Please see below the latest bulletin from Brooks Macdonald, which was received earlier this morning and outlines their overview on the U.S. election so far:

What has happened

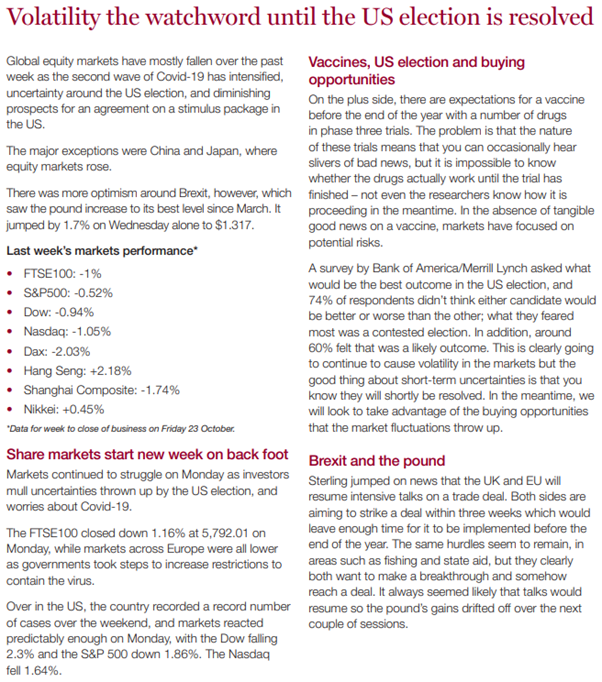

US equity futures and US Treasuries have both swung between gains and losses overnight as the US election results have started to roll in after polls closed. With key ‘swing states’ pointing to a much tighter overall race than expected, markets have had to recalibrate earlier expectations of a Democrat ‘blue wave’. Earlier, during regular trading hours on Tuesday, equity markets and government bond yields had both risen in tandem as investors focused their hopes for a post US election fiscal stimulus. On Tuesday, US ten year government bond yields had risen to their highest levels since June, and economically sensitive sectors including financials, industrials and consumer discretionary led, while gains in US technology shares also kept pace with the rally in the broader US equity market. However overnight, early voting results have suggested a much closer race than the polls had initially been expecting, and futures markets have braced for the risk that there might be a longer wait before a clear overall election result is known. While the race to the White House looks to be somewhat closer than first thought, an early clear winner has been the voting turnout. The latest update from the University of Florida’s US Elections Project (USEP) shows that more than 101m Americans cast their ballots before election day, easily beating past early voting election records, and equal to 73.4% of the entire 2016 election total votes. USEP also estimates that this puts the US on track for its highest voter participation in more than a century, with an estimated 160m votes or 67% turnout rate for those eligible to vote.

Early eyes on Florida, but it is not the only ‘swing state’.

As states race to count the expected record number of ballots, all eyes were on ‘bellwether state’ Florida. The state has a well-established process for counting early votes, and was always expected to be able to declare a result relatively early in the hours after polls closed. Of the two presidential candidates, Florida was considered more important for President Trump in order to keep any hopes of re-election alive. With 96% of the vote counted, Trump has held Florida, with 51.2% of the vote, against Biden’s 47.8%, and by a bigger margin than Trump won in the 2016 election. But Florida is not the only swing state. There are as many as a dozen or so ‘swing states’ to watch in the US election, which are states that historically have been closely divided politically. Alongside Florida (which has 29 electoral college votes), these include Pennsylvania (20), Ohio (18), Georgia (16), Michigan (16), North Carolina (15), Arizona (11), and Wisconsin (10). However, some US states, such as Pennsylvania and Wisconsin could not start processing and counting early votes until election day, so early final results here are less likely. Initial indications across some of these states suggest that the balance of votes might be close.

Not just the race for the White House, as Senate is key

In recent weeks, while polls suggested a Democrat win for the presidency and the House of Representatives, a much closer race has been for the control of the Senate. With Republicans defending a majority of 53 seats to 47 in the Senate, Democrat hopes for control have needed to flip a net of at least 3 Republican-held seats if Biden took the presidency, and 4 if Trump stayed in office (as the Vice-President can vote in the Senate in the event of a 50-50 tie). So far, Democrats have lost a seat in Alabama, and gained one in Colorado. Ultimately, should the Republicans keep control of the Senate, this would suggest more of an economic status quo where fiscal policy hopes might be more constrained that they might otherwise have been under a Democrat majority. As such, a ‘blue wave’ of infrastructure spending looks a little less likely at this time.

Initial reactions from Biden and Trump

Biden was first to speak to his supporters in the early hours, He called for “patience” and conceded that for a result it might be “maybe tomorrow morning maybe even longer“ and “it isn’t over until every vote is counted”. Meanwhile Trump has tweeted “We are up BIG but they are trying to STEAL the Election. We will never let them do it.” In a following address, Trump has remained confident saying “As far as I’m concerned we’ve already won this”. Clearly, neither candidate is looking to concede to the other at this early stage.

What does Brooks Macdonald think

Coming into this week’s US election, markets have had to contend with two key potential headwinds for risk appetite: first, there was the risk of an inconclusive early electoral result and with it likely legal challenges and worries of civil unrest; and second the risk of a corresponding delay to a long-awaited additional stimulus. With results so far pointing to a much tighter race than the polls had predicted in recent weeks, both of these risks remain a focus for investors. With no clear overall victory for either candidate at this stage, uncertainty looks to be the near-term reality for investors.

As you can see from the above, nothing is a given at this stage in terms of the election outcome and uncertainty in markets seems to be the forecast for the near term. I think it is fair to say, that when the outcome has been confirmed and gone through any legal challenges that may arise, that’s when markets will be more indicative of what impact the outcome will have.

As I say, it is imperative to remain focused on your long-term investment objectives, do not let short-term volatility, as we are seeing right now, distract you. It is important to remain invested to ensure you benefit from the recovery when it comes.

We will continue to provide you with updates on the ever-moving feast that is the U.S. election along with market commentary from leading investment houses to keep you abreast of the outlook for the future.

Please keep safe and healthy.

Carl Mitchell – Dip PFS

IFA and Paraplanner

04/11/2020