Please see the below update from Tatton Investment Management received just now:

Overview: Market wobbles turn into a rout

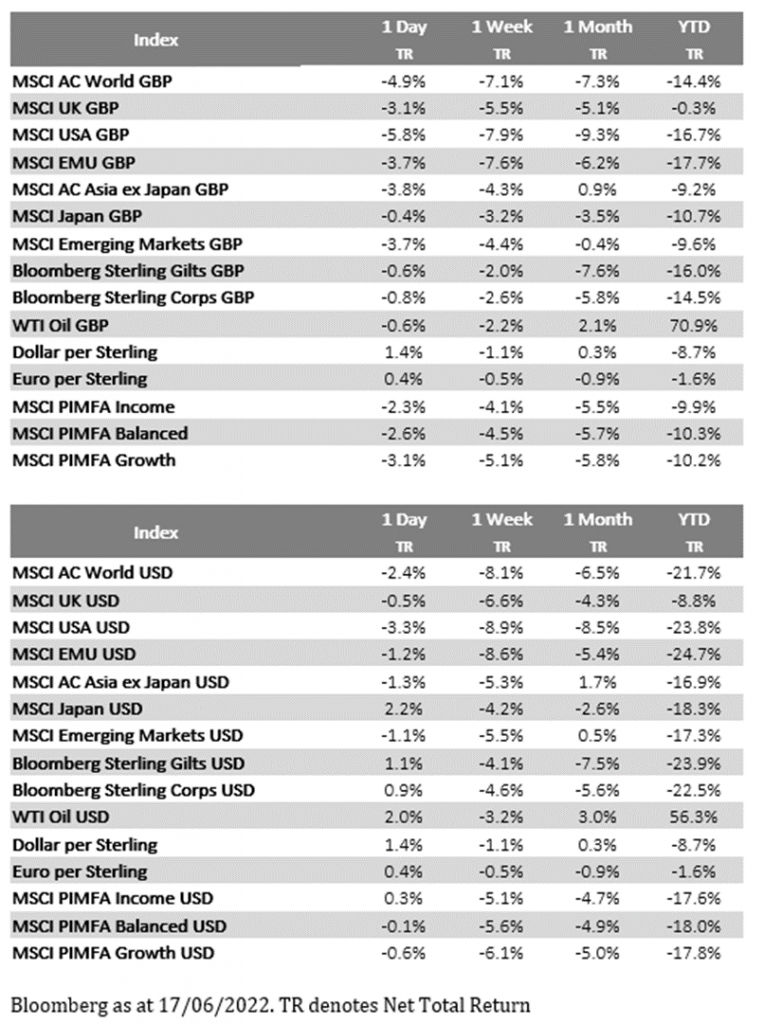

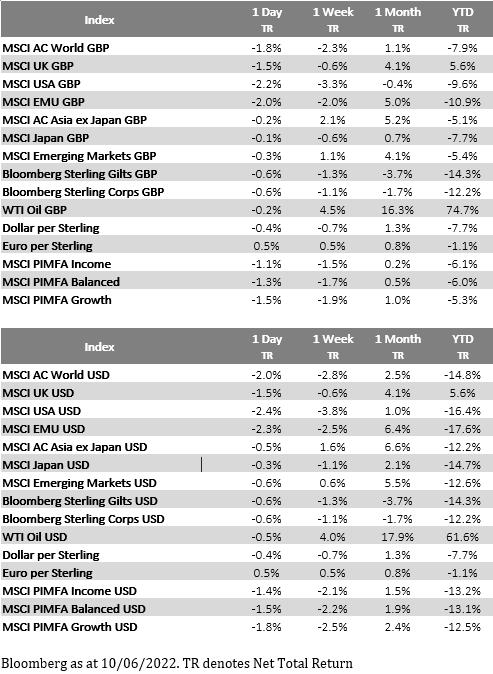

Last week, as central banks around the world were reasserting their credibility as guardians of monetary stability, recent stock market wobbles turned into a fully-fledged rout. Persistent growth concerns turned into fears that central bank actions would indeed lead to a global recession. This must seem extraordinary to most people, as we have all grown used to central bankers being very effective trouble-shooters. But the pandemic period offers very little precedent – and therefore no sort of economic playbook – of how to handle the post-pandemic ‘hangover’ period. We will never know what would have happened had we not had the biggest dose of central bank support ever to protect us from the economic pain inflicted by the pandemic. However, we can see that the medicine itself, huge monetary injections, has almost certainly contributed to global inflationary pressures in a not insignificant way. Unwinding this support without choking off growth is proving increasingly challenging for policymakers.

