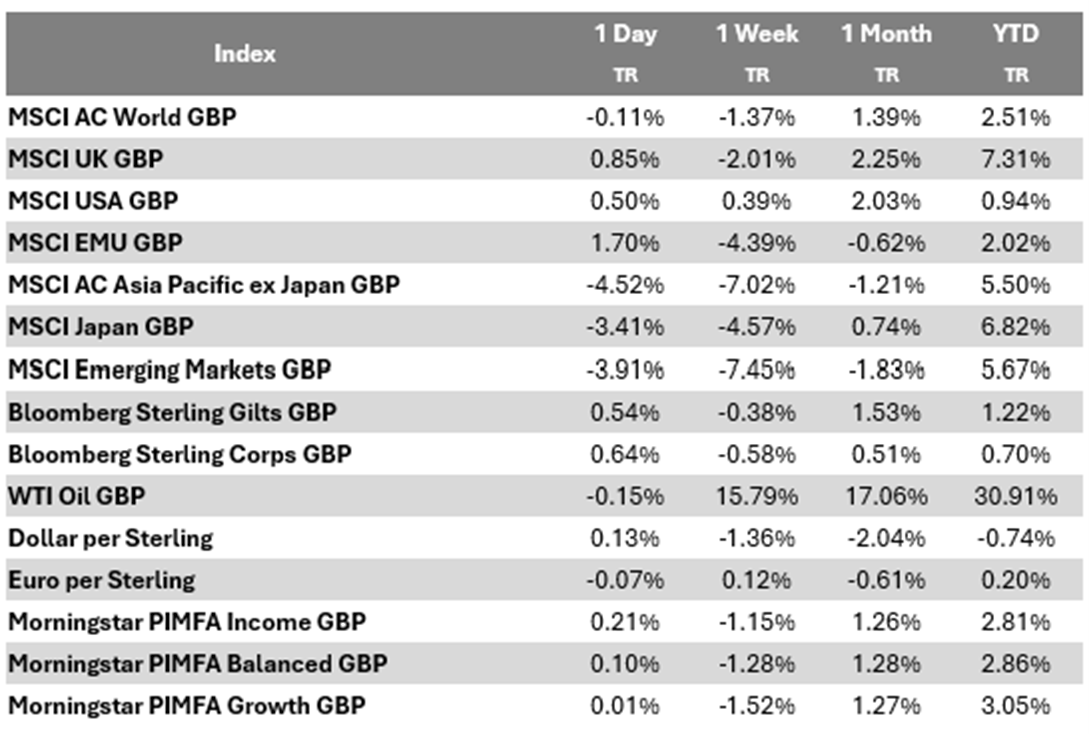

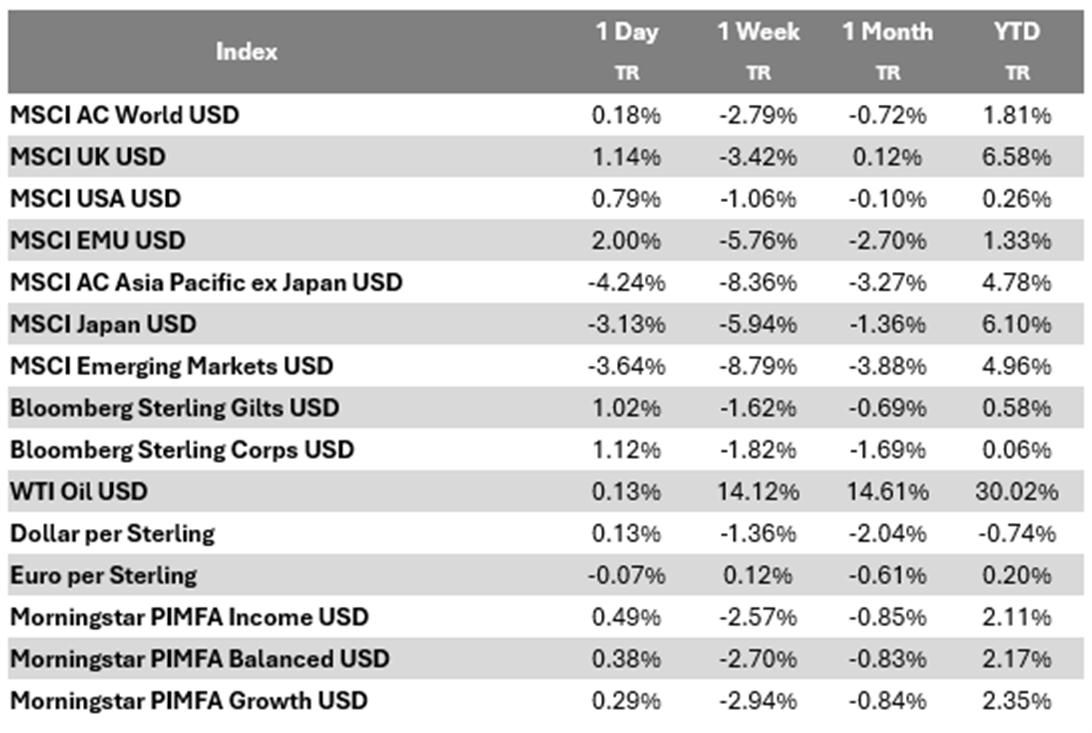

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 10/03/2026.

What next for oil prices?

Energy prices fluctuated at the start of the week on the back of continued geopolitical tension between the U.S. and Iran.

Key highlights

- Iran conflict takes centre stage: Oil prices rose sharply on the back of U.S.-Israeli strikes on Iran, with West Texas Intermediate (WTI) crude oil jumping significantly last week. The oil price has since fallen sharply, after President Trump announced the war in Iran “would be over soon.”

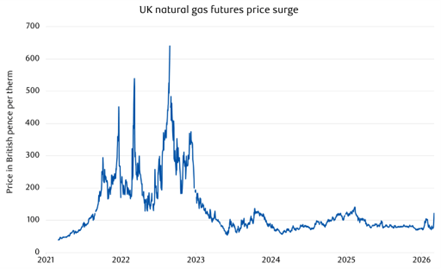

- Bank of England manages interest rate expectations: European natural gas prices doubled in the early part of the week, approaching levels not seen since early 2023. This was sufficient to shift Bank of England rate expectations from two cuts over the coming year to just one.

- Broadcom delivered during earnings season: Broadcom delivered a strong beat driven by its AI semiconductor business, which more than doubled year-on-year. The company now expects to make $100 billion in AI semiconductor revenue for 2027.

Iran conflict takes centre stage

The end of February saw U.S. and Israeli strikes on Iran, which immediately sent oil prices sharply higher. WTI crude oil jumped significantly last week, as markets digested the implications for global energy supply.

Since then, we’ve seen the power over Iran move to Mojtaba Khamenei. As the son of the previous Ayatollah, this signals a continuation of Iran’s previous policy of resistance. Given that he’s lost parents, siblings and children in the attacks, there doesn’t seem to be an obvious path to de-escalation.

This sent oil prices well over the psychologically important $100 per barrel mark, before falling alongside a broad market rally on confidence from President Donald Trump that the war would be completed soon.

Source: Bloomberg, RBC Brewin Dolphin

Notably, the market was somewhat flat-footed. Positioning data suggested limited long exposure to crude oil heading into the weekend, implying traders hadn’t meaningfully positioned for what could be a significant supply shock.

