Please see below the daily update article from EPIC Investment Partners, received this morning – 18/09/2025

The Fed’s decision to cut interest rates by 25bps, to a range of 4.00-4.25%, marks a clear dovish pivot, with policymakers signalling a greater focus on the labour market. The first reduction of the year was nearly unanimous, with the sole dissent coming from newly installed Governor Stephen Miran, a close ally of Donald Trump, who (surprise, surprise) advocated for a more aggressive half-point cut.

This move highlights a notable divergence in views in the outlook for rates. The latest “dot plot” projections show the median view for two more cuts this year, a more aggressive stance than previously held. However, a significant number of officials still see no further cuts this year, underscoring deep divisions on the committee and a stark disconnect from the Trump administration’s public calls to “get interest rates down to ZERO, or less”.

At his presser, Fed Chair Powell, acknowledged the difficult trade-offs facing the central bank, stating, “It’s challenging to know what to do,” and “There are no risk-free paths now.” This shift, from a previous focus on combating tariff-driven inflation to addressing a weakening employment picture, represents a significant change in the Fed’s “reaction function”.

The focus now shifts to the Bank of England’s (BoE) meeting later today. While a hold is widely anticipated, the recent economic data presents a mixed and challenging picture for policymakers. August’s UK inflation rate held steady at 3.8%, well above the central bank’s 2% target, driven by a pick-up in food and services inflation. At the same time, the labour market has shown signs of softening, with the unemployment rate standing at 4.7% and wage growth remaining elevated. The BoE has already embarked on a “gradual and careful” rate-cutting path, with the most recent 25bps cut in August bringing the rate to 4%. The MPC is now faced with a similar dilemma to the Fed, balancing the risk of a weakening economy against the need to bring persistent inflation under control.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 16/09/2025.

U.S. interest rates expected to fall

Guy Foster, Chief Strategist, discusses the implications of a Federal Reserve interest rate cut. Plus, our Head of Market Analysis, Janet Mui, breaks down the latest U.S. inflation data.

Key highlights

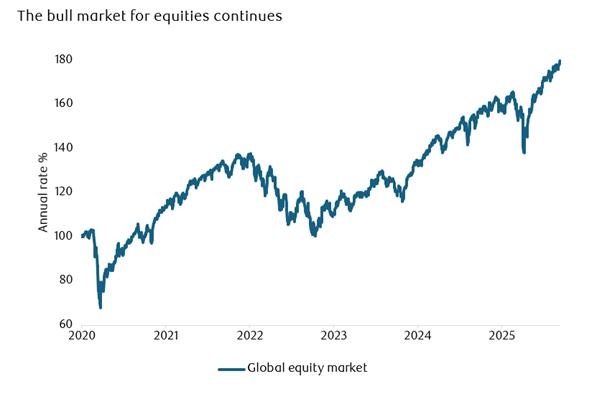

Stocks go up: Equities rallied as the first U.S. interest rate cut of 2025 – and the first of the second Trump administration – approaches.

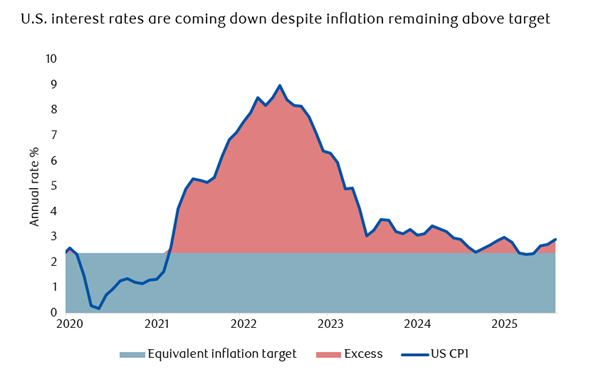

U.S. inflation: Latest figures put U.S. Consumer Price Index inflation at 2.9% in August, which indicates that Personal Consumption Expenditure figures will exceed the Federal Reserve’s target of 2% when released later this month.

