk of a recession in the UK it conjures pictures of queues outside job centres as unemployment picks up sharply. But the opposite remains the problem for now. Jobs growth has been strong and the challenge for businesses has been finding workers.

Although the worst fears of rapidly rising energy bills due to spiralling gas prices have been eased by a warm winter and bolstering of gas supplies, prices seem likely to hover around the level of the fuel bill cap. More pressing will be the cost of refinancing mortgages for anyone whose deal is coming to an end. Mortgage interest rates have moved sharply higher during the last few years. Taxes are also set to rise from April in a bid to shore up the public finances.

The current economic environment is a difficult one, and so lower rates of growth might be inevitable to some extent.

New highs for the UK stock market

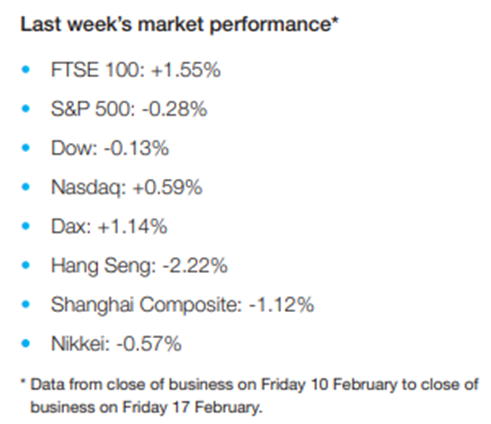

At the same time, though, the FTSE 100 has hit all-time highs. While rising oil and gas prices have weighed on the UK economy, they have helped the commodity-sector[1]heavy FTSE 100 rise by 6.2% year-to-date and breach the 8,000-point mark for the first time ever. Meanwhile, the FTSE 250 is up by around 5% year-to-date. This may initially appear counter-intuitive and, historically, the strength of an economy would inevitably have an impact upon the companies listed on the stock market there.

However, in one of the anomalous features of modern finance, that is no longer necessarily the case. Most of the major companies on the UK stock market are listed there by virtue of history, not as a reflection of their current business activities. Some 80% of FTSE 100 revenues and 50% of FTSE 250 revenues arise from outside the UK. Most companies gather sales from around the world, and a few are even specifically focused on individual countries outside the UK.

That is not just the case in the UK. New technology companies seeking to list on the stock market would feel inclined to do so on the US Nasdaq exchange, almost no matter where they were founded.

The long term

If we were to look to the long term, what can we conclude about the UK?

Convention dictates that we should judge the UK’s performance relative to its peers in the G7. This is a collection of countries who loosely formed a group in the 1970s when they were among the biggest economies in the world, excluding the Soviet Union. Today, most of these countries remain towards the top of the table, with China and India having supplanted the Soviet Union.

Starting at a discreet distance, the UK economy has been a relatively strong performing economy against this peer group since 2000. The trailblazers have been the US and Canada, but the UK has outpaced its European peers.

Much of that strong performance for the UK, however, came in the early years and a series of shocks mark useful milestones to check on our national progress. Since the financial crisis, for example, Germany has pretty much caught up with the UK, while France, Japan and Italy have all lagged.

Looking ahead, we can observe that there are some features of the UK which act as impediments to its economic growth.

The most obvious is demographics. In many parts of the world, populations are growing more slowly or, in some cases, starting to decline. Demographics is one of the key determinants of growth. The UK population has been growing faster than its European peers, but Canada has been the fastest growing in the G7 both economically and in terms of population. The worst-performing economies for growth have been Japan and Italy whose populations, unsurprisingly, are contracting.

Connected with demographics is the fact that the UK is the second-most densely populated of the G7 (after Japan). This results in a lot of opposition to new development, particularly on greenfield sites. This has been a hindrance to economically stimulative activities such as housebuilding as well as new infrastructure projects such as rail links or runways. The UK has a similar population growth rate to that of the US but the latter is managing to grow more strongly than demographics alone would suggest.

The UK also has a disproportionate share of its economy devoted to services. One of the advantages of this is that many services activities create a lot of value. However, one of the shortcomings is that the services sector tends to experience less productivity growth than the goods and production sectors, where new tools and techniques see a more stable pace of efficiency gains.

All European states suffer relative to G7 highflyers like Canada and the US from being relatively poor in natural resources. The UK, in particular, with its higher-than[1]average population density, imports a higher share of energy and food than some other members of the G7.

Growth isn’t everything

If this description of the UK seems very downbeat, then some additional context is needed.

The UK has several strengths, most notably its time zone, its language, its legal system, its universities and its history. As a desirable place to work and live, the UK continues to be an attractive destination for talented young workers. The UK has a strong competence in technology and science, which is not represented in its investment market.

As mentioned at the beginning, GDP is a conventional way of measuring economic performance, but that doesn’t mean that it necessarily captures every aspect of standard of living, which most people would care more about. And which contribute to creating a desirable place in which to work and live.

What does this mean for investors?

When deciding which investment market to invest in, the constituents of the index are as important as the region it is based in. Technology is the largest sector in the US, for example. The UK, on the other hand, has quite a spread of industries represented. The biggest sector is financial companies but that can be misleading; many of them are investment trusts, which themselves invest across a whole host of other sectors within the public markets or more diverse asset classes. The UK is rich in defensive ‘staple’ goods, which are less exposed to the vagaries of the global business cycle. Conversely, however, it also has some of the most economically sensitive companies in the form of its substantial constituents from the energy and mining sectors.

Whilst it makes the market somewhat incoherent – it is neither defensive nor cyclical – it does mean investors in the UK have scope to choose from a lot of different kinds of companies.

The fact that UK stocks generally generate a lot of their revenues from overseas provides some benefits. When the UK economy performs poorly or suffers shocks, the pound tends to fall. We saw this around the global financial crisis, Brexit referendum and emergence of Covid. These falls increase the value of the overseas profits UK companies generate, which helps to cushion some of the falls (although the same can generally be said of overseas-listed companies too).

Other assets such as UK bonds, and particularly UK government bonds (or gilts), are more connected to the UK economy. When the economy is struggling with a more conventional recession, the Bank of England is expected to cut interest rates. This increases the value of UK government bonds, which pay a fixed rate of interest. Some government bonds provide protection against inflation as well, although they are still sensitive to interest rates; balancing the extent to which they may benefit from higher inflation but suffer from higher interest rates is a complex analytical task.

Across the spectrum of company shares, bonds and the pound, there are various ways to benefit from the UK, whether it is on the up or down in the dumps. Currently, we believe that the UK’s economic headwinds make gilts more attractive than most other government bonds. However, we have reduced our long-term UK equity weightings after a strong year that was driven by the resource-heavy nature of the market during 2022.

Please check in again with us shortly for further relevant content and news.

Chloe

17/02/2023