Please see the below article from Brooks Macdonald detailing their discussions on key economic events that occurred yesterday. Received this morning 09/05/2025.

What has happened

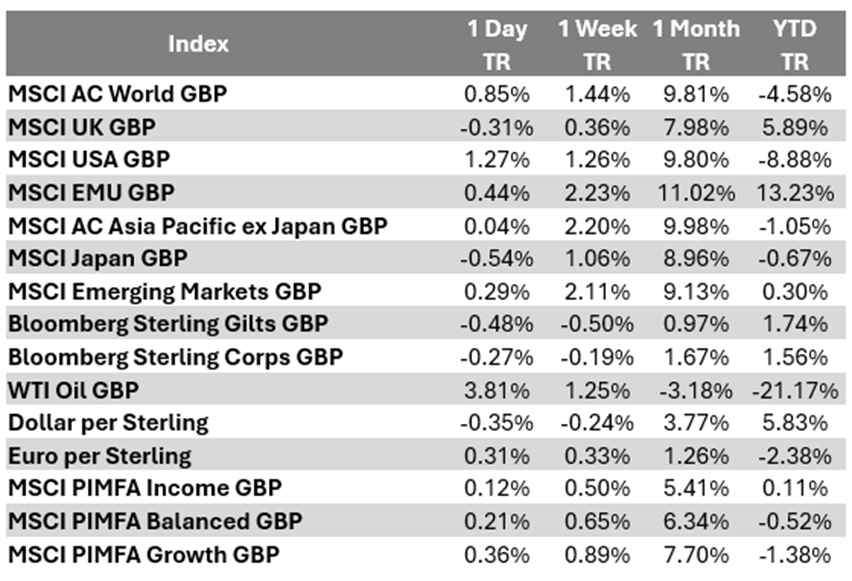

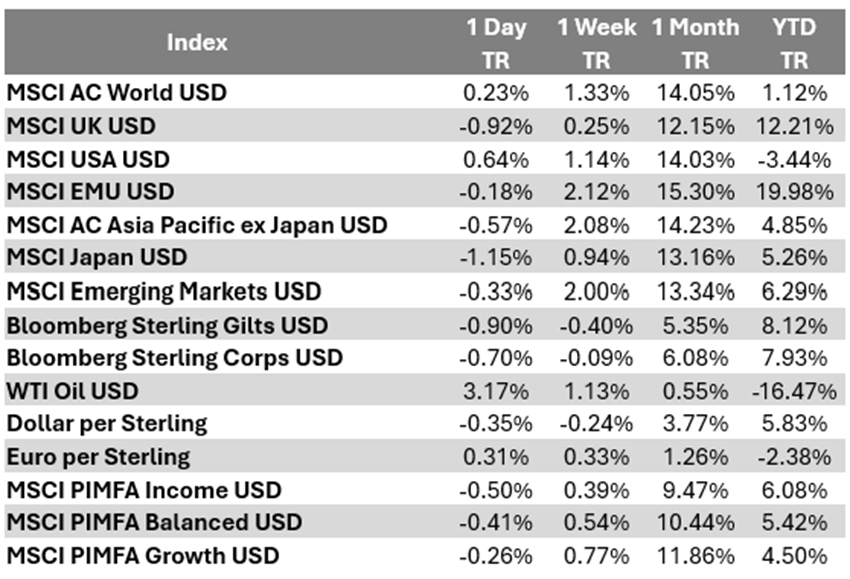

US equity markets on Thursday were riding higher on optimism that following a UK-US trade deal announced yesterday, there might be more US deals to follow, including even perhaps between the US and China. Elsewhere the picture was more nuanced with the UK FTSE100 equity index falling, perhaps reflecting the reality that the UK is still facing tariffs across most sectors – indeed, while UK Prime Minister Starmer referred to yesterday’s agreement as a “historic deal”, as it stands the UK is actually in a worse-off position than before the 2 April US tariff ‘Liberation Day’ Trump announcement.

UK-US trade deal … there are still tariffs for UK

Despite yesterday’s UK-US trade deal, there are still tariffs for UK. In autos, the latest 27.5% total tariff rate (made up of US President Trump’s extra 25% on top of the 2.5% that was originally in place) will now be 10% (so still 4x higher than before Trump took office in January), and only for a quota of 100,000 cars (above that volume, a 27.5% total auto tariff rate would kick back in – for context last year the UK exported around 102,000 cars into the US, so while the deal largely covers existing production for autos, in effect, there is an additional tax on any UK hopes to grow car exports into the US). Elsewhere, aluminium and steel tariffs were cut to zero. Crucially however, for most other sectors the universal base line 10% tariff rate that Trump has levied on all countries globally will also remain in force for the UK as part of this deal as it stands currently.

Bank of England

The Bank of England yesterday wrong-footed, for now at least, dovish hopes that they might accelerate the pace of interest rate cuts going forwards. While yesterday’s 25 basis points (bps) cut in the UK interest rate to 4.25%, from 4.50% previously, was considered by markets to be a foregone conclusion, the Bank was determined to be more balanced around the rate outlook – that was reflected in the split of votes among the Bank members behind yesterday’s cut – there was a 3-way split, with 2 votes for no change, 2 votes for a bigger 50 bps cut, and 5 votes for a 25bps cut, the latter which is what the Bank did.

What does Brooks Macdonald think

Even though UK government bond gilt yields rose on Thursday, the Bank of England probably has more interest rate cuts still to come. From the Bank’s own latest forecasts published yesterday, UK economic growth is mixed (with next year revised lower), unemployment rate projections are higher, private sector wage growth forecasts are flat to lower, and consumer inflation is now expected to be lower than previously assumed for every year of the Bank’s forecast horizon through to 2027. Drilling down to an interest rate forecast is tricky, but Bank governor Bailey yesterday said that market expectations for a terminal interest rate of 3.5% was “not unreasonable” – whether that level is hit later this year is probably the big question now, with markets appearing to be split on whether the Bank delivers 2 or 3 more 25 bps-cuts in 2025.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

09/05/2025