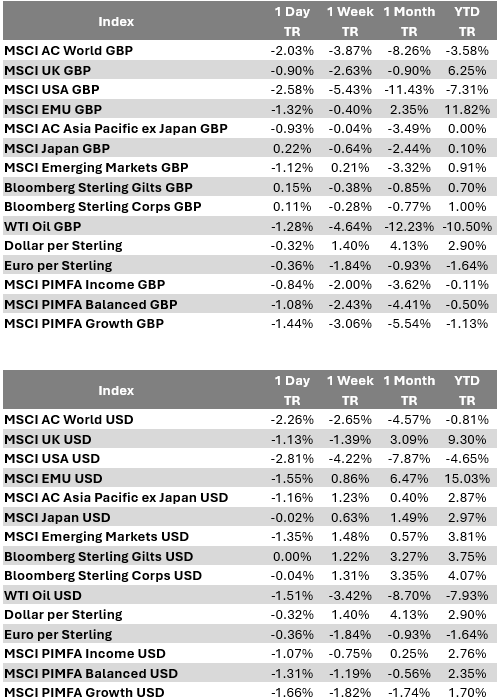

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 18/03/2025.

Why are U.S. equity markets declining?

We examine the impact of the Trump administration’s trade policies on the equity markets and businesses.

Last week saw dramatic escalation and then de-escalation in U.S. President Donald Trump’s global trade war.

After the imposition of 25% tariffs on steel and aluminium imports—measures that will severely hurt Canada’s metal production sector and mean higher metals prices for American manufacturers—Canada’s Ontario premier Doug Ford announced he would impose a 25% surcharge on electricity supplied by Canada to America’s northern states. The response? President Trump declared he would double the tariff on Canadian steel.

Both sides have since withdrawn. The 25% tariffs remain in place.

The European Union announced its retaliatory tariffs, which will come into effect in April should the U.S. import taxes remain in place. President Trump again signalled he would retaliate if the EU implemented these tariffs.

By April, there may be more tariffs on EU exports to the U.S. This will depend on U.S. investigations into the need for reciprocal tariffs to counter any trade restrictions that other countries are deemed to have put in place, including value added tax (VAT).

From ‘Trump bump’ to ‘Trump slump’

Source: LSEG Datastream

There have been two distinct phases to the market action since last year’s U.S. election.

The first was a repeat of the ‘Trump bump’ experienced in his first term. This took place after the election result confirmed there would be a second Trump term. Investors reacted to the prospect of a Trump presidency, anticipating benefits such as reduced regulation and the possibility of tax cuts.

However, even during the last stages of the Trump bump, European equities had begun to pick up steam and following his inauguration, the Trump bump has become a Trump slump! European equities have broadly managed to continue rising despite a sharp sell-off for global equities, which is almost entirely driven by the U.S.

U.S. exceptionalism has been a remarkable trend over a long period. The U.S. began outperforming following the great financial crisis in 2007-2008. Several stars had aligned for this. The U.S. tech sector finally emerged from the shadow of the tech bubble. Meanwhile, Europe suffered from a debilitating debt crisis and saw a slowdown in China and other emerging markets, which had been strong markets for European exports for many years.

As the economy continued to digitise, America’s economy outperformed. It was aided by more favourable demographics, fortuitous natural resource wealth, a dynamic business environment, and capital inflows from other countries, which kept borrowing costs low despite constant budget deficits.

Source: LSEG Datastream

Many of the conditions that have allowed the U.S. to rise to the top of the pack are being challenged by the Trump administration’s unironic pledge to Make America Great Again. Could populism force the world’s biggest economic success story to give up its crown?

The odds still seem strong for America to remain exceptional.

Its geographic benefits are outstanding from a geopolitical and economic perspective because it’s easily defensible and accessible to trade, with incredible natural resource wealth. Europe, on the other hand, is fragmented, with a Russian aggressor on its doorstep.

The largest U.S. companies have remarkable monopoly power and an unrivalled position in the coming artificial intelligence revolution. There’s controversy about how highly their leadership position should be valued, but the fact they’re the leaders is beyond debate.

How are tariffs affecting business sentiment?

Source: LSEG Datastream

There has been a meaningful sell-off in U.S. equities despite there being little evidence of economic weakness from companies and economic statistics. However, surveys hinted that change is afoot.

A couple of weeks ago, anecdotal comments within the purchasing managers indices (PMIs) indicated a more nervous business community.

Last week, this sentiment was reflected by the National Federation of Independent Businesses (NFIB), which had originally cheered the arrival of a new Republican administration. It still considers now a better time to expand its businesses than at most points during Joe Biden’s presidency, but it’s noticeably less ebullient about it now than just weeks ago.

That’s because the threat of tariffs is likely to mean higher costs, with the risk of disrupted supply chains and, for those who export, the possible imposition of retaliatory tariffs. For many companies, there’s no choice but to pass those additional costs on to clients.

In the long term, some companies have pledged to move manufacturing into the U.S. as President Trump wants. But building new plants for manufactured goods typically takes years, so there’s no quick fix to this threat if the tariff is going to remain until companies have genuinely shifted their production.

The potential impact of tariffs is difficult to quantify, especially as the specific targets, levels and duration of the measures remain uncertain, but we shouldn’t be too concerned by dramatic shifts in survey data. There have been instances of surveys suggesting very pessimistic economic outcomes only to rebound when respondents have a better idea of what the new business environment is going to be like. Brexit would be a good example of this.

The immediate impact of these tariffs will be far more material than the years of inaction over Brexit, but that doesn’t prevent people from overreacting in surveys.

Peak bearishness – prime buying opportunities?

Source: LSEG Datastream

The American Association of Individual Investors (AAII) business sentiment survey has been a terrific barometer of stock market overreaction in the past. It has now risen to levels that have been associated with some of the most timely ‘bottoms’ in the stock market over recent decades.

Peaks in bearishness, as per this measure, that were recorded in March 2003, March 2009 and September 2022, were all tremendous buying opportunities for the coming years. In each of those instances, the market was considerably more depressed than it is at the moment, so we probably can’t expect the dramatic gains they offered. But it does indicate that the tariff message has hit investors hard, which sets up the potential for a rebound.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

19/03/2025