Please see below article received from Tatton Investment Management on Friday evening, which provides a detailed update on markets and global economies.

Stock markets around the world continued their volatile trading pattern over the past week, although compared with January, trending slightly up rather than down. Bond markets, on the other hand, continued to retreat as yields continued to rise. This type of market action has now become characteristic for capital markets this year, as they experience their very own climate change, now that the coronavirus appears to have lost its lethal impact on the majority of the population.

We have written at length about the U-turn of the central banks, which have swung from downplaying (if not ignoring) inflationary pressures to seemingly becoming more concerned about fighting inflation than ensuring the continued wellbeing of the economy. This week continued very much in the same vein, but several new data points are beginning to offer more clues into the direction of travel beyond central bank action.

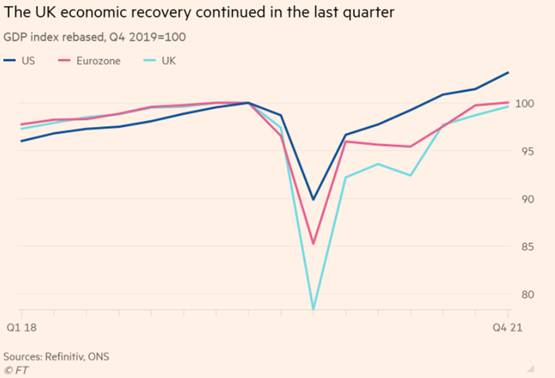

In the UK, GDP growth of 7.5% was reported for 2021, which put the economy roughly back to where we were before the pandemic started back, this time two years ago. The chart below illustrates how the V-shaped recovery has not only taken place in the UK, but also Europe, while the US is the outlier that has surpassed the starting level. As we know, this was substantially achieved by larger and less targeted handouts by the US government that resulted in a significant consumer demand boost. The increased levels of inflation are, to a large extent, the undesired side effect of this necessary, but hard to fine-tune, bridging support for the affected population.

The latest monthly inflation data for the US was therefore keenly awaited and, when it came in higher than hoped at (also) 7.5%, US stocks sold off as they quickly priced in that the US Fed will tighten and raise rates even faster than previously anticipated. Looking at the granular inflation data though, the strong market reaction felt counterintuitive, given all the major inflation-driving components of last year had continued to decline in their contribution, especially durable goods (the things we were most keen to order during the pandemic). What may have caused the negative surprise is that inflation appeared to have started ‘leaking into’ areas broadly unaffected by supply chain issues, and which are seen as more ‘sticky’ (not tending to reverse prices easily), especially the services sector.

On the other hand, there was some good news from the data on wage rises. While overall US wage growth has picked up to an uncomfortable 5%, this is very much concentrated among the very lowest earners. While this means wage growth is not sustained across the whole of the labour market, it also suggests the forces of capitalism are currently addressing the problem of inequality that has become such a divisive force – not just for American society.

Given bond yields are now broadly back to where they stood before the pandemic, equities have not in fact performed too badly so far this month. It appears markets are getting their collective heads around the ‘investment climate change’, and one could argue that by now quite a lot of rising yield headwind has been priced in without causing the substantial ‘damage’ the doomsayers had predicted.

This may be, because the inflation headlines this week were flanked by more positive data from the real economy, which would also explain why implicit long-term growth expectations as expressed by certain parts of the bond markets (ten-year yields, ten-year forward) communicated increasing optimism as they did not mirror the negative vibes from the flattening of the yield curve as they usually do, but went the other way.

To this end, January monetary data from China indicated that the leadership there had once again opened the credit stimulus taps – which has in the past resulted in growth stimulus spilling over into the rest of the global economy. On the trade side, volumes improved in the stream of goods with China which should reduce supply chain issues and stimulate the Eurozone economy.

In the wider world of emerging markets, we may see similar central bank loosening tendencies as in China, given they have already been in a tightening cycle since early last year and are therefore far more likely at the end of it compared to western central banks. This would add to China’s demand stimulus and bring positive growth impulses to global trade (we touch on this in this week’s article on commodities).

In Europe and the UK, strong 2021 growth came about despite significant reductions in inventories. This means that the rebuilding of those inventories in 2022 should carry some of the 2021 demand boost into GDP growth this year. Most surprising, perhaps, was data showing that despite all post-Brexit trade regulation frictions, the trade volumes between continental Europe and the UK are returning to pre-Brexit levels. As observed in the past, when Europe’s economy does well from resurgent global demand, so does the UK and, with the trade linkage seemingly healing, this is good news for domestic growth prospects.

Of course, not all is well and there are plenty of dark clouds still on the horizon, be they the cost-of-living challenge from energy prices reducing aggregate consumer demand, or Russia’s President Putin still threatening to extend the fossil fuel shortage that is now the main driver of inflation. However, the overall mix of data this week provided positive evidence that the current economic slowdown may not be as deep-seated as feared, and that capital markets appear to expect subsiding inflationary pressures will also lower the pressures on central banks to tighten too fast and too soon. The Bank of England’s chief economist’s remarks this week to that end were positively received.

Judging from the significant relative moves between different sectors and investment styles like Growth and Value, the message of change in the investment climate appears to be getting through. Positive returns may no longer be as readily available across all asset classes, sectors and styles, but for those who analyse, search and skilfully anticipate the progress of this uncharted post-pandemic economic cycle, there should be ample opportunities (For more, please read our article on the dynamics of small cap equities).

We endeavour to publish relevant content and news on a regular basis, so please check in again with us soon.

Please find below, the Daily Investment Bulletin update received from Brooks Macdonald this afternoon – 10/02/2022

What has happened

Risk appetite surged yesterday with a broad rally across most major sectors as central bank speak pushed back against the market’s aggressive interest rate pricing. Technology has been a particular beneficiary of this rally and yesterday’s session is another sign that the fate of the sector is showing signs of decoupling away from the grind higher in US bond yields.

Central bank speak

After the comments from Bank of France President Villeroy on Monday, suggesting that monetary tightening expectations in the market may have gone too far, bond markets began to stabilise after a choppy few days. Yesterday we heard from Fed voting member Mester of the Cleveland Fed, Mester said that she didn’t see a compelling reason to raise rates by 50bps when lift off occurs (widely expected to be in the March meeting). In the UK, the Bank of England’s Chief Economist, who pushed back against market pricing at the end of last year, said that ‘I worry that taking unusually large policy steps may validate a market narrative that bank policy is either foot-to-the-floor on the accelerator or foot-to-the-floor with the brake.’ European bond markets reacted positively, with German bunds finally ending their run of 11 consecutive days of yield rises.

US CPI

Today sees the week’s main event, the latest US inflation numbers. Most central banks have stressed the humility required around forward guidance given the uncertainties around inflation and growth for the rest of this year. Today’s CPI number will be closely watched to see if the month-on-month path of inflation is starting to slow. Consensus is expecting US CPI to increase by 0.5% over the last month (reaching 7.3% year-on-year) and for US Core CPI to also rise by 0.5% over the month and 5.9% over the last year. Both Core and headline CPI grew by 0.6% in December so if the consensus is achieved, this would show a slowing of the inflation rate. There is room for caution however, 0.5% month-on-month inflation is still a hefty increase and there may be signs of distortion due to the Omicron variant.

What does Brooks Macdonald think?

Few are expecting a ‘turn’ in inflation data until April/May of this year when the month-on-month figures are expected to start moderating. Should we see inflation come in to the downside today, the current rally may gather further steam. That said, we should be very conscious of impacts from the Omicron variant distorting the information we can garner from one data release in isolation.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below report received from BNY Mellon Investment Management yesterday afternoon, which sets out to explore some of the key drivers behind the persistent gender-investment gap from the perspective of those who currently invest, those who don’t, and the investment industry itself.

We set out to explore some of the key drivers behind the persistent gender-investment gap from the perspective of those who currently invest, those who don’t, and the investment industry itself.

If women invested at the same rate as men, there would be at least an extra:

$ 3.22 trillion of assets under management from private individuals today

$ 1.87 trillionof additional capital into Responsible Investment

We found that if women invested at the same rate as men, there would be at least an extra $3.22 trillion of assets under management from private individuals today. Perhaps more important, our research also reveals that women are more likely to make investments that have positive social and environmental impacts, meaning that there would be an influx of $1.87 trillion of additional capital into Responsible Investment if women invested at the same rate as men.

Three key barriers to higher levels of female participation in investing:

1. Confidence crisis

Globally, just 28% of women feel confident about investing some of their money.

2. Income hurdle

On average and globally, women think that they need $4,092 of disposable income each month – $50,000 per year – before [they can begin] investing some of their money.

3. High-risk investment myth

Almost half of women (45%) say that investing money in the stock market – either directly or in a fund – is too risky for them. Only 9% of women report that they have a high or very high level of risk tolerance when it comes to investing; 49% have a moderate risk tolerance; and 42% have low risk tolerance.

Women tend to feel less confident about investing than savings, property or pensions. In our report, we explore the reasons why more women aren’t investing and how the investment industry can evolve to support more inclusive investment.

1. Why women don’t invest

Women are less likely to invest than men. This gender-investment gap is a global issue, which limits women’s financial futures and their capacity to influence a better future for the planet. Over half of women believe that it’s important that more women invest to give them the choice to support companies and causes they agree with (53%) and to give them more influence over business and its environmental and social impact (52%).

In order to understand why women don’t invest at the same rate as men, and to explore what we in the industry can do to raise levels of female participation, we interviewed 8,000 men and women worldwide.

Our research reveals that the investment industry must tackle three key investment barriers to encourage more women to invest:

Engagement Crisis

The investment industry is failing to reach, appeal to, and engage women to the same degree as men. Globally, as few as one in 10 women feel they fully understand investing, and less than a third of women (28%) feel confident about investing some of their money.

