Please see the below article from Brooks Macdonald detailing their discussions on the ongoing conflict in the Middle East and interest rates. Received this morning 20/06/2025.

What has happened

Global equity indices were lower on Thursday, as a US decision whether to attack Iran appeared to remain on a knife-edge. Later, with US markets shut for “Juneteenth” holiday and after European markets had closed for the day, US President Trump gave a message effectively saying he was giving Iran up to 2 weeks to negotiate a deal aimed at limiting Iranian nuclear capabilities. With Middle East escalation paused for now, oil prices are down overnight while most Asian equity markets are up this morning.

Middle East

White House press secretary Karoline Leavitt last night delivered a dictated message from Trump, saying that “based on the fact that there’s a substantial chance of negotiations that may or may not take place with Iran in the near future, I will make my decision whether or not to go within the next two weeks.” Meanwhile, the US has continued to build up its military presence in and around the Middle East – the US Navy’s newest and most advanced aircraft carrier, the USS Gerald Ford has this week been ordered to deploy to the Mediterranean Sea and is set to become the third US carrier strike group to be positioned in or near the Middle East.

UK interest rates on hold

While UK interest rates yesterday stayed at 4.25% as expected, the Bank of England’s 9-member Monetary Policy Committee (MPC) saw a surprise dovish split: 3 MPC members voted for a 25 basis point cut, 1 more than expected, and versus 6 MPC members who voted for no change. In addition, Bank minutes released yesterday echoed the context for more possible cuts later this year, citing weak economic growth and clearer signs of loosening in the UK labour market. Looking forwards, the Bank continued to see the “gradual and careful” withdrawal of monetary policy restraint remaining “appropriate”.

What does Brooks Macdonald think

With the surprise dovish tilt to the Bank of England’s latest meeting this week, that has fed into the UK interest rate outlook. Looking at market expectations yesterday afternoon, based on derivative option pricing, that pointed to 50.1 basis points (bps) of cumulative interest rate cuts by the Bank of England’s December meeting later this year, with a first 25 bps cut fully-priced-in for the Bank’s September meeting.

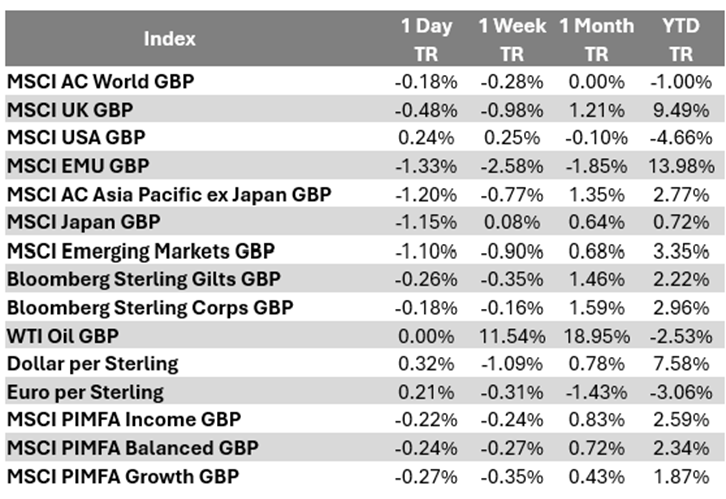

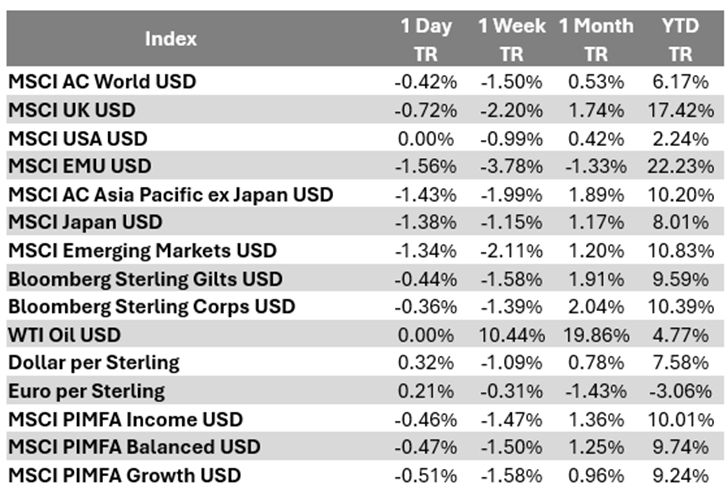

Bloomberg as at 20/06/2025. TR denotes Net Total Return.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, Evelyn Partners thoughts on today’s Bank of England interest rate decision:

What happened?

