Please see below the Daily Investment Bulletin from Brooks Macdonald, which was received early this morning (30/08/2024):

What has happened

Today marks the end of a remarkable month in markets – a cursory glance at current headline equity indices belies the hiatus that hit investors at the start of the month. Indeed, even despite the latest volatility in US megacap technology company Nvidia’s share price with its results earlier this week, markets have continued to recover their poise. As a case in point, the equal-weighted version of the US S&P500 equity index yesterday notched up a fresh record high. It was also a decent day in Europe yesterday with the pan-European STOXX600 equity index closing just a hair’s breadth beneath its all-time high that it hit back in May.

US GDP data pushes back on recession fears

Buoying the market’s positivity in the past 24 hours has been a better-than-expected US Gross Domestic Product (GDP) release (in real terms, adjusting for inflation), pushing back further on recession fears that worried markets in particular just a few weeks ago. The second estimate of US Q2 GDP was published yesterday, and it was even more positive than the first estimate that was released late last month. The latest US GDP print for Q2 was revised up to a quarter-on-quarter annualised growth rate of +3.0% and coming above the preliminary first reading for Q2 of +2.8%. Cutting the data another way, the Q2 year-on-year print now stands at +3.1%. All in all, these numbers really do not support a near-term US recession outlook, especially when you consider that the US Federal Reserve’s so-called ‘longer-run’ GDP assumption for US annual GDP growth is at +1.8%.

More data to end the month

Later today we get the latest US Personal Consumption Expenditures (PCE) monthly inflation reading for July. This data matters, but arguably especially so at the moment, given the US Federal Reserve (Fed) is at a pivotal inflexion point for its interest rate policy, with markets expecting the Fed to cut rates next month. As a reminder, the PCE inflation data is the measure that the Fed officially targets, so this will help inform the Fed as they look to shape their next policy choices.

What does Brooks Macdonald think

Anyone hoping for a meaningful thawing in the frosty relationship between China and the US could be in for a long wait. This past week has seen US national security adviser Jake Sullivan hold three days of talks in China, including a meeting with China’s president Xi Jinping. Of particular note, in his meeting with China’s Foreign Minister Wang Yi, Sullivan said the US would “continue to take necessary actions to prevent advanced US technologies from being used to undermine our national security”.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, an article from Brewin Dolphin providing a brief update on the key factors currently affecting global investment markets. Received last night – 28/08/2024

Equity markets globally continued to rebound last week, and the U.S. S&P 500 index was a whisker away from its all-time high. Recent economic data helped ease recession fears while Federal Reserve (the “Fed”) Chair Jay Powell announced on Friday, at a speech at the Jackson Hole Economic Symposium, that the time has come for the Fed to cut interest rates.

This is music to the ears of traders, households and businesses. There has been a lot of speculation and expectation (resulting in disappointment and confusion) over interest rates in the past year, so to hear such clarity of impending rate cuts from the Fed Chair is both pivotal and a relief. Despite the revelation, Powell fell short of suggesting how the Fed may proceed. Again, there’s an emphasis on data dependency and the assessment of the balance of risk. There’s no doubt that incoming economic data will continue to be scrutinised.

Does a downward revision in U.S. jobs growth matter?

Last week, the revisions to U.S. jobs growth data gained a lot of attention, though market impact was rather muted. Usually, these statistical revisions are a non-event, but any data release related to the labour market is heavily scrutinised by traders.

According to the U.S. Bureau of Labour Statistics, the number of nonfarm payroll positions (which exclude farm workers, private household employees, unpaid volunteers, business owners and some self-employed) will likely be revised down by 818,000 for the 12 months through March. That’s a bumper figure, and the biggest revision since 2009. It translates to about 68,000 fewer jobs created each month than previously thought.

I remember how stunning it was to see several nonfarm payroll releases announce gains of 300,000 jobs over the past year. It turns out the actual state of the U.S. labour market is much less robust.

Does that matter? Yes and no.

Yes, because it adds to the evidence of a cooling U.S. labour market and really seals the deal for a rate cut in September. We don’t know the distribution of this downward revision in job numbers – could it be more concentrated in more recent months? If that’s the case, the lagged impact of higher interest rates could be gathering pace (think of the ‘boiling frog’ syndrome). In this scenario, the Fed could be expected to end the current restrictive monetary stance as soon as possible to avert a recession.

Some economists may argue that no, the revisions don’t matter too much (even after sizeable downward revisions) because the job data was so robust, and the monthly pace of job gains was still a whopping 174,000 on average. This is still a healthy pace of hiring and a picture of economic resilience. The muted market reaction suggests the rate cuts are well priced in, and markets decided the data wasn’t too bad.

How low can the Fed go?

Beyond September, the question is: how much further can the Fed cut? Perhaps even the Fed has no idea given its dependence on data. We think barring a recession, the pace of rate cuts is likely to be measured.