With so few women comfortable investing any of their money, the urgent need for better communication and engagement is clear. Across key aspects of financial decision-making, investment is the area where the fewest women feel confident, compared to making decisions around savings, property and pensions.

Income Hurdle

On average and globally, women believe they need $4,092 of disposable income each month—almost $50,000 per year—before they would consider investing any of it. In the US, for example, on average women believe that they need over $6,000 of monthly disposable income—just over $72,000 per year—before they can start investing.

Clearly, this is unrealistic, especially given the fact that over a quarter of women (27%) describe their financial health as poor or very poor. For the investment industry, overcoming this misconception and explaining that only a small amount of money is needed to start investing should be a key focus.

Overcoming the income hurdle

Despite the widespread belief that you need large amounts of spare money to start investing, even a small investment habit of setting aside a few dollars each month can really pay off over time. For example, if you began 10 years ago investing $30 a month in the S&P 500 Index, your portfolio could be worth over $8,000 today, of which less than half would be money that you put in yourself.

2. How women investing can change the world

Higher levels of female participation in investment could not only have a huge impact on women’s lives but also on the world at large, as women are more likely to invest in causes that they believe in, such as protecting the environment.

What then could encourage more women to invest? Our study shows that women across the world are motivated by the impact that their investments could have. More than half of women (55%), for example, would invest (or invest more) if the impact of their investment aligned with their personal values, and 53% would invest (or invest more) if the investment fund had a clear goal or purpose for good. Two-thirds of women who currently invest (66%) try to invest in companies they like and that support their personal values.

This drive to align investments with values seems to be stronger among those with children: three-quarters of parents—both men and women—who currently invest say that they prefer to invest in companies that support their personal values, compared with 59% of adults who do not have children.

Responsible Investment (RI) means investing for a better future; a more sustainable, diverse, and equitable future. RI covers a spectrum of investing styles, including exclusionary screening, ESG integration, sustainable investing and impact investing. ESG integration is the systematic and explicit incorporation of ESG factors into financial analysis and investment decisions to better manage risks and improve returns. Impact investing goes a step beyond ESG investing. It is the practice of investing with the dual objective of generating a positive, measurable and intended social or environmental impact, as well as a financial return.

Investment Shift

The profile of those who invest is changing, and with it there is a shift in focus and values. Our data shows that older men – traditionally the “typical” investors targeted by the investment industry – are less focused on impact investing and aligning their investments with their values. While 69% of young women (aged 18–30) who currently invest select their investments based on their impact, this is true of only a third (33%) of older men (aged over 50). And more than seven in 10 women under 30 (71%) prefer to invest in companies that support their personal values, compared with 54% of men over 50.

3. Building an inclusive investment industry

If it’s possible to raise the participation rate of women investing, it could increase their personal prosperity and could have a beneficial influence on environmental and social issues.

Making investing more accessible to women isn’t just about ensuring they have the right technology, but also inclusively equipping everyone with the knowledge, skills, and fostering the motivation to engage with investing. This requires a significant cultural shift within the industry—not only in the way that products are developed and marketed but also in the diversity of the investment industry itself.

We asked asset managers – representing nearly $60 trillion of assets under management – for their insights on the key challenges for gender-inclusive investment and for their thoughts on how the industry can change to encourage more women to invest. Their answers reveal the extent to which the investment industry is currently oriented toward male customers and help identify ways in which financial products and messaging could be reshaped to attract and engage more women.

An industry with men in mind

Currently, nearly nine in 10 asset managers (86%) admit that their default investment customer is a man, and three-quarters of asset managers (73%) state that their organization’s investment products are primarily aimed at men, suggesting that they focus on the benefits and features that generally appeal more to men than women.

As a result, potential female investors are met with language, imagery and messaging targeted mainly at a male customer. This often includes the use of high-risk metaphors, such as those used in extreme sports, and the concept of high performance and achievement as a shorthand for investment success.

The answer to engaging women in investment isn’t found in outdated gimmicks and doesn’t require, for example, the increased use of the color pink—rather, it’s about forming a connection by understanding what motivates women to invest and how they like to be communicated with.

If the industry can re-think the language around investing, there’s a significant opportunity to affect how much women invest: 37% of women said that if investment language were easier to understand, it would influence them to invest, or to invest more than they currently do. However, the key takeaway is that the language which describes financial products should not only be simpler, and avoid jargon, but also be more clearly aligned to women’s long-term goals and values.

As increasing health standards mean that today’s women need to plan for what might be a 100-year lifespan, women are motivated to invest by thinking of their long-term financial prosperity, independence, and the impact their investments can have. Products packaged to meet these needs and address these interests, clearly communicated in straightforward language, should go a long way to increasing women’s investment.

What Women Want: Investing in Independence

As discussed earlier in the report, women value responsible investing and investments aligned with their personal values. They are also motivated to invest by a range of other factors, with financial independence topping the list. The investment industry, therefore, has a key opportunity to appeal to women by focusing on messaging around financial independence.

Almost two-thirds of women (63%) believe that it’s important that more women invest to provide for themselves in retirement, and six in 10 women believe that it is important that more women invest in order to give themselves greater financial independence. This rises to eight in 10 women in India (80%) and the US (79%). Historically, the industry has marketed wealth products to women based on financial provision for their families; today, however, we find that investing in independence is more important than financing dependents. Motivators around retirement and independence are rated even more highly than growing a financial legacy for their family, for example (cited as important by 57% of women).

4. Changing investment, changing the world

The amount of wealth controlled by women globally is disproportionately small, but ever-growing and our research reveals that more women are looking to invest. This could bring benefits not only for those who invest but also for women everywhere, and for the world as a whole. However, women are being held back by lack of confidence, concerns about risk, and an industry oriented toward men.

It is up to us – the investment industry – to lead the change, by educating, inspiring, and including more women in all that we do. The traditional stereotype of the person who is interested in investing – the wealthy older man – is outdated and needs to be dismissed. Young women are interested in investing too, but they need to be empowered to do so. The face of investment is changing – and the industry needs to evolve too. Empowering women to invest can come about by bringing the world of investment to them – by providing the knowledge and skills they need and realigning the messaging to promote conversations both inside and outside of the industry that speak to their motivations, be they financial, societal, or both.

Responsible investing allows women to champion causes they believe in effectively by using their money to directly help reach social and environmental goals. A greater focus on this type of messaging and on the wider benefits of investing should help to attract more women.

Greater diversity within the industry should also help to achieve higher levels of female participation and ultimately investment; but in order for a meaningful industry shift to take place, both women and men will need to help drive change.

If we all work together, we can achieve the goal of making investment more inclusive, for the benefit of all.

The time to act is now. The investment industry needs to be more inclusive, find a better way to engage with women, make investing more accessible and close the gender-investment gap. Because more women investing will benefit everyone: society, the investment industry and the planet.

Please check in again with us soon for further relevant content and news.

Please find below, a breakdown of the impact of Russian politics on economic markets, received from Invesco, yesterday afternoon – 31/01/2022

Key takeaways

Russia could be on the brink of war with Ukraine

We’d like to think that the economic arguments will be enough to prevent conflict, but the Kremlin’s desire to restore friendly buffer states on its borders may yet prove their priority.

How are we exposed?

The Invesco Emerging Markets Strategy has three Russian holdings that comprise approximately 4% of the strategy.

Should we exit our Russian holdings?

We are cautious about capitulating at the moment of maximum fear. During periods of greatest fear, investors get their biggest opportunities.

Assessing risk

Investing by its nature involves taking risks. We’re all taught about the inverse correlation between risk and return, ‘nothing ventured, nothing gained’, even if the psychology of human behaviour can often make that relationship somewhat perplexing.

There have been countless examples of asset bubbles caused by irrational exuberance. This ultimately led to financial calamity for many of those involved, suggesting that risk is often heightened when greed is in abundance, rather than when investors are most fearful. We would argue that it’s often not the risks themselves that prove disastrous for investors, but how those risks are priced.

Take the example Cisco during the Dotcom bubble. In the 10 years following the year 2000, when the shares peaked at US$80 per share, Cisco grew revenue at an 8% CAGR and earnings per share at a 10% CAGR – a respectable rate. Yet, the shares were down around 70% over that period, and they trade at only US$56 today.

The fundamental risks to Cisco’s business in the first quarter of 2000 proved far, far less important to shareholders than the risk they were taking by paying such a high valuation. Cisco shares were trading on roughly 150x earnings in 2000, but trade on around 16x today.and US$.

We seek to minimise the main risk investors face – that of permanent loss of capital – by making sure we don’t overpay for stocks and by ensuring the companies we own shares in have strong balance sheets. We take this approach with companies wherever they’re listed, including in Russia.

Russia and geopolitics

It’s important to keep the context in mind – Russian equities have traded at a steep discount to emerging market peers for many years. There are a good reasons for this:

Commodities. A predominance of commodity producers in the Russian market, which typically trade on lower multiples.

Governance. Whether it’s fears about government expropriation (à la Yukos in 2003), or that a particular oligarch may get on the wrong side of the Kremlin – there is a governance deficit in Russia.

Geopolitics. Russia’s foreign policy approach under Putin has become increasingly muscular, which has led to tensions with neighbours, including those in an expanded NATO. Following Russia’s annexation of Crimea, Western countries introduced a raft of sanctions, largely targeted at individuals close to the Russian President himself.

Given this context, we typically ascribe lower ‘fair’ valuation multiples for Russian stocks than we do for other countries in emerging markets. Effectively, we assume these risks will persist and so we price them into our estimates of what constitutes fair value. This means that we require higher returns from our Russian holdings than we do from holdings in other countries to account for these risks. We believe this fundamental approach to valuation helps reduce the risks associated with investing in Russia.