Coming hot on the heels of the Federal Open Market Committee leaving US interest rates unchanged last night, the Bank of England (BoE) followed suit with a widely expected ‘hold’ in their midday release keeping their target rate at 4.25%. This is a continuation of the one-cut-every-other-meeting approach since the current easing cycle began last August.

The vote was split 6-3, versus the 7-2 shown by the Bloomberg survey, with Dave Ramsden joining external members Swati Dhingra and Alan Taylor on the dovish side, preferring to reduce the Bank Rate by 25 basis points, to 4.00%.

The meeting did not come with updated forecasts, but guidance recognised ‘there remain two-sided risks to inflation’ with the ‘gradual and careful approach to the further withdrawal of monetary restraint’ reiterated.

What does it mean?

The focus of Bank watchers was if the news flow had been enough to sway members in the dovish direction… and clearly it had.

Since the May Monetary Policy Report, the Monetary Policy Committee (MPC) has seen two rounds of GDP, inflation, and labour market releases. Overall, the economy has proved to be more resilient than the MPC expected with the latest data coming in with quarter-over-quarter growth at 0.7% (versus 0.6%), inflation slightly hotter at 3.4% (versus 3.3%) but with the labour market softening quicker than expected. Unemployment rose to 4.6% in the three months to April (ahead of the BoE’s 2Q25 projection) and HMRC’s latest PAYE Payrolled Employees Monthly change came in at -109k (vs 20k surveyed). Wage momentum, while still elevated with average weekly earnings 3-month/year-over-year at 5.3%, showed progress coming in below the anticipated 5.5%.

Outside of the domestic data releases, marginal progress has been made on the trade front with the ‘UK-US Economic Prosperity Deal’, the ‘UK-India Trade Deal’ and the new UK-EU deal all small positives for the UK’s growth outlook. However, economic policy uncertainty remains elevated globally with geopolitical developments in the Middle East further muddying the outlook.

Bottom Line

The BoE held interest rates steady at 4.25%. The UK swap market is pricing in an 85% chance of a cut at its next meeting in August and one further cut through to the end of 2025. Given Ramsden’s reputation as a bellwether on the committee, it will be interesting to see if weakening labour market data encourages more committee members to start look through inflation concerns, resulting in the pace of quarterly rate cuts picking up.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below, todays Daily Investment Bulletin from Brooks Macdonald covering their thoughts on markets and the ongoing Geopolitical Issues:

What has happened

Yesterday saw global equity markets seesaw as US President Trump left everyone guessing whether the US would join Israeli attacks on Iran. Elsewhere, the US Federal Reserve left rates unchanged as expected – the Bank of England announces its latest interest rate decision (also no change expected) at 12 o’clock midday today UK time. US markets are shut today (“Juneteenth” public holiday), so expect trading volumes to be lighter elsewhere.

Middle East

While Trump said yesterday that Iran had reached out about the possibility of negotiations, he said that he hadn’t yet made his mind up about US military strikes. Yesterday the Wall Street Journal reported that Trump had privately approved of attack plans but had held off on the final order. Overnight, Bloomberg has reported that US officials are preparing for a possible US strike on Iran in the coming days.

US Federal Reserve

As widely expected, the US Federal Reserve (Fed) left interest rates unchanged yesterday for the fourth meeting in a row, at a range of 4.25-4.5%. As for Fed members’ rate expectations ahead, the median estimate for -50bps of cumulative cuts by calendar 2025 year end was also unchanged. There was a small hawkish shift however – more Fed members see no cuts at all this year, while the median rate expectation was nudged up for 2026 and 2027.

What does Brooks Macdonald think

Reflecting tariff risks, Fed members nudged up inflation expectations for 2025 and 2026, while economic growth was nudged down. Feeding into our more cautious outlook recently, the risk is that the tariff impact eventually shows up in the economic data, albeit with a lag. As Fed Chair Powell said yesterday, “ultimately, the cost of the tariff has to be paid, and some of it will fall on the end consumer … we know that because that’s what businesses say, that’s what the data say from the past.”

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 17/06/2025.

Markets calm despite conflict in the Middle East

Despite the recent conflict in the Middle East there has been a surprising lack of market movement.

