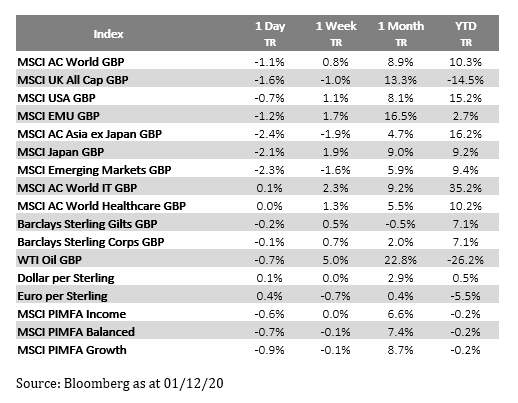

Please see below update received from Brooks Macdonald this morning. It explains where the markets stood by the end of November, as the world continues to wait for vital vaccine efficacy results in the fight against Covid-19.

What has happened

With yesterday’s close November capped off one of the best months of performance for global assets. The quid pro quo was weakness in safe havens such as the US dollar and gold, but sovereign bonds were remarkably resilient as monetary accommodation outweighed the changing vaccine winds.

OPEC+ delayed

The OPEC+ meeting that was planned for today has been pushed back to Thursday as members needed to have further discussions ahead of the summit. The main items on the agenda is whether or not to keep to a planned easing of supply cuts from the start of January. The oil price is walking a tightrope at the moment, with vaccine hopes for a faster recovery on one side, against continued COVID risks during the winter months on the other. As well as trying to judge the likely pace and scale of the nascent global economic recovery, OPEC+ members also have the challenge of keeping production discipline intact. Should OPEC+ members break ranks on production, this risks a lot more volatility for the oil price as well as uncertainty for the energy sensitive parts of the market.

COVID update

Whilst we didn’t, as expected, see any new vaccine efficacy results yesterday the incremental vaccine news continued. Moderna announced that it would request emergency authorisation from both the US and EU regulator and Novavax said that its UK study was expecting results soon. Meanwhile cases continue to fall in Europe with the UK seeeing its 7-day average move to early October levels and France seeing its lowest daily case rise since August. Of course, the UK partial lockdown is about to ease so there will be a knock-on impact on cases down the line, but this will all occur with a familiar lag. In the US we have seen cases continue to rise particularly in the original hot spot, New York, and the summer hot spot of California.

What does Brooks Macdonald think

Whilst November was an exceptionally strong month for equity returns the relative outperformance of cyclical equities over defensives was the main story. Selectivity remains key within the cyclical sectors as there are some areas, such as bricks and mortar retail, that have likely seen their decline accelerated by the pandemic. For others, such as airlines, it’s too early to say whether COVID-19 will cause a permanent reduction in business travel for example. This may prevent some sectors from rallying to their start of year levels for some time.

We will continue to publish relevant content and market updates as we enter the final month of a challenging year. Please check in again with us soon.

I’ve just cut and paste this from an article received from A J Bell yesterday, Sunday 29/11/2020. It’s a little late into the pandemic but I agree with most of the content.

1. Can you use other income sources to tide you over?

If you take taxable income from your pension, your annual allowance will reduce from £40,000 to just £4,000 (the ‘money purchase annual allowance’ or MPAA). This is one of the main reasons why you might avoid taking taxable income from your retirement pot. If you have money saved in an ISA, for example, you could consider taking this out tax-free, while also keeping your full pensions allowance intact.

2. Take your tax-free cash first

Note that the MPAA only kicks in if you take taxable income from your pension pot. So if you have no other options open to you, taking only your tax-free cash will at least leave you more flexibility to rebuild your retirement fund later on.

3. Do you have a plan?

If you have been forced to access your pension early – or are planning to in the coming months – spend some time thinking about how you can rebuild your fund once your income bounces back. It might be that you need to pay more in as a result to get back on track, or consider working a bit longer. But whatever you do, don’t stick your head in the sand.