Europe holds rates: The European Central Bank held interest rates last week and the Bank of England is expected to follow suit on Thursday.

Stocks go up, rates come down

Source: LSEG Datastream

Stocks performed well last week, cheered on by the fact that the first U.S. interest rate cut of 2025 – or, perhaps more significantly, of the second Trump administration – is almost upon us.

Last week’s data removed any lingering doubt that rates will be cut this week, despite inflation seeming to move further above the Federal Reserve (the Fed)’s 2% target for Personal Consumption Expenditure (PCE) inflation. Last week’s Consumer Price Index data showed the rate of price growth accelerating to 2.9% per annum, indicating that the PCE will also have accelerated when it’s released later this month.

Source: LSEG Datastream

The Fed has a dual mandate to maintain price stability and employment. Inflation is expected to remain above target, but employment growth is slowing. The Fed is expected to prioritise heading off recession risk over the risks associated with inflation staying above target for a fourth consecutive year.

That judgement has been accompanied by an unusual amount of political pressure. President Trump’s nominee for governor of the Federal Reserve, Stephen Miran, was confirmed on Monday by the U.S. Senate. He will simultaneously retain his position as chair of the Council of Economic Advisers. Miran’s expected to take part in the Federal Open Market Committee’s meeting, which is being held over the next two days.

The increase in inflation was driven by a few factors. Cars, clothes and appliances all saw increases, suggesting the possible passthrough of tariffs. However, medical goods, toys and technology saw price falls. The data was not therefore conclusive on the speed with which tariffs are being passed through. If they are, there’s a convincing argument for the Fed to overlook tariffs as a source of inflation, and to consider them a one-off rather than a recurring source of price increases.

Will Europe see rate cuts?

Outside the U.S., the outlook for interest rates is steadier.

The European Central Bank (ECB) left rates on hold in its most recent meeting, and the Bank of England is expected to hold rates this week as well. For the ECB, the cuts made so far seem to have been successful in prompting an uptick in loan demand.

The central bank seems quite confident on the outlook for inflation and was able to upgrade estimates of current growth despite being hit by tariffs on exports to the U.S.

How’s the UK economy faring?

The UK still suffers from persistently high inflation but as we’re seeing signs of the labour market slowing, this should diminish over the coming months. Growth during July was estimated to have stagnated after a strong start to the year, and the housing market has slowed despite improving affordability. The obvious headwind to UK growth is concern over taxation as the Autumn Budget approaches.

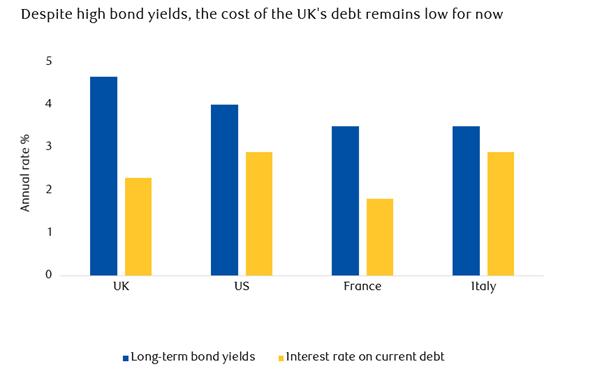

In fact, UK borrowing costs are the highest in the G7 (which consists of Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) and most developing markets. This is often seen as a sign that the markets are concerned about UK creditworthiness but in reality, the UK’s need to raise taxes is a function of its fiscal rules, designed to ensure that its creditworthiness stays intact.

The UK isn’t struggling to finance itself despite having some of the highest bond yields among developed markets. The average interest rate the UK is paying on its debt is 2.3%, well below current yields.

Bond yields reflect the cost of debt the government will pay on its next borrowing, but most UK debt was issued when interest rates were much lower. This means the UK is currently paying less for its debt than other countries, despite having higher bond yields.

Source: LSEG Datastream

However, that situation won’t last forever. As the UK’s need for new borrowing catches up with its current high yields, its borrowing costs will drift upwards, so there’s good reason to get the fiscal books in order.

