Please see the below article from Brooks Macdonald detailing their discussions on US policy and Geopolitical risk. Received this afternoon 05/03/2026.

What has happened?

Yesterday, investor sentiment improved on the back of strong US economic data and the absence of any immediate escalation in the Middle East. Equity markets rebounded across regions. The S&P 500 rose +0.78%, moving back to within 2% of its record high, supported by a strong rally in tech stocks, with the Magnificent 7 up +1.52%. In Europe, the STOXX 600 gained +1.37%, alongside solid advances in the DAX (+1.74%) and FTSE 100 (+0.80%). The recovery extended into Asia this morning, where South Korea’s KOSPI surged +11.02% following the previous day’s sharp sell off. That said, the calm remains fragile. Oil prices have moved higher again overnight, with Brent up 3.18% to $83.99/bbl, reflecting the fast-moving geopolitical backdrop.

Energy market volatility amid geopolitical risk

While broader stress eased, there has been little evidence of de escalation in the Middle East. Comments from Iran’s IRGC suggested an intensification of strikes, alongside confirmation from the US that it had sunk an Iranian warship in the Indian Ocean. Markets have remained highly sensitive to headlines, with oil prices swinging sharply intraday on incremental reports. European natural gas prices fell more than 10% yesterday, reversing part of their sharp gains earlier in the week. This pullback helped ease immediate inflation concerns in Europe and pushed back speculation around an ECB rate hike, with 10 year government bond yields edging lower across core and peripheral markets.

Strong US data challenges the rate cut narrative

Away from geopolitics, US economic data provided reassurance on growth and undercut near term stagflation fears. The ISM services index rose to 56.1 in February, its highest level since 2022, driven by a surge in new orders, while the prices paid component fell to its lowest level in almost a year. The ADP private payrolls report also surprised modestly to the upside, reinforcing the picture of still-resilient labour demand ahead of the official jobs report. As such, markets further reduced the probability of a June Fed rate cut, with investors increasingly sceptical that a new Chair would move quickly in the face of firm activity data. US Treasury yields moved higher across the curve, with the 2 year yield rising to 3.55% and the 10 year yield climbing above 4.10%.

What does Brooks Macdonald think?

Trade policy also remains an important area to watch. Bloomberg reported that the EU has received assurances from the US that the current 10% universal tariff rate will be maintained for now, rather than increased to 15%, following the Supreme Court ruling against the previous IEEPA tariffs. At the same time, attention has turned to the potential for tariff refunds, after a US judge ordered Customs and Border Protection to halt the calculation of IEEPA tariffs on import paperwork. With the administration indicating that interest will be paid on any refunds, the timing and scale of repayments could have implications for the fiscal outlook.

