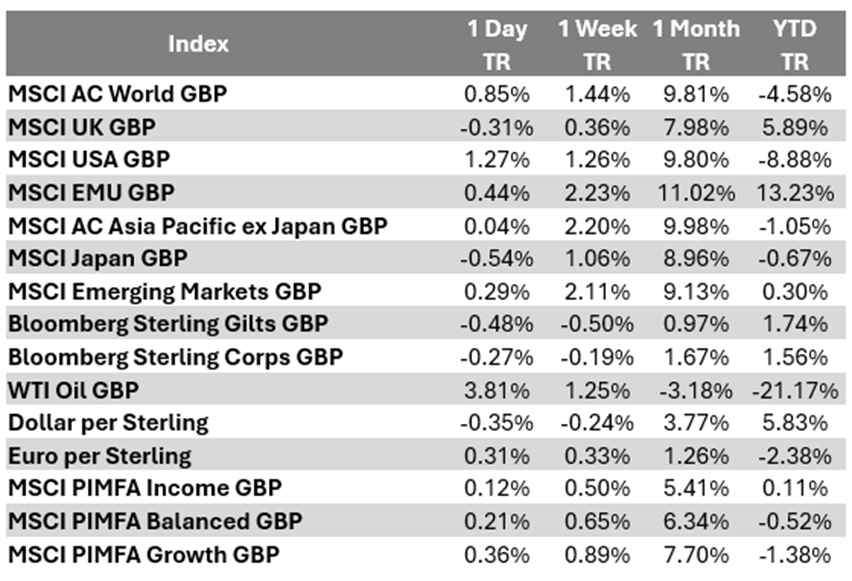

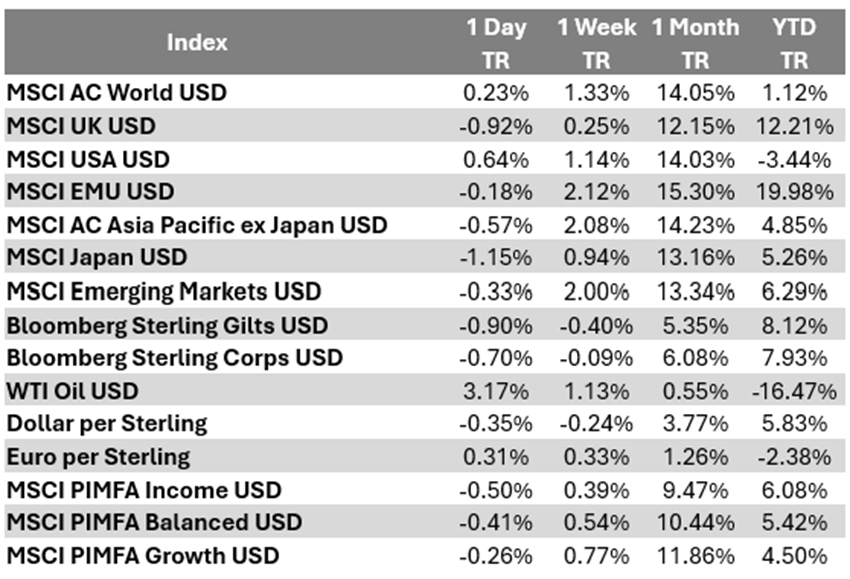

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 13/05/2025.

Markets rally on positive trade new

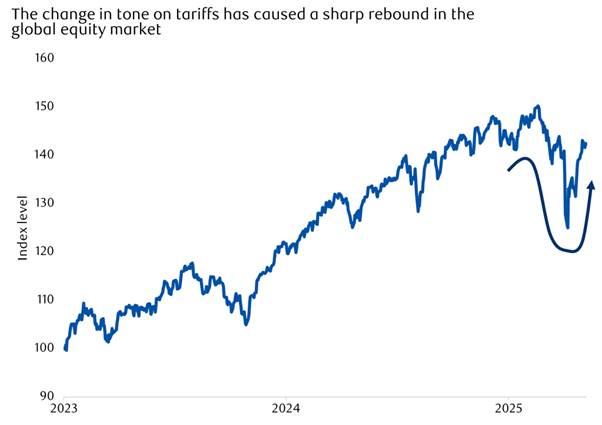

We examine how easing trade frictions have helped boost equity markets.