That will be difficult as the government won power on promises to enhance public services while committing to not raise most major taxes.

The situation is much less acute than in France though. France’s current debt is more expensive, its budget shortfall is greater, it has no apparent plan to resolve the issue and its parliament is divided.

After the fall of François Bayrou and Michel Barnier’s governments, French President Emmanuel Macron has appointed Sébastien Lecornu as the new prime minister and tasked him with getting agreement on a budget to begin to restore France’s economic credibility.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see the below article from EPIC Investment Partners detailing their discussions on China’s Hydro Infrastructure project. Received this morning 16/09/2025.

Construction officially began in July on what is likely to be the biggest infrastructure project in history. Beijing first laid out definitive proposals for the dam back in 2021.

The Yarlung Tsangpo river flows from the melting glaciers of the Tibetan Plateau, cutting a sharp U-turn around Namcha Barwa, the highest peak in Nyingchi prefecture, before plunging more than 2,000 meters over a 50-kilometer stretch forming one of the world’s deepest canyons and an irresistible source of hydropower potential. Engineers plan to drill tunnels from the top of the bend to the bottom, channelling water through multiple turbines before sending it back into its natural course. It is a system designed to minimize upstream and downstream disruption. The project should significantly cut China’s dependence on coal which still powers more than half the national grid.

To put the size of the project into context, the project will consume sixty times the cement of the Hoover Dam, more steel than over one hundred Empire State Buildings and enough concrete to build a two-lane highway around the Earth five times. Another way to understand the full scale of this $167bn project is to compare it to the $37 billion Three Gorges Dam – the world’s largest power plant. The hydropower project, with a potential capacity as high as seventy gigawatts, could generate three hundred terawatt-hours a year (roughly equivalent to the UK’s total annual electricity consumption).

There are several difficulties. The project lies in a seismically volatile region. The 1950 8.6 magnitude Assam-Tibet earthquake, one of the strongest ever recorded on land, happened just 150 miles away from Nyingchi. Engineers plan to drill tunnels from the top of the bend to the bottom, channelling water through turbines before sending it back into its natural course. This raises multiple ecological issues, not least the impact on water flows to the Indian subcontinent.

The economic impact to the Tibet region will be considerable. Hundreds of thousands of jobs will be created while it is estimated that project will add perhaps 0.2% to China’s GDP each year. Construction of transmission lines will allow the plant to serve China’s industrial east coast and southern regions like Hong Kong as well as poorer western areas such as Tibet itself.

It is an audacious project but carries considerable economic and environmental risks.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 15/09/2025

Markets’ outlook preference turns positive

It was a slightly confusing week. US 30-year government bond yields dropped sharply – suggesting weaker growth expectations – but small cap stocks had a strong week, suggesting the opposite. In a sense, both narratives are true. Weaker US jobs data suggests slower growth, but locked in a Federal Reserve rate cut this Wednesday. Incoming tariff revenues also make the US a more reliable borrower, making treasury bonds look like good value.

Stock markets, on the other hand, see decent corporate profits for large cap stocks. Small caps have struggled with high borrowing costs, but those will fall as the Fed eases and growth rebounds. Investors are looking through the current slowdown to improvement later on.

Moreover, American business sentiment is still strong – and inflation is picking up. We calculate that 3-month annualised inflation is now running above 4%. Companies feel they can pass on tariff costs, so inflation will likely continue over the next few months. Does that mean the Fed shouldn’t cut? Not really, as their focus in on weak employment, which makes a wage-price spiral unlikely. US economic resilience means there is no emergency to cut rates – but on balance they are probably a little too high.

The rosy stock market view doesn’t match up with current geopolitical tensions either. Neither Russia’s polish incursion of Israel’s strike on Qatar upset risk assets. Neither are likely to cause retaliation (and in Russia’s case, could restore a US-Europe alliance) but they do raise risks. Those risks aren’t themselves enough to upset the outlook; that would require clear signs of economic disruption. Global instability can make markets more volatile if and when there is a strong catalyst for a downturn. Without that catalyst, there’s nothing to stop equities grinding higher. With recession now highly unlikely, it’s no surprise that investors are focussed on the positives, not the negatives.

