Please see below article received from Brooks Macdonald yesterday, which provides a global market update as we enter August.

What has happened

If, like me, you had holiday and time away from markets in July, then you probably missed something of a game of two halves in markets in the month that wrapped up yesterday. Early on in July, markets at an index level were doing well, with the US S&P500 equity index hitting a succession of record highs. We also saw government bond prices up (and bond yields down) during the month, on the back of hopes that interest rate cuts would increasingly start to filter through, especially in the case of the US on the back of a softer US inflation print. But about half-way through July, equity market leadership shifted, as tech stocks fell. The so-called ‘Magnificent 7’ group of US megacap tech stocks were down over -10% from peak to trough, entering technical correction territory. Given their weight in US equity indices, that was a big headwind for larger-stock index performance. Instead, we saw a meaningful rotation into the smaller capitalised end of the stock market, as rate cut hopes lifted the outlook for smaller companies who are generally much more sensitive to funding and credit conditions. Indeed, the outperformance in July of the US Russell 2000 small cap equity index over the US Nasdaq technology equity index was the largest in any month since February 2001. Coming back to tech, it was a better day yesterday, with good results from Meta after the US close driving the company’s shares up over +7% in after-market trading. Nvidia shares meanwhile staged an impressive one-day rally up +12.81% yesterday.

US job data points to further cooling, supporting Fed rate cut hopes

A broad gauge of US labour cost growth closely watched by the US Federal Reserve (Fed) cooled in the calendar Q2 by marginally more than analysts had been forecasting. Out yesterday, the US Employment Cost Index (ECI) a broad measure of labour costs, increased by +0.9% in Q2 sequential quarter on quarter (QoQ). This was weaker than the +1.0% expected, after rising +1.2% QoQ in Q1. In year-on-year terms, the ECI was up +4.1% in Q2. Separately, a report from the US-based ADP Research Institute showed US companies added the fewest number of jobs in July since January, while wage growth fell to the slowest pace since 2021 for both so-called ‘job-changers’ and ‘job-stayers’ alike. That was a constructive backdrop for the Fed meeting later in the day, where rates yesterday were kept on hold as expected, but Fed Chair Powell pointed markets in the direction of a first US rate cut in the current cycle to likely come in September. Specifically, Powell said that if the Fed get the data that they hope to get, then a reduction in the policy rate could be on the table at the September meeting.

Investors are proving to be less forgiving

The current calendar Q2 corporate reporting season is seeing a somewhat mixed picture unfold, and in turn it is prompting a somewhat mixed reaction in markets. We highlighted this in our post-Asset Allocation Committee meeting communication out earlier this week. That is to say, according to Factset who have reviewed the latest US S&P500 company reports, while the percentage of companies reporting positive earnings surprises is above average levels, the magnitude of earnings surprises is below average levels. Furthermore, while the aforementioned index is reporting its highest year-over-year earnings growth rate since Q4 2021, the market has been rewarding positive EPS surprises reported by companies less than average and punishing negative EPS surprises reported by companies more than average.

What does Brooks Macdonald think

The market reaction to the latest round of US quarterly earnings results makes sense. Mindful that we are roughly only coming up towards half-way through the results season, nonetheless, these results are landing having followed a period of very strong equity market performance, where the US S&P 500 equity market had notched up fresh record highs as recently as mid-July. As a result, there is a lot less room for manoeuvre left in equity valuations should company results, or their outlooks not beat expectations, in particular focused around megacap US tech stocks. In valuation terms, the MSCI USA equity index 12-month forward Price-to-Earnings Per Share ratio is currently 21.00x versus the past 30-year average of 16.98x. Interestingly, such a valuation gap versus historical averages is virtually non-existent when looking at equity markets on a global ex-US basis. Here, the MSCI All Country World excluding US equity index trades on 13.48x versus the average since 2001 of 13.44x.