Source: LSEG DataStream

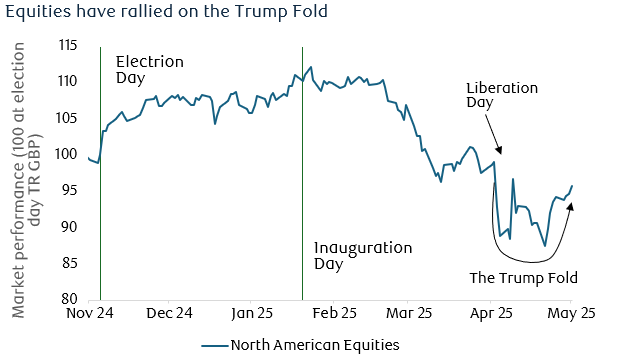

If the onset of tariffs was a major headwind for the markets, then the easing of them should be seen as a tailwind. Globalisation allows countries to specialise in activities in which they have a comparative advantage; doing so increases global economic growth, allowing each country a larger individual share of that growth.

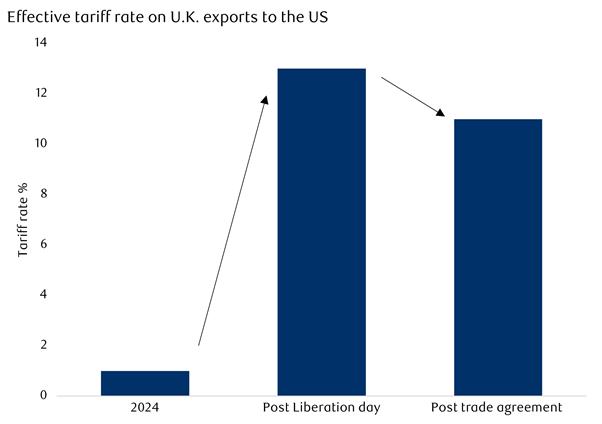

With that in mind, the news last week was dominated by the lifting of trade restrictions. After ‘Liberation Day’, it’s become increasingly clear that the Trump administration is seeking deals that lower tariffs, but questions remained over which countries it dealt with first, when this was done and how much tariffs would be lowered by.

We got a partial answer last week when U.S. President Donald Trump announced a “full and comprehensive” trade agreement with the UK. For context, this isn’t a traditional free trade agreement, which would take the form of an international treaty and would usually need to be implemented by legislation. Instead, this is President Trump agreeing to amend the trade tariffs that he placed on UK exports by executive order under emergency powers.

As far as we can tell, the agreement is verbal at this stage, and details will be agreed over the coming weeks.

America had placed 25% tariffs on steel, aluminium, cars and car parts from all countries, but the UK has achieved a partial exemption from that, with steel and aluminium being potentially zero tariffed. The UK has also been promised preferential treatment when President Trump applies tariffs to the pharmaceutical sector. In both these instances, details remain unclear.

Most UK car exports to the U.S. will be tariffed at 10% and there were some agreements on aeronautical deals (the U.S. buying engines from the UK and the UK buying planes from the U.S.). The cost of these easements is that the UK has had to drop some agricultural tariffs – it will probably adjust its digital services tax, too.

The overall impact of these measures is likely to be very small, though. This is partly because the most significant measure, the 10% universal tariff rate on all (now most) exports to the U.S., will remain in place, so the average tariff rate has only come down a little bit. Moreover, the UK runs fairly balanced trade with the U.S. anyway, and so the initial measures didn’t really affect us that much. Achieving big gains from trade is now much harder than it used to be, since the most significant barriers have already been dismantled.