Is China’s rally real?

Chinese stocks have outperformed all other major regions year-to-date and on a 12-month basis. That’s remarkable, considering the economic challenges it faces: tariff pressures, persistent deflation and weak consumer demand. Recent trade détente with the US can’t explain China’s rally alone. The usual explanations are government stimulus (including interest rate cuts) and a tech boom following DeepSeek’s AI release. Underpinning these has been a strong capital rotation into stocks – partly from property (the traditional Chinese savings vehicle) but also from low-yielding bonds. At the start of September, China set a new record for debt-financed stock ownership: ¥2.29 trillion.

The record it beat had stood since 2015 – a year marked by a euphoric China rally and subsequent stock market collapse. Beijing was also trying to reduce excess production capacity back then, exactly as it is now. But we don’t think this is 2015 again. Debt-financed positions account for just 2.3% of market cap, compared with 4.7% a decade ago, and policymakers aren’t as gung-ho as they were – even trying to calm the rally by allowing more short-selling and cracking down on speculative buying. Beijing’s efforts to fight deflation are softer than in 2015 too. The government is trying to limit excessive price competition and support corporate profits, but isn’t shuttering capacity or forcing mergers.

Beijing has struggled to support consumption over the past year, but the resolve is clearly there – evidenced by Premier Li Qiang’s recent promise to support a fledgling property market recovery. That’s good for China’s long-term prospects, and abundant liquidity is good for medium-term stock flows.

Global investors should keep in mind that Chinese equity comes with an added risk of stranded capital – either from government crackdowns or Chinese-Western financial decoupling. But its stock market has a lot to offer: a well-supported rally now, and diversification benefits for the future.

Make Tesla Magnificent Again

The ‘Magnificent Seven’ US tech companies dominated the Q2 earnings season, but one member doesn’t look so magnificent; Tesla’s profit and share price performance has been dire this year. The electric carmaker is no longer in the top seven US companies by market cap, having been supplanted by Broadcom.

Tesla talk often focusses on Elon Musk and his on-and-off friendship with Donald Trump, which hurt Tesla sales in Europe. Rumours of the board looking to replace Musk were quashed by its $1tn compensation offer. But Tesla’s struggles aren’t all about Elon: it has also lost market share to cheaper alternatives like China’s BYD.

Tesla’s latest earnings call pivoted to newer tech like robotaxis and Optimus robots. Some of that is a sales pitch to investors (there are many hurdles to clear before techno-optimism turns into profit) but it’s also a long-term strategy. Tesla has always sold itself as a pioneer in a new landscape rather than a car manufacturer. Now that the rest of the EV market is catching up, Tesla is looking for even newer landscapes.

That’s very different to the rest of the Mag7, most of whom are established players with strong cashflows. A promise to dominate driverless cars and future robots is a different investment pitch to the likes of Apple. That doesn’t make a bad pitch; Morgan Stanley researchers rate Tesla’s stock highly for its earnings potential.

But we should question how useful it is to group Tesla in the Mag7. All those companies are pivoting toward frontier sectors, but none of them base their current valuation as highly on those sectors as Tesla. Its pivot to the future might make Tesla magnificent again one day, but in the here and now, investors should evaluate companies according to their risk-return profiles, not catchy names.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below the daily update article from EPIC Investment Partners, received this morning – 11/09/2025

China’s government is taking significant steps to address a mounting issue of unpaid bills owed by local authorities to the private sector, a problem with estimated arrears reaching over $1 trillion. This initiative, which has the backing of President Xi Jinping, aims to complete a comprehensive settlement by 2027, restoring trust and stability to a private sector that has been significantly impacted by the financial delays.

