Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 07/05/2025.

Oil price hits lows as OPEC accelerates production

We examine potential reasons for OPEC producing 400,000 extra barrels of oil a month – and how this could help President Trump.

Saudi Arabia shifts OPEC strategy

Shortly after the ‘Liberation Day’ furore, OPEC (the Organisation of the Petroleum Exporting Countries) announced an increase in oil production. In many ways, it was the opposite reaction to what would normally be expected. OPEC increases energy production when energy is undersupplied or reduces it when demand for oil is weak (this usually happens when the economy is weak). It does this to prevent the oil price from falling too low.

OPEC is a cartel. It manages the oil price to ensure that oil producing countries make healthy profit margins. Unusually low demand or members producing too much oil are two reasons oil prices could be weak.

Since the ‘Liberation Day’ tariffs were announced, growth expectations have generally declined. Normally, you might expect that OPEC would reduce production in anticipation of weaker oil demand. Instead, it announced increased production immediately after the tariffs were announced; this week, it announced further increases. Why?

OPEC has been struggling to control the energy market because of new supply introduced from non-OPEC members. The U.S. is a big one since it developed shale oil. While OPEC restricts its own production to maintain high margins, it’s also ceding market share to higher-cost shale oil producers at the same time.

Despite OPEC’s efforts, the oil price has fallen, largely due to weak demand from China. OPEC may have decided that if it can’t maintain the margin it needs, then its next best option is to leverage its position as lowest cost producer, pump more oil, allow the price to fall and discourage further supply from non-OPEC members.

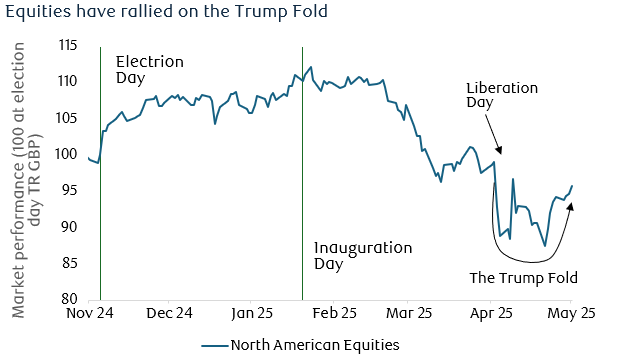

Market rally on the Trump Fold

Source: LSEG/DataStream

The early part of U.S. President Donald Trump’s second term has been challenging for stocks. Most notably U.S. stocks, which took their biggest hit when he shifted his rhetoric from “Make America Great Again” to “Make America Wealthy Again”. This coincided with his announcement on ‘Liberation Day’ tariffs, prompting a remarkable sell-off in global, particularly U.S., stocks.

Within a week, those tariff measures were partially walked back. Notably, the 90-day delay in the implementation of the individual tariff rates, affecting 60 countries, prompted a sharp rally in stocks. However, the president was keen to impress that the tough stance on trade was still in place by doubling tariffs on China. The situation has been chaotic ever since. Businesses have been in turmoil as they grapple with the measures and Apple announced last week that the measures would impose $900 million in additional costs this quarter. It presumably could have been worse, as the impact of tariffs was again diluted in response to a revolt from investors and business leaders. Consumer electronics were exempted, and although President Trump attributed this to the forthcoming additional measures on semiconductors, so far, those measures haven’t materialised. All of this has allowed a period of ‘announcement-calm’, during which the stock market has recovered most of the ground lost since ‘Liberation Day’.

By the end of Thursday last week, the S&P 500 had risen for eight consecutive days, a record run of strength. That still leaves U.S. stocks well below Inauguration Day levels, and the extent of the U.S. recovery is flattered when presented in local currency terms (i.e. U.S. dollars), due to the weaker dollar. Perhaps the leadership of the U.S. recovery has been a more significant factor.

Over this very short period, investors have used this weakness as an opportunity to get back into the exceptional U.S. companies that will benefit from the artificial intelligence (AI) revolution, a trend that will certainly outlast President Trump’s second term. Whether ‘Trumpism’ endures beyond the next few years remains less certain.

When will the economy weaken?

Source: LSEG/DataStream

Last week’s U.S. Q1 GDP estimate was weak, suggesting that the U.S. economy contracted by -0.1% in Q1 (-0.3% on an annualised basis). Although this might suggest that the tariff policy has been a failure, in truth, the headline weakness is quite misleading.

Anticipation of tariffs prompted businesses and consumers to stock up ahead of possible measures. Imports detract from GDP while exports add to it, so this front-running weighed heavily on GDP in Q1. Final demand, by contrast, was very strong, also reflecting front-running of tariffs.

Trade will certainly be more of a tailwind in the second quarter; however, the uncertainty and higher costs are likely to be an overwhelming headwind to both consumption and investment.

The economy is currently showing potential, despite business and consumer surveys suggesting otherwise. Consumer confidence, according to the U.S. Conference Board, has collapsed to a level last seen in the depths of the initial COVID-19 wave. Respondents expressed more negative views on the labour market, expected higher inflation, and perceived the highest risk of recession in two years.

Businesses responding to the Institute of Supply Management (ISM) Manufacturing survey were also downbeat. Decline in new orders slowed, suggesting that business activity continues. The anecdotal comments released alongside surveys have been telling. All ten issued by the ISM mentioned tariffs in a negative light, citing difficulty in finding non-Chinese sources for tariffed imports, and an inability to tender for business because of the uncertainty over costs.

All eyes are on the labour market now. A fall in job openings reported Tuesday and a rise in jobless claims reported on Thursday, alongside the survey evidence listed above suggest the jobs market should be weakening. However, the official jobs report was a little stronger than expected. There were some negative revisions to previous reports, but forecasts now expect jobs growth to slow down to around 50,000 per month over the rest of the year.

The art of negotiations

Last week highlighted the different negotiating styles of the Chinese and U.S. administrations. We’ve previously described how Trump’s negotiating style aligns with aspects of his book ‘The Art of the Deal’ (despite allegations that he wasn’t particularly involved in its writing).

The key philosophy of ‘thinking big’ has been evident in terms of the measures used and, presumably, the concessions sought, although little substance has come from the negotiations so far. He has been aggressive, and outspoken, which are key tenets of ‘The Art of the Deal’ approach. One missing element has been a resolution. The book suggests that negotiations should be reconciled quickly, something that is unlikely to be possible in trade negotiations.

Perhaps most controversially, President Trump has actually made concessions. In general, his book suggests that concessions are unwise and can be perceived as a sign of weakness. However, he does suggest that a very aggressive negotiating stance can be moderated to make the opponent feel they have achieved something. It’s certainly conceivable that for many countries, reducing a 20% tariff to 10% could be perceived as a victory, despite being in a much worse position that they were just a few months ago.

China is now seeking to reduce a 145% tariff, which offers enormous scope for negotiation. According to Trump’s book, concessions should be given in return for negotiating wins, which has categorically not happened yet, it seems clear that the strategy has been at least partially flawed.

By contrast, China’s approach seems more consistent with Sun Tzu’s ‘The Art of War’. Ironically, despite being a military treatise, the text recommends avoiding conflict where possible. It takes a more strategic and measured approach, which seeks to win without fighting.

Last week, China sought to project a strong position, claiming not to be in talks with the U.S., while representatives of the White House were keen to concede that a deal and tariff reductions are possible; they’ve even suggested that current tariff rates are unsustainable. It seems to have been a public relations victory for China so far, but that doesn’t diminish its powerful need to persuade the U.S. to reduce taxes on trade with the richest economy in the world.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Charlotte Clarke

08/05/2025