Declining tariffs are generally good news, but the UK deal suggests that trade with the U.S. is likely to be subject to a minimum tariff level of 10% on most goods. As discussed a couple of weeks ago, the U.S. seems very ready to reduce tariffs with China. President Trump reiterated last week that he won’t do so pre-emptively, but it’s clear that the current rate of 145% tariffs won’t remain in place.

The UK also agreed a more conventional trade deal with India after three years of negotiation. The government says this deal will boost the UK’s gross domestic product (GDP) by £4.8bn by 2040. To put this into context, that’s only 0.19% of the UK’s current GDP. So, however things play out, this isn’t likely to be something that really moves the needle for the economy.

Overall, tariffs remain a force that’s likely to depress growth and increase inflation – but they’re set to decline from their current levels.

Source: LSEG DataStream

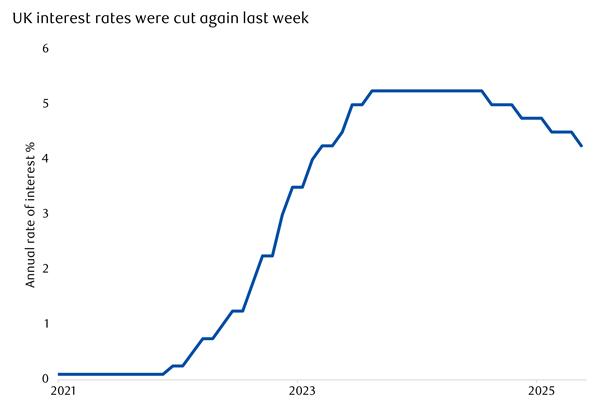

The Bank of England’s Monetary Policy Committee (MPC) probably had relatively little notice of the trade deal, and its effect was marginal anyway. Instead, the MPC has been focusing on an economy which has experienced relatively little growth momentum and a cooling inflation picture.

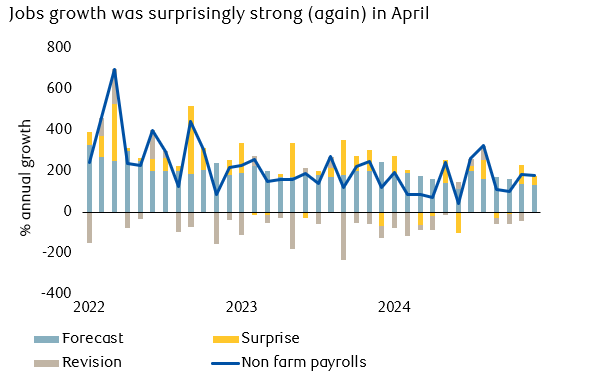

As an important caveat, there will be an increase in inflation over the coming months due to gas and electricity bills, but beyond that, disinflationary pressures seem set to bring the inflation rate back down towards target. Jobs growth has been softening and job postings have been declining. The cost of employees has risen due to the increase to Employers National Insurance contributions, and companies now have the options of absorbing the costs in their profit margins, passing them on in higher prices (inflation), or reducing their staff numbers.

This creates a lot of uncertainty, which was reflected in a three-way split when the MPC voted on whether to cut interest rates last week; two members wanted to cut interest rates faster and two wanted to stay on hold.

In the end, the majority decision was a 0.25% cut, but that uncertainty meant that markets reduced their expectations for future cuts for the time being. Interest rates are currently expected to fall from 4.25% to 3.5% or 3.75% by the end of the year.

Source: LSEG Datastream

As we’ve seen so often before, the markets are climbing the wall of worry that was built by President Trump’s erratic behaviour during the first few months of his second term.

Interest rates have been falling in the Eurozone, have started to fall in the UK, and will likely fall in the U.S. too (eventually).

Last week, the U.S. Federal Reserve left interest rates unchanged (as expected) as the outlook for inflation is difficult to gauge due to the erratic trade policy environment. However, with equity sentiment quite depressed, the conditions for markets to continue climbing that wall of worry seem quite supportive in the short term.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

14/05/2025