The core of the strategy involves leveraging state lenders and policy banks, such as the China Development Bank, to provide loans to local governments. This financial injection is intended to cover at least 1 trillion yuan ($140 billion) in a first phase, with the ultimate goal of clearing the substantial debt. The move acknowledges the severity of the situation, as President Xi has publicly warned that delayed payments can cripple businesses and erode public confidence in the government.

While this plan offers much-needed relief to private companies and contractors, it also shifts a considerable financial burden onto the nation’s state banks. These institutions are already grappling with reduced profitability and a growing number of bad loans, a consequence of being enlisted to provide cheap credit to support the economy. Bankers are reportedly concerned about the potential for these new advances to turn bad and are seeking assurances from regulators.

It is estimated that local government-related entities owe an astounding CNY 10 trillion ($1.4 trillion), a sum equivalent to 7% of China’s GDP last year. This new policy is not just a financial manoeuvre; it is a critical effort to stabilise the economy, support the private sector, and uphold the credibility of the government’s financial commitments. The success of this long-term initiative will be a key indicator of China’s economic resilience.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 09/09/2025.

U.S. job market cools

Guy Foster, Chief Strategist, discusses seasonal weakness in equity performance and whether the adage “sell in May and go away, come back on St Leger’s Day” still holds true. Plus, our Head of Market Analysis, Janet Mui, analyses fresh U.S. jobs data.

Key highlights

Bonds rally: Bond yields rose following record levels of borrowing in the U.S. and Europe.

French government collapse: Prime Minister François Bayrou lost a confidence vote on Monday after his government failed to achieve sufficient support from the legislative chamber to pass a restorative budget. President Emmanuel Macron is likely to appoint a new prime minister.

U.S. jobs growth slows: : The U.S. saw just 22,000 new jobs created in August, a significant decline from the previous month. However, the slowing jobs market bolsters the case for an interest rate cut.

Seasonal weakness – will it manifest?

An old investor’s adage used to be “Sell in May and go away, come back on St Leger’s Day” (an annual horse racing fixture that falls in mid-September), as the summer months would be among the weakest for the equity market.

It was true that, on average, performance tended to be weaker during those months – though capitalising on that was difficult because, as another idiom runs: “a six-foot man can still drown crossing a river that’s five feet deep on average” – a reminder to not underestimate risk.

In any given month of any given summer, there’s a chance that seasonal weakness might not manifest, which has proven to be the case. Over the last five years, global equities have risen each month from May to August, while September has stood out as the worst month of the year for equity returns. This shows how easily investors can tie themselves in knots trying to take advantage of seasonal trends, particularly if you can’t explain why seasonal moves occur.

Source: LSEG Datastream

Seasonal weakness in September isn’t just limited to equities; bonds have been suffering from it too. As a result, there have been fears of a debt crisis this year – a situation in which investors are reluctant to lend because they think borrowers are overly stretched.

The explanation for this seasonal weakness is that during the summer when liquidity and investor attendance are low, companies tend not to try and borrow money in the bond market. Instead, they hold their borrowing back and try to fill it in September when there are plenty of investors around to meet it.

This year was a good example of that. The first day back after the Labor Day holiday in the U.S. (which this year fell on 2 September) tends to mark the reopening of the debt markets. This year, Europe and the U.S. experienced their largest and third-largest day of borrowing ever, respectively.

Bonds rally

Once this wave of new borrowing was digested, bonds rallied over the rest of the week. It’s because demand for bonds has been so high that many corporate issuers are taking advantage of the relatively tight credit spreads.

In the UK, rising bond yields are incorporated into the Office for Budget Responsibility’s models, and increase the assumed cost of borrowing. This makes compliance with Chancellor Rachel Reeves’s fiscal rules more difficult and increases the need for spending restraint and, more critically, tax increases in the forthcoming Autumn Budget.

This year, the Autumn Budget will take place on 26 November, which is relatively late. This is presumably because it will allow more time for inflation to subside along with borrowing costs, which would reduce the pressure for tax increases.

Meanwhile, French Prime Minister François Bayrou’s government collapsed after the prime minister lost a confidence vote on Monday. The ousting comes after the government failed to achieve sufficient support from the legislative chamber to pass a restorative budget. President Emmanuel Macron is likely to appoint a new prime minister, and the process will need to start again.