4. Sustainability is the key

For those who have already stopped working and are taking a retirement income via drawdown, it is vital to review withdrawals regularly to make sure they remain sustainable. These reviews should happen at least annually, and you should be prepared to potentially reduce your income if your investments suffer significant short-term falls (as we saw in March and April).

5. Consider a ‘natural income’ route

A ‘natural income’ retirement strategy involves living off the dividends your investments produce, thereby preserving the capital value of your underlying fund, allowing it more time to grow. While a natural income strategy has been particularly difficult in 2020 as swathes of companies have cut dividends, positive vaccine news could mean it is more viable in 2021 and beyond.

Summary

I struggle with the last point on a ‘natural income.’ If this were for your main source of income, you would have to be able to manage significant variation in income yields, particularly at the moment. This would work for a secondary income, a top up income from, for example, a Stocks & Shares ISA portfolio.

From my point of view, I advise all clients to build at least three different assets to help manage risk and aid tax efficiency in retirement; cash deposits, Stocks & Shares ISA portfolios and pension funds.

If markets drop as they did in March and your pension fund values follow, you can then switch your Drawdown pension income off, start to draw on your cash deposits to cover living costs and wait for the market to recover. This will help you protect your pension assets for the long term. As the markets recover, you can start your Drawdown pension income, perhaps at a lower level initially.

When markets fully recover, you can use your Stocks & Shares ISAs to top up your cash deposits. Your Stocks & Shares ISAs and pension funds remain invested and recover in value so that you are fully prepared for the next shock to markets – hopefully, a good long time away.

Any guaranteed income you have, for example State Pensions, will help through volatile periods.

Please see below commentary received from AJ Bell this morning which highlights key points for investors on the Chancellor’s spending review.

After postponing the Budget earlier this year, and with public sector borrowing at a peacetime high, Chancellor Rishi Sunak’s spending review was keenly awaited.

While the health emergency is not yet over, despite over £280 billion of spending on health and employment measures, ‘the economic emergency has just begun’ according to the Chancellor.

UK output is expected to shrink by 11% this year, the most in history, with next year forecast to see a rebound of 5.5%, and by 2025 the economy will be 3% smaller than estimated pre-pandemic.

Sunak promised another £18 billion to help the NHS fight the virus, along with £30 billion in extended furlough payments, restart programmes, local council grants and rail subsidies, to help firms in hospitality, staffing and travel.

Also, as part of a ‘once-in-a-generation’ £100 billion infrastructure plan, there is a big increase in spending on public services, building new schools and hospitals, hiring more nurses, recruiting more police officers and building more prisons, which will benefit the outsourcing sector.

Spending on roads and other transport schemes to ‘level up’ the regions is good news for infrastructure firms, while on top of Help to Buy, which is estimated to be worth £12 billion, there is a new £7 billion national housebuilding scheme and planning regulations will be eased, all of which will be music to the ears of the housebuilders.

The UK economy requires continuous support from Government in order to recover from the effects of the pandemic. Please check in again with us soon for further interesting and relevant content based on world-wide events.

Please see below the latest ‘Markets in a Minute’ update from Brewin Dolphin – received last night – 24/11/2020.

Brewin Dolphin – Markets in a Minute

Equity markets have been mixed over the past week as positive sentiment surrounding vaccine news gave way to worries about the near-term economic impact of the pandemic and associated lockdowns.

Brexit news has also been mixed, with reports of progress countered by reiterations of sticking points around fishing and state aid. There is a deadline of this week to strike a deal but it may well be pushed back. In the US, President-elect Biden has now been given the go-ahead to begin the transition process, as President Trump’s legal efforts to get the election result overturned all appear to be failing.

Last week’s markets performance*

FTSE100: +0.55%

S&P500: -0.77%

Dow: -0.73%

Nasdaq: +0.21%

Dax: +0.46%

Hang Seng: +1.12%

Shanghai Composite: +2.04%

Nikkei: +0.55%

*Data for week to close of business on Friday 20 November.