Last week, we saw interest rate hikes in the UK and US, an emergency meeting at the European Central Bank (ECB) and some poorly received comments from the Bank of Japan (BoJ) governor. By far the biggest story of the week was the decision from the US Federal Reserve (Fed) to raise interest rates by 0.75%, its biggest single increase since 1994. The decision came after a two-day meeting of the Federal Open Markets Committee (FOMC), where the Fed’s rate setters discussed rampant inflation and its effects. Consumer prices in the US jumped significantly more than expected in May, while a report last Friday showed Americans’ long-term inflation expectations have risen. Together with the continued tightness in US labour markets, this is a worrying sign, suggesting price rises could become embedded in the economy through the dreaded wage-price spiral dynamic that became the hallmark of the 1970s decade of economic stagnation and decline.

Fed chair Jay Powell told the press he is determined to tame soaring prices, even if that means a hit to growth and jobs. According to the ‘dots plot’ of FOMC members’ interest rate expectations the Fed will push interest rates well above 3% by the end of the year, with more hikes to come in 2023. This is a far cry from what was telegraphed as recently as March’s meeting, which pencilled in rates of less than 2% by the end of the year. This is a sign of how much the outlook has changed in the last three months alone. On this basis, it is very likely that Fed tightening has already had an impact on future inflation – just one that will take some time to filter through. The somewhat worrying conclusion is that any further Fed tightening might only have an impact next year, at which point inflation is expected to be much lower anyway. In other words, there is a good chance that hiking rates over the next few months will only serve to make a recession – if and when it does happen – worse.

The good news is that bond markets have not reacted badly to Fed tightening. Indeed, the calm in bond markets after the Fed’s announcement perhaps suggests that investors expect a sharp but manageable slowdown, and that the Fed will indeed do what it takes in the fight against inflation. Credibility – the most important thing for any central bank – seems to have been restored. And even if a recession comes in the next year, market resilience suggests the financial system is stable enough to cope with it. There are many risks ahead, but markets seem confident the Fed can handle them.

The UK: stuck between a rock and a hard place

The Bank of England (BoE) raised interest rates for the second time in as many months last week, after a Monetary Policy Committee (MPC) meeting that had a distinct air of déjà vu. After a split vote – with some members wanting a large hike – the MPC opted for a 0.25% increase that took UK interest rates to 1.25%. And just like at the beginning of May, more dire economic warnings were issued. The BoE now expects inflation to reach 11% in October. At the same time, Britain’s economy is expected to shrink by 0.3% this quarter – a worrying combination of high prices and low growth. The quarter-point rise was in line with expectations, but a minority of economists were expecting a more aggressive 0.5% hike. The MPC promised to “act forcefully” against rapid inflation in its accompanying statement, but investors did not seem convinced. Sterling weakened against the US dollar in the day’s trading – the latter of which was buoyed by the Fed’s much larger rate hike.

On the one hand, Britain faces the highest inflation of any G7 country and has a worryingly tight labour market. On the other, it has the worst growth numbers in the same group, and some economists think we may already be in a recession. These forces pull monetary policy in opposite directions – the former calling for drastic tightening and the latter calling for support. To make matters worse, the UK government has announced several support measures which are expected to boost consumer demand, and more are likely on the way. That drastically reduces the BoE’s room for manoeuvre, and has led some analysts to predict a 0.5% rate hike at the August meeting. In this context, the MPC’s latest move looks particularly cautious. This could well be accompanied by a further deterioration in growth prospects. Ultimately, these will feed through into lower inflation at some point. But given how much consumer inflation can lag, there could be a great deal of pain before that point.