Take Sberbank, for example, which has delivered a median ROE since 2006 of 20.8%. This compares favourably with HDFC Bank, one of India’s highest quality private banks and a stock we have owned in the past. It has generated a median ROE of 18% over that time (the period in which HDFC Bank has been listed). While returns have been far less volatile at HDFC Bank compared with Sberbank (standard deviation of 1.6 vs. 6.6), we would highlight that Sberbank still provided a around 10% ROE in 2015 – a year of financial crisis in Russia following a more than halving in the rouble’s value vs. the US dollar.

Today, Sberbank trades on 0.9x price to book, having averaged around 1.5x over the last decade. HDFC Bank trades on 3.9x price to book today, having averaged above 4x over the last decade. In short, it feels to us that the risks associated with Sberbank are being clearly factored into the shares when compared to a similarly high-return bank in India.

Portfolio Construction

For portfolio construction, there are some key pillars that further reduce risk for the strategy. They are:

Diversification by industry. This applies to the strategy as a whole, but also to our Russian holdings. We are keen to make sure that we have diversification across industries within Russia, so that we’re not overly exposed to sanctions that may fall hardest on one industry.

Diversification by owner. We aim to be diversified by the type of business owners, be that government-owned companies, companies run by oligarchs, Western owned companies, or private equity firms. This again reduces the risk that any one type of controlling shareholder is targeted by sanctions.

Strong domestic market positions. We make sure that the companies we’re invested in have strong domestic businesses that will enable them to survive even in a tough sanction regime.

Strong balance sheets. Ensuring that contrarian ideas have the balance sheet strength to withstand temporary setbacks or ‘unknown unknowns’ is an important way to manage downside risk.

Position sizing. By far and away, the biggest tool we have to reduce risk is to keep position sizes measured. Given how lowly valued Russian equities are relative to emerging market peers, you might expect valuation sensitive investors like us to be significantly overweight Russia. We are not. We much prefer to focus on picking stocks and analysing their business fundamentals as the potential source of alpha while minimising country factor risk.

Conclusions

It should go without saying that we see few winners from war in Ukraine, and we hope that diplomacy will prevail. Conflict would likely end up being protracted and destabilising. The economic impact of sanctions could be very severe for Russia’s economy, even after considering Russia’s strong fiscal position (large current account surplus and low government debt).

We’d like to think that the economic arguments will be enough to prevent conflict. But the Kremlin’s desire to restore friendly buffer states on its borders may yet prove their priority, for better or worse.

Regarding potential sanctions, we believe the range of potential outcomes is extremely wide. We’d like to highlight that valuations for many Russian stocks are now back at the levels of the 2014/15 financial crisis. To us, this implies that a good deal of bad news is already priced into shares.

We also feel that the lessons from previous episodes, such as the sanctions that were imposed on Rusal in 2018, will give Western countries pause before enacting sanctions that risk destabilising global commodity markets, as they did for aluminium then. Likewise, should the West choose to cut Russia off from the SWIFT payments system, it could wreak havoc for companies and countries that rely on Russian exports of gas and oil – including many in Western Europe.

Of course, we could just exit our holdings in Russia. However, we are cautious about capitulating at the moment of maximum fear. Looking back, it has been during periods of greatest fear that investors get their biggest opportunities. This experience, plus the low valuations (and high dividend yields) on offer, keeps us invested in Russia, albeit in a measured way.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

Please find below, an update in relation to share prices, received from AJ Bell yesterday – 23/01/2022

Well, that didn’t take long. The Fed began to pump less Quantitative Easing (QE) into the financial system in November and the stock market’s wheels have started to wobble after barely two months of less cheap money, let alone move to withdraw it.

Investors are already starting to ask themselves how much the US Federal Reserve can do to tighten monetary policy before it either puts the brakes on the economy, breaks the stock market or both – and the answer might be not very far at all.

Some of the asset classes, funds and individual stocks which have performed best, attracted the hottest money flows and drawn the biggest headlines have started to flag, or even fall sharply. All are generally toward the riskiest end of the asset class spectrum, where the rewards can be highest, but the risks are too, should something go wrong.

Small caps are wobbling. America’s Russell 2000 index is now trading below where it was twelve months ago, and the UK’s FTSE Small Cap benchmark is losing a little momentum.

Source: Refinitiv data

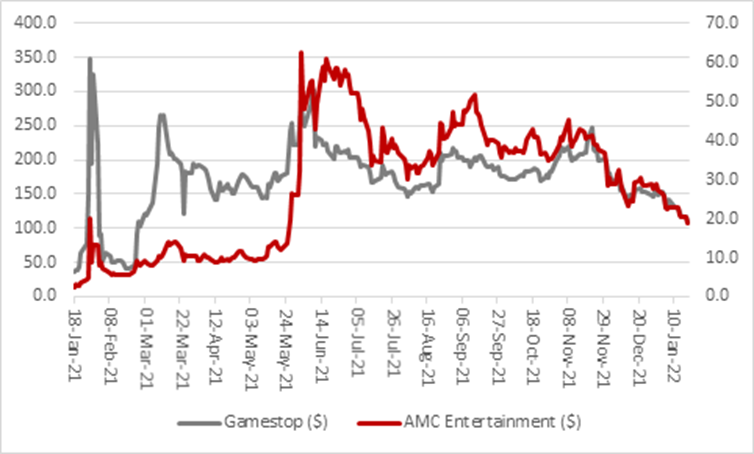

Meme stocks are taking a pasting. You have to hope that anyone who has held on to GameStop, AMC Entertainment and others to thwart the hedge funds who were short-selling these names have not ended up cutting off their own noses to spite their face. Buyers in the very early days may still be in the black, but anyone who piled in late to join the fun or try to make a fast buck could now be deeply in the red.

Source: Refinitiv data

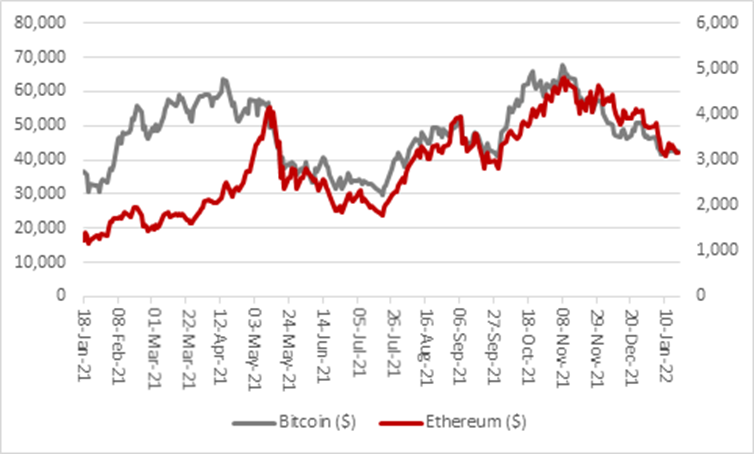

Cryptocurrencies have swooned once more.

Source: Refinitiv data

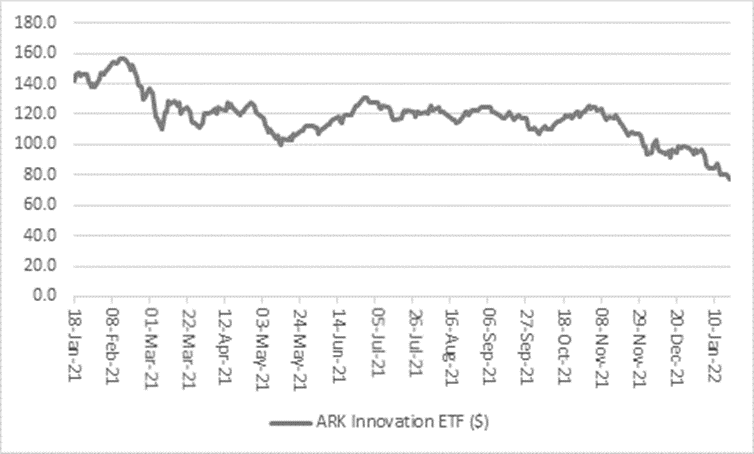

And the poster child for fans of momentum, tech and potential disruptive winners, the ARK Innovations Exchange-Traded Fund (ETF), continues to sink.

Source: Refinitiv data

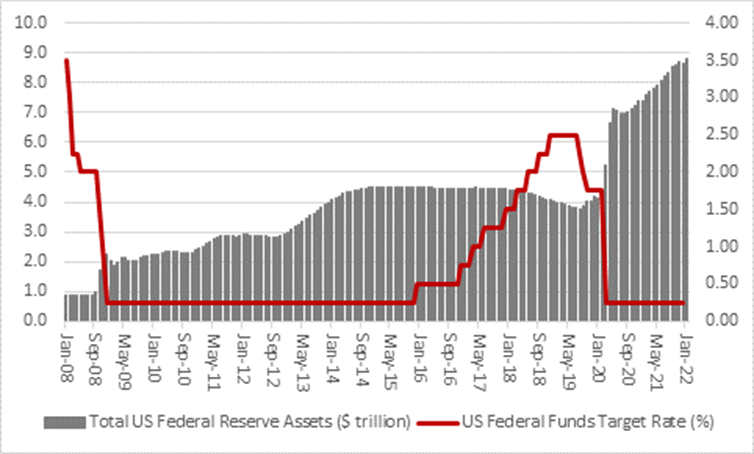

It may not be a coincidence that the Fed has started to reduce the amount of monetary stimulus it was pumping into the US economy via Quantitative Easing. It started to cut QE from a run-rate $120 billion a month by $15 billion a month in November and then by $30 billion a month from December.

That should mean the Fed’s $8.8 trillion balance sheet stops growing in March. After that, the central bank may turn to Quantitative Tightening (QT) and start to withdraw stimulus and shrink its balance sheet.