Source: LSEG Datastream

On 12 June, 2025, Israel launched a series of airstrikes targeting Iranian nuclear and ballistic missile facilities, scientists, and senior military personnel, marking a significant escalation in the long-standing conflict between the two nations. The attacks reportedly damaged the Isfahan and Natanz uranium enrichment facilities, whilst also striking the Fordow but with limited success.

Iranian state media confirmed the killing of the Commander of Iran’s Islamic Revolutionary Guard Corps (IRGC), Hossein Salami, however it is the attacks on the nuclear facilities which is of greatest strategic importance as the actions taken so far would slow but not prevent Iran’s progress in enriching uranium to the grade required to develop a nuclear weapon.

In recent months, Iran has made rapid advances in its uranium enrichment activities, with the International Atomic Energy Agency (IAEA) finding Iran in breach of non-proliferation obligations. Israel’s Prime Minister, Benjamin Netanyahu, stated that Iran has enough enriched uranium for nine atomic bombs and insisted that the preventive action was necessary to avert a full-scale nuclear crisis. Israel has indicated that ending that progress is its objective, and it has a strategy to achieve it over a number of weeks.

The situation is volatile, and there is a risk of a wider conflict involving other regional actors. For now, Israel and Iran have been exchanging fire with Israel expanding targets to include energy infrastructure. A particular focus is on the U.S., whose involvement would mark a clear escalation but is assumed to be required in order to do lasting damage to the Iranian nuclear programme. President Trump’s comments on the subject have been vague and laced with implicit threat but so far, the U.S. official line is that it is not a party to this conflict.

Possible options for an imperilled Iran would be disruption of traffic through the narrow strait of Hormuz, however the U.S. Fifth Fleet’s presence in Bahrain makes it unlikely that this can be achieved for an extended period.

The market reaction has been fairly benign so far. That reflects hopes that the conflict can be contained and an assumption that we won’t see the kind of global energy supply interruptions which occurred in the 1970s.

Source: LSEG Datastream

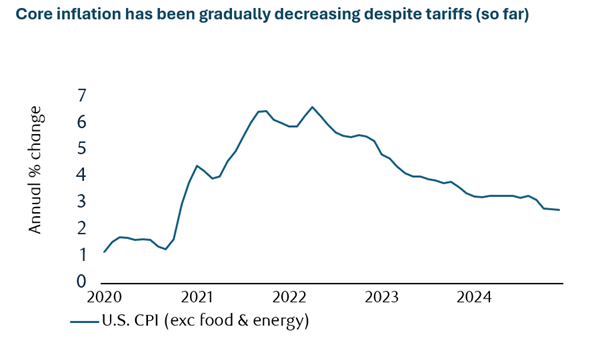

The U.S. Consumer Price Index (CPI) report for May showed a 0.1% monthly increase in core inflation, below expectations for the fourth consecutive month. Despite the current lack of impact from tariffs on inflation, it’s likely that the effects of the tariff-driven boost to U.S. inflation will be felt soon. The effective average tariff rate is currently at 15%, significantly higher than the 2.4% rate prior to Trump’s inauguration, and is expected to add around 1.5% to U.S. inflation. While some categories, such as appliances and toys, saw a notable pickup in prices, others, including apparel and footwear, experienced declines.

The report also highlighted the impact of tariffs on businesses, with some being forced to absorb the higher costs themselves, rather than passing them on to consumers. This is in line with Trump’s stated desire for businesses to eat the tariffs, rather than increasing prices for consumers. However, with the huge surge in imports prior to the tariff increases, businesses may be able to sell their existing inventory without raising prices, which could delay the impact of tariffs on inflation. Nevertheless, with the average effective tariff rate expected to remain high, it’s likely that goods prices will start to rise due to Trump’s tariffs in the near future.

The CPI report also provided insight into the state of the labour market and its impact on inflation. Core services ex-shelter inflation was weak, rising less than 0.1% monthly, which suggests that there isn’t much labour market-driven inflation. This, combined with the decline in airfares and the drop in inbound U.S. tourism, may indicate caution among American consumers.

Shelter inflation also decelerated further, with primary residence rental prices hitting a new cycle low, and measures of new lease inflation signalling that shelter inflation will remain subdued in the months ahead.

