Please see investment bulletin below from Brooks Macdonald received this afternoon – 17/06/2022.

What has happened

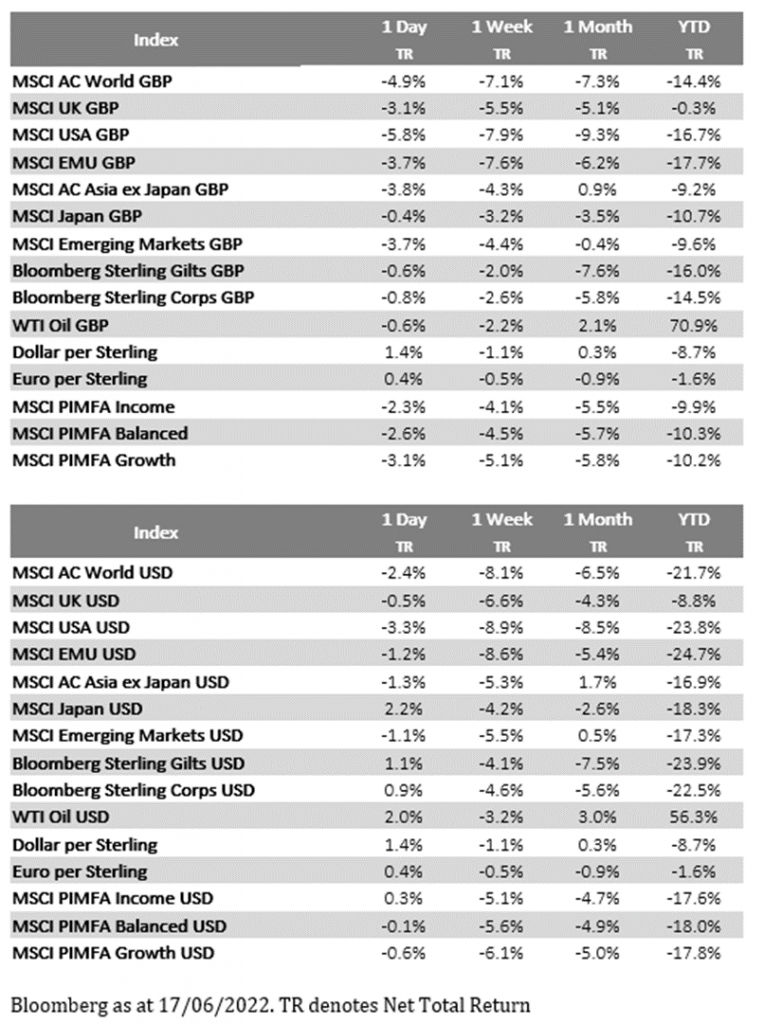

The latest policy announcements from the Swiss National Bank and Bank of England added to the hawkish rhetoric of recent days, driving equity markets lower. Equities slumped globally with few areas avoiding a widespread collapse in optimism.

Bank of Japan

The Bank of Japan concluded their monetary policy meeting earlier today with the bank deciding to retain its quantitative easing programme. Whilst this was widely expected, the BoJ is a notable exception to the global theme of slamming on the monetary brakes. Bucking the trend has been costly to the Yen which has weakened significantly as policy divides between Japan and, most notably, the United States. The quantitative easing programme is also becoming more expensive, with the Bank of Japan needing to defend their 0.25% cap on 10-year bond yields. The central bank this week alone has had to purchase $9.6tn worth of assets – a staggering amount.

Bank of England

The Bank of England voted for a smaller 25bp rate rise with 3 of the 9 voting members opting for a larger 50bp hike. The move arguably prioritises the committee’s economic growth fears above inflationary fears although the statement was keen to underline the bank’s commitment to tackle inflationary pressures. The bank said it would be ‘particularly alert to indications of more persistent inflationary pressures, and will if necessary act forcefully in response’. The bond market took this as a signal that the bank would act more aggressively in upcoming meetings however there is clearly still some reticence in the committee over the UK economy’s ability to bear much higher rates. Sterling continues to trade weakly versus major trading peers which, given the UK’s dependence on imports, may provide further inflationary pressure over the coming months.

What does Brooks Macdonald think

One of the factors behind yesterday’s selloff was the unexpected hawkish shift from the Swiss National Bank. The SNB hiked rates by 50bps, which not only represents the first hike in 15 years but the bank also decided to go with a super-sized hike to start the cycle. The SNB also established a new currency policy, with the result effectively putting a cap on the Euro/Swiss Franc exchange rate. Whilst it might feel like central bank hawkishness has reached its limit, the SNB decision yesterday is a reminder that central banks still have room for surprise and this reminder was particularly unwelcome given the widespread pessimism amongst market participants this week.

Please continue to check back for our latest blog posts and updates.

Charlotte Clarke

17/06/2022