Stocks rally at start of week

Global markets largely rose yesterday after more positive vaccine news, although stocks were mixed in the UK thanks in part to a stronger pound. The FTSE100 closed down 0.28% at 6,333.84 as the pound rose on Brexit hopes, while the more domestically focused FTSE250 rose by 0.39% to 19,582.35. Sterling gained 0.17% against the dollar, rising to $1.3298, and by 0.37% against the euro to €1.1242.

In Europe, shares were up in early trade but faded towards the close, with the pan-European Stoxx 600 closing down 0.2% and the Cac-40 closing 0.08% lower. In the US, the tech-heavy Nasdaq closed up by 0.22% but the more ‘old economy’ Dow gained 1.12%.

Overall trends in the markets showed a continued outperformance of stocks that are expected to benefit from life returning to normal, such as energy, financial stocks and industrial companies, while the tech sector lagged, since it has benefitted so much from the lockdowns.

Economic data shows slowdown in UK, eurozone

Closely watched surveys of business activity suggested the UK was slowing rapidly in November while the US was performing better. The flash Purchasing Managers’ Index for the UK services sector, which covers leisure and hospitality, fell to a reading of 45.8 in November, its lowest for six months, as the second lockdown took hold. Any reading below 50 suggests business activity is falling compared to the previous month.

The manufacturing sector index was stronger, rising to 55.2 from October’s 53.7, as many firms build up stock ahead of the Brexit deadline.

However, the eurozone saw an even worse reading on its services sector, which hit a level of 41.3, lower than expected due to the severe lockdowns imposed across the continent which has forced the closure of so much of its services economy.

The near-term outlook is likely to remain weak but the stock market may look beyond the short-term data and focus on the vaccine news, which looks increasingly likely to bring a sense of normality back next year.

Source: Refinitiv Datastream, Brewin Dolphin Nov 2020

Vaccine upside

The better news for the pound is the continued positive vaccine news. Last Monday we had confirmation that both mRNA-based vaccines (Pfizer and Moderna) have similarly high levels of efficacy of 94%-95%. Some more details from Pfizer and BioNTech later in the week provided further encouragement in that the jab shows 94% efficacy in those aged 65 and over.

The Oxford/AstraZeneca team yesterday announced initial findings that showed it prevented an average of 70% of infections. Given the very high bar set by the two mRNA vaccines, it might be natural to feel a little disappointed at the 70% efficacy level, but it is important to note that a smaller cohort of the trial produced results showing 90% efficacy if the vaccine was administered as a half dose, followed by a full dose a month later. AstraZeneca also indicated that the two-dose regime was successful in preventing asymptomatic infections, although this needs to be validated with more results.

AstraZeneca is now looking to adjust its phase three trials that are still under way to incorporate these different dosing regimes, and hopefully prove a higher efficacy rate.

If its efficacy can be improved through the dosage techniques, then it can be a very positive addition to the two mRNA vaccines. Unlike the Pfizer and Moderna jabs, which have to be stored in ultra-cold conditions, the AstraZeneca jab can be kept in a normal fridge and is far cheaper than the two other vaccinations. The trial data has been welcomed by medical experts, who remind us that many were expecting an efficacy rate of around 50%-60% for the first round of vaccinations. All have exceeded these expectations.

Brexit latest

Although there is supposed to be a deal done by this week, as with most EU deadlines, this seems to be a rolling one. Back in June, a deal had to be done by the summer, then it had to be done by mid-October to allow time for the treaty to be translated into all the bloc’s official languages and scrutinized by the European Parliament. Now Michel Barnier is understood to be briefing that it could even get done with an agreement being reached in December. The anticipated date for a European Parliament rubber stamping vote is 16th December but nobody will be surprised if it drifts to just before New Year.