The implications of the CPI report for Federal Reserve (Fed) policy are significant. While the Fed has made progress in getting inflation lower, with the six-month annualised rate of change in the core CPI near its cycle low, the risks of cutting rates too early and losing credibility are high. It’s unlikely to cut again until there is a meaningful weakening in the labour market and/or more clarity around the impact of tariffs on inflation. With trade uncertainty still high and the potential for tariffs to boost inflation, the Fed will likely wait for more clarity before making its next move.

The UK economy is at a crossroads, with recent data releases painting a mixed picture of its health. On one hand, the labour market appears to be slowing down, with payroll employee numbers falling by 109,000 in May, the worst first estimate of payrolls in two years. This decline, combined with a rise in the unemployment rate to 4.6%, gives the Bank of England’s Monetary Policy Committee (MPC) license to cut interest rates again. They’ll probably stay on hold at next week’s meeting, but lower interest rates in August seem likely.

However, other indicators suggest that the labour market is not as weak as the payroll data suggests. The more dated, but less volatile, Labour Force Survey (LFS) showed a healthy increase in employment in April and business surveys have also stabilised or improved since March. The redundancy rate has fallen to its lowest level since before October’s budget.

The Recruitment and Employment Confederation (REC) survey indicates that the worst of the jobs slowdown may be over. The permanent staff placements index is still at an eight-month high, excluding April’s reading, and the temporary staff placements balance rising to a six-month high.

The recent spending review has also shed light on the UK’s fiscal situation, with the government maintaining its commitment to increase overall day-to-day resource spending by 1.2% in real terms on average between 2025/26 and 2028/29. However, this increase is largely driven by a rise in healthcare spending, which will absorb most of the increase in the total spending envelope. The government has announced plans to increase defence spending to 2.6% of Gross Domestic Product (GDP) by April 2027, which will add to the fiscal burden. So, we’re back in a situation where unprotected departments will be asked to make cuts in real terms.

In the housing market, the recent stamp duty hike has caused a temporary slowdown, but overall, the market seems stable. After a strong start to the year, momentum in the housing market has stalled a little. However, the RICS survey showed an improvement in forward-looking indicators, such as price expectations and sales activity, and the sales-to-stocks ratio, although still low, suggests that there’s little overhang of unsold property that would weigh on prices.

The UK GDP data for April suggested that the economy declined, partly due to the weakness of trade and the associated efforts of companies to get ahead of President Trump’s tariffs, but the domestic economy was also sluggish. Overall, the second quarter is on course for a small decline and over the course of the year growth will likely be just about 1%.

So, recession still seems unlikely, but with domestic businesses cutting spending to compensate for increased costs due to tax rises and the government quite constrained in terms of its spending, there seems adequate reason to cut interest rates.

In the UK, government spending is constrained, and interest rates are falling, whereas in the U.S., bond issuance continues at pace and the economy is holding up surprisingly well, all of which suggests that the outlook for UK government bonds is better than that for the U.S. treasuries.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below article received from Brooks Macdonald this morning, which provides a market update for your perusal.

What has happened

A degree of relative calm returned to markets yesterday, as fears of a worst-case Middle East conflagration eased. While Iran and Israel continue to trade attacks, there is a growing view that the latest conflict might yet be contained. Avoiding further escalation, Israel has not targeted Iranian oil production while Iran has not targeted US people or assets in the region – and crucially for the oil price, Iran has as yet shown no interest in blockading the Strait of Hormuz through which close to 30% of the world’s seaborne oil trade goes through.

Signs of Middle East de-escalation?

Rather than ratcheting up, it seems the conflict might even be de-escalating behind the public rhetoric. The Wall Street Journal said yesterday that Iran was signalling it wanted to end hostilities and restart nuclear talks, citing unnamed Middle Eastern and European sources, while a similar report by Reuters said that Iran conveyed that message through Qatar, Saudi Arabia and Oman. Separately, Iranian foreign minister Abbas Araghchi yesterday said that “the Islamic Republic of Iran has never left the negotiating table”. According to US news website Axios, there may be meeting this week between US Middle East envoy Steve Witkoff and the Iranian foreign minister to discuss a nuclear deal and an end to the Israel-Iran conflict.