U.S. jobs growth slows

Like France and the United Kingdom, the U.S. also has an unsustainable budget deficit. But the latest set of employment data out of the U.S. provided further evidence that the jobs market is slowing and bolstered the case for an interest rate cut.

Source: LSEG Datastream

In addition to slower jobs growth, the average working week shortened, and hourly earnings slowed. That might seem bad news from a growth perspective, but lower interest rates are still considered good news for equity and bond investors alike.

Jobs growth slowed from 79,000 in July to just 22,000 in August, a mere month after President Donald Trump fired the previous head of the Bureau of Labour Statistics (which compiles the figures).

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below article received from EPIC Investment Partners this afternoon, which provides a global market update for your perusal.

“If you see a dam leaking, do not wait for it to burst,” goes an old engineer’s maxim. In financial markets, policy uncertainty often begins as a trickle such as minor skirmishes over tariffs or election rhetoric. But it can quickly flood asset prices. Recent research from the European Central Bank highlights how measures of economic policy uncertainty (EPU), drawn from news sentiment, spiked this spring following the US tariff announcement back in April. Yet volatility in both equities and bonds only rose sharply once that uncertainty fed through to weak equity market momentum.

This disconnect between policy noise and market choppiness is not new. Studies have documented long stretches (such as after the 2016 US election or during the energy crisis) when EPU surged but volatility stayed muted. ECB authors show that in Germany, EPU rose steadily into early 2025, driven by domestic fiscal questions and global trade tensions, yet equity‐market volatility diverged until the sudden sell‐off in April realigned the two. Additional academic work suggests that strong prior equity gains lull investors into complacency, suppressing implied volatility even as policy risk mounts.

Today, with autumn under way, policy uncertainty remains elevated on both sides of the Atlantic, from looming US elections to fractious EU budget talks. Yet headline VIX and VSTOXX readings trade near multi‐month lows, suggesting another potential mismatch. The danger is that a fresh shock arising from a market comment by a central bank governor or a sudden credit‐rating downgrade could trigger volatility clustering, where initial jitters cascade across asset classes.

For advisers, the lesson is twofold. First, recognise that EPU indices and realised volatility often co‐move only when equity momentum fades. Monitoring both news‐based uncertainty measures and market breadth indicators can flag when the dam’s wall is weakening. Second, tilt portfolios towards assets with negative sensitivity to broad volatility spikes. Low‐beta equities, inflation‐linked bonds and select investment‐grade credit historically outperform during clustered sell‐offs. A modest allocation to defensive sectors such as utilities or consumer staples can also cushion portfolio drawdowns when policy noise turns into market turbulence.

Ultimately, markets adapt by repricing risk. The real flood comes when leaks become uncontrollable, and those who built windmills rather than walls long before, will weather the storm more easily.

Please check in again with us soon for further relevant content and market news.

Please see below, an article from Tatton Investment Management, analysing the key factors currently affecting global investment markets. Received this morning – 08/09/2025

Pause for thought

When traders return from their summer holidays, they reassess their outlooks, but while there’s no shortage in narratives, stocks moved very little last week.

Long-term bond yields continued rising on Monday and Tuesday – fuelling more panic about inflation and debt – but even they fell back into the weekend. The main driver of bond moves is real yields, which reflect growth expectations rather than inflation or credit risk, so it’s unclear what message the ‘bond vigilantes’ are sending. They might be demanding a higher term premium (the return investors demand for tying in for longer), as you might expect when the long-term bond supply is set to increase.

But this isn’t a panic signal. UK yields rose last autumn to similar derision, but quickly fell back. The US court ruling against Trump’s tariffs worsened the US debt outlook this week, but when 30-year treasury yields hit 5%, bond traders sensed a bargain regardless.