The aggressive rate cuts priced in by the bond market appear to be overdone if the economy continues to expand. For instance, the Fed’s median interest rate projections (the so-called ‘dot plot’) suggest the Fed funds rate will be just above 4% by the end of 2025. That compares with about 3% currently implied by the Fed funds futures. While the next dot plot may see downward revisions, the current 100-basis point disconnect seems big.

If the U.S. economy continues to hold up, are the 100-basis point interest rate cuts priced in by markets for the end of 2024 and 2025 warranted? We think probably not. What we can learn from the past two years is that the market pricing of interest rates can change drastically. What is significant is that we’re moving into the next phase of the interest rate cycle. While we don’t know the exact quantum, the direction of travel of interest rates is highly likely to be south over the next 12 to 18 months – important information to consider for both businesses and households, for example if you’re holding a lot of cash or if you’re looking to buy a property.

The price of gold soars

As a result of the intensifying expectations of interest rate cuts by the Fed, the U.S. dollar has weakened notably across a basket of major currencies. Meanwhile, gold prices blasted past $2,500 to an all-time high last week.

Gold prices, which are denominated in U.S. dollars, tend to strengthen with a weaker dollar. They’ve been on a tear of late, having risen around 21% this year. Prices have been supported by increased central bank purchases, as emerging market central banks look to increase gold as a percentage of their reserves.

Gold, an asset traditionally expected to retain or even increase in value during times of market turbulence, has been a beneficiary of the ongoing geopolitical and economic uncertainty. It served as an effective hedge in the recent bout of equity market volatility, for example. Furthermore, gold prices have recently re-aligned with their fundamental driver: real interest rates. Gold prices tend to move in the opposite direction to real interest rates (for example, the higher the interest rates, the lower the gold prices) because gold generates no income.

With global central banks likely to cut rates simultaneously over the next six to 12 months, and U.S. growth moderating, the stars are aligned for gold to perform well and deliver as a portfolio diversifier.

The UK is recovering – but some fears of inflation remain

Turning to the UK, and there are more signs the economy is recovering. The latest purchasing manager indices (PMI) for manufacturing and services show both expanded more than expected in August. This is rather special, because manufacturing PMIs in the U.S. and the Eurozone both contracted in August. This sets a good backdrop for Q3 gross domestic product (GDP) growth – and don’t forget, GDP was already expanding at +0.6% in Q2 and +0.7% in Q1, respectively.

However, there are concerns that higher inflation will return. The large wage increases given to train drivers and junior doctors raise concerns on further public sector and labour union wage demands.

In addition, on Friday, energy regulator Ofgem announced an increase of 10% to the energy price cap from October. While expected, this risks feeding into consumers’ inflation expectations. The Bank of England (BoE) already expects UK CPI to re-accelerate to 2.7% in Q4 from the current 2.2%. As a result, markets are no longer betting that the BoE will cut interest rates again in September, with the next cut more likely to be in November.

Overall, the markets have priced in higher UK interest rates compared to those in the U.S. for at least the next 12 to 18 months. For instance, U.S. interest rates are expected to be at about 3% by the end of 2025, versus about 3.7% in the UK. This has contributed to the recent strength in sterling, which surged past 1.32 versus the U.S. dollar last week, meaning £1 now buys $1.32.

Please continue to check our blog content for the latest advice and planning issues from leading investment firms.

Please see the below daily update article from EPIC Investment Partners:

Following on from our Demographics Matter article we take a deeper dive into South Korea’s demographic crisis, characterised by an alarmingly low birth rate and a rapidly ageing population. Despite various government incentives to encourage parenthood, many young Koreans remain unconvinced that having children is a more worthwhile investment than pursuing personal fulfilment through luxury and leisure activities.

South Korea, Asia’s fourth-largest economy, has continuously recorded the lowest birth rate globally, a situation that shows no sign of improvement. Efforts to reverse this trend, including proposals to establish a dedicated ministry for demographic challenges, have so far failed to yield the desired outcomes. The lifestyle choices of Generations Y and Z, prioritising experiences over long-term commitments like marriage and parenthood, further complicate these efforts. Park Yeon, a 28-year-old fashion influencer, exemplifies this trend: “I’m all about YOLO (you only live once),” she says, prioritising self-reward and immediate happiness over saving for marriage and children.

It has been suggested that the younger generation’s tendency to prioritise status and online recognition over traditional markers of success, such as home ownership and family, contributes significantly to the declining birth rate. Jung Jae-hoon, a professor at Seoul Women’s University, points out that the high spending habits of young Koreans reflect their pursuit of personal and social validation, leaving little room for savings or family planning. Data indicates that the savings rate among individuals in their 30s has declined over recent years, despite interest rate hikes aimed at curbing consumer spending. Additionally, there has been a marked increase in spending by younger Koreans on luxury goods, high-end dining, and travel.