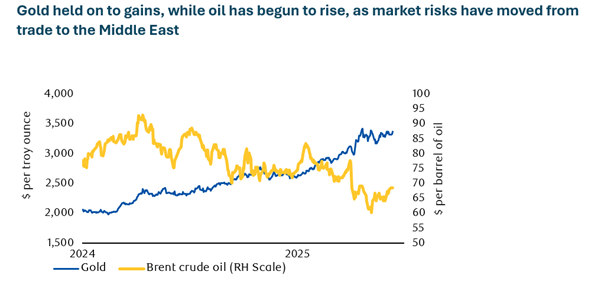

Markets shift back to risk-on

Global equity markets rose, while US government bond, gold and oil prices all fell back yesterday. The US S&P500 equity index finished yesterday up +0.94%, recouping most of Friday’s -1.13% decline, while the pan-European STOXX600 equity index was up +0.36%, having dropped by -0.89% on Friday. Overnight in Asian equity markets, the Japanese Nikkei225 equity index has closed up +0.59% (all equity indices in local currency price return terms).

What does Brooks Macdonald think

Overnight the Bank of Japan has left interest rates unchanged and announced it is looking the slow the rate at which it reduces its bond purchases next year, both decisions widely expected. On the latter, the Bank is presumably hoping to take some of the heat off Japanese government bond yields which have risen this year. This is all market positive as it reduces the risk of ‘something breaking’, avoiding a redux of the market hiatus last August when the Bank hiked rates unexpectedly.

Please check in again with us soon for further relevant content and market news.

Please see below, an article from Tatton Investment Management analysing the key factors currently affecting global investment markets. Received this morning – 16/06/2025:

Markets calm but not comfortable

Markets’ reaction to the war that broke out Friday, after Israel’s strike on Iran, has been mild. Global stocks have fallen slightly, while gold prices and the dollar have edged up. Oil prices climbed the most – and their future inflationary impact is probably why bonds fell as yields rebounded. Investors have become a little desensitised to geopolitical mayhem. You might call that resilience; you might call it resignation. In any case, we have said for a while that investors (particularly in the US) might be overly optimistic.

On the UK spending review, it was notable that Chancellor Reeves stuck to her fiscal rules, even though she probably would have got away with tweaking them. Bond yields fell, sterling strengthened and the FTSE 100 gained in response – a reaction any party’s chancellor would welcome. Despite weak growth, the UK has an opportunity to take advantage of US capital outflows – but our markets have a trading liquidity problem, which we’ll write more on soon.

US stocks held up decently, despite weaker earnings and lower than expected inflation. Trump will take that as tariff vindication, but really it suggests economic weakness. It means companies will struggle with higher input costs. Stocks can still grow in that sluggish environment (they did before the pandemic) but we shouldn’t expect the stellar returns of the last few years.

The other concern is that slower profit growth means higher equity valuations – which already look expensive compared to higher bond yields. There are reasons to doubt the bond valuation effect: there are more bonds than there used to be (see below) and they’re not easily substitutable for stocks. But eventually, higher bond yields make equities more vulnerable, either because companies need to raise capital (see Eutelsat) or sharply higher yields make everyone afraid. High yields are a big problem for equities if investors expect a recession. That’s a risk, but hasn’t happened yet.

Governments borrow more but could pay less

Markets are worried about government debt sustainability. We call government bonds ‘risk free’ because they can theoretically print money to pay back the loan (assuming they borrow in their own currency) but they are still risky by the usual understanding. We measure these risks in two ways: the term premium (long versus short-term yields) and swap spread (government yields minus central bank guaranteed interbank lending). Both measures have increased across most major economies, for a simple reason: government debt has grown much faster than private debt in the last decade.

That means governments are demanding more capital than companies. Or inversely, the private sector is deleveraging, relatively speaking, with corporates eating less of the capital pie. Corporates have also been issuing less equity for an unusually long time – despite the fact investors are happy to buy that equity. There are a couple of ways of looking at this. A Keynesian would say governments are making up for the shortfall in private sector credit demand; a supply-side economist would say governments are crowding out private investment by making borrowing rates too high to be profitable. The truth is probably somewhere in between.

Even a slight crowding out of investment could constrain long-term growth – depending on your beliefs about the efficiency of public versus private spending. Japan is arguably a cautionary tale here: its debt-to-GDP ratio is higher than any other large economy, plausibly one of the factors behind its decades of stagnation. China might be on that same path, with massive government debt expansion in the last decade and a weak private sector to show for it.

The interesting thing about these examples is that they show how higher government debt can actually mean lower yields – by lowering growth. That’s the opposite of what people usually worry about when they worry about growing government debt.

