Interesting input from Russ Mould of A J Bell written on Thursday and received on Saturday lunch time (25/04/2020). I am conscious of the dates of articles as some of what we receive is out of date by the time we receive it!

Why markets have rebounded and what could happen next

Short-term viral implications for investors to ponder

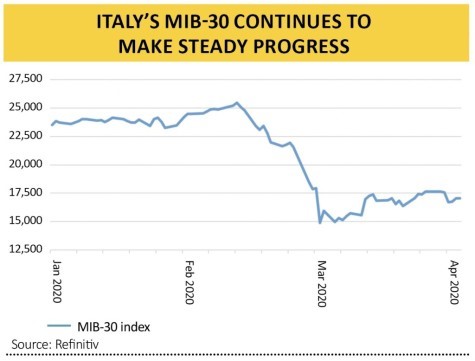

At the time of writing, Italy’s MIB-30 index is up by 15% from its 12 March low, a trend from which this column, looking at it solely from the narrow perspective of investments, can draw some modicum of encouragement.

It is impossible to be dispassionate about, or comfortable with, such matters, but the Milan market benchmark’s steady recovery reflects a peak in the number of new daily cases across Italy on 21 March at 6,155 and in the number of fatalities at 919 six days later.

At the time of writing the last reading for those numbers are 3,047 and 433 respectively and it is to be hoped that the trend remains down, for humanitarian reasons above all others.

As suggested here three weeks ago, this shows that equity markets are responding to changes in the curve of the coronavirus outbreak.

A slowdown in the number of cases was always going to be seen as good news, given how investors would interpret this as a sign that things were getting less bad, and that as a result the outbreak would eventually stop getting worse and once it stopped getting worse it would eventually start getting better.

This is where markets are now. The number of new cases is growing much more slowly, even if the aggregate number of those unlucky enough to catch the dreadful virus is still growing overall. This has been enough for equity markets to start pricing in what might happen if, as and when the government-imposed lockdowns are brought to an end and economic activity resumes.

As a result, several benchmarks are looking even sprightlier than that of Italy. The UK’s FTSE 100 is up 16% from its 23 March nadir of 4,994, while Germany’s DAX and America’s S&P 500 are back in bull-market territory, with gains of more than 20%.

The question now is whether these gains can be maintained or extended and in the short term a lot of that will depend upon the shape of the upturn. The latest Bank of America institutional investor sentiment survey suggests that U-shaped is the current favourite, over W, V, L, ‘bathtub’ or tick-shaped (or any other options that you could think of).

ALPHABET SOUP

What is interesting to note is how a V-shaped recovery is only third choice, according to that Bank of America monthly survey. This suggests some degree of circumspection among the professional investment community and it is easy to see why, as Spain, New Zealand and the UK, to name but three, extend their lockdowns and other nations such as Italy ease them at a very steady pace.

When it comes to judging what sort of recovery might ensue, investors can ask themselves the following questions:

1 When will I first want to use public transport?

2 When will I first want to eat in a restaurant or drink in a bar or pub?

3 When will I first want to board an aeroplane or cruise ship?

4 When will I first want to attend a public event at a cinema, theatre or sports stadium?

The answers could be informative. In addition, you can then imagine that you have been furloughed or even lost your job and see if the answers change at all. The assumption that all of those unlucky enough to find themselves in that position walk straight back into full-time employment could be an optimistic one as unfortunately some firms are going to fail, no matter how much support they receive from the government, management, staff and customers alike.

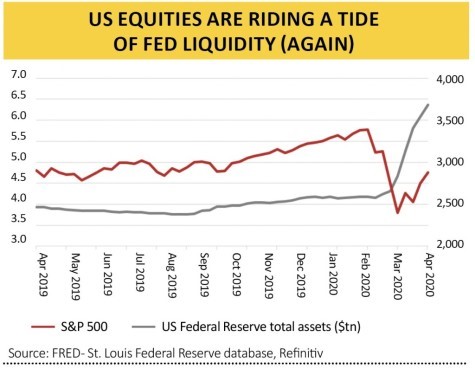

These questions are very difficult, if not impossible, to answer. As such, investing money on the back of them could prove a fraught exercise, even if markets do seem to have one very powerful ally in the form of central banks, notably the US Federal Reserve. The value of the assets held on the American central bank’s balance sheet has swollen by $2.2tn, or 53%, since the end of February.

That tidal wave of liquidity looks to be carrying US stocks higher. Students of history will however remember that the first round of quantitative easing that began in autumn 2008 had a similar initial effect, only for the S&P 500 to buckle in face of weak macroeconomic data and corporate earnings reports and only bottom five months later.

This column will revisit the issue of central bank intervention in an analysis of long-term potential implications of the coronavirus outbreak for financial markets next week. Before then there is one further short-term indicator of note: whether the FTSE 100 can reach (which it did very briefly on 20 April, only to fall back) and stay above 5,816, the high reached after the three-day rally that followed the low on 23 March.

If so, that could break the traditional ‘bear’ market pattern of a series of lower highs and lower lows and give investors real grounds for hope, at least from a portfolio point of view.

A J Bell offer products in the pension SIPP, SSAS and investment areas. They have a Stockbroker within their business too. Russ Mould is quite often heard commenting on Radio 4.

Steve Speed

27/04/2020