Financial concerns remain a significant barrier to childbearing, as highlighted in a recent survey by research firm PMI Co., where nearly half of the respondents cited job insecurity and education costs as the primary reasons for not having children. This economic strain, combined with the preference for immediate gratification, helps explain why government measures such as subsidies and extended parental leave have failed to reverse the trend. South Korea’s creation of a new ministry dedicated to demographic issues reflects a strategic shift, yet the cultural and economic barriers remain.

New analysis by Michael Clemens of the Peterson Institute for International Economics provides a fresh perspective on South Korea’s demographic dilemma. Clemens suggests the country could see a 10% decline in income per citizen within 18 years due to the ageing population, assuming no additional immigration post-2024. His research indicates that the shrinking labour force will diminish the productive capacity of the economy more rapidly than can be offset by increased capital accumulation or current pronatalist policies. This will result in a decline in per capita income, further exacerbated by the growing financial burden on the working-age population, who must support an increasing number of dependents, including both the elderly and children.

Clemens argues that traditional pronatalist approach might not be sufficient to counteract the demographic decline. Instead, Clemens suggests that temporary labour migration could play a crucial role in mitigating economic stagnation. Using countries like Malaysia as a model, South Korea could potentially alleviate pressure on its labour market and support economic stability. However, this economically promising approach raises important questions about migrant rights and integration.

To prevent severe economic stagnation and reduce the financial burden on the younger generation, tackling the demographic crisis in South Korea, and even globally, will require a comprehensive strategy that balances economic incentives with cultural and social shifts.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from Tatton Investment Management detailing their thoughts on markets over the past week. Received this morning 27/08/2024.

Late summer heatwave

Global stocks have turned things around from the early August sell-off. Up until the end of last week, the gains of the recovery were strong and remarkably stable. Last week’s main capital markets event was Federal Reserve chair Jerome Powell’s speech at the annual Jackson Hole central bankers conference. He basically confirmed a steep path down in US interest rates to start in September, and markets approved. This is good news, but investor optimism is a little unnerving; markets seem to be running a little hot.

For the S&P 500, the two-week period following the sell-off was in the top percentile of any two-week periods of the last 50 years. Daily gains were remarkably smooth – to an extent you rarely see. But many of the previous concerns are still here (slower growth and stretched US valuations) so we shouldn’t be surprised if another bout of volatility comes soon.

The dollar has weakened, seemingly because of slower US growth and the Fed’s expected cuts. But the US economy is still expansionary, according to the most reliable business sentiment surveys. Company earnings forecasts are going up too. Investors bristled at Kamala Harris’ interventionist economic proposals last week, but the election is unlikely to hurt strong corporate earnings too much regardless of who wins.

Markets are currently under a spell of ‘goldilocks’ mentality: they are happy with slower growth if it means lower rates. But this could be self-defeating. If valuations and corporate credit are supported enough by the goldilocks narrative, growth will be stronger after all, meaning less of a need for rate cuts. That is exactly the debate we have seen in recent weeks. Powell’s messaging was dovish, but if he keeps talking down US economic strength it could unnerve markets for the opposite reason. We could see another bout of short-term volatility. This isn’t a big problem for long-term investors, but we shouldn’t be lulled into a false sense of security.

Who’s afraid of UK wage rises?

The Bank of England cut interest rates earlier this month, and bond markets expect them to continue cutting over the next couple of years. But the monetary policy committee’s (MPC) more hawkish members keep warning about wage inflation. Opposition politicians have suggested that the government’s recent public sector pay rises are an example of this.

Put simply, though, we don’t think these public sector pay deals will materially affect inflation. BoE governor Bailey suggested as much earlier this month, and bond markets wouldn’t bet on more rate cuts if inflation was about to spike. Services inflation, which is more sensitive to wages, keeps falling and was below economists’ expectations in July. The drop in headline inflation will feed through to wages too, since many pay packets are indexed to CPI.

Hawkish MPC members argue that the recent inflation spike has structurally increased workers’ pricing power – and hence inflation pressures are higher – but these claims are hard to evaluate when cyclical effects are still being felt. Survey data from service providers suggest wage pressures are close to the long-term average, and growth seems to be as much to do with productivity gains as price pressures. If we were about to see a wage-price spiral from higher pay demands, all these indicators would be showing the opposite.

The UK rate cut path is not as steep as elsewhere for both cyclical (growth is improving) and structural (the BoE has a more restrictive legal framework) reasons. But bond markets have a benign inflation outlook, predicting another rate cut in the Autumn. Current public sector pay deals are more about ‘catch up’ after years of real-terms cuts – and those agreements tend to be short-run. The MPC has its hawks, but the majority opinion will be driven by the data, which points to a steady fall in rates. Nothing in recent wage data suggests otherwise.

The monopolistic seven?