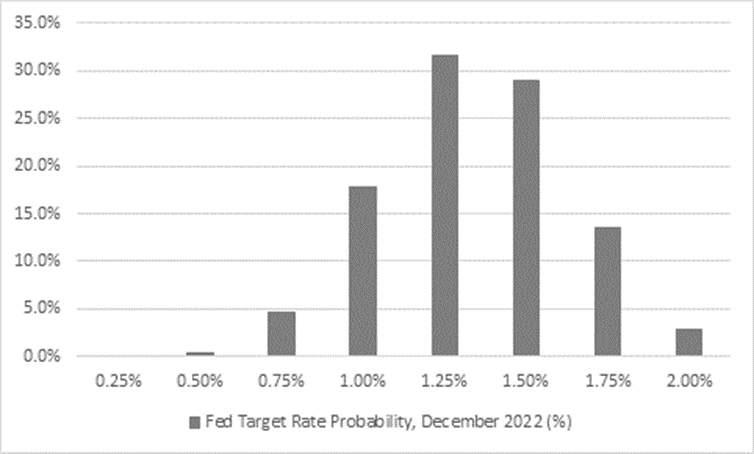

Meanwhile, the markets have started to price in at least four one-quarter percentage point interest rate increases from the US central bank by the end of this year.

Source: CME Fedwatch

Recent precedents for tighter monetary policy (or even simply, less loose, less accommodative policy) are enough to give investors pause for thought:

In 2013, financial markets rebelled at the very talk of tighter policy and the so-called Taper Tantrum persuaded the Fed to back off.

Between December 2015 and December 2018, under Janet Yellen and then Mr Powell, the Fed raised rates from 0.25% to 2.50%. It also shrank its balance sheet by $700 billion, or some 17%, between 2017 and 2019. But it then stopped as the US economy began to slow and signs of stress began to show in the US interbank funding markets in autumn 2019. As a result, the Fed’s balance sheet had started to grow again several months before the pandemic prompted fresh interest rate cuts and more QE in the spring of 2020.

Source: FRED – St. Louis Federal Reserve database, US Federal Reserve

There are good reasons for such caution. Global debt is so much higher now than it was in 2013 or even 2018, so the economy will be much more sensitive to even minor changes in interest rates.

More specifically for share prices and company valuations, tighter monetary policy – at a time when indebted Governments are throttling back on their fiscal stimulus programmes and looking for fresh sources of income from tax or social levies – has four possible implications:

Higher interest rates may mean an economic slowdown, again because there is so much more debt in the system. As the old saying goes, economic upturns don’t die of old age, they are murdered in their beds by the US Federal Reserve. In addition, consumers’ ability to consume will be crimped if inflation outstrips wage growth and their incomes start to stagnate or fall in real terms.

Higher rates reflect inflation, and faster (nominal) GDP means investors do not have to pay a premium for long-term future growth (for secular growth names like technology and biotechnology) when potentially faster, near-term cyclical growth (‘value’) can be bought for much lower multiples (even if it comes from oils, miners, banks).

Inflation can eat away at corporate margins and profits. Right now, they stand both at pretty much record highs, as do valuations, at least in the USA, based on ratios such as market cap-to-GDP and Professor Robert Shiller’s cyclically-adjusted price-to-earnings (CAPE) ratio. If earnings start falling, valuations could do so, too, if confidence wobbles. Instead of the double-whammy that provides gearing to the upside, as investors pay higher multiples for higher earnings to give ever-higher share prices, markets see the opposite: earnings fall, investors pay lower multiples for lower earnings and share prices fall faster.

Higher interest rates mean analysts and investors deploy an increased discount rate in their discounted cash flow models to calculate the net present value (NPV) of future cash flows from long-term growth stocks. A higher discount rate means lower NPV. A Lower NPV means a lower theoretical value of the equity and that means a lower share price.

All four are clearly worrying previously rampant financial markets but that in theory should not be the concern of the US Federal Reserve, or indeed any central bank. Their job is to keep inflation on the straight and narrow, to ensure it does not destroy wealth and prosperity and imbalance the economy.

But a decade and more of zero interest rates and QE – unintentionally or intentionally (judging by a string of speeches from former Fed chair Ben S. Bernanke dating back to at least 2003) – have persuaded or forced investors to take ever-increasing amounts of risk to get a return on their money.

Central banks are presumably concerned that having tried to create a wealth effect by stoking asset prices, the opposite effect could kick now in, hitting confidence and consumers’ ability and willingness to spend.

If inflation really does prove to be sticky, or even keep going higher, central banks may therefore be stuck between a rock and a hard place. They will want to control inflation on one side but their ability to jack up interest rates and withdraw QE may be constrained by record debts and concerns about the economy, employment (and financial markets’ stability) on the other.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

Please see below, a European political and regulatory outlook from Invesco – received late yesterday afternoon – 13/01/2022

Key takeaways

Covid-19 continued to present a threat to European economies in 2021 and revealed deep fissures in the political landscape. The pandemic didn’t just leave its mark on the political scene but also in the regulatory sphere — a trend that will continue in 2022.

We expect key political drivers to include the recent German election and the upcoming French presidential vote, which comes amid concerns over Russia and China’s influence. The cost of the green transition, inflation and Brexit will also be major themes this year.

On the regulatory side, policymakers will make further refinements to ESG frameworks; roll out initiatives to enhance retail investor participation; increase their focus on financial stability; and turn their attention to the supervision of digital financial services.

Covid-19 continued to present a threat to European economies in 2021 and revealed deep fissures in the political landscape. The pandemic isn’t just leaving its mark on the political scene but also in the regulatory sphere, where regulators are grappling with the lessons to be learned from the market volatility and so-called ‘dash for cash’ at the start of the pandemic in March 2020.

We turn our gaze to 2022 and seek to highlight what we see as the major political and regulatory risks on the horizon.

Section 1: Political outlook

Our analysis identifies 8 key themes that will influence the political landscape:

The outcomes of European elections in France (this year) and Germany (in 2021) are likely to colour approaches to further EU integration, opening the field for a triumvirate with Italy.

Battles over the rule of law in Hungary and Poland will raise questions about the nature of the EU and its members, as well as fears regarding Russia’s intentions.

The EU’s strategic autonomy to act against a backdrop of increasing global polarisation between the US and China will influence trade, defence and economic thinking.

Reviewing the fiscal rules that govern the eurozone will shape the EU’s ability to invest in the green and digital transformations.

Implementing the UK and EU’s climate commitments will finally turn promises into action, with fights expected on the pace, and who should bear the cost, of the transition.

With above-target inflation likely to persist in both the euro area and the UK, the cost of living will likely re-emerge as a political battleground.

Further antagonism between the UK and the EU over the implementation of Brexit will continue to weaken incentives to build cooperation in other areas, such as financial services.

Opposition to UK planning reforms could undermine Boris Johnson’s election pledge to ‘level-up’ the UK outside London and the South East.

European leadership and integration

France and Germany are the traditional motors of European integration, and it’s often difficult to get anything done in Europe without the endorsement of these two states. It is therefore significant that Germany has a new government that will start to reach cruising speed in 2022 while France will head to the polls in April 2022.

In Germany, the so-called “traffic light” coalition made up of the Socialists, Liberals and Greens took office in December 2021. This was a watershed moment that brought to a close the stability and statesmanship that Angela Merkel brought to Germany and to Europe more widely.

In France, President Macron will face voters in April 2022, along with a fragmented field of candidates. While current polls indicate that Macron remains the favourite to win the election, the campaign has been marked by increasing populist sentiment, particularly from the right and far-right that are hoping to capitalise on anti-immigrant attitudes.

The outcomes and consequences of these elections will have a strong impact on what can get done in Europe in 2022, as well as the years to come. Although the new German government is likely to be closer to France in terms of European integration, the ability of a new and untested coalition to bring key European partners with them is likely to be weaker than under Merkel. France may have less appetite for grand integration projects for fear of it triggering heightened populist sentiment at home.

The Franco-German axis may be weakened, but it may also to include the Italians as Mario Draghi brings stability and statesmanship that has been absent in Italy for some time and gives it a strong voice in European matters. The recent Quirinale Treaty between France and Italy could be a first step in building a strong triumvirate at European level that would be pro-European integration.

Threat from the East

While not new, the battle over the rule of law in the Eastern bloc, and in particular in Poland and Hungary is likely to continue simmering in 2022. For many member states and the European Parliament, the values on which the EU is built are at stake due to the issues presented in Poland and Hungary. These challenge the EU’s ability to advocate about democratic values abroad if they can’t keep their own members from backsliding.

For Poland and Hungary, the issue is as much about domestic politics as it is about the financial incentives on offer from the EU, with Poland having threatened to bring the EU decision-making process to a standstill if EU funds are withheld. It’s not only about Poland and Hungary. Czechia, Slovenia and Bulgaria are also at risk of breaches of rule of law.

But there is division within the remaining member states on how to respond. Although the European Parliament is urging the European Commission to invoke the rule of law provisions in the EU budget — which enables the Commission to withhold funding until steps have been taken to address rule of law issues— Germany and others have called instead for dialogue.

The one glimmer of hope on the horizon is that there are elections in Hungary in May 2022 and recent polls indicate that the opposition candidate that aims to unite all opposition parties against Prime Minister Viktor Orban has a realistic prospect of unseating the incumbent. With Prime Minister Andrej Babis of Czechia having also recently lost elections, is the tide turning on populism in the East?

Even if the debate over the rule of law is primarily an internal issue within the EU, it also has geopolitical dimensions given the increasing assertiveness of Russia and pressures on the EU’s Eastern border from Belarus. As a result, some countries such as Germany have been wary of a direct confrontation with wayward Eastern states for fear of alienating those countries and driving them into the arms of Russia.