For stock markets, higher yields make equities less attractive – and investors were already worrying about high price-to-earnings valuations (mainly the US). But high valuations come from high expected profits, and US earnings are rebounding (as are Europe’s, covered below). If the economy grows, companies usually beat their earnings forecasts, so factoring in growth expectations makes valuations look more reasonable. Earnings have been the main driver of the recovery rally from ‘Liberation Day’ after all.

That long rally has paused, as investors weigh up mixed growth signals (Friday’s US jobs report was weaker than expected). Gold prices are rising, which could be about higher bond yields or lingering nerves. Higher gold prices are sometimes read as geopolitical stress, but we think it’s more a continuation of years-long momentum and uncertainty around risk assets.

That makes sense. Markets are trying to work out whether the US’ mixed-to-weak economy is bad because it hurts profits, or good because it means more rate cuts – benefitting small and mid-cap companies. We think it’s good that markets are pausing to reflect; it sets up for well-founded gains when the outlook clears.

August 2025 Asset Returns Review

August was a pretty flat month with low volatility: global stocks gained 0.4% and bonds 0.5% in sterling terms. It started with another US tariff deadline and brief sell-off, but Washington’s trade deals eased some concerns. Markets were also helped by expectations of Federal Reserve rate cuts, after weaker US jobs data and a dovish speech from Fed chair Powell. But US stocks still lost 0.1% in sterling terms, due to a weaker dollar.

UK and European stocks climbed 1.2% and 1.3% respectively, thanks to improved business sentiment and suggestions of a ceasefire in Ukraine. An improved earnings outlook should help European equity regain some lost momentum from earlier in the year. For the UK and France, stocks fell into the end of August after a sharp rise in 30-year government bond yields. We don’t think this is a debt or inflation panic – contrary to the media – as the main driving force was higher real yields (which reflect growth expectations).

Japan led the way, gaining 4.8% after stronger data and a US trade deal. Japan is still benefitting from long-term corporate improvements. China wasn’t far behind (+3.1%) and is comfortably the best performer year-to-date (+20.4%). The Chinese economy is still struggling, but investors are betting on a turnaround.

Low volatility would normally boost risk appetite, but markets fell flat instead. We see this as a liquidity story: there was a strong liquidity flow earlier in the summer – which made it easy to buy risk assets – but it’s tapering off. Much of this is related to the running down (and now building up) of the US Treasury General Account. Liquidity isn’t yet contracting but it might in September. Investors will need more economic growth to get excited about, if markets are to move higher.

European Earnings Update

UK and European stocks have outperformed the US in 2025 – but company earnings are still lagging. Looking at the Q2 earnings releases, JP Morgan found that Eurostoxx 50 companies’ EPS fell 2% year-on-year, while Eurostoxx 600 (which includes UK companies) EPS dropped 1%. Revenues were hit worse, reflecting the challenging economic environment.

Earnings did beat analysts’ expectations by 3% for both the narrow and broad indices, though. With tariffs and continued weakness in global manufacturing, last quarter was always going to be tough – and it wasn’t as bad as it might have been. Banks were the biggest source of earnings growth, while energy and automotives struggled.

With US earnings staying strong and Europe’s staying weak, the rotation of capital from US to European assets we have seen this year looks harder to justify. JP Morgan analysts think investors got ahead of themselves on European growth and are now realising it – hence why US markets have outperformed recently.

But European profits are better than expected and the sectoral breakdown (strong banks and weak energy prices) is a positive for growth. More importantly, 2026 earnings expectations have moved up – compared to a weakening of 2026 projections in the US.

US earnings strength is heavily concentrated in the biggest tech companies; other US companies have similar EPS performance to Europe’s. But US stocks have higher valuations. Higher valuations are fine if you expect earnings to outperform, but that’s no longer what the analysts are saying. That should mean European valuations catch up – which can only happen if stocks outperform. The earnings outlooks could change again of course (US companies have a habit of proving the doubters wrong) but the current outlook suggests improvement in Europe.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened?