Google is an illegal monopoly, according to a US federal judge. The Justice Department is reportedly considering breaking up the tech giant in response. That would be a huge blow not just to parent company Alphabet, but the entire ‘Magnificent Seven’ big tech stocks. The Mag7 dominated for most of this year, but investors have become concerned about their high valuations, leading to recent underperformance. Antitrust cases against tech giants would certainly give investors more to worry about – a sign that US politicians are cracking down on their market power. What happens depends on the upcoming election, but neither major party seems fond of silicon valley.

This isn’t a problem for the entire Mag7. Nvidia and Tesla can’t really be described as predatory monopolies, for example. But internet companies like Alphabet, Amazon and Meta are in many ways prime targets of antitrust litigation: they dominate new tech spaces, and actively limit competition by buying up competitors or investing to “make the ecosystem exceptionally resistant to change” (in the words of a former Google executive). Newer entrants can’t realistically compete without policy intervention – which makes it more likely it will come.

For a long time, US politicians were reluctant to pursue big tech; cases against Google and its ilk were mostly in Europe. This is probably because the US benefits from its national champions acting like monopolies abroad: capital flows back to the US, bolstering stock markets and tax revenues. That has changed under President Biden, and Washington now sees fewer benefits in giving its tech giants free reign.

It isn’t clear that the global dominance of US tech has helped American companies or citizens more broadly, for example, and most voters prefer government intervention to level the playing field. Antitrust pressure will not go away anytime soon.

Please continue to check our blog content for advice, planning issues, and the latest investment market and economic updates from leading investment houses.

Please see the below an article from Epic Investment Partners providing their thoughts on the jobs data and the anticipation of Powell’s speech at Jackson Hole:

This week, we have focussed on jobs data and the anticipation of Powell’s speech at Jackson Hole. Today we are turning our attention to a factor often overlooked but crucial for job creation: the growth of the working-age population.

Back in December 2000, the US working-age population was flourishing at a robust pace of 3.9 million annually. Fast forward to today, and the latest figures paint a starkly different picture, with growth estimates hovering at around 1.7m per year, compared to an overall population of 342 million. This slowdown matters because GDP growth relies heavily on the number of people employed and their incomes.

The US Congressional Budget Office (CBO) projections on US population growth are worth considering. While the population is set to reach 383 million by 2054, this growth is decelerating. More importantly, the civilian non-institutionalized population aged 25 to 54 – prime working years – is projected to increase at a mere 0.3% annually, a sharp contrast to recent decades.

The implications are clear: a slower-growing workforce means fewer people contributing to the economy, which can dampen GDP growth and put downward pressure on wages. While not necessarily negative, as real wages are what truly matter, this highlights that underlying demographics do not support sustained high inflation. Even achieving 2% inflation may be challenging given the ageing population and slower growth in demand from the working-age population.

While the US enjoys a more favourable position compared to countries like China, Japan, and Germany, where the working-age population is shrinking, the global trend of slowing working-age population growth cannot be ignored. This will put downward pressure on economic growth rates worldwide in the coming years.

So, while Powell’s speech and jobs data grab headlines, let us not forget the silent force shaping our economic future: demographics. Prior to the pandemic, bond yields had been falling for decades, in part due to the slowdown in the rate of population growth. So, it is conceivable that bond yields could return to those lower levels in the years to come once the current excessive budget spending in the US slows to more normal levels.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below an article from Epic Investment Partners providing their thoughts on the recent US economic data that has been published.

Earlier this week, we posed the question: “Where did the jobs go?” Yesterday, the Bureau of Labor Statistics (BLS) offered an answer, albeit an unsettling one. They admitted to an error in their estimates, revealing that the “true” payroll number for the year ending March 2024 was a staggering 818,000 less than previously reported.

The whereabouts of these missing jobs remains shrouded in uncertainty, a mystery even the BLS can’t unravel. However, the most likely explanation points towards the birth/death model as the culprit. This statistical tool, employed by the BLS to estimate job creation or loss from new business formations and closures, is a crucial component of the Current Employment Statistics (CES) survey.

However, the CES survey’s reliance on sampling established businesses inherently overlooks job fluctuations stemming from newly formed or recently closed enterprises. The birth/death model strives to bridge this gap, but the COVID-19 pandemic has dramatically disrupted business dynamics, making its application more complex than ever.

The surge in business formations during the pandemic and the subsequent unpredictable patterns have thrown off the statistical relationships and trends that the birth/death model relies upon. This could lead to significant inaccuracies in the BLS’s job estimates, potentially overestimating job growth during economic slowdowns and underestimating it during periods of improvement.

The implications of these revelations are far-reaching. Since the BLS cannot pinpoint the source of the errors, the payroll data will be adjusted by a flat 68,000 per month for the period ending March 2024. This casts a shadow over July’s already weak jobs report, suggesting the “true” number was much worse.

