Please see below today’s Daily Investment Bulletin from Brooks Macdonald, which was received this morning, 23/07/2024:

What has happened

Equity markets began to regain their footing yesterday with the Magnificent 7 (+2.33%) leading the recovery after a 4-day slump last week. The renewed vigour comes just as the corporate earnings season is set to ramp up, with industry giants Tesla and Alphabet poised to release their financial results after market close in the US today. The anticipation of these announcements has infused the market with a sense of optimism, contributing to significant gains in major indices such as the S&P 500, which rose by 1.08%, and Europe’s STOXX 600, which increased by 0.93%. Both indices experienced their best sessions since the early days of June, recouping a portion of their recent declines.

Politics driving market?

In the political arena, the aftermath Joe Biden’s withdrawal from the presidential race captured the media’s attention, though there remains some scepticism regarding any immediate, substantial changes in the election’s trajectory. Donald Trump continues to be viewed as the leading candidate, with a Republican victory still perceived a likely outcome. While Trump’s momentum has contributed to some of the recent significant shifts in the market, it is the narratives of disinflation and a potential ‘soft landing’ for the economy that appear to be more influential. Investors are keenly awaiting the release of the second-quarter GDP and June’s core PCE inflation data, which are anticipated to reinforce these themes. The bond market has already fully factored in expectations for a rate cut in September.

What does Brooks Macdonald think

There is no single catalyst behind the resurgence in momentum and growth stocks. A commonly cited explanation is that the market rotation into small caps following the CPI announcement last week may have been overly aggressive. Despite some concerns about capital expenditures in AI versus their monetization, and a projected deceleration in earnings growth for major technology firms, expectations remain high. The six largest companies within the index—Amazon, Apple, Alphabet, Meta, Microsoft, and Nvidia—are still projected to achieve an impressive y-o-y earnings per share growth of 30%, while the remaining companies in the index are expected to see a more modest growth of 5%.

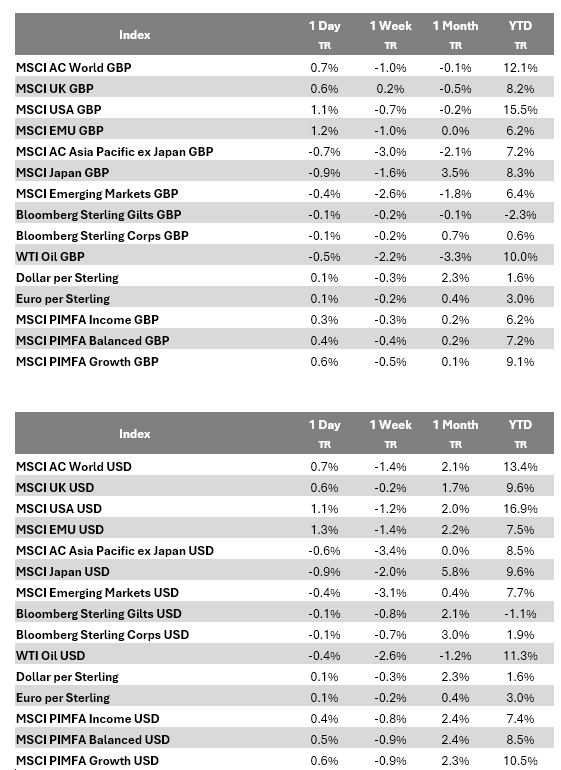

Bloomberg as at 23/07/2024. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Charlotte Clarke

23/07/2024