Markets delivered a robust performance over the past 24 hours, fuelled by soft US labour data that bolstered expectations for a Federal Reserve rate cut this month. Weaker labour market signals, including a disappointing ADP private payrolls report of +54k (vs. +68k expected) and initial jobless claims hitting a 10-week high of 237k (vs. 230k expected), underscored concerns following last month’s unexpectedly poor jobs report. The August ISM Services Index rose to 52.0 (from 50.1 in July). Prices paid component dipped slightly from 69.9 to 69.2, signalling persistent cost pressures. This backdrop drove a bond rally, with the 2y Treasury yield dropping to an 11-month low and the 10-year yield falling to a 5-month low. The S&P 500 gained +0.83% and the Magnificent 7 gained +1.31% hitting record highs, led by Amazon’s +4.29% surge after news of its AI-powered workspace software testing.

Fed independence under scrutiny

The Federal Reserve’s independence took centre stage yesterday during Stephen Miran’s Senate confirmation hearing for the Fed’s Board of Governors. Miran emphasised, ‘If confirmed, I will act independently, as the Federal Reserve always does.’ Questioned about retaining his CEA Chair role while serving as Governor until January, he clarified he would resign from the CEA if nominated for a longer-term Fed position. Meanwhile, news of a US Justice Department investigation into Fed Governor Lisa Cook for alleged mortgage fraud added uncertainty, as markets await updates on her bid for a court order to block potential dismissal.

Europe steadies ahead of French confidence vote

Across the Atlantic, French markets steadied as fears over Monday’s National Assembly confidence vote subsided. With a defeat widely expected, investor concerns about prolonged instability eased. French OATs outperformed, with the 10-year yield dropping 5.0bps to 3.49%, narrowing the Franco-German spread to 77bps, a recent low. The STOXX 600 rose +0.61%, reflecting cautious optimism in European markets.

What does Brooks Macdonald think?

As markets ride the wave of Fed rate cut optimism, today’s US Payrolls report marks the start of a pivotal two-week period that could shape global markets for the rest of 2025. Expectations are for August nonfarm payrolls to slightly outperform July’s figures, with the unemployment rate holding at 4.2%. However, revisions to prior months’ data will be crucial after last month’s significant downward adjustments (+19k for May, +14k for June), the largest in over five years, which led to the ousting of BLS chief Erika McEntarfer. The presumptive nominee, E.J. Antoni, awaits Senate confirmation this month. With US CPI next Thursday and the FOMC decision the following Wednesday, the labour market’s trajectory and inflation data will be pivotal in guiding the Fed’s next moves.

Please check in again with us soon for further relevant content and market news.

Please see below the daily update article from EPIC Investment Partners, received this morning – 04/09/2025

Following a weaker than expected job openings report, the futures market increased the probability for a rate cut at this month’s FOMC meeting to 95%. The weak data supports the case for a rate cut, as it shows a softening labour market with a broad-based rise in layoffs across many sectors, including construction, manufacturing, and transportation, rising to the highest levels in a year. It aligns with the Fed Governor Waller’s comments that the central bank should implement multiple additional cuts in the coming months, given that he expects inflation to approach the central bank’s target within the next six to seven months.

In another signal of a slowing US economy, the Fed’s Beige Book, released yesterday, reported that economic activity was flat or declining across most of the country. This slowdown is largely attributed to households cutting back on spending as wages fail to keep pace with rising prices. The report noted that nearly every region is experiencing price increases, with tariffs being a significant driver of higher costs for businesses, which are in turn being passed on to consumers. Furthermore, the report highlights a softening labour market, with employment levels seeing little to no change in most districts and several regions reporting a reduction in immigrant workers. This data reinforces the argument for the Fed to ease monetary policy, indicating that the economy is cooling more than previously thought.

Bond yields rallied following the weaker jobs data and a subdued Beige Book, paring the losses experienced during the week’s bout of volatility. The recent sell-off had pushed yields on the 30-year Treasury to an attractive ~5% level, which has historically been a good entry point to secure long-term returns. The combination of these higher yields with the growing expectation of a more accommodative monetary policy creates an appealing environment for bond investors.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.