The trend of increasing errors over time adds another layer of complexity. While we cannot simply subtract 68,000 from July’s payrolls, it is highly probable that next year’s BLS revisions will reveal a much larger adjustment. Even an adjustment of 68,000 would bring July’s NFP reading down to a mere 46,000, well below the rate needed to prevent a rise in unemployment.

The Federal Reserve is not oblivious to the overstatement of job numbers. In last year’s Jackson Hole speech, Powell acknowledged the potential for inflated job growth figures due to the intricacies of the birth/death model amid the pandemic’s disruptions.

Expect this year’s speech to reiterate this concern. The new data provides the Fed with ample justification for rate cuts, perhaps as much as 50 basis points in September, especially if inflation continues its downward trajectory. The missing jobs, it seems, may pave the way for significant changes in US monetary policy.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from Brewin Dolphin, providing a brief analysis of the latest movements in global investment markets. Received last night – 20/08/2024

Japanese political drama

A lot of economic data and a few key earnings reports were expected last week. What was unexpected, although not entirely surprising, was the announcement from Japanese Prime Minister Fumio Kishida that he won’t take part in the race to become party leader in September, effectively resigning the premiership.

Kishida has been dogged by scandal this year, but still had a relatively long tenure of nearly three years; his predecessor served just over a year as prime minister, which is not unusual in Japan.

Kishida’s replacement will be important. Currently, the most popular of his potential replacements is former Defence Minister Shigeru Ishiba. He has expressed a desire to see Japanese monetary policy normalised, which seems the most pronounced threat to the Japanese economic status quo.

At the time, only Takayuki Kobayashi, the Minister of Economic Security, had declared his candidacy and he has yet to comment on Japanese monetary policy. There’s still plenty of time for other candidates to join the race.

Yields rose and the yen rallied upon Kishida’s announcement, possibly because of Ishiba’s stance. Nevertheless, the week saw strong performance from risk assets and Japanese equities. That could be because last week saw information that could support or refute the case against the U.S. economy. Is it plunging into recession, or is the consumer just taking a breather?

Overall, the data was reassuring. This meant less pressure for sharp interest rate cuts in the UK and it may even have rekindled the carry trade.

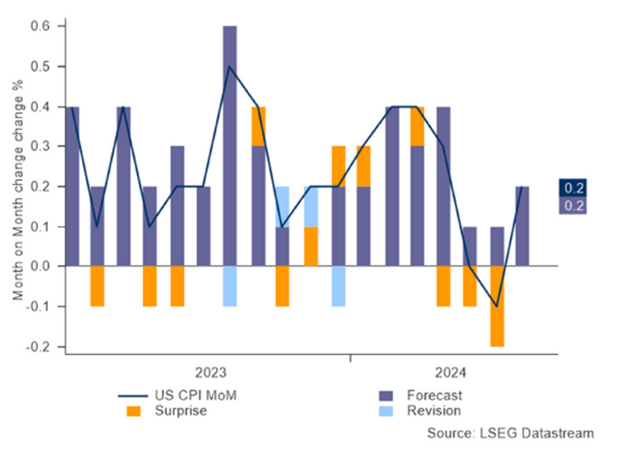

U.S. inflation

The U.S. consumer price index (CPI) was the most important monthly data for a long time, as inflation remained the main source of angst for investors. But weak price growth in May and June seemed to help investors channel their neuroses elsewhere.

Inflation’s certainly not the demon it was. Prices rose at 2.9% over the last 12 months, which is still too high, but well down on the 9% rate reached in June 2022.

Although headline inflation hasn’t dropped much in the last year, one of the bright spots about this month’s report was that it dropped below 3% for first time since June 2022. Since then, inflation has been stubborn and is unlikely to fall much faster over the coming months.

An alternative perspective

Investors, however, have learnt to look beyond the headline CPI rate. The Federal Reserve’s (the “Fed”) preferred inflation gauge is the personal consumption expenditure price index (PCE), but CPI gets the headlines because it’s released earlier in the month.

In terms of the differences between the two, CPI is increasingly reflecting increases in rental costs. For example, rent makes up 38% of the CPI basket and contributed 1.8% of the 2.9% rate.

Rental costs accelerated this month, which was very disappointing, but it’s not something to be worried about. We can say with enormous confidence that they’ll fall in the coming months, as the CPI basket, which measures one sixth of the rent revisions of the overall inflation basket, lags the timelier All Tenants Regressed Rent Index. The latter has been slowing rapidly and implies that the path of rental CPI normalisation has further to run.

To reflect the part of the economy that can actually be influenced by monetary policy, the Fed has placed more emphasis on a measure called ‘core services excluding rent’. This seems the most important number to take away from CPI, as it will influence how the Fed considers changing interest rates. When core services excluding rent declined in May and June, it suggested that inflationary pressures had finally been tamed. But having stripped out many of the volatile prices, what’s left really ought to be quite a stable number, so two months of declines seemed unsustainable.