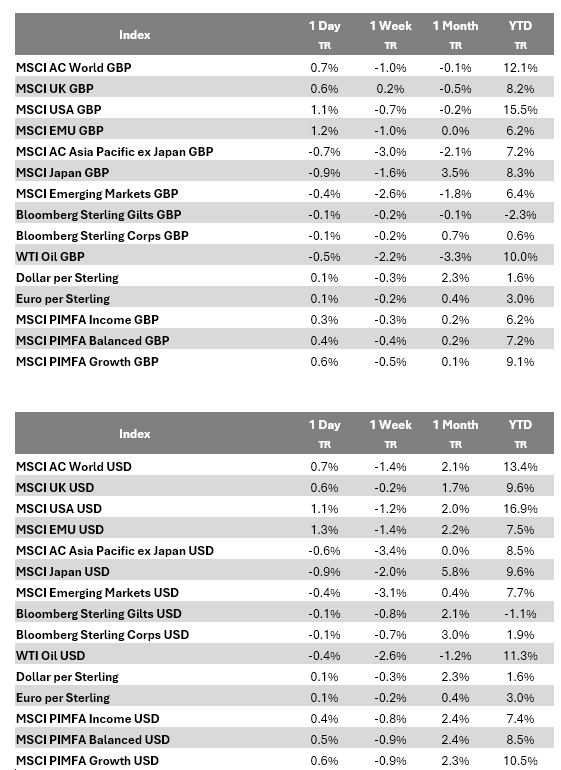

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World GBP | 1.6% | 2.2% | 0.1% | 12.4% | |

| MSCI UK GBP | 1.1% | 2.7% | 2.5% | 10.5% | |

| MSCI USA GBP | 1.6% | 2.5% | -0.3% | 15.4% | |

| MSCI EMU GBP | 0.5% | 0.6% | -0.3% | 5.7% | |

| MSCI AC Asia Pacific ex Japan GBP | 1.2% | 0.9% | -1.4% | 8.0% | |

| MSCI Japan GBP | 4.1% | 2.2% | 4.2% | 11.8% | |

| MSCI Emerging Markets GBP | 1.2% | 0.9% | -1.2% | 7.1% | |

| Bloomberg Sterling Gilts GBP | 0.5% | 1.3% | 1.9% | -1.1% | |

| Bloomberg Sterling Corps GBP | 0.3% | 0.9% | 1.8% | 1.4% | |

| WTI Oil GBP | 4.2% | 1.1% | -5.9% | 8.1% | |

| Dollar per Sterling | 0.2% | -0.4% | 1.7% | 1.0% | |

| Euro per Sterling | 0.1% | -0.3% | 0.6% | 3.1% | |

| MSCI PIMFA Income GBP | 0.9% | 1.6% | 1.3% | 7.0% | |

| MSCI PIMFA Balanced GBP | 1.0% | 1.7% | 1.2% | 8.0% | |

| MSCI PIMFA Growth GBP | 1.1% | 1.9% | 1.0% | 9.9% | |

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World USD | 1.6% | 1.5% | 1.6% | 13.1% | |

| MSCI UK USD | 1.2% | 2.0% | 4.1% | 11.2% | |

| MSCI USA USD | 1.6% | 1.8% | 1.2% | 16.1% | |

| MSCI EMU USD | 0.6% | -0.1% | 1.3% | 6.3% | |

| MSCI AC Asia Pacific ex Japan USD | 1.2% | 0.2% | 0.2% | 8.6% | |

| MSCI Japan USD | 4.2% | 1.5% | 5.8% | 12.4% | |

| MSCI Emerging Markets USD | 1.2% | 0.3% | 0.3% | 7.7% | |

| Bloomberg Sterling Gilts USD | 0.6% | 0.7% | 3.5% | -0.3% | |

| Bloomberg Sterling Corps USD | 0.4% | 0.3% | 3.4% | 2.2% | |

| WTI Oil USD | 4.3% | 0.4% | -4.5% | 8.7% | |

| Dollar per Sterling | 0.2% | -0.4% | 1.7% | 1.0% | |

| Euro per Sterling | 0.1% | -0.3% | 0.6% | 3.1% | |

| MSCI PIMFA Income USD | 0.9% | 0.9% | 2.9% | 7.6% | |

| MSCI PIMFA Balanced USD | 1.0% | 1.0% | 2.7% | 8.6% | |

| MSCI PIMFA Growth USD | 1.2% | 1.2% | 2.6% | 10.6% | |

Bloomberg as at 01/08/2024. TR denotes Net Total Return.

Please check in again with us soon for further relevant content and market news.

Chloe

02/08/2024