Please see below article received from Brooks Macdonald this morning.

What has happened?

Equity markets fell sharply, led once again by technology. The S&P 500 dropped -1.57% in its third straight decline, while the NASDAQ (-2.03%) and the Magnificent 7 (-2.24%) also saw meaningful losses. Investors continued to focus on the potential scale of AI‑driven disruption, which contributed to a series of pronounced single‑stock moves. Cisco (-12.32%) was among the worst performers following earnings, and several other names across the index posted double‑digit declines—an unusually broad reaction. The selloff extended into financials, with the KBW Bank Index down -3.21%, and even traditionally defensive assets such as gold (-3.19%) and silver (-10.67%) came under pressure. Bitcoin also fell (-2.92%), adding to a generally risk‑off tone.

AI concerns intensify across industries

Fears around the impact of AI continued to ripple through multiple sectors. CH Robinson Worldwide (-14.54%) declined sharply after a small AI logistics company claimed it had helped customers scale freight volumes by several hundred percent without additional staff, triggering a -6.64% drop in the Russell 3000 trucking index. Commercial real estate faced renewed pressure as CBRE (-8.84%) fell for a second day following comments from its CEO that fewer office workers in an AI‑enabled future could reduce long‑term office‑space demand. The weakness broadened beyond tech and AI‑exposed segments. S&P Financials fell -1.99%, while the equal‑weighted S&P 500 dropped -1.31% from a record high. Europe’s STOXX 600 (-0.49%) also edged back from recent peaks.

Europe’s leaders debate economic direction

In Europe, attention centred on the leaders’ summit in Belgium, where policymakers discussed competitiveness, industrial strategy, and the balance between regulation and support. President Macron backed a ‘Buy European’ approach for strategic sectors, while Germany’s Merz and Italy’s Meloni emphasised deregulation to boost growth. Appetite for additional joint borrowing remained limited, with Merz reaffirming that shared debt should be reserved for exceptional circumstances. In the UK, gilts outperformed after Q4 GDP came in softer than expected at +0.1% (vs. +0.2% expected), leaving annual growth at +1.3% for 2025. Markets responded by pricing in a slightly more dovish Bank of England path, with the 2‑year yield falling to 3.60% and the 10‑year yield moving down to 4.45%.

What does Brooks Macdonald think?

Market attention now turns to today’s US CPI release, which arrives at a delicate moment for rate expectations. Investors still anticipate further cuts under the new Fed Chair, but recent stronger‑than‑expected data (including the robust jobs report earlier this week) has introduced fresh uncertainty. A hotter inflation print today would add to those doubts, especially given that the current quarter is already benefitting from the fiscal impulse of the Trump tax cuts. The CPI data could play a bigger role in shaping near‑term market sentiment, as it will help determine whether recent volatility reflects a temporary adjustment or the beginning of a more sustained reassessment of inflation risks and policy trajectories.

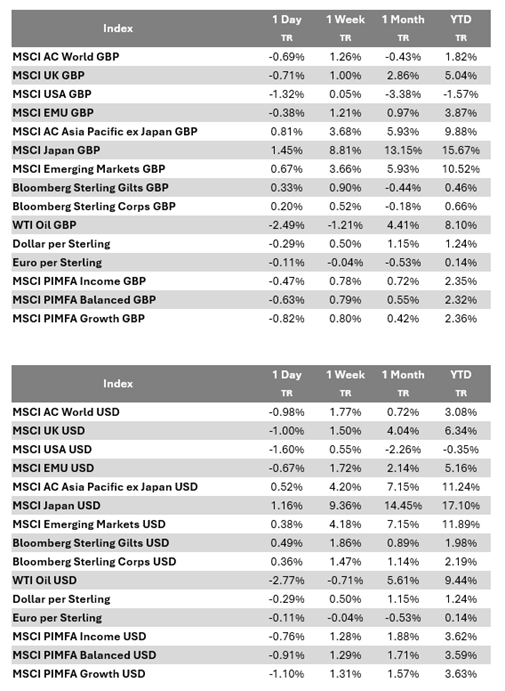

Bloomberg as at 13/02/2026. TR denotes Net Total Return.

Please check in again with us soon for further relevant content and market news.

Chloe

13/02/2026