Strategic Autonomy and National Security

The EU’s focus is often internal but increasingly the theme of “strategic autonomy” is discussed within EU circles. In part a response to former US President Donald Trump’s exposure of EU reliance on the US and growing Chinese assertiveness on the world stage, the question of the EU’s place in the world — squeezed in between the US and China, as well as its ability to act independently — continues to be actively discussed.

The EU is increasingly eager to review its dependence on the US for defence and its reliance on the dollar clearing, which has limited the EU’s ability to run an independent foreign policy. The strained relationship with the Trump Administration and the Biden Administration’s recent missteps including the disorderly withdrawal from Afghanistan and the recent AUKUS nuclear submarine deal have raised questions about EU-US relations within European policy circles. In particular, the EU fears being forced to choose between the US and China, which it is loath to do.

The EU’s relationship with China is equally complex. It branded China a negotiating partner, economic competitor and systemic rival in 2019 — and the EU continues to struggle to define a clear China strategy. While the commercial imperative remains strong, with China having become Germany’s top trading partner, the stalled investment treaty negotiated at the end of 2020 shows that the economics cannot be fully divorced from the politics, with voices increasingly urging the EU to use its influence to address the human rights issues and other security threats in China. For example, a recent motion by the European Parliament called for the EU to get tougher with China when it comes to human rights violations; spreading disinformation; assessing the origins and spread of Covid-19; and banning companies from 5G and 6G networks that do not fulfil security standards, all while continuing to work together on climate change and other areas of mutual interest.

Concerns regarding the US, China and strategic autonomy are likely to continue to exert a strong influence across several areas, including trade and defence but also economic topics such as the internationalisation of the euro and work on central bank digital currencies where the EU fears falling behind the US and China.

Instinctively closer to the US, the UK is confronting many of the same questions as the EU regarding China – seeking to maintain access to the commercial opportunities of the Chinese market while being increasingly vocal on human rights issues; taking steps to protect its critical infrastructure from Chinese influence; and pursuing a more active role in scrutinising the takeover of British companies in sectors deemed sensitive for national security. The (non-retrospective elements of the) National Security and Investment Act came into force from 4 January 2022, increasing the risk that certain takeovers and mergers could be significantly delayed due to increased government scrutiny.

Reviewing the Stability and Growth Pact

The rule governing the EU and eurozone fiscal policies, known as the Stability and Growth Pact (SGP), was suspended when Covid-19 hit and remains suspended until 2023. However, 2022 is likely to be dominated by debates as to how to re-introduce the rules and whether the SGP needs to be overhauled given the significant budget deficits and debt overhangs that many countries suffer from due to the pandemic.

With the EU average debt-to-GDP ratio above 100%, there is concern that a strict re-introduction of the rules[1], could force a significant number of countries to introduce austerity measures. This would potentially plunge the EU back into recession and prevent member states from undertaking the necessary investments in climate change and digital to reform their economies for the future. There is also concern that the rules have become increasingly complex and hard to monitor adequately. However, a number of the so-called “frugal” member states consider the current rules sufficiently flexible and have limited appetite to reform the framework.

The success, or otherwise, of the Covid Recovery Fund, could also play a role here as many see it as a potential blueprint for a more permanent EU-level fiscal capacity that might serve as a bridge between the current SGP rules and the need to invest in the green and digital transformations across the EU.

The review of the fiscal framework comes at a time when Europe is suffering from high inflation. While the European Central Bank considers current inflation rates transitory and has so far resisted calls from hawks to increase interest rates, it remains to be seen how long this view will prevail, particularly if other central banks start to consider higher inflation is here to stay and start raising rates.

Net Zero and EU Green Deal

If 2021 and COP26 was the year of climate promises, then 2022 is set to be the year of climate delivery. Both the UK and the EU have committed to ambitious carbon reduction targets of 68% and 55% respectively by 2030.

The debate in 2022 will be focused on how we get there. In the EU, the European Commission published in July 2021 a package of proposals known as “Fit for 55”, which will amend a range of EU law, including the Emissions Trading Scheme, the Renewable Energy Directive and the Energy Taxation Directive with the aim of aligning the EU regulatory framework with the EU’s climate targets. However, the cracks are already starting to appear. The EU Taxonomy, which aims to classify which activities are “green” has already run into the buffers as various members seek to protect their own industries — such as France on nuclear or the Scandinavian region on forestry — which risks rather fraught negotiations across the package to ensure that EU states feel that the burden of achieving net zero is fairly distributed across countries and sectors.

In the UK, following a flurry of government strategy papers in the run-up to COP26, attention will also turn to implementation of the Prime Minister’s 10-point plan and the cross-government Net Zero Strategy. With ambitious decarbonisation targets to achieve by the end of this decade, political debate will centre on the cost of ‘going green’ to consumers, as the government seeks to switch energy levies from electricity to gas; to incentivise the take-up of domestic heat pumps to replace gas boilers; and to finance further new nuclear generating capacity. Against this backdrop, further Government-mandated corporate climate disclosures will be rolled out and the Treasury will unveil the UK’s version of the EU’s Green Taxonomy (expected to include nuclear) before the end of the year.

Brexit

The second anniversary of the UK’s exit from the European Union will be marked on 31 January. While day-to-day cooperation at working level between the UK and EU remains strong across a range of areas, the post-Brexit political relationship is characterised by a lack of trust and accusations of bad faith on both sides.

The Northern Ireland Protocol, agreed as part of the original Withdrawal Agreement, is an area of contention. The UK’s challenge to the terms and the implementation of the Protocol has further eroded trust – but also yielded some movement from the EU on goods inspections. However, fundamental UK objections to the role of the European Court of Justice and the application of EU state aid rules are unlikely to be reconciled, meaning antagonism over the Protocol, as well as other sensitive issues such as fisheries, will likely persist. This will continue to weaken EU incentives to enhance cooperation in areas such as migration, scientific research and financial services – continuing to put at risk items such as the Joint UK-EU Financial Regulatory Forum, which was envisaged in the Trade and Cooperation Agreement.

Cost of living

Rising energy prices and above-target inflation brought cost-of-living issues back into political focus across Europe at the turn of the year. In the UK, the immediate effects are being felt in the retail energy supply market, which is being redrawn with the collapse of a significant number of smaller suppliers, further concentrating the customer base in the hands of the largest providers. If inflation persists, greater political scrutiny is likely to be applied to the costs to households of ‘going green’, resulting in the continuation of the long-run UK fuel duty freeze (potentially delaying the switch to electric vehicles), a delay in the government’s ambition to switch the costs of subsidising green energy from electricity bills to gas bills and pressure to delay the Government’s timetable for encouraging homeowners to replace gas boilers with low-carbon heat pumps. The debate may also weaken enthusiasm for committing to additional new nuclear generation, given the pass-through of part of the costs to consumers.

Similarly, the EU is also concerned about the rising energy prices, triggering conversations about whether such pressures are transient or more long-term and therefore warrant a structural response through reform of EU energy market regulation. The current backdrop of high energy prices and record high carbon prices could also bleed into negotiations on the EU Green Deal where the spectre of the French “gilets jaunes” protests continue to haunt politicians.

Levelling up

Alongside “Get Brexit Done”, “levelling up” was Boris Johnson’s other 2019 Election refrain. Following the Covid hiatus, the Prime Minister is now under pressure to outline a coherent levelling-up strategy that can deliver benefits to communities – focused outside London and the South East – ahead of the next general election.

With a relabelled a government department to lead the charge, a major policy paper to define the agenda and a set of Government actions is expected soon. However defined, building more homes is likely to be both central to the agenda and one of the toughest political challenges the PM faces next year. The government backed down on previous reforms to liberalise planning rules in the face of a rebellion from Conservative MPs, so a new approach is being devised. Given the impossibility of the government being able to significantly increase the number of new homes being built, in areas where demand is high and while only building on brownfield sites, there is a risk that the new proposals follow the path of their predecessor and the housing agenda remains stuck on the status quo.

Section 2: Regulatory outlook

Our analysis identifies 5 key themes that will influence the regulatory landscape in EMEA:

Refinement of the framework governing sustainable finance and environmental, social and governance (ESG) issues to address the climate transition.

Continued focus on the resilience and supervision of the non-bank sector and the stability of financial markets more broadly following the March 2020 period of volatility.

New initiatives to enhance retail investor participation in financial markets and continued focus on retail investor disclosures.

Improving the functioning, effectiveness and transparency of financial markets.

Developing the framework governing the regulation and supervision of digital financial services and operational resilience.

Sustainable Finance and ESG

The continuing development of sustainability- and ESG-related requirements applying to supervised entities will continue to be a priority for policymakers globally. For example, policymakers will continue to commit significant resource to refining the frameworks governing sustainability-related disclosures for products and financial market participants across jurisdictions.

The data required by firms to meet such disclosure obligations will also be a focus as they take forward initiatives seeking to enhance the availability of, and access to, reliable ESG data. In this regard, the development of ESG taxonomies will continue apace, with focus moving beyond “climatemetrics” towards defining the broader environmental social component of such taxonomies.

Additionally, from August 2022, intermediaries in the EU will be required to consider investors’ ESG preferences when distributing investment products, with a significant impact on their activities as well as those of product manufacturers.

Financial stability

The impact of the Covid-related market volatility experienced in March 2020 has drawn significant attention from policymakers over the last 18 months or so and we expect this to continue in 2022. Indeed, we anticipate policymakers’ analyses to evolve into proposals for regulatory reform to enhance the resilience of the non-bank sector, in particular with respect to the functioning of short-term money markets and money market funds (MMFs), as well as liquidity risk management within open-ended funds more generally.

The European Commission has already put forward amendments to the EU frameworks governing the operation and supervision of retail and alternative investment funds, with the aim of finalising proposals clarifying rules on fund liquidity risk management, loan origination and delegation over the course of 2022. Likewise, in the UK, we expect the Bank of England and the Financial Conduct Authority (FCA) to take forward their joint initiative on enhancing the resilience of the non-bank sector, with a particular focus on finalising a regulatory approach to asset liquidity classifications and swing pricing.