China exporting disinflation to Europe

Many expect US tariffs on China will mean Chinese exports being rerouted to Europe – and hence lower European goods inflation. This isn’t happening yet, but Americans’ rush to buy ahead of tariffs is distorting the data. Chinese exporters have room to grow their European consumer share, but JPMorgan analysts point out that changing market shares don’t affect official inflation statistics in the short-term. Europeans buying more Huawei and less Apple only lowers inflation if Huawei prices fall. JPM see the bigger short-term impact coming from the euro’s 7% appreciation against the renminbi. But even this currency impact is relatively small.

Changing market shares eventually impact inflation by changing the weightings of different goods. That could take a while, though, and it would require a consistent shift towards buying Chinese. This could be difficult, because European politicians are already worried about Chinese ‘dumping’ of electric cars. There’s nothing sinister about China selling cheap goods after overproducing, but ‘dumping’ is a politically persuasive story. German carmakers and British steel producers have already lobbied for import controls on this basis, and politicians will get more sympathetic the more China exports.

That’s good news for Washington, which wants European anti-China tariffs to be included in any US-EU deal (and successfully put them in the UK-US deal). European leaders have been reluctant to go along with the US trade war on China in the past, but the difference now is that domestic European pressures could push them in the same direction.

We think it’s likely, therefore, that the EU will put up some trade barriers with China – albeit not the 145% tariffs Trump likes to post on social media. Potential EU tariffs will probably be more commensurate with the scale of Chinese ‘dumping’, which is likely why bond markets aren’t expecting significant European disinflation.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see the below article from EPIC Investment Partners detailing their discussions on a tightening Labour Market. Received this morning 13/06/2025.

Over the past few weeks, we have focussed closely on the jobs market. Why so much attention? With inflation moving towards the Federal Reserve’s target, any further easing will increasingly depend on clear signs of labour market weakness. While recent payroll data and a stable unemployment rate appear reassuring, the underlying reality is notably different.

The Bureau of Labor Statistics (BLS) employment report for May 2025 illustrates why headline figures can be misleading. The report indicated a modest payroll gain of 139,000 jobs; however, a closer look reveals a much weaker picture. Strikingly, total employment measured by the Household Survey fell sharply by 696,000. This is not simply a statistical anomaly—it may signal a hidden deterioration in the labour market.

Each month, the BLS produces two employment measures from separate surveys. The Establishment Survey provides the headline payroll figure, counting each job on employer payrolls separately—even multiple jobs held by one person. This approach can inflate perceptions of strength. In contrast, the Household Survey directly interviews individuals, counting each person as employed only once, while including self-employed and agricultural workers who are not captured by payroll figures.

In May, payroll jobs rose slightly by 139,000 to 159.6 million, yet the Household Survey reported total employment fell by 696,000, dropping to 163.3 million. This divergence is largely because around 625,000 people exited the labour force entirely—they were not merely unemployed; they stopped looking for work altogether. This coincided with an additional 813,000 people categorised as “not in the labour force,” including retirees, students, those with family responsibilities, and discouraged jobseekers.

As a result, the labour force participation rate fell 0.2 percentage points to 62.4%. When the working-age population grows (as it did by 188,000 in May), yet fewer people actively engage in employment, deeper structural issues emerge. The headline unemployment rate remaining steady at 4.2% masks this underlying weakness, as it excludes individuals who have stopped actively seeking employment.

Moreover, the strength in payroll data may be overstated by the BLS’s Birth/Death Model, which estimates jobs created or lost by businesses not yet captured in surveys. This model relies on historical data, potentially problematic in a rapidly shifting economy. Recent downward revisions (totalling 95,000 fewer jobs in March and April) reinforce this concern, indicating that payroll growth may have been previously overstated, making the current divergence even more significant.

Investors should not rely solely on headline payroll numbers. May’s employment report clearly demonstrates that headline strength can mask genuine underlying weakness. Declining total employment and increased workforce exits point to structural challenges potentially limiting future economic growth and productivity. Investors should therefore adopt a cautious perspective, acknowledging the employment landscape may be weaker and more vulnerable than initial headlines suggest.