If a deal is not reached by the 1st January then the UK and EU will trade on WTO terms. That would mean tariffs, quotas and an effective border with the EU. The UK has granted an exemption to incoming goods during the first half of 2021 so incoming goods should suffer less disruption, but the EU has not reciprocated.

The two sides are still trying to bridge their differences over fishing, the level playing field for businesses and the governance of a potential trade agreement. Because of its size, the EU has the leverage. It wouldn’t be surprising to see Boris offer up a last-minute concession, with the EU granting a smaller concession that allows him to spin it up into a win.

This week’s article from Brewin Dolphin focuses on the economic data that is starting to show a slowdown in business activity across the UK and eurozone, with updates on the market reaction to more positive vaccine news and the latest news on Brexit.

Please continue to check back for our regular blog posts and updates.

Please see below article received from Legal & General yesterday afternoon, which provides a market insight from the Head of their Asset Allocation team.

The mood swings, finally

Over the past week, after the election and vaccine news, investors’ animal spirits seem to have emerged at last. The AAII Bull/Bear spread, one of the indicators we rate most highly, jumped to its most bullish reading in nearly three years and one of the highest since the financial crisis. Recent fund-manager surveys from BAML, Strategas and ISI showed a similar surge in investor optimism.

To cap things off, the first sell-side outlooks for 2021 have also been more optimistic than both the historical average and last year’s ‘mid-single-digit upside’ consensus. The average S&P 500 target for end-2021 from Goldman Sachs, Morgan Stanley and Credit Suisse suggests 15% upside from here.

But despite the notable spike in investor bullishness, our own indicators are not sending contrarian sell signals yet. Our interpretation is that sentiment has simply become a headwind, rather than so excessively bullish that it starts to dominate our thinking about equity risk. Even at the latest reading of 31% net bulls in the AAII survey, for example, the average return over the following 12 months has been +6.3%, not far below the average return in any 12-month window. Historically, only readings above 40% net bulls have been significant sell signals.

Holding onto the barbell

We have been running a barbell strategy within equities since the spring. On the one side, our highest-conviction long is one of the most loved parts of the market, the secular growth story in tech. On the other side, we also like some of the least loved deep value and recovery plays in the form of telecoms, travel and leisure, and cyclicals.

European telecoms easily meet the deep value criteria with attractive relative valuations compared with history and regularly score as one of the least popular parts of the equity market. But a deep value case only has merit if there is a potential catalyst on the horizon. We see this in the likelihood of the sector benefitting somewhat from greater regulatory leniency and possibly some modest pricing-power gains in a post-pandemic environment. From a multi-asset perspective, telecoms also offer us some diversification with low correlation to broader equities and a low beta in equity drawdowns.

‘Cyclicals versus defensives’ is an obvious play on a strengthening economic cycle. Having recovered a lot of the pandemic losses since the spring, we see no overshoot against the improving macro data yet. With sentiment for cyclical sectors also remaining less optimistic than for defensive sectors, we expect this trade to have more room to run in the remainder of the economic rebound.

Value stocks and the travel and leisure sector both score well on sentiment (the consensus on them is bearish) and should both benefit particularly from the next phase of the economic re-opening dynamics. With the vaccine announcements behind us, we still expect generally positive macro news flow with a restart of travel activities and pent-up demand.

Calmer waters for a while

The New Political Paradigm (NPP) has been one of our medium-term themes as a framework for thinking about the market impact of gradually growing populist pressures.

As with so many things, the pandemic has accelerated the underlying trends of the NPP. The jump in food inflation does not affect everyone the same way. Job losses have been most severe among the lowest-earning groups, for multiple reasons. School closures have widened the education gap between students from different economic backgrounds. The Edelman Trust Barometer at the start of the year showed a significant gap in optimism about the future in different parts of developed markets’ populations before the pandemic hit. That gap is likely to be wider now.

The US election, however, should help keep some of the most market-moving elements of the NPP policy mix off the agenda for the time being. A Biden presidency should provide a calmer style in the US approach to China and trade policy in general, even if there is little change in substance. And with a divided congress, an aggressive change in fiscal policy (e.g. to modern monetary theory, universal basic income, or Medicare for All) has become all but impossible.

