Please find below a ‘Markets in a Minute’ update, received from Brewin Dolphin, yesterday evening – 07/12/2021

The S&P 500 has surged over the past 20 months. Could the spread of the Omicron variant spark the first correction of the bull market? Paul Danis, our Head of Asset Allocation, provides context and discusses the outlook.

Last Friday saw a sell off in higher risk asset classes when the Omicron variant of Covid-19 suddenly landed on everyone’s radars. The news was poorly received as many investors had become quite relaxed about the virus. The S&P 500 fell 2.3% – its biggest one-day loss in nine months – while the pan-European STOXX 600 slumped 3.7% in its worst session since June 2020.

Economic growth-sensitive plays like small caps underperformed. At the industry level, it was the travel[1]sensitive airline, hotel, restaurant and leisure sectors, oil-sensitive energy plays, and yield-sensitive banks that were among the worst hit.

Where do we stand now after the Omicron[1]induced sell off?

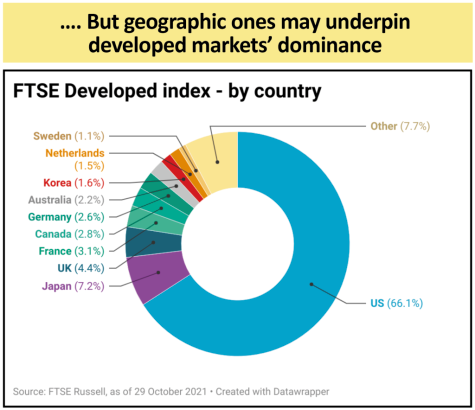

Notwithstanding Friday’s selloff, global equity markets have surged over the past 20 months, led by the US. As of the end of November, the MSCI All Country World Index is up 89% (in US dollar terms) from the March 2020 low. The US large cap benchmark, the S&P 500, is up 104%. We focus on the S&P 500 in this article because it represents over 60% of the global equity market cap, it acts as a bellwether for equity bourses around the world, and US equities constitute our largest overweight position.

Although there have been several US equity bull markets that have seen much greater total price appreciation than what has occurred so far this cycle, what has made this cycle’s bull market stand out is the intensity of the rally. This cycle, the S&P 500’s annualised performance since the bull market began is just over 62%. Looking at all the bull markets where the total gain has been at least 100%, one must go back to the early 1940s to find rallies that have been as intense.

What’s more, we have now gone much longer than the average length of time without seeing a 10% correction in the S&P 500. Since the late 1920s, the average time between the start of a bull market and an S&P 500 decline of 10% or more is about a year and two months. This cycle, we’ve gone about a year and eight months without a 10% correction. The worst we’ve had was a 9.6% decline in September last year, and a milder 5.5% pullback in September this year.

Is Omicron enough to spark the first 10% correction of the bull market?

It’s possible. How much downside we get will be determined by what the data show in terms of Omicron’s ability to evade vaccines and natural immunity, as well how dangerous it is. The good news is that a lot of work has already been done to find solutions to Covid-19. As such, if it turns out that Omicron poses a new serious challenge, the world is in a better place now to address it.

Preparing new vaccines is not trivial, but it would be a shorter and more certain process than the development of the original vaccines. Furthermore, we also have some effective treatments for Covid-19. These are not expected to be impaired by the new variant.

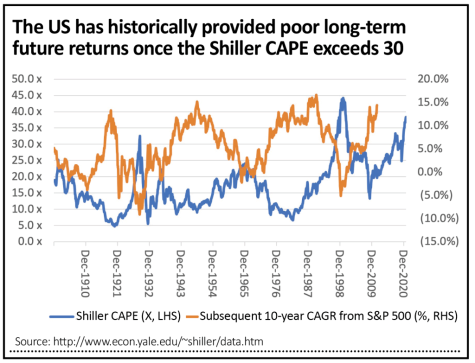

When compared to the historical averages cited above, the S&P 500 bull market is looking long in the tooth. Other concerns include extended valuations, profit margins that are at risk of turning lower, and the likelihood that we may soon enter a slower growth phase in the global economic cycle. With all this in mind, the next 12 months are likely to prove bumpier than the past 20 months for equity investors. Nevertheless, it looks like the equity bull market is still on a solid foundation. Importantly, The S&P 500 has surged over the past 20 months. Could the spread of the Omicron variant spark the first correction of the bull market? Paul Danis, our Head of Asset Allocation, provides context and discusses the outlook. Could Omicron derail the US equity bull market? 01 December 2021 we believe the economy will continue to expand at a healthy pace. Based on cycles from 1990, the S&P 500 peaks on average two months after the unemployment rate begins to rise.