For the Federal Reserve, which targets maximum employment and stable 2% inflation, these nuances are critical. While typically prioritising payroll figures, the Fed will also closely monitor labour force participation and overall employment levels. If underlying employment continues to weaken, this could prompt policymakers to adopt a more accommodative stance sooner rather than later. So, despite the positive headlines citing payroll growth, the Fed may in fact be much closer to resuming its easing cycle than many currently assume.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, todays Daily Investment Bulletin from Brooks Macdonald covering their thoughts on the overnight events in the Middle East:

What has happened

Markets have been rocked overnight by fresh Middle East geopolitical risk, with Israel launching air strikes on Iran’s nuclear and ballistic missile programme sites, and warning of more action to follow. Iran has already retaliated, sending drones into Israel and vowing further reprisals. With renewed fears of Middle East conflict emerging earlier this week alongside risks of a wider Middle East conflict, that has pushed the oil price higher – at one point overnight Brent crude US dollar oil prices were up around +13%, peaking at US$78.50 per barrel – for context, that marked a gain of around +20% from where prices were at the start of June at under $65 per barrel – at the current time, the Brent crude oil price has pulled back some of its latest move, and is currently trading up at around US$73 per barrel, up around +5% on the day.

Israel’s strike on Iran

As we said in our Daily Investment Bulletin only yesterday, with US President Trump growing less confident around the prospects of limiting Iran’s nuclear programme through talks, reading between the lines it suggested a higher risk of military action instead. The US overnight has claimed that Israel acted without US involvement or assistance – however, according to Israeli public broadcasts, Israeli officials notified the US before beginning the strikes. The United Nations atomic watchdog (the International Atomic Energy Agency) has said there are no signs of increased radiation at Iran’s main nuclear enrichment site, Natanz in central Iran – while there are reports that a number of Iran’s high-ranking military officials and nuclear scientists have been killed.

Market reaction

Unsurprisingly, markets are reacting in a risk-off move this morning, with equity markets lower, and safe havens, including US Treasuries, the US dollar currency and gold prices all higher earlier. For the UK FTSE100 equity index, the falls this morning appear to be limited, largely due to gains in oil major heavyweight stocks BP and Shell this morning following the higher oil price moves overnight. Prior to the events overnight out of the Middle East, yesterday had seen equity markets put in a solid session, with US equity indices up on the back of a weaker-than-expected US Producer Price Index (PPI) inflation report, echoing the weaker US Consumer Price Index (CPI) inflation data the previous day.

What does Brooks Macdonald think

Keep the latest oil price moves in context. Back in January, Brent crude oil prices were even higher, at over US$82 per barrel at one point mid-January. So far this year, for the most part, oil prices have been in a downward price-channel, as markets have reacted to increased oil supply from OPEC+ (Organization of the Petroleum Exporting Countries plus non-OPEC members including Russia), who have been continuing to reduce post COVID pandemic supply curbs, alongside broader economic growth concerns amid global trade tariff uncertainty. If history is a guide, conflict-driven higher oil prices usually subside as wider economic and supply/demand fundamentals reassert themselves – nonetheless, there will likely be unwelcome oil price volatility in the interim.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below, an article from EPIC Investment Partners providing a brief analysis of the UK economy following the recent GDP data release. Received today – 12/06/2025

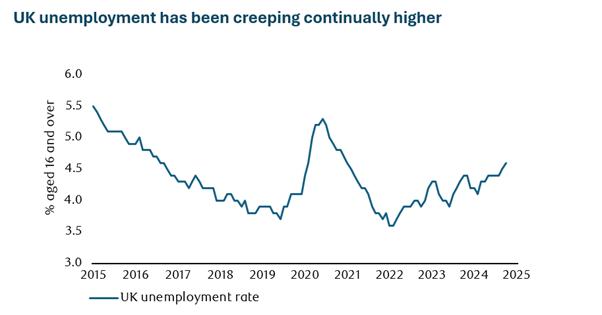

The UK economy is exhibiting increasing signs of strain, with multiple indicators pointing to a marked downturn. The labour market, a key barometer of economic health, is under growing pressure. According to the Office for National Statistics (ONS), the unemployment rate has climbed to 4.6%, the highest level in four years, accompanied by weakening wage growth and significant job losses across critical sectors.

This uptick in unemployment follows April’s policy changes, including an increase in payroll taxes and the national minimum wage, part of Chancellor Rachel Reeves’ latest Budget. Wage growth has also faltered, with average weekly earnings (excluding bonuses) rising just 5.2%, below expectations and down from 5.5% previously. Growth in private sector pay has been particularly subdued, with recent public sector pay deals providing only modest support.

At the same time, consumer spending is showing signs of fatigue. Retail sales growth in May slowed to just 1%yoy, the weakest pace of 2025 and well below both the year-to-date average of 2.5% and April’s inflation rate of 3.4%, indicating a decline in real-term spending. According to the British Retail Consortium (BRC), lower consumer confidence is leading shoppers to cut back on discretionary purchases, particularly fashion and high-ticket items. While food sales remained resilient, the broader retail picture is increasingly fragile.