Retail investing

In the continuing low interest rate environment, and with more responsibility being placed on individuals to plan for their financial futures, improving retail investor participation in financial markets will be a key theme in 2022. For example, the European Commission is expected to bring forward an EU Retail Investment Strategy with the aim of addressing this theme by, in part, enhancing the effectiveness and transparency of the current EU inducements regime. In the UK, the FCA will continue to develop its cross-sectoral Consumer Duty, reinforcing firms’ obligation to consider their retail clients’ best interests when undertaking activities on their behalf. Final rules are expected in Q3 2022.

Policymakers also see improving the usefulness of retail investor disclosures as key to enhancing retail investor participation in financial markets. We expect regulators in the EU and the UK to make changes to the content of packaged retail investment and insurance products’ (PRIIPs) Key Information Document (KID) template in 2022, with EU authorities requiring Undertakings for the Collective Investment in Transferable Securities (UCITS) funds to produce a PRIIPs KID by the end of the year. Separately, work undertaken by ESMA in collaboration with EU national competent authorities last year on UCITS costs and charges, and the ongoing review of the implementation UK value assessment requirements, will increase regulatory scrutiny on the transparency, cost and performance of retail products.

Functioning of financial markets

Over the last year, EU and UK policymakers have undertaken several consultations assessing the potential effectiveness of proposals to improve the regulatory framework governing financial markets. Looking forward to 2022, we anticipate that policymakers will prioritise initiatives that seek to ensure the emergence of a privately provided consolidated tape (CT) of record for market data, alongside a reduction in complexity of pre- and post-trade transparency regimes. Indeed, the European Commission has already suggested rule changes to this effect.

Moreover, current market-wide reforms seeking to enhance the effectiveness of investment and market infrastructures, such as activities in respect of the London Interbank Offered Rate (LIBOR) benchmark’s cessation or the implementation of the EU’s settlement discipline regime, will also continue in 2022.

Digital Finance and Operational Resilience

In the year ahead, policymakers in the EU and UK will continue to encourage innovation and the emergence of digital products and services. While significant resources will continue to be put towards existing regulatory sandboxes and pilot regimes, we expect EU-wide and UK rules governing markets in crypto assets to be finalised alongside separate frameworks for the operation of market infrastructures based on distributed ledger technology (DLT). We also expect exploratory work on central bank digital currencies to continue next year, as well as initiatives relating to Open Finance and e-IDs; artificial intelligence; and the development of common data standards.

Finally, there will be a continuing focus, in 2022, on the implementation of EU rules governing cloud outsourcing while, in parallel, policymakers seek to finalise the EU’s new Digital Operational Resilience Act (DORA) within the first half of the year. In the UK, firms across the financial sector will likewise be focusing on implementing the regulatory changes necessary to comply with new rules relating to operational resilience which will apply from March 2022.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

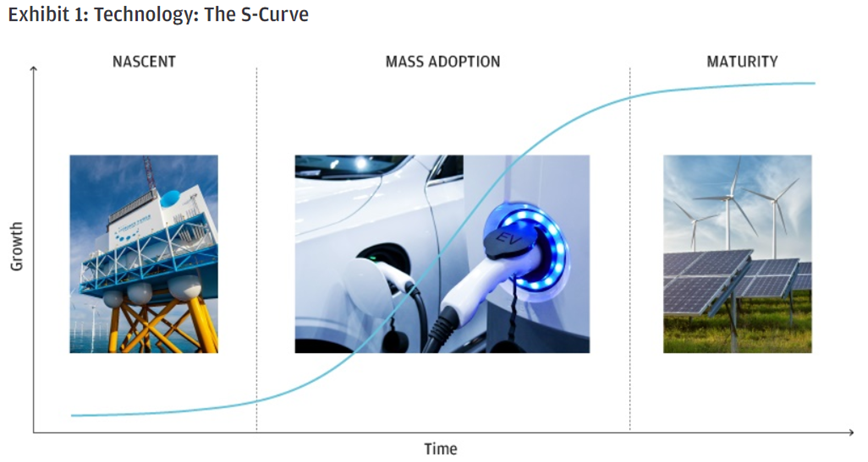

Please see below article received from J.P. Morgan yesterday, which reminds us that green technology is our ticket to a more sustainable future. Despite this, 50% of the technology we need to reach the world’s net zero carbon targets is not yet commercially viable, according to the International Energy Agency.

Meanwhile the other 50% is spread across both rapidly growing, innovative businesses, and more mature, profitable companies. As a result, green technology businesses find themselves at various points on what we call the S-Curve. This creates a range of very different opportunities for investors.

The S-Curve provides a framework for assessing almost every successful technology business since the first industrial revolution, with growth proceeding through three distinct phases – nascent technologies undergoing a burst of innovation, followed by exponential growth as mass adoption takes off, and finally reaching maturity.

Phase 1 – Nascent Technology

The nascent phase is the most volatile end of the curve. A new and innovative company faces a particularly wide range of possible outcomes, and the valuation will reflect the probability of these occurring. For example, a business may be valued at $1 billion today if investors believe there is a 10% chance it could be worth $10 billion in the future – but that valuation still implies a 90% chance it will be worth nothing. So while there can be massive upside if things go right, there is a significant risk it may not.

To move from the nascent phase to mass adoption, new technologies require a catalyst. In the green technology space, catalysts can include government initiatives, regulations, or consumer behaviour.

A good example is hydrogen technology – is it the future of decarbonising transport? The answer to this question may well depend upon the actions of governments. Following the COP26 summit, the US government made some encouraging statements about their plans for green hydrogen, which boosted stocks in the space. However, there still remain multiple fundamental issues, such as the volume of green power needed to produce meaningful quantities of hydrogen. Therefore, predicting whether this will be an area of focus for future government support is a fiendishly difficult task.

Those companies which do achieve mass adoption of their product can deliver windfall returns for early investors. Although it does not eliminate the risk of loss, diversification can be key to managing risk in this phase, as some technologies will simply never take off.

Phase 2 – Mass Adoption

Companies in this phase are those which have already hit their inflection point, leading to fast-growing revenues and a battle for market share.

In the green technology space, electric vehicles are the most visible mass adoption technology right now. Tailwinds here include government incentives and targets (the UK’s goal of banning the sale of new petrol and diesel cars by 2030, for example), as well as the growing number of charging points and advances in battery technology. With such forces behind them, it’s little wonder the likes of Tesla are enjoying huge revenue growth. Surely, it’s just a case of investing in a theme enjoying exponential growth and watching the returns flood in?

Not so fast. A technology theme may be thriving, but that doesn’t mean every company will be a winner. Far from it. In the mid-19th century, the railways were clearly set to be the backbone of Victorian Britain, but of the more-than 250 railway companies set-up, only a handful survived. In fact, a third of proposed rail tracks were never even laid. Some companies will be gaining market share, while others will see their costs spiral and profits suffer. Essentially we’re asking, who is going to be left standing?

There is another way to approach this phase of curve. A common saying is: during a gold rush, it’s best to be the one selling shovels. One way investors can get attractive exposure to the electric vehicles theme is through semiconductor companies, such as Infineon, which supply the chips all electric vehicles need to operate. Whether it’s Tesla, Volkswagen or another company that comes out as the dominant producer, they will all need semiconductors in their cars.

Phase 3 – Maturity

Once everyone who wants an electric vehicle has one, the industry will reach the mature phase of its growth. People may change their car every few years, as they do with their smartphones, but exponential growth will be over.

Wind energy is an example of a mature technology in the green space. Such businesses are no longer so reliant on government support, they generate predictable earnings streams, and many have high quality management teams. Wind farms often have power price agreements that can last for more than 25 years, which results in very stable cash flows.

One such leader in offshore wind is Denmark-based Orsted, a company that generates strong returns from its various projects and has been highly successful in winning large tenders. As investors, we’re interested in what we’re paying for such consistent earnings. This is where company quality becomes even more important, as just small improvements in cost of capital can dramatically increase project values and share prices.

Unlike early and mass adopters, pure economics is a larger driver of mature companies’ fortunes. We’re looking for attractive valuations, earnings visibility, and best-in-class management teams delivering profitable projects while reducing their cost of capital.

In Summary

Green technology isn’t just about trends, it’s about identifying the winners within those themes. For those companies which do grow to dominate the space, the rewards can be huge. Across the S-Curve, we focus on quality, valuation, and diversification – while also looking for the standout winners gaining momentum. Ultimately we aim to invest in the green technology companies that will power our transition to a more sustainable future.

Please check in again with us soon for more relevant content and insight.

Please see below this week’s Markets in a Minute update from Brewin Dolphin – received late yesterday afternoon – 05/01/2022

Global equities made solid gains in the final week of 2021 to start the new year on a strong footing.

A ‘Santa Claus rally’ helped the S&P 500 reach new record highs and end the week up 0.9%, as fears about Omicron waned. The Dow also gained 1.1%, while the technology[1]focused Nasdaq was flat.

The pan-European STOXX 600 and the FTSE 100 ended their holiday-shortened trading weeks up 1.1% and 0.2%, respectively, with the latter closing near its highest level for 2021, despite surging coronavirus infections.

Over in Asia, the Shanghai Composite advanced 0.6% following encouraging manufacturing data.

Last week’s market performance*

• FTSE 1001 : +0.17%

• S&P 500: +0.85%

• Dow: +1.08%

• Nasdaq: -0.05%

• Dax2 : +0.82%

• Hang Seng3 : +0.75%

• Shanghai Composite: +0.60%

• Nikkei2 : +0.03% *

Data from close on Friday 24 December to close of business on Friday 31 December.