The key concern isn’t Iran’s own production – at roughly 3.2 million barrels per day, it represents just over 3% of global supply. Rather, it’s the potential disruption to the Strait of Hormuz, through which approximately 20% of the world’s oil passes. Iran’s Revolutionary Guards have warned that passage through the Strait of Hormuz isn’t permitted, and traffic has already dried up as insurers either raise premiums or cancel coverage altogether.

However, with Iran facing the world’s dominant military force, surrounded by regional enemies, and with Russia incapable of providing meaningful assistance, the base case among market participants is for a relatively short conflict. This is despite several challenges that make a decisive victory difficult.

There’s speculation that Iran may become rapidly overwhelmed in the current direct conflict, and could resort to an asymmetric phase, in which the goal isn’t to defeat but rather to frustrate their opponents through, amongst other things, maritime disruption of the Strait of Hormuz.

This would be accomplished through Iran’s ‘mosaic’ strategy of using decentralised provincial units that have been pre-authorised to harass shipping through surface-to-sea missiles and drones. A major concern is Iran’s remaining capacity to deploy mines in the Strait, which wouldn’t require its largely disabled naval fleet.

Conversely, Iran’s economic situation was dire heading into this crisis. Official inflation stands at 68% year-on-year, though this almost certainly understates the problem given shortages and the collapse of the Iranian currency. Compare this to wage growth of just 45% over the same period, and the pressure on ordinary Iranians becomes clear. The longer the conflict continues, the more this economic strain may force the regime towards negotiation – especially as closure of the Strait cuts off Iran’s own oil income.

How are energy markets and portfolios impacted by the conflict?

For energy stocks, the picture is nuanced. For example, the two major UK oil producers – BP and Shell – naturally benefit from higher crude oil prices and elevated volatility as their trading operations tend to thrive in dislocated markets. BP’s oil trading earnings rose by roughly $1 billion in a single quarter when conflict last flared in the region two years ago.

