Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 24/02/2026.

Markets respond to political uncertainty

How continued U.S. tariff uncertainty and geopolitical tensions are affecting markets.

Key highlights

- Iranian shadow looms over markets: Oil prices (and associated equities) rose as fears grew over potential supply disruptions.

- U.S. Supreme Court rules against Trump tariffs: America’s highest court ruled that President Donald Trump’s emergency powers don’t include the authority to impose tariffs. Potential refunds could total as much as $170 billion.

- UK economic data shows signs of weakness: Economic data, including unemployment, wage and inflation data, broadly underlined the case for further UK interest rate cuts.

U.S. Supreme Court rules against Trump tariffs

The week ended with a landmark ruling from the U.S. Supreme Court, which upheld the view expressed by lower courts that President Donald Trump’s authority under emergency powers does not extend to levying tariffs.

The decision, which was reached by a margin of six votes to three, was widely expected, but included no detail on whether the importers are entitled to refunds. This will now need to be addressed by a lower court.

If fully permitted, refunds could total as much as $170 billion – representing the biggest portion of President Trump’s tariff revenue – but the agonising wait for a decisive legal decision from America’s highest court has only presaged a further wait for the detail be resolved.

President Trump responded by imposing a 10% global tariff under powers designed to prevent large balance of payment deficits.

The immediate reaction is one of weakness from U.S. bond markets and the dollar, as public finances are further weakened and an accidental tax cut is being delivered to a very distinct sector of the economy – even though the risk is that the refund issue becomes a drawn out legal argument.

Iranian shadow looms over markets

Source: Bloomberg

The risk of U.S. military action against Iran remains materially elevated. This has led to gains in oil prices, and the associated equity sectors, on fears of potential supply disruption. So far, diplomatic negotiations have failed. U.S. military assets, including the world’s largest aircraft carrier, continue being deployed to the Middle East, posing a significant potential threat to Iran.

This constitutes a major test of the TACO (Trump Always Chickens Out) framework. The administration has already launched airstrikes on Iranian facilities, so the question is how willing it is to make a greater commitment, and what objective such a commitment might have.

At the end of the week, President Trump twice referenced a period of 10 to 15 days, during which Iran would need to reach a deal with the U.S. to avoid military action. That was less immediate than the build-up of military assets in the region might suggest.

However, unpredictability is one of President Trump’s hallmarks, and Iranians will remember that a previous 60-day window was cut short by last June’s U.S. air strikes against Iranian nuclear facilities (on that occasion, America’s hand was rather tilted by the earlier Israeli strikes).

The other factor that will be weighing on the Iranian regime’s minds is this year’s extraction of President Maduro from Venezuela, which may indicate that regime change would be the objective of any operation. However, President Trump is a pragmatist, and his stated aim is to end Iran’s nuclear and ballistic missile programs. To what extent that requires a regime change is open to question. There’s a strong desire to avoid the extended deployments that were required in Iraq and Afghanistan in the early 2000s. In the case of Venezuela, for example, elements of the regime were retained and subject to U.S. pressure, avoiding the chaos that comes from a complete removal.

So far, the impact on oil is assumed to be roughly $6 to $7 of risk premium reflected in the current oil price.

Helima Croft of RBC Capital Markets notes: “Regional observers warn that Iran would target energy facilities and economic assets to force Washington to stand down. Using naval bases in Bandar Abbas and Jask, Iran retains the ability to target tankers and mine the Strait of Hormuz, while the Houthis in Yemen and Iraqi militias maintain significant disruptive capabilities.”

The base case of a limited U.S. strike would likely see oil prices spike initially, then unwind as disruption fears fade. However, the rule of thumb is that a 1% loss of supply can cause a 4% increase in price, and with the potential for widespread disruption to transit, significant action could push prices up to $100 per barrel or more.

President Trump’s administration will be very conscious of the domestic political impact of a price spike. It would weigh on growth and compound cost of living pressures, particularly for lower income cohorts. The president’s net disapproval over his handling of inflation has improved in recent weeks, but an oil price spike would change that, and the public support for military intervention in Iran is low.

The U.S. midterm elections take place in November, and Republicans are expected to lose control of the House of Representatives, which will radically alter the balance of power in Washington. With this in mind, a de-escalation would seem to be in the president’s best interests.