This month, these prices rose by 0.21%, which would be consistent with a 2.5% annual rate. 2.5% CPI is only just above the equivalent 2% rate for PCE, so things are definitely moving in the right direction. These CPI numbers would not dissuade the Fed from cutting interest rates in September.

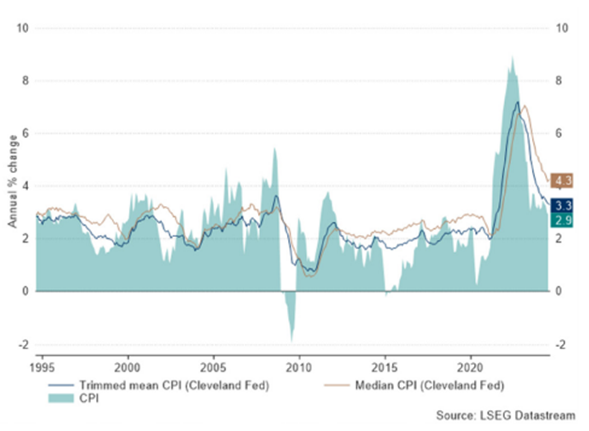

The only warning sign for policymakers here would be the persistence of alternative measures of CPI. Measuring price increases without the most volatile elements can be done by excluding food and energy (to give ‘core’ CPI), or it can be done by literally excluding the most volatile elements, no matter what they are (the ‘trimmed mean’ CPI) or by only measuring the median price increase each month.

These approaches show that inflation is slowing, but remains above the headline rate of inflation, and the most recent month actually saw prices increase. And that belies the true message of last week’s CPI report: that inflation remains above target, but not far enough above target to prevent the Fed from cutting interest rates when it meets in September.

The Fed believes rates are currently restrictive and can see a change in consumer behaviour, so it has become very concerned about the economy being too weak, and less concerned about inflation being too hot. Expectations that rates might be cut twice look wide of the mark though.

The UK economic recovery continues We also had the UK inflation report last week. It was biased by some volatile numbers, but again, the alternate measures of CPI, for example the median CPI, show that inflation hasn’t normalised yet.

In the UK, of course, interest rates have already been reduced. There’s also less evidence of the economy slowing.

Earlier in the week, it did seem as if there was a reducing number of job vacancies, but an apparent reduction in payrolled employees a few months ago has turned out to be a misestimate, which has been corrected by revisions.

The employment data are acknowledged as being unreliable due to low response rates to surveys. Fundamentally, it seems unlikely the labour market is particularly weak, because the economy has been picking up speed. Retail sales announced Friday morning reflected this, and the slowdown in inflation the UK has experienced so far, coupled with increases to the National Living Wage and the cut in National Insurance, have been wind in consumers’ sails.

What do U.S. retail sales tell us?

Flipping back to U.S. retail sales, and these were more upbeat than anticipated. We’ve heard a downbeat story from many retailers during earnings season, and this broadly continued with Home Depot confirming customers have spent more on wares to spruce their homes up over those required to perform major renovations.

Walmart saw similar focus on value from customers. It’s difficult to square with the official retail sales numbers. Perhaps the message that some retailers have seen things pick up a little at the start of August is the most telling.

What’s next?

The Democratic National Convention kicked off on Monday and will continue until Thursday. The conference began with President Joe Biden and former secretary of state Hillary Clinton endorsing Vice President Kamala Harris in November’s presidential race. While it’s unusual to see policy surprises at the convention, the change in nominee means the Democratic agenda is still being put together. If that does lead to any policy announcements, they’ll come later in the week.

Tim Walz, the current Governor of Minnesota and somewhat surprising vice-presidential nominee, will speak on Wednesday, while current Vice President and presidential nominee Kamala Harris will speak on Thursday.

This week will also see the publication of meeting minutes from the European Central Bank (ECB) and the Fed, as well as provisional purchasing managers indices for August.

Fed Chair Jay Powell and Governor of the Bank of England Andrew Bailey will both speak at the Kansas City Fed’s Jackson Hole Economic Symposium, which takes place between 22 and 24 August. The symposium features keynote speeches from prominent economists and policymakers. These speeches often provide insight into the Fed’s monetary policy thinking. They can also move financial markets and offer an opportunity to hear from some of the world’s most prominent central bankers.

Bank of Japan Governor Kazuo Ueda has a prior engagement and will instead attend a special session at Japan’s parliament to discuss the 31 July rate hike. This took the market by surprise and was seen as a significant contributor to the sharp sell-off in Japanese equities that took place thereafter. It will be a busy week for him.

Please continue to check our blog content for the latest advice and planning issues from leading investment firms.

Please see the below daily update article from EPIC Investment Partners:

As the financial world keenly observes the Jackson Hole Economic Symposium for clues about the future of monetary policy, another critical event looms on the horizon: the BLS’s Annual Benchmark revisions. While perhaps less captivating than a gathering of central bankers, these revisions hold the potential to shed light on a perplexing puzzle: if payrolls have been so robust over the past year, why has US employment growth been so lacklustre?