So overall, the NPP will likely be quiet for a while, but our expectation is that the underlying trends that gave rise to populism stay in place and become market drivers again in the years ahead. In the meantime, our mantra remains ‘don’t predict, prepare’.

We will continue to publish up to date content sourced from a wide variety of investment experts. Please check in again with us soon.

Please see below weekly news update received from Blackfinch Group this morning. The commentary provides a summary of global events and their effects on the markets.

UK COMMENTARY

Prime Minister Boris Johnson was forced to self-isolate after coming in to contact with a Tory MP who later developed COVID-19 symptoms

UK inflation rose more than expected to 0.7%, driven by higher prices in clothing and furniture, and partially offset by lower prices in recreation, culture and transport

The Government announced its intention to ban the sale of new cars and vans powered only by petrol or diesel by 2030. It will invest £2.8bn to help build out of UK countries’ charging point infrastructure and the development of long-lasting batteries.

A Confederation of British Industry (CBI) manufacturing survey showed that manufacturing orders fell at a faster pace in November than in October. The total orders balance fell to -40 from -34. The CBI calculated the figure by subtracting the percentage of respondents reporting a fall in orders from those reporting a rise.

The Office for National Statistics (ONS) reported that 14% of UK businesses said they had low or no confidence that their business would survive the next three months

The ONS also reported that UK retail sales volumes increased in October by 1.2% from September’s number, the sixth consecutive month of growth for the sector

US COMMENTARY

Retail sales data for October came in slightly lower than expected at 0.3% growth, the slowest pace of expansion since April

Initial jobless claims rose to 742,000 last week, above economist expectations of 707,000

Treasury Secretary Steve Mnuchin and Federal Reserve Chairman Jerome Powell have so far failed to agree on extending the SME emergency loans package beyond the end of 2020

ASIA COMMENTARY

More than 15 countries in the region signed the world’s largest trade alliance, the Regional Comprehensive Economic Partnership. Having supposedly taken eight years to finalise, it marks the first single trade agreement involving China, Japan and South Korea. The intention is to gradually reduce tariffs across many areas.

Japan’s economy showed growth of 5% in the third quarter of the year, bouncing back stronger than expected

COVID-19 COMMENTARY

Moderna Inc announced that its COVID-19 vaccine was effective at immunising against coronavirus in 94.5% of cases. The results compare favourably to Pfizer’s results. As an added benefit Moderna’s vaccine won’t require the same heavy-duty freezing in transit.

The UK has signed a deal worth US$125mn to secure 5mn doses of Moderna’s vaccine, due for delivery in spring 2021. The deal will allow 2.5mn people to be vaccinated, with each vaccine requiring two doses.

The Oxford University and Astrazeneca vaccine also shows encouraging immune responses in the older population. However these results stem from a phase II clinical trial, whereas both Moderna and Pfizer have already taken part in phase III trials.

We will continue to publish relevant content and market updates as we enter the final month of an eventful year. Please check in again with us soon.