1 Closed Monday 27 and Tuesday 28 December; early close on Friday 31 December at 12:30pm.

2 Closed Friday 31 December.

3 Closed Monday 27 and Friday 31 December.

US indices hit fresh record highs

The S&P 500 and the Dow hit new record highs on their first trading day of 2022, rising by 0.6% and 0.7%, respectively, on Monday (3 January). Easing concerns about the economic impact of Omicron helped to boost investor sentiment, despite rising case numbers. Bank stocks performed particularly strongly on speculation the Federal Reserve could lift interest rates earlier than expected.

The FTSE 100 also rose in its first trading session of 2022, gaining 1.6% on Tuesday to finish above 7,500 for the first time in almost two years. The IHS Markit/ CIPS manufacturing purchasing managers’ index (PMI) measured 57.9 in December, up from an initial reading of 57.6 although slightly below November’s three-month high of 58.1. Companies maintained a positive outlook at the end of 2021, with 63% forecasting that production would increase over the coming 12 months, compared to only 6% anticipating a contraction.

The STOXX 600 also rose by 0.8% on Tuesday, with travel and leisure stocks surging after the UK’s vaccine minister said Britons hospitalised with Covid-19 are generally showing less severe symptoms than before.

At the start of trading on Wednesday, the FTSE 100 was down 0.2% ahead of the release of the Federal Reserve’s December meeting minutes later in the day.

US jobless claims fall despite Omicron

US weekly jobless remained close to their lowest level for over 50 years in the week ending 25 December, showing the rapidly spreading Omicron variant has yet to impact employment. Initial claims for state unemployment benefits totalled 198,000, less than the 205,000 forecast by economists and 8,000 lower than the previous week, according to the Labor Department data.

US initial jobless claims

Continuing claims – which measures the number of unemployed people who have already filed a claim and continue to receive weekly benefits – fell by 140,000 to 1.72 million in the week ending 18 December. This was the lowest level since 7 March 2020, just before the first wave of Covid-19 lockdowns.

Investors are now waiting for the latest monthly employment figures, which will be released on 7 January. Economists polled by Reuters expect the unemployment rate to edge down to 4.1% in December from the 21-month low of 4.2% in November.

Festive retail sales soar

In another sign that Omicron is having a milder effect on economic activity, US retail sales surged by 8.5% during this year’s holiday shopping season (1 November to 24 December). This was the biggest annual increase in 17 years, according to the Mastercard data. Online sales grew by 11.0% compared to the same period last year, while sales at physical stores rose by 8.1%.

“Shoppers were eager to secure their gifts ahead of the retail rush, with conversations surrounding supply chain and labour supply issues sending consumers online and to stores in droves,” said Steve Sadove, senior adviser for Mastercard. “Consumers splurged throughout the season, with apparel and department stores experiencing strong growth as shoppers sought to put their best dressed foot forward.”

Covid restrictions tighten

Several countries in Europe tightened their coronavirus restrictions last week as infections surged to record levels. In France, where daily infections reached a new high, the government announced that from 3 January people must work from home if they can and public gatherings will be limited to 2,000 people for indoor events. Other countries cancelled official new year celebrations, and introduced limits on bar and restaurant opening hours.

Over in China, which is holding on to its zero-Covid strategy, 1.2 million people were placed into strict lockdown in Yuzhou in the Henan province this week, joining 13 million others who have been locked down in Xi’an for almost a fortnight.

China manufacturing PMI beats forecasts

China’s official manufacturing PMI beat forecasts in December, rising to 50.3 from 50.1 in November, according to the National Bureau of Statistics. Analysts had expected it to fall slightly to the 50-point mark that separates growth from contraction. Activity in the services sector also grew at a slightly faster pace in December, rising to 52.7 from 52.3 the previous month.

However, China’s vice commerce minister warned last week that the country faces “unprecedented” difficulties in stabilising trade next year. Export gains could slow as other countries recover their production capabilities and inflation eases, Ren Hongbin said.

To view the latest Markets in a Minute video click here

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.

Maximise tax reliefs and allowances. This will help you get more for your money when investing and planning. The obvious options are pension funding and using your ISA allowances. But we have plenty more to use if appropriate.

Have you any lazy capital sitting in cash? If you have a medium or long term investment horizon, consider investing some of it for real capital growth over time. Cash buying power is eroded by inflation over the long term.

Do you have any legacy pension and investment assets that have not been reviewed recently? Are they invested in line with your risk profile, capacity for loss and objectives? If not, you could be missing out on potential investment returns and/or taking too much risk.

Do you have any spare monthly income? If you have, you could invest it in either your pension or a Stocks & Shares ISA. Other investments are also available.

Get your ‘legal’ house in order:

Do you have up to date Wills in place? If not, please take legal advice.

Have you got both Power of Attorney in place? One for Finance and Property and the other for Health and Welfare: https://www.gov.uk/power-of-attorney

Are your pension nomination forms up to date on your current Workplace Pension and on any legacy pension assets? As these are potentially some of your biggest assets, it’s important that your nominations/Expression of Wishes reflect your current situation. They can drift out of date and legislation can and does change.

Please take independent financial advice and legal advice as appropriate.

Whilst any of the above won’t help you lose weight or get a (better?) beach body they could help you straighten out your finances for your financial good health.

All the best for 2022, have a happy, healthy and prosperous year.

Please find below an article detailing the impacts of Covid on stock markets and investments, received from AJ Bell yesterday – 19/12/2021