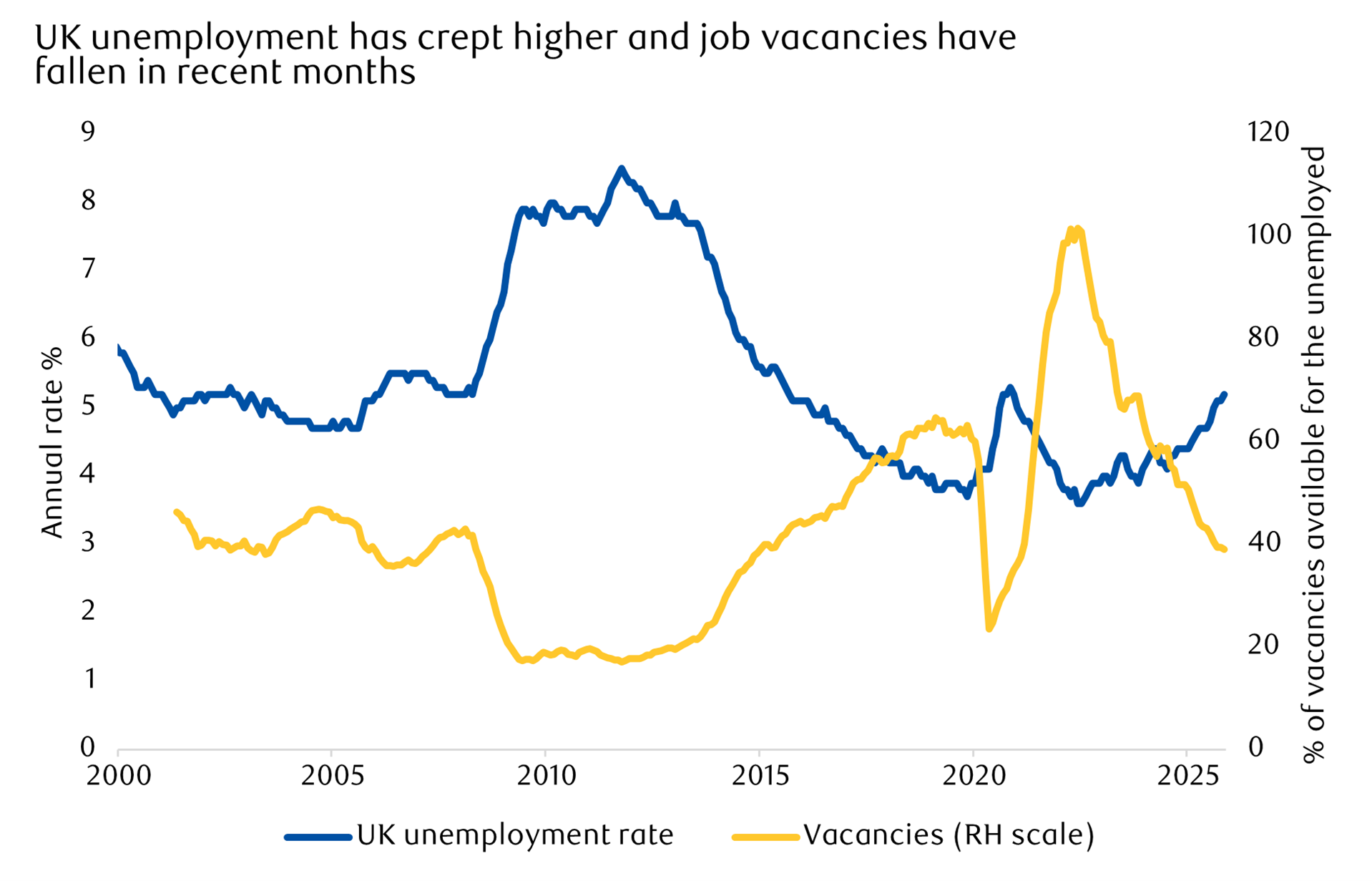

UK economic data shows signs of weakness

The UK had a series of economic reports out last week. They broadly underlined the case for further interest rate cuts because the labour market in particular, appears to be quite weak. An important caveat is that the data quality is low, but the unemployment rate has continued to rise to a level not seen for about a decade outside of economic crises.

Source: LSEG Datastream

However, these levels of unemployment were quite commonplace prior to the global financial crisis of 2008. It’s easy to see this as a watershed moment. While we don’t know to what extent the weakness of employment is caused by the adoption of AI (it’s assumed to be modest for now) and how much is explained by the higher cost of employing UK workers, a longer-term trend seems likely.

The use of AI seems set to alter the constraint on increasing production; historically, this has been heavily tilted toward the shortage of workers, but it could be driven to a greater extent by resource and energy shortages in the future.

For now, the timeliest data comes from PAYE. It suggests employment is stable rather than collapsing – and employment surveys seem to suggest the same. The recent trend of public sector wages outstripping private sector pay abated somewhat.

Consumer price inflation slowed significantly from 3.4% to 3%, a considerable improvement but still well above target. Prices always fall in January, as some categories are discounted heavily. However, the change in the annual rate reflected the resilience of prices seen in January 2025, rather than any specific weakness earlier this year.

A way of looking through these seasonal factors is to consider median price increases. These also remain above the Bank of England’s target.

Friday saw strong retail sales, which we hoped would come, as consumers put the concerns of last year’s budget behind them. With that in mind, a measured approach to cutting interest rates remains warranted.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

25/02/2026