Please see the latest weekly market commentary from Brooks Macdonald published yesterday evening:

US and European equities lose ground last week despite a late US rally on Friday

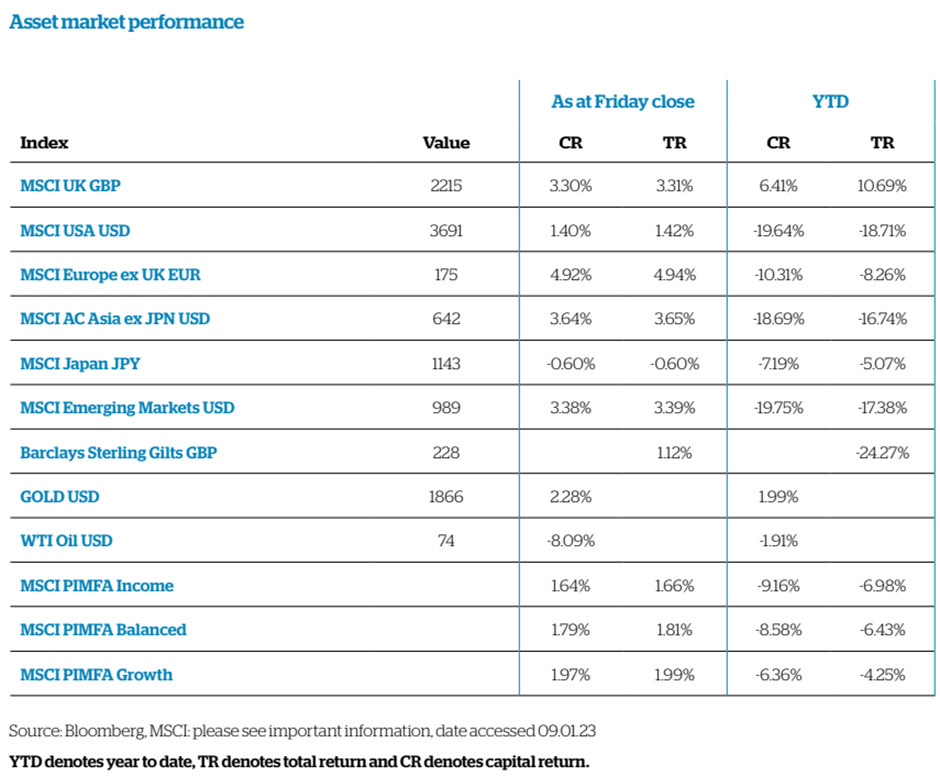

The strong equity market rally so far this year, slowed last week with the US and European headline equity indices falling slightly on the week. US equities rallied significantly at the end of last week which helped mitigate the index level losses. Technology outperformed with positive corporate news flow coming alongside an improving outlook for growth stocks as bond yields fall.

Economic data will be in focus this week with US Q4 GDP, Global PMIs and US lead indicators all featuring

With the US Federal Reserve now in its communication blackout window, the market’s focus will turn to the latest global economic data as well as commentary from ECB speakers. In a busy week for economic releases, highlights include the US Q4 GDP release on Thursday and global PMI surveys tomorrow. The Conference Board’s US leading indicators are out later today and are expected to continue to decline, which historically has been associated with a US recession. Last month the Conference Board said that they ‘project a US recession is likely to start around the beginning of 2023 and last through mid-year. On Friday we will see the latest Personal Consumption Expenditure (PCE) report which contains the Fed’s preferred inflation measure. PCE inflation and Consumer Price Index (CPI) inflation differ in important ways and therefore the market expects PCE inflation to remain stickier in the near term.

With the Fed in communication blackout, close attention will be paid to ECB President Lagarde today

Market attention will pivot towards the ECB this week with President Lagarde speaking later today. President Lagarde delivered a hawkish narrative when she spoke at Davos therefore today will be an opportunity to either double down on her rebuke of market pricing or start to become specific in terms of forward guidance. Over the weekend Dutch central bank head Knot told the market to expect at least two 50bp ECB rate rises (February and March) before the central bank downshifts again to 25bps. Lastly on central banks, the Bank of China is expected to hike by 25bps on Wednesday.

Behind the central bank rhetoric and economic data, corporate earnings are beginning to gain momentum. This week sees the start of the Big Tech results with Microsoft tomorrow and many of the other big names reporting next week. Tesla will release on Wednesday with investors eager to gauge demand for cars, which is highly cyclical, as well as electric vehicle demand more specifically.

Please continue to check our Blog content for advice, planning issues and the latest investment, markets and economic updates from leading investment houses.

Andrew Lloyd DipPFS

24th January 2023