Japan’s outlier role has good and bad effects

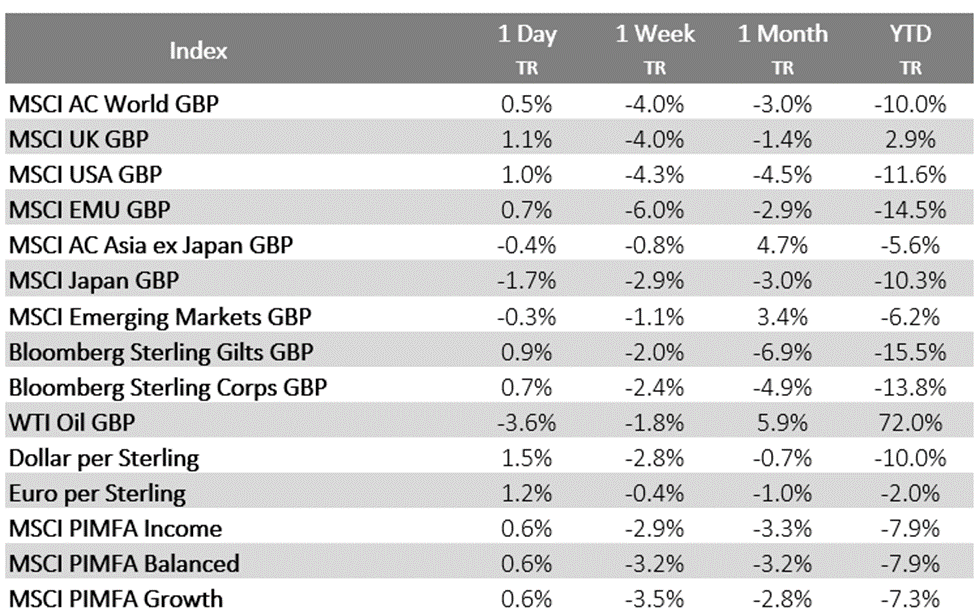

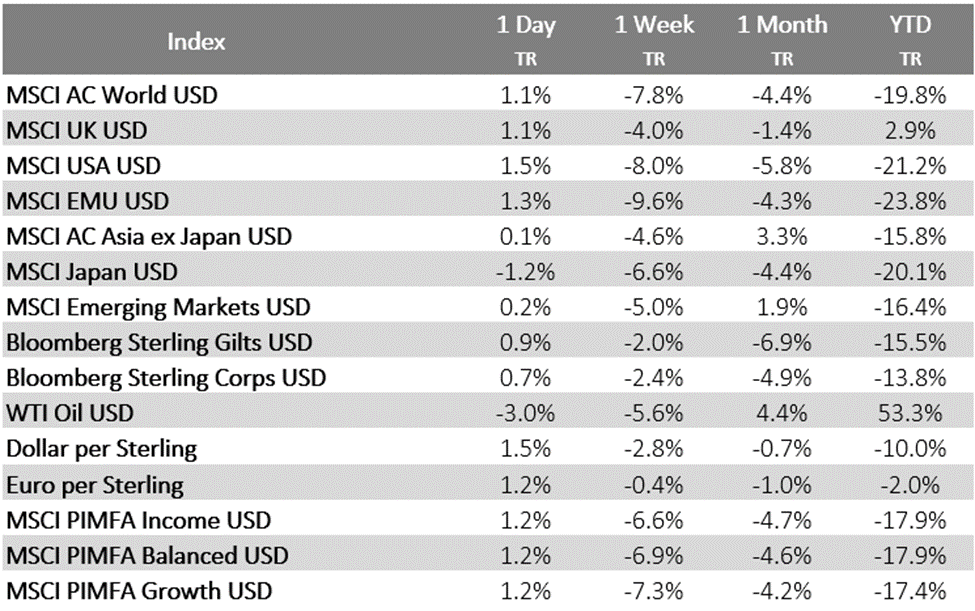

It may seem the world’s central banks are in a synchronised tightening mode, but that’s not the case throughout. Both the BoJ and the People’s Bank of China are engaged in forms of quantitative easing. Last week, the BoJ committed to unlimited bond purchases (effectively new easing), a stance reiterated at its Friday meeting. Neither Japan nor China engaged in the massive monetary easing of 2020-2021. Indeed, both have had quite anaemic monetary growth over the period. This may well be a factor in why their (and Asian) growth levels had been well below potential, but now they are able to ease policy rather than having to tighten.

The Bank of Japan is an outlier among the world’s major central banks. While others have fretted over global inflation, Governor Haruhiko Kuroda has stayed calm. And when others trimmed balance sheets and raised rates, Japan stayed the course. Rates are still negative in the world’s third largest economy, and the BoJ is still buying government bonds in massive quantities to maintain its policy of yield curve control. The contrast with the rest of the developed world is now causing strain in Japan’s financial markets. Last Monday, the yen sank to its lowest dollar value in 24 years. That is despite the BoJ, Ministry of Finance and Financial Services Agency issuing a rare joint statement expressing concern over the yen’s slide. The implication was that policymakers may have to shift gears and match their hawkish contemporaries across the globe. But economists expected no changes at Friday’s BoJ meeting, and that is exactly what they got. At the same time, Japanese consumer inflation rose to 2.5% year-on-year in April – the highest level 2014. While that is well short of the price rises seen elsewhere, Japan’s history of chronic disinflation makes anything above the 2% target an eye-catching figure. Earlier this month, Kuroda gave a speech where he claimed that “Japanese households’ tolerance of price rises has been increasing”. His comments were badly received by the public. All of this has increased speculation that the BoJ may finally relent in its monetary support – allowing bond yields to rise. The short trade on Japanese government bonds has increased significantly, forcing the BoJ to spend billions defending yields.

We think this trade is misguided. Japan is in a completely different situation to other major economies, with very little inflation pressure and a still-sluggish economy. Financial conditions have eased recently, and we suspect the BoJ is willing to let this continue. After decades of inertia, the BoJ is likely to want a temporary overshoot of its inflation target, and will likely see it as a spur for economic activity. The same could well be true of currency weakness. There has been speculation that Kuroda sees benefits in a weaker yen, which could help exporters. Even if this is wide of the mark, the yen is extremely cheap on a fundamental basis; rapid inflation elsewhere has increased Japanese consumers’ relative purchasing power. A move down from here would therefore be difficult to sustain. In short, investors bet against the BoJ at their own peril.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

20/06/2022