Financial markets responded, sterling fell against the dollar, while expectations for a Bank of England interest rate cut shifted to September (from November).

Attention now turns to Chancellor Reeves’ Spending Review later today, where a credible response to these gathering challenges will be closely scrutinised.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 10/06/2025.

Markets calm despite ongoing trade uncertainty

Recent events have fostered a surprising lack of market movement, despite ongoing trade tensions.

Source: LSEG Datastream

As we enter the summer period, it’s worth reflecting on what a hectic year this has been for markets. But more recently, there’s been a period of unusual calm. This isn’t a period of calm in which markets rally, we’ve essentially already experienced that. This has been a period in which markets have actually done very little.

There’s normally some kind of rotation taking place between sectors and styles at all times, but for the second half of May, the markets entered a bit of a holding pattern.

The calm began following the relief rally sparked by the deferral of the ‘Liberation Day’ tariffs and coincided with the de-escalation of mutual tariffs between the U.S. and China. Those events gave rise to the markets’ new favourite acronym TACO − Trump Always Chickens Out.

During this period of calm there has been plenty of news to potentially rock markets. The Trump administration has been stressing the challenges of reaching an agreement with China. It’s also trying to pass a bill that will allow it to impose taxes on foreign investments if other countries impose unfair taxes on the U.S. That bill, at least ostensibly, has been the cause of infighting within the president’s former inner circle. It’s been largely ignored by the equity market but has been causing anxiety for bond investors due to the bond issuance it would promise in the future. All the while the TACO accusation was brought to President Trump’s attention and this could prompt him to push back against it.

So, there’s been plenty to potentially worry the market over the last few weeks, but it has managed to cope with that anxiety for now. We can’t be sure why that is, but an obvious potential catalyst is the end of the deferral of those ‘Liberation Day’ tariffs, now just a month away.

Source: LSEG Datastream

The de-escalation of trade talks doesn’t discourage the trend of central banks adding to their reserves of gold, which is likely to be a long and slow-moving phenomenon. However, gold has risen whenever trade fears have escalated and has slid back as they ease. This can be seen in the ratio of gold to other metals, most notably precious ones like silver.

The ratio of gold to silver has been rising over time because silver doesn’t have such an acute restriction on supply that gold does – for this reason, silver has tended to be a poor man’s gold in an investment sense. However, currently silver supply is quite limited, making it seem like an attractive metal in its own right. Therefore, with the ratio of gold to silver stretched by recent trade anxiety, there’s scope for a recovery in silver prices, which took effect last week.

Beyond this correction in the ratio, precious metals, in particular gold, should benefit from America’s abdication of its role of reserve currency as well as concerns over the expanding U.S. fiscal deficit.

The euro rally, despite falling relative interest rates, echoes previous market responses to political developments

The ECB has cut interest rates by 25 basis points, bringing the deposit rate down to 2%. Despite this, the ECB’s policy rate is now considered broadly neutral, and future rate decisions will depend on the evolution of the trade backdrop. The ECB has maintained its gross domestic product (GDP) forecast for the year but expects growth to slow down in subsequent quarters due to trade policy uncertainty.

The ECB’s stance is data-dependent, and it is open-minded about the direction of its next rate move. The labour market is tight, with low unemployment and moderating wage growth. Loan demand is picking up, and monetary policy is no longer considered restrictive. The deposit rate is now broadly neutral, and markets are pricing in one more rate cut this year.

The implications for investors are that the euro is likely to appreciate over the longer term, despite current bond yield spreads moving against it. The euro has been creeping higher, and some investors are questioning whether it can break out to higher levels. However, extraordinary developments such as the Trump administration’s policies can justify deviations from relative interest rate fundamentals. This happened before when the euro rallied due to populist governments failing to win European elections before it eventually fell again due to the victory by the Five Star Movement in Italy.

Longer-term, the path of least resistance for the euro appears to be up, driven by higher inflation in the U.S. compared to the Eurozone and a cheap currency relative to estimates of purchasing power parity. If Europe can avoid being at the centre of another crisis, it seems reasonable to believe that the euro rally has further to go.

Overall, investors should keep a close eye on the trade backdrop and the ECB’s policy decisions, as these will have a significant impact on the euro’s trajectory.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.