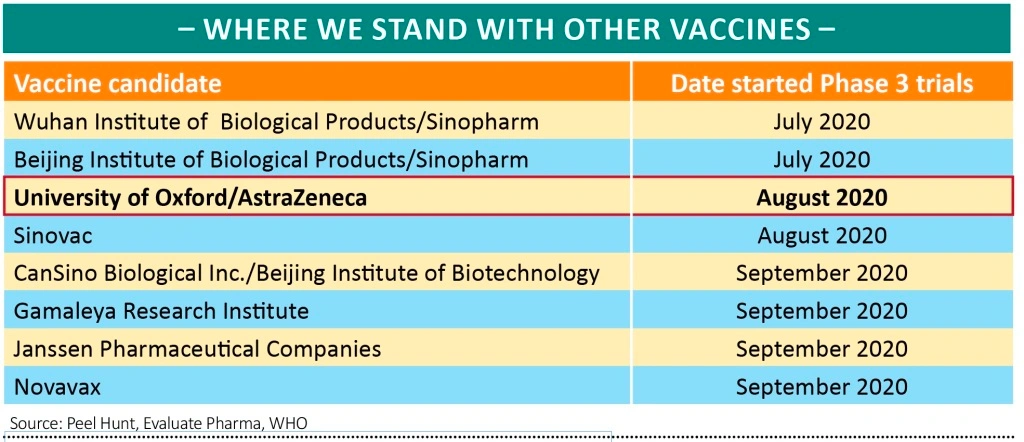

The revelation from US pharmaceutical company Moderna that its vaccine was 94.5% effective in treating coronavirus, with no significant safety concerns, sent global stock markets up between 1% and 2% on 16 November.

This compares with a bump of around 5% in response to the positive update from Pfizer and BioNTech a week earlier and suggests there may be diminishing returns from further vaccine news – with the table showing some of the main other candidates, several of which are centred in China.

The most meaningful will probably come from Astrazeneca (AZN) which is due to report on its vaccine, being developed together with the University of Oxford, in the next month.

According to Adam Barker, analyst at Shore Capital, AstraZeneca’s treatment ‘doesn’t have to hit a 90%+ efficacy bar to still be useful, and it remains the most stable of all the candidates at refrigerated temperatures’.

The market winners and losers were much the same on the Moderna news as the earlier vaccine catalyst, with hotels and airlines racking up large gains and previous lockdown ‘winners’ including online retailers suffering losses, albeit the moves were not as spectacular.

Moderna claimed preliminary analysis of its late-stage trials involving more than 30,000 volunteers showed the vaccine prevented the most serious cases of infection, with no severe cases at all among those who received it. ‘That for me is a game-changer’, said Moderna chief executive Stephane Bancel. Moderna shares initially soared 12% on the news.

Like the Pfizer/BioNTech vaccine, which claims to be more than 90% effective, the Moderna treatment uses mRNA technology designed to turn the body’s own cells into vaccine ‘factories’, creating copies of the virus’s ‘spike protein’ which in turn stimulates the production of antibodies. Both firms have struck significant supply deals with the US government.

While the results are preliminary and the technology has yet to be approved, both firms are expected to ask the US Food and Drug Administration for emergency-use authorisation dependant on follow-up safety data later this month.

Crucially, while the Pfizer/BioNTech vaccine has to be stored at ultra-low temperatures of -60 to -80 degrees Celsius until a few days before use, the Moderna vaccine is stable at normal refrigerator temperatures of -2 to -8 Celsius and can be kept for up to 30 days or can be frozen if needed. This gives it a significant advantage in terms of ease of distribution.

A good update from AJ Bell with some more positive vaccine news this week, this is another step in the right direction.

Please continue to check back for our latest blog posts and updates.

Please see below market update received from Brooks Macdonald this afternoon, which makes reference to ongoing Brexit negotiations and Pfizer’s upgraded vaccine efficiency rating.

What has happened

The hangover from Monday’s market exuberance continued as rising US restrictions offset positive Pfizer news. The US closed down over 1% with technology marginally outperforming in line with previous COVID centric sell-offs.

Latest on the virus

Positively, the Pfizer efficacy rate was upgraded to 95% but more importantly the efficacy rate for those older than 65 is 94%. Given the over 65s are those most at risk of serious COVID complications it is undoubtedly the most important age group to defend through a vaccine. This was not enough to distract markets from the US new case growth which continues to rise. In New York City schools will now close as the city’s positivity rate of first time COVID tests is above 3%, the threshold previously set. Colorado has urged residents to not travel around Thanksgiving and Minnesota has closed gyms, restaurants and bars. In Europe, numbers are showing signs of plateauing in some regions but France, one of the worst effected countries, looks likely to extend its lockdown due to end at the start of December. The main concern for markets is that relatively heavy restrictions (but ones that stop short of the actions in March/April) only seem to stabilise new cases rather than see them drop significantly. With winter coming this likely heralds an era of tougher restrictions interspersed with periods of loosening rather than the other way around.