BP benefits from having limited direct Middle East upstream exposure (around 8% of volumes, none of which are from Iran) and superior trading optionality. Shell benefits from greater sensitivity to the more significant liquefied natural gas price rises.

Bond markets react to inflation concerns

The conflict’s impact on UK inflation expectations has been swift. European natural gas prices doubled in the early part of the week, approaching levels not seen since early 2023. This was sufficient to shift Bank of England (BoE) rate expectations from two cuts over the coming year to just one.

Gilt yields have risen more sharply than in other markets. This partly reflects positioning after a solid rally in recent months, but also the UK’s particular vulnerability to energy price shocks as a net importer. With current yields approaching 4.5%, gilts offer attractive value relative to global sovereign bonds.

Chancellor Rachel Reeves delivered the Spring Statement earlier in the week. She resisted the temptation to adjust tax policy as the Office for Budget Responsibility forecasts implied that headroom against fiscal rules has improved. However, those forecasts have been overtaken by events in the Middle East.

Dollar strength and currency dynamics

The differences in energy competitiveness between the self-sufficient U.S. and Europe and Asia, which are reliant upon imports, drive divergences in asset class performance across equities, bonds and currencies. The clearest representation of this is in gas prices, which are more sensitive to local supply than oil, which trades globally.

U.S. gas prices were unmoved by conflict in the Middle East, whereas UK and European futures prices soared, undoing a lot of the improvement in relative competitiveness that European futures had enjoyed since July last year.

Source: Bloomberg, RBC Brewin Dolphin

Precious metals: Gold under pressure

Gold continued to be under pressure last week. This was due to the strength of the dollar and generally weaker sentiment amid Middle East tensions from both retail and institutional buyers. After having such a strong run over the last two years, led largely by central bank buying, we’ve now seen the first public hints of a possible sale by this group of investors.

Thursday saw the Polish central bank chief lay out a proposal to generate as much as $30 billion from the sale of the country’s gold reserves to finance defence spending. While it’s legally prohibited for Poland’s central bank to fund the government directly, the mere fact that one of the most aggressive central bank buyers of gold is considering such action given current gold prices is telling, and something that needs to be monitored going forward.

Economic data: U.S. payrolls

The U.S. economy unexpectedly shed 92,000 jobs in February, falling far short of forecasters’ expectations of a 55,000 gain. The unemployment rate rose to 4.4%, up from 4.3% in January. Adding to the weak headline, December and January payrolls were revised down by a combined 69,000 jobs.

The data signals the U.S. labour market remains in a ‘low-hire, low-fire’ mode as employers navigate tariff-related inflation pressures, AI adoption, and geopolitical uncertainty. Thrivent’s David Royal noted that while AI may be contributing to productivity gains – which helps explain why economic output has grown even as hiring has slowed – companies remain uncertain about their future workforce needs.

The healthcare sector lost 28,000 jobs (largely due to a Kaiser Permanente strike during the survey period), while the information sector shed 11,000 jobs, and the federal government cut 10,000 jobs. Social assistance was a rare bright spot, adding 9,000 jobs.

Wage growth also ticked higher, with average hourly earnings rising 0.4% to $37.32 in February and annual growth coming in at 3.8%.

As with the BoE, markets have already scaled back Federal Reserve (Fed) rate cut expectations, from over two cuts to just over one by year end. Friday’s data crystallises the key risk: a sharp employment slowdown coinciding with persistent inflation concerns could back the Fed into a difficult corner and create a substantial headwind for markets.

Corporate earnings: Broadcom delivers

Amid the geopolitical noise, Broadcom delivered a strong beat driven by its AI semiconductor business, which more than doubled year-on-year. The company now expects to make $100 billion in AI semiconductor revenue for 2027 – a remarkable figure that provides considerable comfort around the durability of AI-related capital expenditure.

Importantly, Broadcom has secured its supply chain – wafers, packaging, high-bandwidth memory – at a time of rising costs and industry-wide shortages. Concerns around gross margin dilution from the AI business appear overdone, with management signalling improved yields and scaling cost structures.

The stock now trades on 20 times 2027 earnings and is therefore priced for a significant slowdown in growth, with scope for further upgrades. This provides a constructive read-across for the broader AI supply chain – as do comments from Alphabet’s CFO, Anat Ashkenazi, at Morgan Stanley’s Tech, Media and Telecom conference, which reiterated that demand exceeds supply for cloud services. Meanwhile, AMD’s CEO, Dr. Lisa Su, expressed that the cycle “continues to feel very durable”.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

11/03/2026