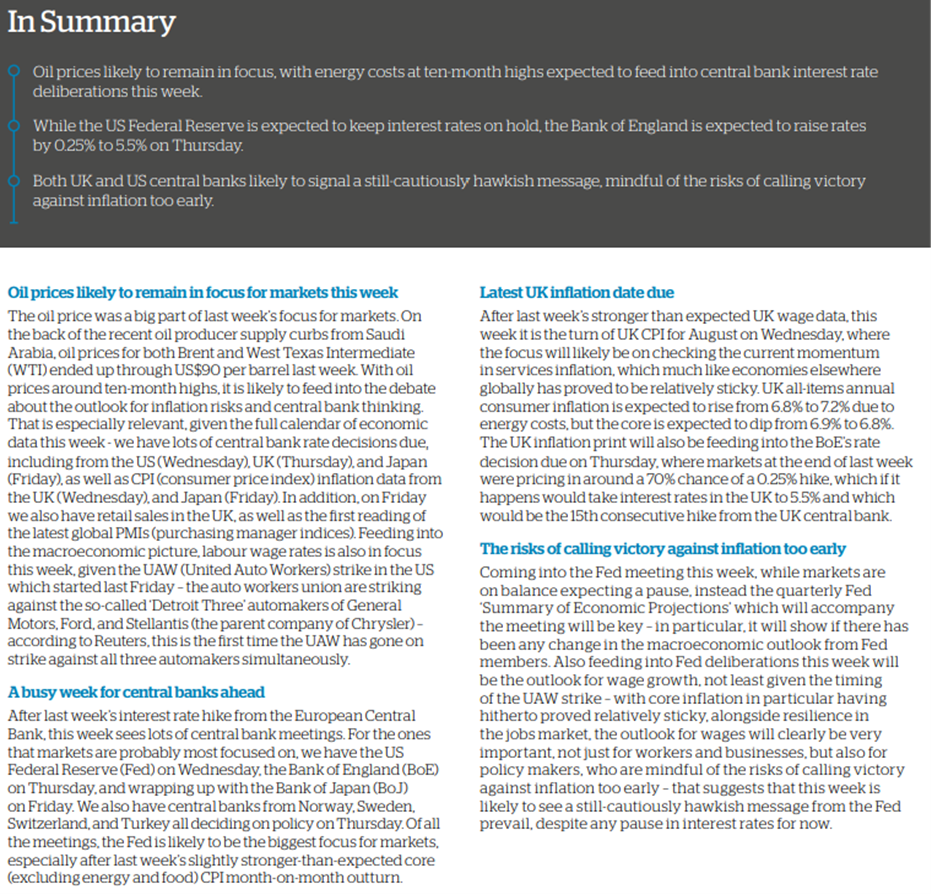

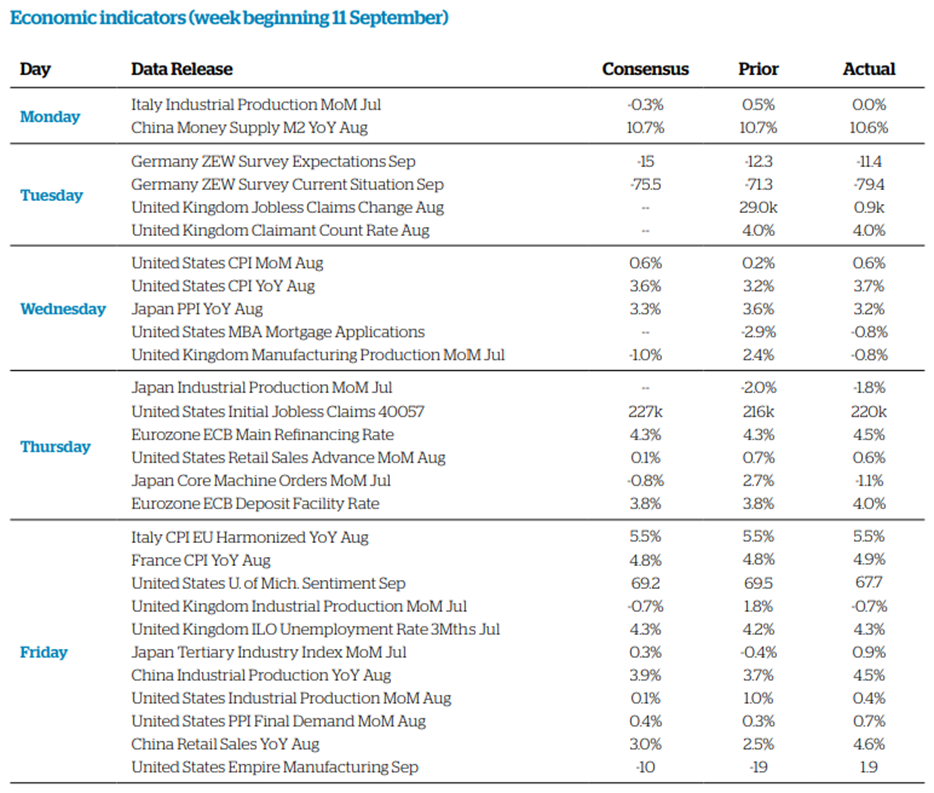

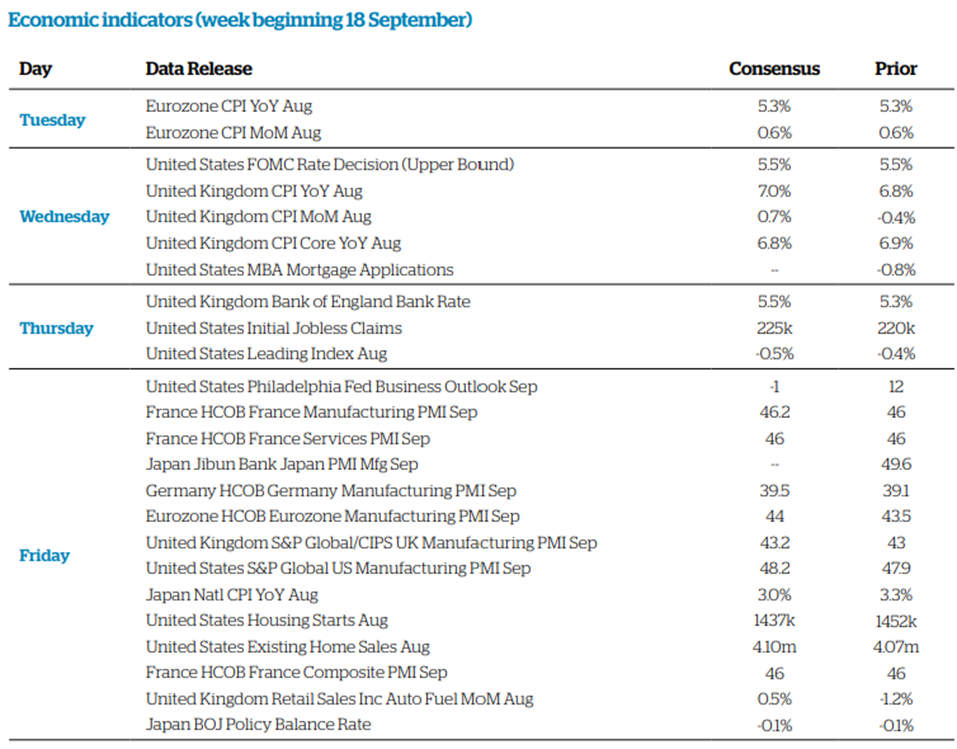

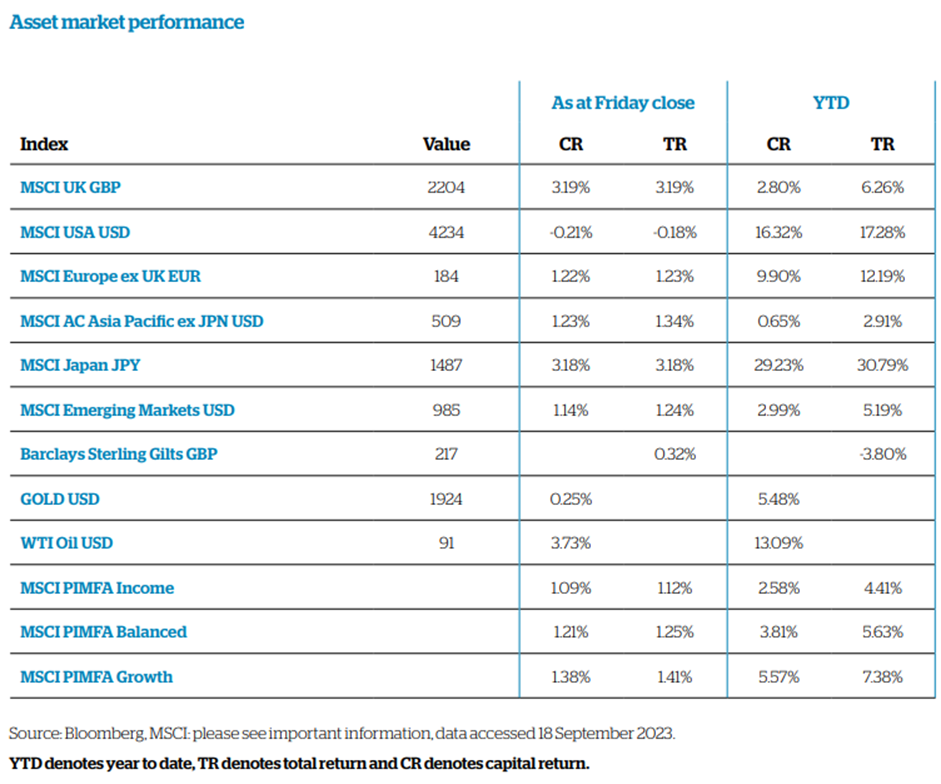

Please see below the Tatton ‘Monday Digest’, which was received this morning (11/09/2023) and provides their views on global economic news from the past week:

