Please see the below article from Tatton Investment Management detailing their discussions surrounding the ongoing Trump Tariff saga and how trade markets are responding. Received this morning 02/06/2025.

Complacency or checks and balances

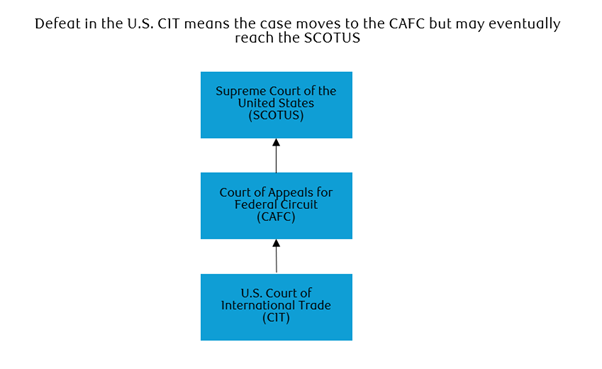

The pullback a couple weeks ago has proved just a blip, thanks to the TACO trade (Trump Always Chickens Out) and a US trade court ruling Trump’s tariffs illegal (though the ruling was quickly suspended). Markets were happy but the previously “Mr Nice Guy” president was furious.

So we expected and got some Nasty Trump. On Friday, steel and aluminium tariffs were raised from 25% to 50%, probably signalling a greater focus on sectoral levies. While there is probably more internal logic to a sector-based approach, this makes country-based negotiations generally more complicated and certainly disrupts current talks. Deadlines are unlikely to be hit.

The start-date for the increase is Wednesday but, given his beef with the chicken jibe, there is virtually no hope of a Trump back-down.

The end of the Q1 US earnings season has been resilient. Nvidia continued to show the AI boom is driving profit growth. Meanwhile, US consumers are still showing some confidence and previous recessionary signals have faded. This helped credit spreads come down and financial conditions ease. The main problem now is that economic strength will prevent the Federal Reserve from substantially cutting interest rates – especially since companies are still retaining employees.

It’s notable that markets took the court’s tariff ruling so well, considering bond investors have been fretting about government debt. Tariff revenues are necessary to fund Trump’s tax cuts, and that’s why the Republican-controlled Congress will almost certainly hand tariff-setting power back to the president.

Unlike the US, the UK is signalling some fiscal discipline but a little less so. Everyone expects tax rises to fund the budget gap, and Reeves intends to keep to the rules – except that she might change those rules to allow more investment spending, given that the IMF helpfully suggests she cuts herself some slack. Any such change will give the UK a one-off boost, raising overall debt levels and increasing probably, marginally, increasing the interest burden. Nevertheless, on balance, the policy mix is likely to improve long-term stability, helping rate expectations and sterling. It’s just unfortunate that our borrowing costs are still heavily tied to the undisciplined US.

As for the fights a wounded Trump might pick, the Fed independence question could rear its head again. The Supreme Court recently suggested the president could fire who he wants, but curiously signalled an exception for the Fed. Jerome Powell shouldn’t get too comfortable though, as many in the White House are looking to test the bounds of executive power.

Meanwhile, China’s economic weakness is being taken as evidence that Beijing might play nice – but this might be mistaken. Beijing could well replace economic prosperity with nationalist expansionism, like a rumoured Taiwan blockade in the autumn.

But markets are more focussed on the positives. We hope that’s a good sentiment sign, rather than complacency.

The end of US exceptionalism?

By “American exceptionalism” we mean the dominant of US asset performance over the last decade and a half, particularly in stocks. This shouldn’t be confused by the political theory of American exceptionalism – though the shared name is no accident; both about people believing that the US is exceptional. This has manifested in US assets being the best and safest earners in tangible (Sharpe ratio) and intangible (reserve currency safe haven, stable business-friendly government) terms. We’ve written before about how the US’ current account deficit typically returns as a flow of dollars into its asset markets. That, combined with US businesses’ focus on high profit industries, has led to corporate profits and equity valuation outstripping the world.

But Trump’s erratic policies are undermining both pillars of American exceptionalism: high returns and low risks. His obsession with balancing the trade deficit would undermine the flow of dollars back into asset markets, but even without that the uncertainty is preventing business investment and souring consumer sentiment – which dampens long-term returns. That uncertainty also makes US assets riskier, like the spike in volatility we saw post “Liberation Day”. It’s telling that the dollar has not recovered in line with US stocks recently, suggesting the safe haven status has been weakened.

The end of US exceptionalism doesn’t mean bad returns; the US economy is too resilient for that, and ‘buy the dip’ mentality is too strong. But it means returns will be less world-beating. That’s a problem for American companies – as their high stock valuations depend on capital inflows which have already started reversing this year. We expect that trend to continue, as long-term institutional investors reduce their portfolio allocations to the US. This might only be a marginal change – but a marginal change on such a huge part of global markets means a big impact on global markets.

China’s Belt and Road

US trade isolationism has many wondering if China could capitalise – perhaps through its Belt and Road Initiative (BRI). More than 150 countries have signed BRI agreements with China, which typically provides capital and labour for overseas infrastructure. Westerners often consider the BRI a foreign policy tool, but it was originally a solution to economic imbalances: China had too much capital and construction capacity, but needed access to materials.

Some accuse Beijing of “debt trap diplomacy”, as BRI agreements are opaque and have left poor countries facing high debt payments. Foreign policy experts don’t find this accusation credible, and many BRI agreements have been mutually beneficial – particularly with Latin America, which now trades more with China than it does the US.

Beijing would struggle take advantage of US isolationism, though, and BRI investment has slowed in recent years amid an economic downturn. Beijing domestic stimulus programs take precedence over building trade ties. The trade ties China is building seem mostly practical – ‘connector’ countries on route to the US.

Cutting off China is also part of the US’ plan – as seen in Panama abandoning its BRI deal after a visit from Washington. The Trump administration also made sure to include anti-China measures in its trade deal with the UK, and is reportedly planning to do the same for any EU deal. The US wants to force its trade partners to chose between the world’s two largest economies.

There’s no guarantee everyone will pick America, of course. Brazil’s Lula recently declared he wants “indestructible” relations with China, at a conference of 33 Latin American and Caribbean countries in Beijing. President Xi notably promised to back Panama against US threats at that meeting, showing how the US’ hard line could backfire. A Chinese-dominated world trade order is unlikely but, amid US aggression, many leaders will like the sound of Xi’s promised multipolar world.

Please continue to check our blog content or advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

02/06/2025