We’ve long observed a curious divergence between nonfarm payroll job gains and actual employment levels. From September 2020 to early 2022, these two measures moved in tandem. However, around March 2022, they began to part ways. The past 12 months have seen strong payrolls with an average of 209k new jobs added per month, totalling a healthy 2.51 million. Yet, over the same period, the employment level has barely budged, increasing by a mere 57,000. Even more concerning is the decline in full-time employment, which has dropped by 508,000.

The BLS relies on surveys and models to estimate economic data, but these estimates are often based on samples and can be subject to lags and revisions. Benchmark revisions, incorporating more comprehensive data sources, provide a more accurate historical record, although they can lead to significant changes in previously published figures. The 2023 benchmark revision, for example, resulted in a downward adjustment of nearly 500,000 jobs.

While the BLS rarely provides explanations for its revisions, one likely culprit behind the payroll-employment discrepancy is the birth/death model used to estimate job creation from new businesses. This model relies on historical trends and can be less reliable at economic turning points.

This is why we prioritise the unemployment rate, which is unaffected by these statistical adjustments. The recent surge in unemployment has triggered the Sahm rule (a simple but effective recession indicator that looks for a 0.5 percentage point increase in the three-month average unemployment rate from its recent low), suggesting a possible recession – a stark contrast to the more rosy picture painted by payroll numbers alone. Tomorrow’s BLS revisions may finally offer some clarity on this divergence. While the birth/death model may not be the sole culprit, the report could have significant implications for our understanding of the true state of the US labour market.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see the below article from Tatton Investment Management detailing their thoughts on global markets over the past week. Received this morning 19/08/2024.

Tornado rather than hurricane

The market storm looked like it would become a hurricane in early August, but it ended as fast as whirlwind: stocks climbed last week without hesitation. Positivity is good, but a little unnerving. Our medium-term outlook is bright, but there might be further storms ahead.

Last week’s recovery was helped by surprisingly good economic data – including 0.6% Q2 growth for the UK. Markets mainly got excited about US retail sales, which grew 1% month-on-month in July. US consumers are still proving the doubters wrong – counter to the recession fears in recent weeks. If unemployment was about to spiral, consumption would be the weakest part of US data, but in fact it’s the strongest.

We shouldn’t get ahead of ourselves though. A ‘soft landing’ (growth slows without going negative) is on the cards, but not a ‘no landing’ (growth doesn’t slow at all) scenario. Markets reacted like July’s figure was great news, but month-to-month data is noisy and next quarter’s profit growth still looks likely to be a little soggy. We can’t tell yet if market optimism is justified – but should get a better idea after central bankers’ Jackson Hole conference.

In other news, a US judge ruled that Google illegally monopolised the search engine market, and the Justice Department is reportedly considering breaking up the tech giant. That would be terrible news for US tech – a signal that regulators will tackle their market power. We suspect a Harris administration would be tougher on them than a Trump one, but anti-tech sentiment is a rare point of bipartisanship in Washington.

Finally, there is talk that the Bank of Japan might be able to cut rates in December after all. That would add to yen strength, which would benefit neighbours China. Maintaining a renminbi-dollar peg amid a falling yen has forced China into tight policy, so if the yen strengthens authorities will be able to loosen their grip.

Would ‘Kamalanomics’ mean US fiscal expansion?

Vice-President Kamala Harris is now the slight favourite to win the US presidential election, across polls, betting markets and most forecasts. She has begun to announce policy measures – mostly focused on support for children and families. But the market implications of a Harris presidency are unclear, largely because she had been tactically vague on the big issues. Neither party is likely to win a clean sweep (the House, Senate and Presidency), so we will probably see a degree of policy gridlock and status quo anyway.

It isn’t a given that Harris would continue President Biden’s economic agenda, given Americans’ disapproval of his handling of the economy. If she wants to distance herself from unpopular parts of his record, she will likely focus on lowering inflation. That could make her administration more fiscally disciplined than either Biden or Trump. However, she will likely extend time-limited Trump-era tax cuts that are set to expire, which could push Trump to promise more tax giveaways (he has already suggested making the time-limited cuts permanent).

US fiscal metrics have deteriorated under Trump and Biden, but there has been no ‘Liz Truss moment’ in treasury bonds, thanks to America’s status as the world’s leading market. This invulnerability is harder to maintain the worse debt metrics become, particularly if coupled with tariffs that limit capital inflow. External observers have warned there is not much capacity to expand US fiscal policy further – but that is unlikely to stop Trump from trying.

While neither party will be fiscally conservative, we suspect Harris will be less willing or able to run the risk of a ‘Liz Truss moment’. Both candidates will probably be tempted to offer ‘giveaways’, given the lack of public concern over the budget. Just like in the UK, opposition to fiscal expansion will come from bond markets, if at all. And just like here, any turmoil would probably be a short-lived buying opportunity.