Overview: oil prices up and an ill wind for renewables

So far Markets have been generally quiet during September, but energy is again becoming an issue. Oil prices have risen since the start of the summer, with Brent crude having bounced along a bottom of $73 per barrel for the first half of 2023. Compared with the wild swings of 2019 to 2022, it doesn’t feel like much, however, it has been a factor in pushing bond yields back above 4.2% in the US and German yields to 2.6%. Much of the rise in near-term prices is driven by the seasonal variation in prices, with the passage into autumn meaning the nearer contracts now cover cooler months. The rise in oil prices is not enough to seriously create disturbance by itself, but US government bond yield levels are close enough to their recent highs to suggest a build-up of market tension. In a sense, the risks for government bonds are higher because risks are lower elsewhere. Credit spreads rose slightly on the week, but the extra return from higher coupons allows higher yielding bonds to outperform.

Returning to energy, no offshore wind projects won contracts in this year’s annual auction for UK Government subsidies last week, a significant setback for increasing capacity to 50 gigawatts by 2030. Keith Anderson, chief executive of offshore wind developer Scottish Power, said the “economics simply did not stack up” and the results were a “wake-up call for the government”. It’s not just the UK. There has been a marked change in sentiment towards the developed world’s renewable energy companies. Orsted (previously Danish Oil and Natural Gas), which is a leading player in wind power development, announced it was seriously considering abandoning its US wind power development projects unless the US government guarantees more support. Mads Nipper, Chief Executive of Orsted said that future projects need consumer prices for energy to increase. He said. “And if they don’t, neither we nor any of our colleagues are going to build more offshore. It’s very simple”, sounding just like Keith Anderson.

Offshore farms may be critical to environmental goals but are capital and labour-intensive. At the same time, input costs have shot higher, partly because of the large size of the IRA. Similar large projects run by Vattenfall AB and Iberdrola SA have also been scrapped. This is putting some supply chain companies under substantial pressure, and one potentially difficult consequence is that the companies facing problems are the ones widely owned by ESG investors. Many recognise that their ESG principles are more important than any near-term investment return problems, but many also thought that the inevitable demand forced through climate change would ensure these companies would be winners. ESG investors, perhaps more so than others, will need to be prepared to stick it out for the long term.

It’ll cost an Arm and an IPO

Last Tuesday, Japan’s SoftBank unveiled initial public offering (IPO) plans which would bring microchip designer Arm, one of Britain’s biggest tech companies, to public markets with a valuation of around $52 billion. The tech sector’s big hitters have already lined up to buy a big chunk. Cornerstone investors including Apple, Google, Nvidia, Samsung, Intel and TSMC have indicated they will purchase up to $735 million in Arm shares. Since SoftBank plan to list only around 10% of the tech company’s stock in New York, analysts estimate that around 15% of the IPO’s demand is already accounted for, although not date is confirmed.

Some analysts and commentators think the price is too high. Arm designs key parts of the microchips that feature in most of the world’s smartphones. The crux of the issue is how Arm relates to the artificial intelligence (AI) growth story that has captivated the tech sector. Arm’s designs are currently indispensable to global tech, their role in the next decade’s predicted AI-related boom is considered fairly small (of course, this is disputed by the company itself).

Untangling the tech and chip sector noise for Arm specifically is difficult, so a valuation based on industry fundamentals is hard to gauge. From our perspective, it makes it a great test case for the mood in wider capital markets and on that front, it looks like investors have a big appetite for equity. Things may change, but the fact that so much capital is already lined up from cornerstone investors shows that there is certainly money and demand. Even if SoftBank fall short of their $4.9 billion target to raise, the fact so much can be raised for an IPO when interest rates are so high is quite something.

The failure of significant IPOs was one of the big factors underlying the change in market sentiment in the run up to the dotcom bubble bursting in 2001. Back then, it became apparent that there was no demand for investment, and investors got valuation vertigo. It seems quite apt that, in the midst of another tech investment craze, there should be another stern test of market resolve. Anything close to SoftBank’s valuation would be a sign that confidence is still high, and we will be watching closely to see if investors are still willing to pay an Arm and a leg.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Carl Mitchell – Dip PFS

Independent Financial Adviser

11/09/2023