EU Summit today

There was hope last week that today’s EU Leaders Summit may discuss a draft Brexit deal, but this has now been rolled into yet another week. On the agenda however will be the tough topics on the EU’s long-term budget and the recovery fund. We were reminded over the late summer that these topics weren’t exactly sorted when the vague ‘rule of law’ requirements led to a spat between some of the fiscal blocs within the EU. Indeed only this week, Hungary and Poland used their veto over conditions that would link access to budget funds to ‘adherence’ to the rule of law. Today’s meeting could therefore be a source of headlines even without a Brexit deal to deliberate.

What does Brooks Macdonald think

Whilst Brexit might not be on the agenda today, Sterling did falter overnight as the Times reported that EU leaders are asking the Commission to publish their no-deal contingency plans ahead of year end so businesses could prepare for that scenario. There is plenty of noise out there and expect some comments post today’s summit from the EU on the state of the talks but given the backlash against the hard line taken at the last meeting, expect calmer words this time.

We will provide further market analysis as the UK approaches its final week of Lockdown 2.0. Please check in again with us soon.

Please see below blog received from Legal & General yesterday afternoon. We have followed the markets’ reaction to both negative Covid-19 statistics and positive vaccine news. This commentary focuses on the effects of British and US politics on investments.

Cummings and goings

Last week, Downing Street’s internal soap opera spilled into the public domain. With the departure of Lee Cain and more importantly Dominic Cummings, two key advisers to Boris Johnson who were instrumental in the Vote Leave campaign, there are now questions about the future direction of policy.

In particular, there is speculation that the government may need to make significant compromises to get a Brexit deal over the line in the coming few weeks. Clearly progress has been made in some areas but, as both sides willingly admit, significant differences remain on some seemingly intractable issues such as fishing rights, the level playing field, and governance.

Another factor is the interaction between the UK and the new US President-elect. Joe Biden made clear his concerns that the (recently defeated) Internal Market Bill could undermine the Good Friday Agreement. But to what extent could this influence negotiations with the EU?

One line of reasoning is that the UK may need to compromise with the EU if it looks as though a transatlantic trade deal will be less of a priority to a Biden administration. But, regardless of the occupant of the White House, it was never likely that a deal with the US would be straightforward. It is therefore unclear whether the change in US government will have a material influence on the UK’s negotiating stance.

The market consensus is that a last-minute deal can be reached. Given the importance to our sterling-denominated long-only funds (where any unhedged foreign-asset exposure results in a short sterling position), we continue to watch developments closely.

Tick, tock tech?

The positive vaccine news last week was like a shot in the arm to much of the equity market. Not so for the tech sector, however, which has performed strongly through the lockdowns. Yet while a vaccine – hot on the heels of Biden’s election victory – may bring about some market normalisation and appear to dampen the relative attractiveness of tech in the short term, the structural trends that have been the backbone of our longstanding tech position look set to continue, in our view.

Despite the rally this year, valuation is not a large concern for us. Tech stocks do trade at a premium to the market, but the sector’s outperformance has been driven by superior earnings growth rather than any re-rating, a big difference compared with the 1990s tech bubble.

And while Biden and the Democrats may be regarded as a headwind for tech, governing with a (likely) split Congress probably means a continuation of the status quo and very little policy that could significantly move markets. There will likely be an acceleration of antitrust investigations into big tech, but so far such investigations have delivered somewhat toothless conclusions.

Biden did not show a particular passion for tech regulation either before or during the campaign, and centrist appointments to his government would signal a more market-friendly approach than some feared earlier in the year (the decision to select Kamala Harris instead of, for example, Elizabeth Warren as vice president is a prime example).