The long-term case for Japan

Despite an intense market shakeout, the long-term case for Japanese assets is strong. Profitability has improved, thanks to corporate reforms. These should help companies’ capital efficiency – which is much worse in Japan than the US or Europe. Firms have become less averse to foreign ownership, and shareholders appear more willing to vote against company directors. The shakeout of speculative investors this month should actually help here, aligning incentives more toward long-term profitability.

The yen is still cheap, despite sharp recent gains (it was ¥100 to the dollar at the start of 2021, and it is ¥148 at the time of writing). That, together with comparatively low inflation, means Japanese labour (among the world’s most highly skilled) is highly competitive in dollar terms. Exporters seem to be reaping the benefit, as shown by Honda’s recent earnings. Many company outlooks assume a ¥140-to-the-dollar rate, and the Bank of Japan’s structural dovishness means it is likely to stay there or weaker.

Growth has been disappointing, but the comprehensive picture is arguably better than individual indicators. Export growth should feed through into stronger domestic demand, which Goldman Sachs note has been decent. Exporters will get a profit boost even if domestic demand is lethargic, and in any case Japan’s equity valuations are very cheap (a reflection of weaker growth). To stay that cheap, you would have to assume that growth will be as weak as it has been recently.

We have little reason to be that pessimistic. Japan is not suddenly seeing a ‘new dawn’ or an end to its long-term malaise, but its long-term profit outlook is improving. Since stock values are based on those earnings, and Japan remains cheap in terms of currency and valuations, the long-term case for Japan still looks solid.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see Brooks Macdonald’s Daily Investment Bulletin covering their thoughts on global markets:

What has happened

Equity markets were in confident mood on Thursday. Buoying the economic outlook and pushing back on recession worries, yesterday’s US weekly initial jobless claims data was better than expected for the second week running. Initial claims fell by -7,000 in the week to Saturday 10th August, to 227,000 and below the Bloomberg consensus estimate of 235,000. The continuing claims number also fell. Reflecting the better news, the US S&P500 equity index ended yesterday up +1.61% in US$ terms. It is now up +8.28% above the intra-day low it reached last Monday (5th August) and is now only -2.19% below its record all-time high … a reminder for investors of the risks of trying to time short-term market exit and entry points. Within equity markets, as well as megacap US tech shares leading, smaller company share prices also outperformed with the US Russell 2000 equity index up +2.45% having its best day in four weeks. European equity markets also gained on Thursday, with the UK, French, and German equity markets all up on the day.

US recession positioning dealt a blow by better retail sales

Anyone still positioning for an impending US recession were dealt a blow by US retail sales yesterday. US retail sales month-on-month (MoM) saw their biggest gain since January 2023, up +1% MoM, and easily surpassing the consensus estimate of +0.3%. That the previous month saw a small downward revision didn’t seem to impact the positive market reaction. Adding to the resilient consumer picture, US retailer Walmart came out with better Q2 results yesterday and raised its sales and profit outlook for the full year as well. Walmart shares ended the day up +6.58% and notched up a new record closing high. Walmart CEO Doug McMillon summed up the view neatly, saying that “we aren’t experiencing a weaker consumer”. For completeness, it would be remiss not to mention that US industrial production numbers for July missed estimates yesterday, recording the first annual drop in three months – that said, the weakness was put down to the recent weather impact from Hurricane Beryl impacting factory certain factory activities.

China’s economic malaise continues

The economic malaise in China has continued into the calendar Q3, according to Chinese government data published yesterday. The standout was a surprise slowdown in fixed asset investment, to +3.6% for the first seven months of the year (versus the same period last year). It was below consensus estimates and is the fourth month in a row of declining growth rates. Industrial production growth was also weaker than expected and the third month in a row of falling growth rates. While retail sales looked better, it was thought to be largely down to a seasonal uptick and remains well below pre-pandemic levels of growth. Elsewhere, China’s arguably all-important housing market continues to be problematic: new home prices fell -4.9% year on year in July, the sharpest annual drop since June 2015, and deeper than the -4.5% slide in June.

What does Brooks Macdonald think

Economic performance doesn’t necessarily always correlate to equity market performance, but in China’s case this year, they are both suffering. So far in 2024, against the MSCI World (developed markets) equity index up +14.0% in US$ total return terms, China is lagging, up just +3.1%. And for context, China’s relative underperformance in FY 2023 was much worse. This has led to some to suggest China is worth looking at, if only on valuation grounds – but we continue to see China more of a value trap than a value opportunity. China’s policy makers are stuck between a rock and a hard place – desperate to deleverage the economy after decades of overbuilding in its property market in particular, this, more than anything else perhaps, explains why Beijing appears to be so reluctant to sign off on a large-scale fiscal stimulus to pump up growth rates.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.