Please see the below article from Brewin Dolphin analysing the key measures announced in the UK Spring Statement and how they could impact personal finances, investments, and the wider economy. Received – 26/03/2025

UK Chancellor Rachel Reeves has unveiled the 2025 UK Spring Statement, aiming to balance public finances and “secure Britain’s future in a world changing before our eyes”.

The Spring Statement follows a significant Autumn Budget, in which tax rises totalling £40 billion were announced. Despite a shifting geopolitical scene since that announcement, the Chancellor is resolute in reserving major fiscal decisions to once annually in the autumn, leading to a restrained Spring Statement that zeroed in on expenditure reductions and a boost in defence spending.

Our analysis examines the Spring Statement’s relatively limited measures affecting personal wealth and investments, with Guy Foster, chief strategist, evaluating the UK’s economic prospects in light of the Office for Budget Responsibility (OBR)’s projections.

Financial planning highlights

Tax

The Chancellor’s Spring Statement eschewed further tax rises, maintaining the status quo on income, capital gains, inheritance tax (IHT), VAT, and National Insurance.

Instead, there was a heavy focus on enhancing HMRC’s debt management, targeting promoters of tax avoidance, and intensifying efforts to clamp down on tax evasion. This includes action to prosecute more tax fraudsters, reform the rewards for informants, increase penalties, and tackle advisers facilitating non-compliance.

Looking ahead, the UK’s substantial debt burden and limited fiscal leeway mean that expectations for a more lenient personal tax regime in the upcoming budget are muted. Meanwhile, the current stability in tax legislation provides a window for individuals to review their financial planning strategies in anticipation of possible changes in autumn. Engaging with your wealth planner and professional advisers can help you understand what options are available to you.

Business Relief

Business owners face an increased IHT liability starting April 2026 due to a previously announced £1 million cap on relief. However, a recent HMRC consultation suggested there could be the potential to benefit from the £1 million allowance multiple times.

Any gifts of Business Relief assets between 30 October 2024 and 5 April 2026 will count towards the £1 million allowance, with the reset period for Agricultural and Business Relief set at every seven years from the date of each gift of the assets. It’s important to note that Business Relief investment allowances cannot be shared between spouses, which differs from some other IHT allowances.

With careful planning considering existing IHT strategies, business owners could benefit several times by making multiple gifts on a rolling seven-year basis. Note that it’s vital to consider the suitability of the alternative investment market or other schemes for IHT planning, considering how Business Relief assets are divided between spouses and their eventual distribution upon death. Keeping detailed records of all Business Relief assets transferred since 30 October 2024 is imperative. Currently, this area remains without draft legislation and consultation continues.

The outlook for the UK economy

In the autumn, the government announced significant tax hikes and increased borrowing to fund major investments in public services. The Spring Statement would ideally be an update on how those policies were affecting the economy.

Firstly, it’s important to remember that the government must abide by rules which limit how much it can borrow in the future. These rules are designed to prevent governments from being tempted to take risks now, which could have significant costs later. The OBR’s role is to estimate whether the government abides by these rules.

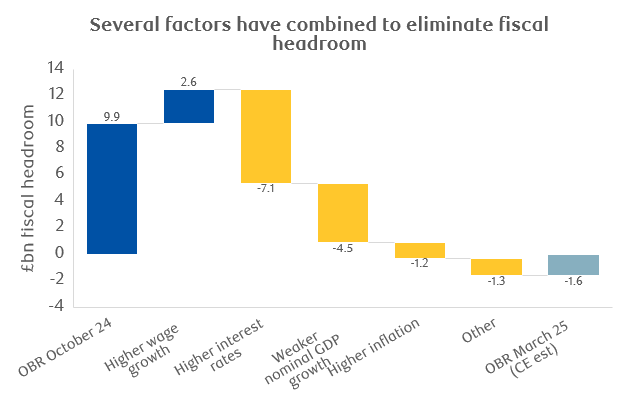

For the Chancellor, the most challenging thing is to ensure that the current budget (that means day-to-day spending but does not restrict investment) is on course to be in balance by the 2029/30 financial year. At the last budget, the OBR estimated that the government would meet this restriction by £9.9bn — although such forecasts are inherently uncertain.