Is there continued scope for the labour market to improve?

The US unemployment rate has already dropped a lot. It is currently at 4.6%, significantly lower than the April 2020 high of 14.8%. The Omicron variant creates new uncertainty, but most of what we are seeing suggests it will go down further. Importantly, US households are still sitting on roughly $2.5trn in excess savings built up during the pandemic. True, there have been signs of weakness from the all-important US housing market, such as housing starts. But that does not appear to be because of weak demand. Rather, supply bottlenecks appear to be the problem, with homebuilders struggling in terms of hiring workers and with the high price of building materials. Housing units authorised in the US have attained new highs, which likely indicates some pent-up demand.

Is there anything else supporting the equity market?

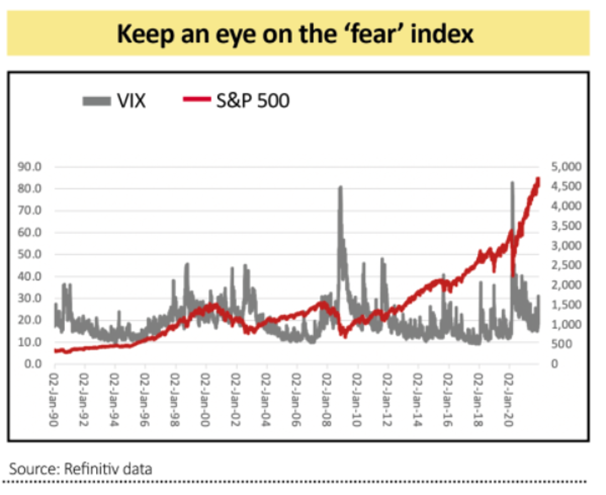

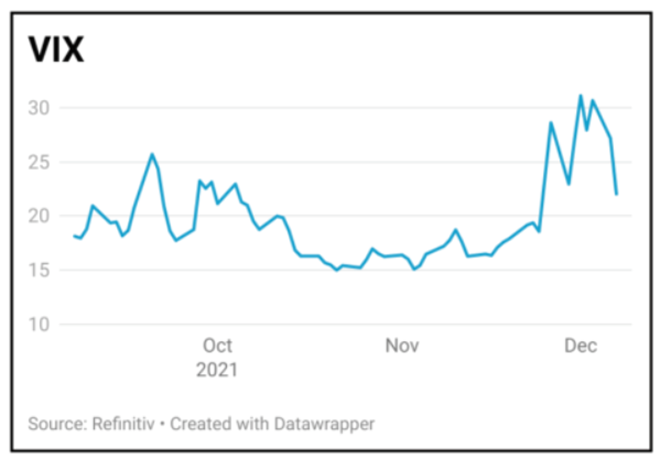

There are some silver linings to the Omicron-induced sell off. On the greed and fear spectrum, the Omicron news turned the dial meaningfully toward the latter. On that front, the market’s ‘fear gauge’, the VIX index, hit the highest level since February on Friday. A healthy level of fear in the market tends to be more supportive of future gains compared to a backdrop of greed/complacency.

In addition, the market is now pushing back expectations of Federal Reserve interest rate hikes. The Fed’s continued willingness to stimulate the US economy, by keeping interest rates low, is also something that should support equities.

Aren’t equities now just too expensive?

It is true that equities are expensive by historical standards. But so are bonds, and investors are disincentivised to hold cash, thanks in large part to the Fed’s accommodative policy stance. The inflation-adjusted ‘federal funds rate’ is currently below -4%. This means investors’ cash holdings are depreciating in real terms at an annualised rate of over 4%. These low real yields on cash and bonds combined with solid corporate profits growth are keeping the yields on equities at relatively attractive levels even after such a strong rally.

So, you remain bullish – what are the risks?

Omicron is clearly a big one. Another is that the Fed will end up tightening policy sooner than most expect. This could happen if long-term inflation expectations change. While ten-year inflation expectations implied by US inflation-linked bonds are elevated, they are not at extreme levels. Other measures of inflation expectations also suggest the market is not overly concerned about inflation over the longer-term. While there’s no room for complacency on inflation, the data are not behaving in a way that would make one believe the Fed will imminently pull the rug out from under the equity market.

Conclusion

The emergence of the Omicron variant is undoubtedly a concern. Nevertheless, on a 12-month view, we believe that a continued overweight in equities and underweight in bonds is appropriate. Equity investors are likely to be in for a bumpier ride over the next year. But with the economic outlook still largely positive and given the Fed’s currently supportive policy stance, it looks like the equity bull market remains on a reasonably solid foundation.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

David Purcell

8th December 2021