Furthermore, over the medium term the US has little incentive to over-regulate domestic companies given tech’s importance in the broader geopolitical rivalry with China.

The tech selloff early last week thus gave us an opportunity to top up our overweight in the sector, but we remain alive to the concentration risk this position carries. Within portfolios we continue to balance this risk with positions in some of the least-loved corners of the equity universe, such as European travel and leisure.

This time is different?

Back in April (which feels like a lifetime ago), we downgraded our medium-term duration view to underweight. With the post-election/vaccine selloff, we have taken the first steps to moving that view back towards neutral.

Taking the Federal Reserve’s (Fed) ‘dot plot’ at face value implies that rates will be on hold until the end of 2023. From that point forward, if we assume a similar hiking cycle to the last one (i.e. once per quarter), we get to an average Fed funds rate of 0.5% over the next five years. The last cycle was admittedly slower than previous iterations, but given the Fed’s recent switch to average inflation targeting and its repeatedly quoted ambition to wait until inflation is above target on a sustained basis before tightening policy, there is an increased chance that the central bank will again hike gradually, all else equal.

Further along the curve, the difference between 10-year and five-year yields (also around 0.5% currently) is in line with the average of the past five decades. It follows that, with the front five years of the yield curve in line with the dot plot and the slope of the next five years back to ‘normal’, a neutral view is consistent with a 10-year treasury yield of 1%, a level that it is gradually approaching.

One key risk is that the curve steepens further on ‘crowding out’ or supply concerns in the event of another big fiscal package. That has become less likely since the US election (notwithstanding the runoff for Georgia’s senate seats), although the current COVID-19 wave in the US could focus minds on Capitol Hill.

Even if we do see a stimulus package between now and the end of the first quarter of 2021, it feels as though $1 trillion is the tipping point between a positive and negative surprise on this front.

As we move into the final weeks of what has been an eventful year, we will continue to publish up to date market analysis and relevant content. Please check in again with us soon.

• UK gross domestic product (GDP) rose by 15.5% in the third quarter, the fastest increase on record. However, the pace of growth is noticeably slowing, with an expansion of just 1.1% in September, following increases of 6.3% in July and 2.2% in August.

• The National Institute of Economic and Social Research predicts that the UK economy will shrink around 2.2% in the last quarter of the year. It estimates that growth will drop to 0.3% in October, and contract by 12% in November, before rebounding in December. This is if the current lockdown ends on 2nd December as planned.

• The UK jobs market data was weaker than expected, with the unemployment rate reaching 4.8% in October

• In the third quarter redundancies reached a record high of 314,000, an increase of 181,000 on the previous quarter

• Total retail sales increased 4.9% in the four weeks to October 31st against a decline of 0.3% in the same period the previous year

• UK ministers put the finishing touches to the National Security and Investment Bill. This increases their ability to block takeovers by foreign companies on national security grounds.

US COMMENTARY

• Joe Biden’s election victory over Donald Trump was all but confirmed. However, Trump has shown no signs of conceding, so question marks remain over how smooth the transition may be.

• The Republican party retains control of the Senate, which will no doubt hamper Biden’s ability to enact all of his election promises

• Initial jobless claims fell to 703,000 last week, the lowest amount since March

EUROPE COMMENTARY

• Eurozone GDP rose 12.6% in the third quarter according to the second estimate of the quarterly economic data. There was a slight downwards revision to the initial estimate of 12.7%. On an annual basis this means that GDP fell 4.4%.

COVID-19 COMMENTARY

• The vaccine in development by Pfizer and BioNTech successfully prevented more than 90% of candidates from contracting COVID-19 in a preliminary test of 43,500 people. The companies have confirmed that they would be able to supply 50 million doses by the end of the year and around 1.3 billion in 2021. Each administered vaccine would require two doses.

Another quick update from Blackfinch, these updates are a good way of keeping up to speed with developments in the markets.

Please continue to check back for our latest blog posts and updates.

{kind=link}