Ideally, chancellors would like more margin for error, or scope to spend. As it turns out, the forecast has deteriorated due to a combination of weaker economic growth and higher interest rates, leaving the government on course to break its fiscal rules.

This has led to a series of pre-Spring Statement announcements, including welfare reductions and public sector efficiency measures. However, the government intends to increase borrowing, but to use more of that money to invest, particularly in defence.

Whilst few would doubt the necessity of investing in defence, it doesn’t help the Chancellor meet her fiscal rules. For each pound invested in defence, the additional economic activity is relatively modest. By contrast, housebuilding generates a lot of additional economic activity, which is why promising to reduce planning hurdles can improve growth overall, despite carrying no fiscal cost.

The net result is that despite the deterioration in revenue growth assumptions, the OBR judgement once again predicts that the Chancellor will meet her current spending rule at £9.9bn. If that number seems familiar it’s because it restores exactly the same headroom the Chancellor had last autumn.

Clearly £9.9bn is better than nothing, but the last few months have shown just how easy it is for economic performance to change and for perceived headroom to disappear. So far, most of the current parliament has seen a constant debate over whether tax increases and spending cuts might be required, and retaining this modest headroom invites that to continue. The real risk is that this uncertainty leads to companies feeling too unsure to invest. This is particularly relevant given the existing economic uncertainty that stems from the new U.S. government and its plans to introduce an uncertain range of tariffs.

At a time when the economic outlook is even more uncertain than normal, the Chancellor would ideally have more margin for error.

The other nuance about the fiscal rules is that they allow for the government to meet its targets by forecasting austere measures in the coming years. We share some scepticism about the extent to which spending growth will slow in some departments as the current parliamentary term concludes.

The fiscal rules are just one constraint that the government is under. The other, arguably more meaningful constraint, is the bond market reaction.

If governments are expected to borrow more money or if their actions are expected to boost inflation, then the cost of issuing new government debt will rise. With relatively few announcements made in the Spring Statement, and with recent days having seen reductions in welfare costs, the bond market has been relatively stable. This has been helped by the news indicating that UK inflation slowed slightly during February.

Overall, the Chancellor has reiterated the government’s commitment to its manifesto pledge against raising core personal taxes, taking a more cautious approach after earlier bond market jitters.

Much will now depend on how the economy fares between now and autumn’s budget.

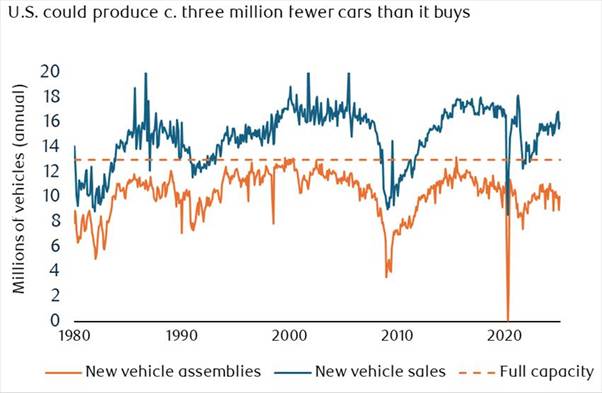

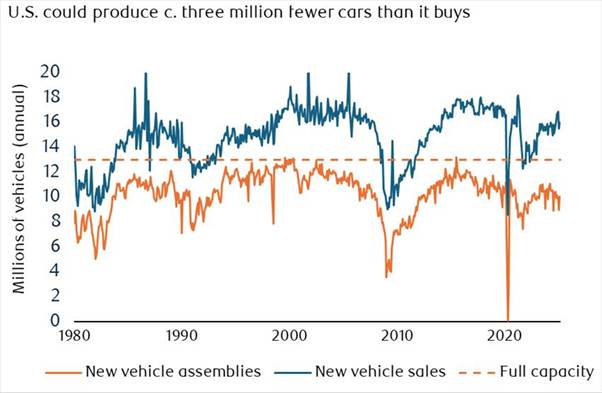

Last night, Trump announced a 25% tariff on all car imports, which could escalate the ongoing tariff war. This could have a global impact on markets and undermine Rachel Reeves Spring Statement yesterday.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Marcus Blenkinsop

27th March 2025