Please see below, an article from Brooks Macdonald providing a brief analysis of the key factors currently affecting global investment markets. Received today – 04/03/2025

What has happened

In a measure of how investors are responding to the unprecedented geopolitical developments around Ukraine, yesterday saw another big gain for European defence stocks in particular. The pan-European STOXX Aerospace & Defence Index jumped +7.7% yesterday, recording its strongest daily gain in over four years, since November 2020. Among the companies leading those gains, UK-listed BAE Systems closed up +14.6% yesterday, and is now up +40.3% this year alone, all in local currency price return terms.

US pauses military aid to Ukraine

The White House yesterday confirmed that US president Trump has ordered a pause on all fresh military aid to Ukraine not yet drawn down by the outgoing Biden administration. The order applies to all US military equipment not currently in Ukraine, including weapons in transit on aircraft and ships or waiting in transit areas in Poland. While the extent of the affected weapons is not public knowledge currently, Trump had inherited an authority from Biden’s administration to deliver some US$3.85 billion’s worth of weapons from US stockpiles.

Trump tariffs arrive, and trade retaliation comes quickly

There was no last-minute reprieve for US president Trump’s tariffs on Canada, Mexico and China which have come into force in the last few hours. There are now 25% trade tariffs on Canada and Mexico, as well as a second 10% hike in tariffs on China trade on top of past China tariff measures – according to Bloomberg, this collectively impacts around US$1.5 trillion worth of annual US imports. Canada has retaliated with a first wave of 25% tariffs on some US exports while China has added tariffs of up to 15% on US exports.

What does Brooks Macdonald think

Yesterday’s latest US economic data did nothing to ease stagflation fears that have been stalking markets lately. The US Institute for Supply Management (ISM) manufacturing survey headline was weaker than expected (at 50.3), and only just expansionary month-on-month, versus the 50-halfway mark that separates economic expansion and contraction. Within the data, new orders (at 48.6) and employment (at 47.6) were both weaker than expected and in contraction territory, while Prices Paid jumped 7.5 points (to 62.4), and now at the highest level in almost 3 years, since June 2022.

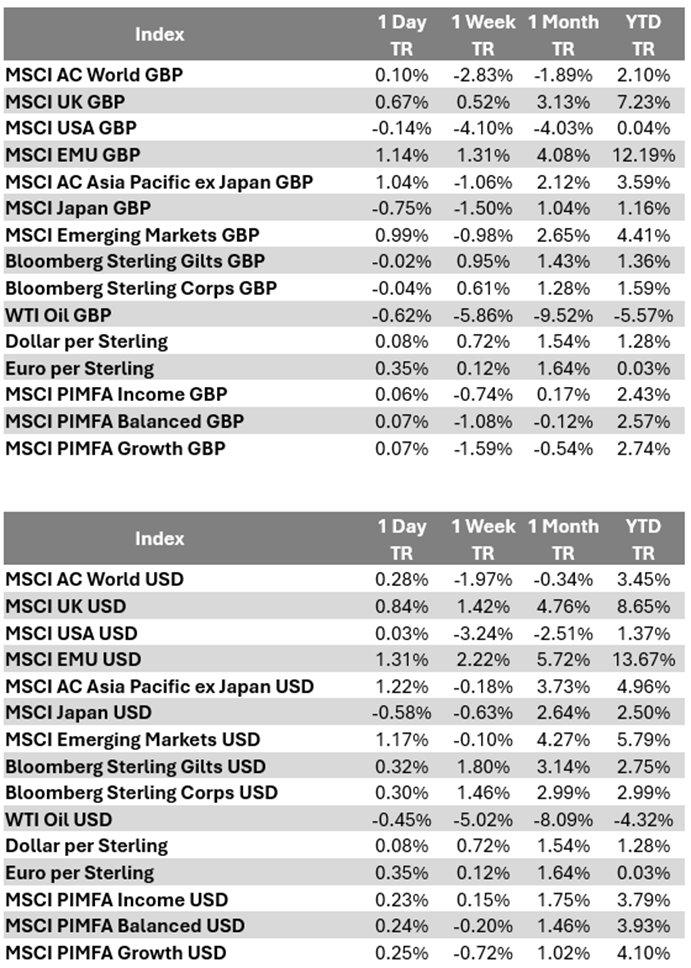

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World GBP | -1.81% | -2.26% | -2.83% | 0.31% | |

| MSCI UK GBP | 0.71% | 2.63% | 3.94% | 9.12% | |

| MSCI USA GBP | -2.75% | -2.86% | -5.10% | -1.98% | |

| MSCI EMU GBP | 1.29% | 1.24% | 5.60% | 12.28% | |

| MSCI AC Asia Pacific ex Japan GBP | -0.95% | -3.89% | -0.18% | 0.04% | |

| MSCI Japan GBP | 1.13% | -1.67% | 0.76% | 0.75% | |

| MSCI Emerging Markets GBP | -0.98% | -3.91% | -0.26% | 0.71% | |

| Bloomberg Sterling Gilts GBP | -0.56% | 0.16% | -0.12% | 1.08% | |

| Bloomberg Sterling Corps GBP | -0.37% | -0.07% | -0.13% | 1.29% | |

| WTI Oil GBP | -2.96% | -3.87% | -8.91% | -6.15% | |

| Dollar per Sterling | 0.99% | 0.60% | 2.02% | 1.48% | |

| Euro per Sterling | -0.12% | 0.40% | 0.62% | 0.21% | |

| MSCI PIMFA Income GBP | -0.68% | -0.48% | -0.52% | 1.93% | |

| MSCI PIMFA Balanced GBP | -0.79% | -0.68% | -0.71% | 1.97% | |

| MSCI PIMFA Growth GBP | -0.96% | -0.99% | -1.01% | 1.98% | |

| Index | 1 Day | 1 Week | 1 Month | YTD | |

| TR | TR | TR | TR | ||

| MSCI AC World USD | -0.82% | -1.67% | -0.31% | 1.89% | |

| MSCI UK USD | 1.72% | 3.24% | 6.64% | 10.84% | |

| MSCI USA USD | -1.78% | -2.27% | -2.63% | -0.44% | |

| MSCI EMU USD | 2.30% | 1.85% | 8.34% | 14.05% | |

| MSCI AC Asia Pacific ex Japan USD | 0.04% | -3.31% | 2.41% | 1.62% | |

| MSCI Japan USD | 2.14% | -1.08% | 3.37% | 2.33% | |

| MSCI Emerging Markets USD | 0.01% | -3.33% | 2.33% | 2.29% | |

| Bloomberg Sterling Gilts USD | 0.30% | 0.81% | 2.22% | 2.50% | |

| Bloomberg Sterling Corps USD | 0.50% | 0.57% | 2.21% | 2.72% | |

| WTI Oil USD | -1.99% | -3.30% | -6.55% | -4.67% | |

| Dollar per Sterling | 0.99% | 0.60% | 2.02% | 1.48% | |

| Euro per Sterling | -0.12% | 0.40% | 0.62% | 0.21% | |

| MSCI PIMFA Income USD | 0.31% | 0.11% | 2.06% | 3.53% | |

| MSCI PIMFA Balanced USD | 0.21% | -0.08% | 1.87% | 3.58% | |

| MSCI PIMFA Growth USD | 0.03% | -0.40% | 1.56% | 3.59% | |

Bloomberg as at 04/03/2025. TR denotes Net Total Return.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

4th March 2025