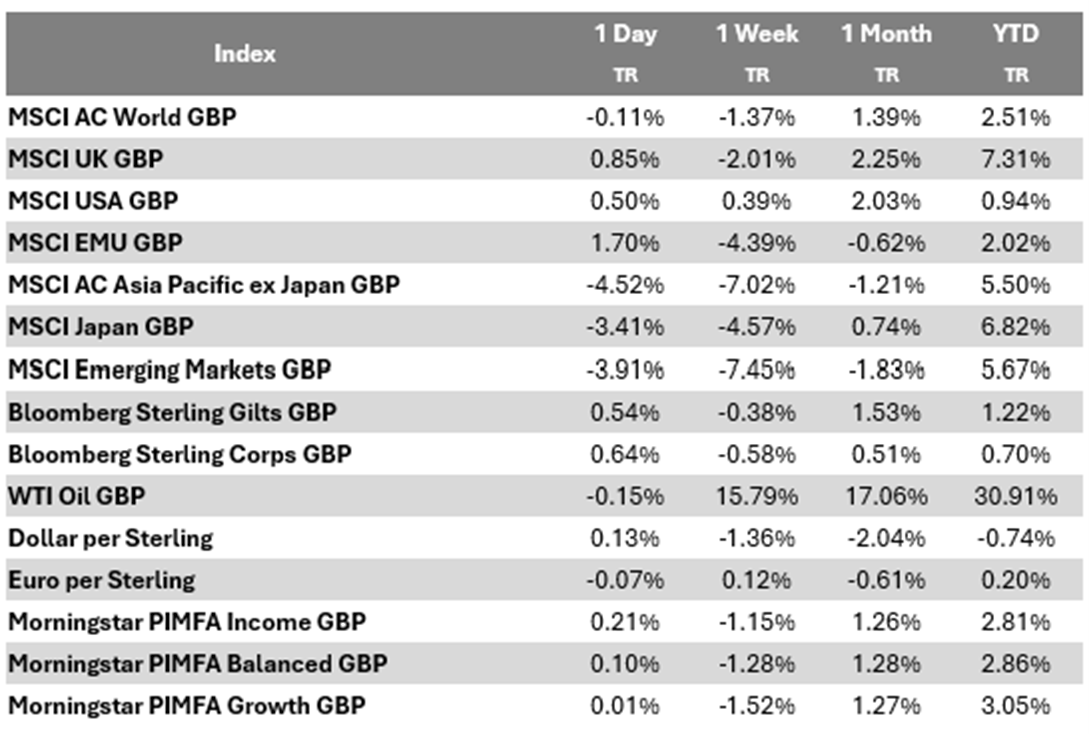

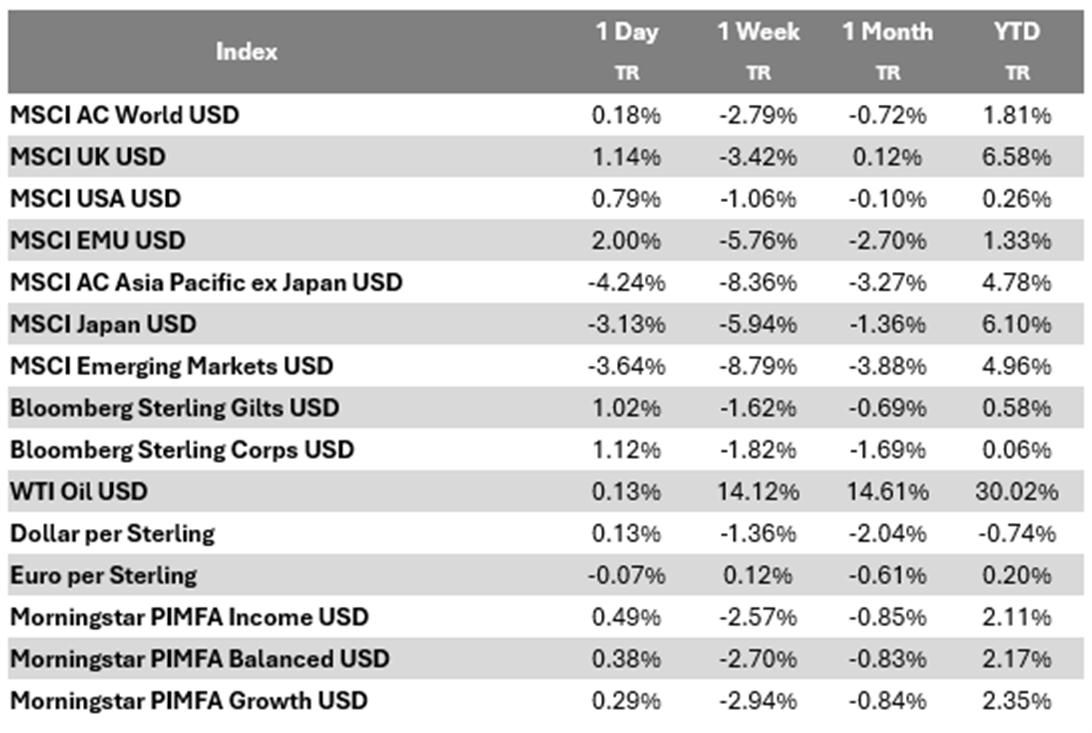

Bloomberg as at 05/03/2026. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

05/03/2026