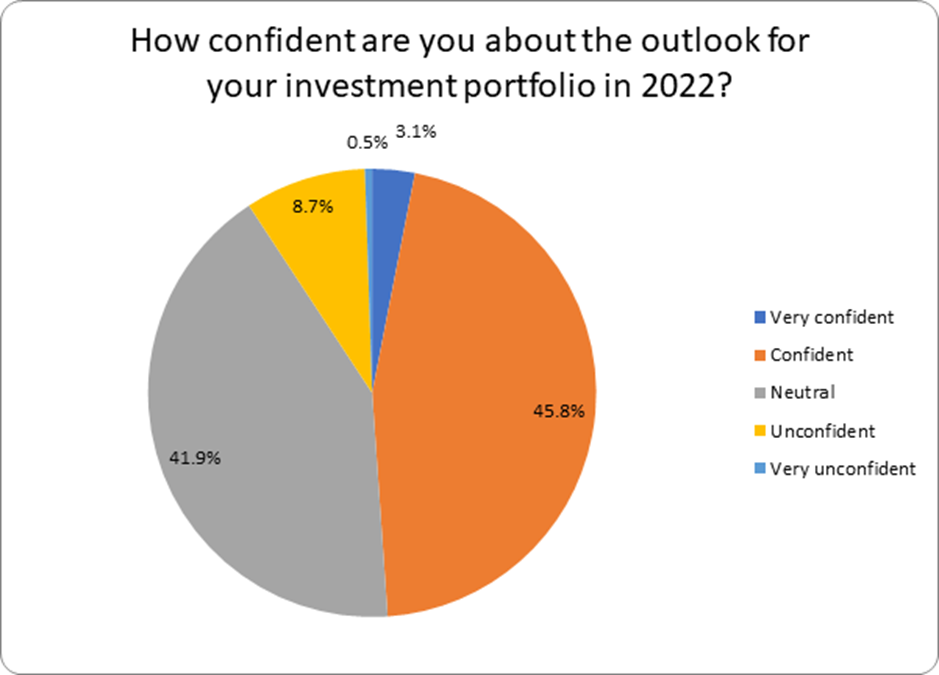

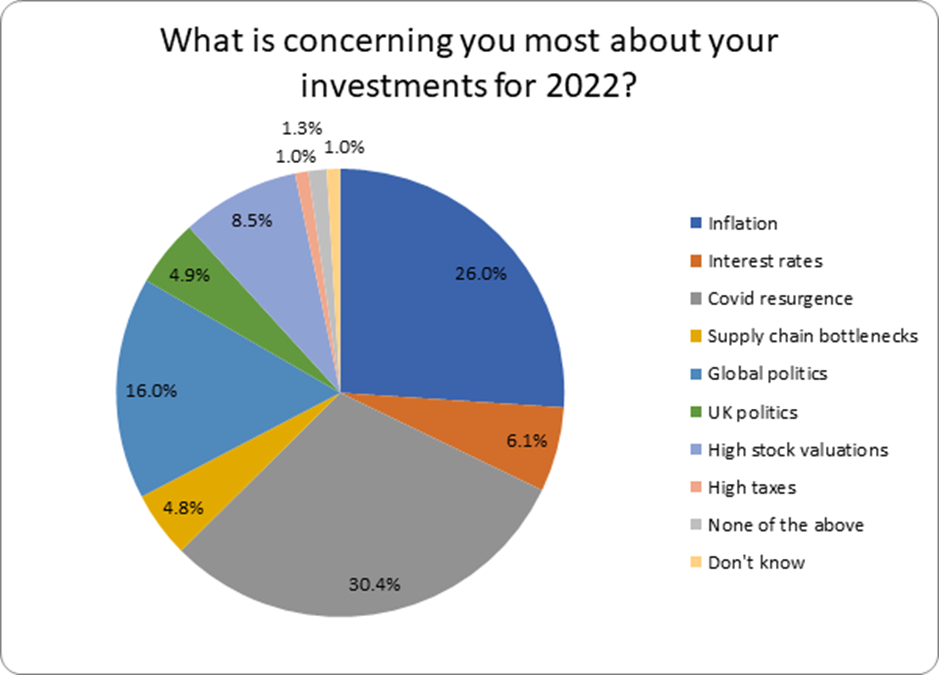

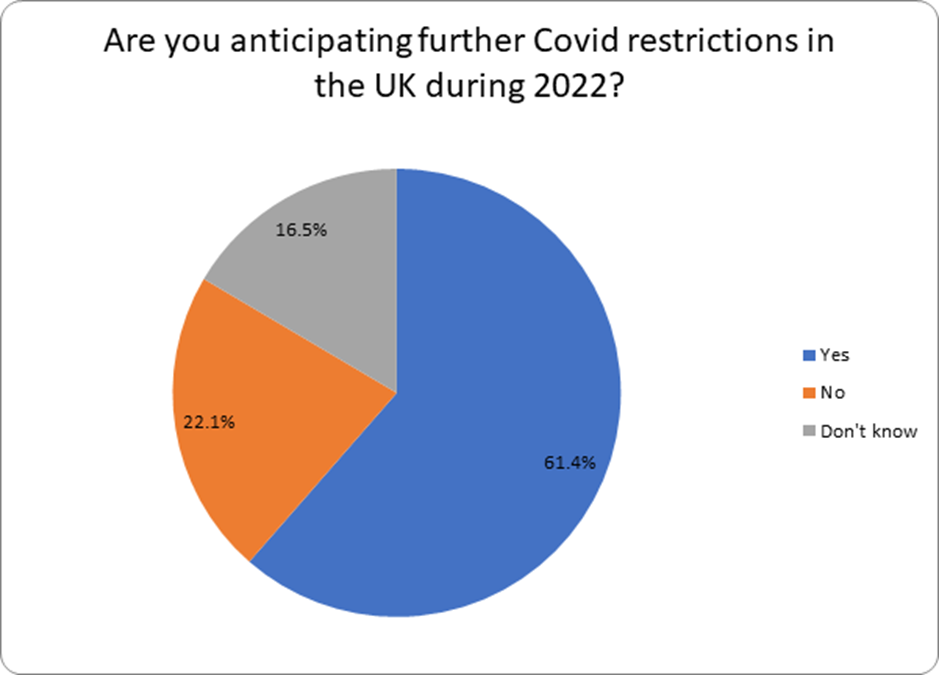

DIY investors are entering 2022 in a mood of constructive realism, recognising market risks, but also largely confident in their investments. Six in ten expect further covid restrictions in 2022, and a resurgence in the pandemic is the number one worry for investors as we head into the new year. Indeed, covid is seen as a greater risk than inflation, which makes sense seeing as the stock market provides some protection from price rises. Inflation comes a close second in the list of concerns for 2022 though, which shows investors are wary of price rises and the effect this may have on their portfolios. Global politics and high stock valuations are also cause for concern for some investors.

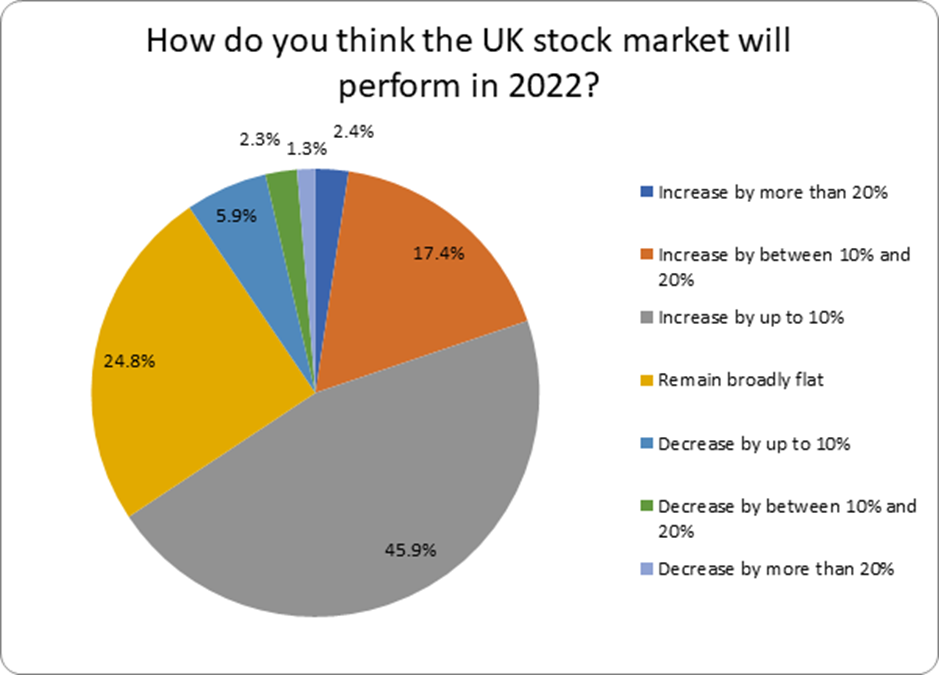

On the whole though, investors see the glass as half full rather than half empty. About 50% were confident or very confident about their investments in 2022, and around four in ten were neutral. That’s also reflected in forecasts for the Footsie, with two thirds of investors (65.7%) expecting the UK stock market to make further ground over the course of the coming year. Almost half of investors expect single digit returns in 2022, which suggests investors aren’t getting carried away, and are settling in for a more modest year for growth than 2021.

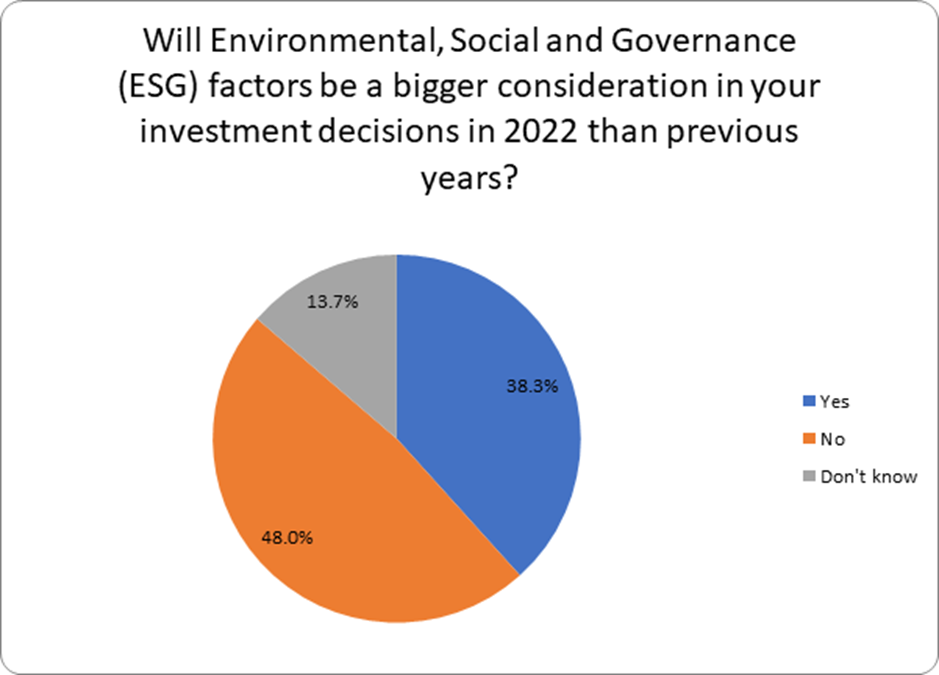

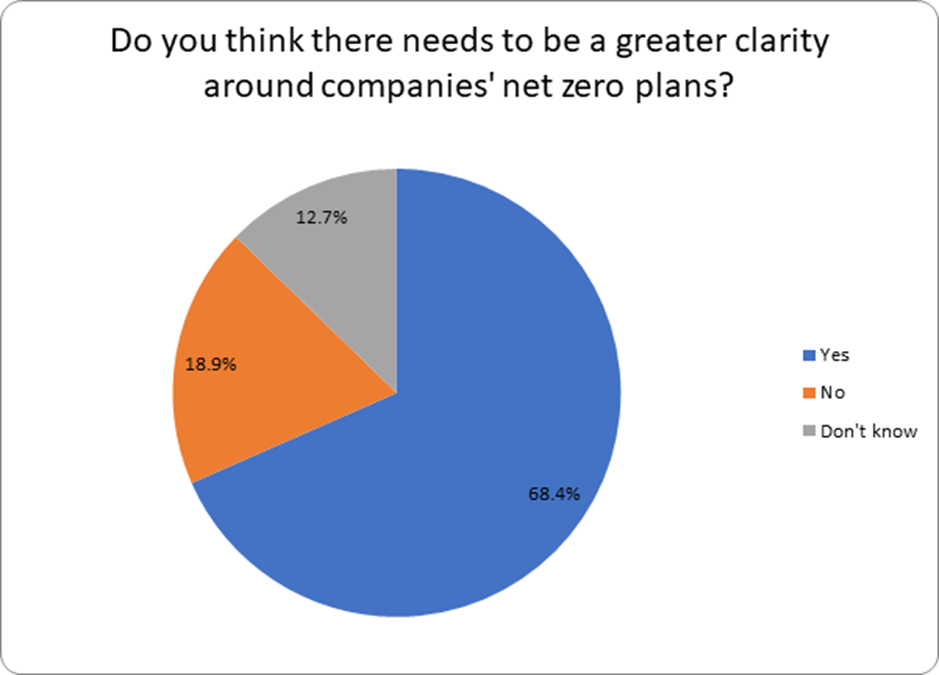

Investors are also becoming more attuned to ESG considerations, with four in ten (38.3%) saying these were going to play a bigger part in investment decisions in 2022. There’s already been a groundswell of interest in ethical funds in the last two years, and our survey suggests this isn’t going to abate in 2022. More than two thirds of investors also said they think there should be grater clarity over companies’ net zero plans.

The ESG agenda has developed so rapidly across the investment industry that the information available to investors is struggling to keep up. The FCA is formulating proposals on a new green labelling regime, expected in the first half of 2022, which should help make things a bit easier for investors seeking ESG investment options.

Please continue to check back for a range of blog content from us and from some of the world’s leading fund management houses.