Liberation Day 2.0 – What’s next for global markets?

Please see below, todays Daily Update from EPIC Investment Partners covering their thoughts on Global Markets in relation to Trump’s upcoming tariff pause deadline:

The deadline for the 90-day pause in ‘Liberation Day’ tariff hikes moves closer as we approach the 9th of July, dubbed ‘Liberation Day 2.0’; investors and global markets are waiting for signs from the Trump administration. The quick de-escalation was to enable trade talks to move forward, but stability has been more elusive than perhaps the US had hoped. So far, the only confirmed deals have been with the UK and China, and the negotiations with other countries continue.

Since Liberation Day 1.0, the S&P 500 has rallied markedly, with a climb of over 20% from the recent lows. However, there are now concerns that the restoration of tariffs will threaten market stability. Analysts have warned of risks to equities, and ensuing volatility, especially if we see a more marked move towards deglobalisation and the ‘TACO’ trade gets cut short.

Another important area of concentration is bond markets. The US Treasury market witnessed significant volatility around the most recent round of tariff announcements, leading to a short-lived spike in yields and borrowing costs. With the US debt reaching more than $36 trillion, and the ‘Big Beautiful Bill’ potentially widening the deficit, the bond markets may be under further pressure, with more comprehensive and wider reaching ripple effects.

White House comments show that an extension is still possible, but recent statements by President Trump have created more ambiguity. Whether Trump follows his classical ‘the Art of the Deal’ playbook, or indeed goes with a more sanguine approach, volatility in markets is much more likely in the short and medium term.

We continue to actively monitor the global environment and stand ready to adjust portfolios if needed, rather than being passengers in passive indices with no option but to be taken along for the ride.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 01/07/2025.

Unpacking the drivers of renewed market optimism

We examine the factors driving renewed market optimism and their potential implications for interest rates.

Key highlights

Optimism returns to markets: The S&P 500 hit new highs, inflation pressures eased with lower oil prices, and slowing inflation supports expectations for two U.S. rate cuts by the end of the year.

Geopolitical and policy stability: Geopolitical tensions eased with an Israel-Iran ceasefire and progress in U.S.-China and U.S.-Canada trade negotiations, while the removal of Section 899 from Trump’s ‘One Big Beautiful Bill’ has reassured Wall Street.

U.S. domestic demand concerns: Personal consumption growth slowed sharply, U.S. first-quarter GDP was worse than expected, and May household spending contracted, raising concerns about domestic demand.

Stocks rally as risks recede

Source: Refinitiv Datastream

The S&P 500 surged to a new record high, finally joining the MSCI World and Nasdaq 100, which had already surpassed previous peaks. The move completes a rapid rebound from April’s correction − a full recovery in just one quarter − as investors reprice assets on the back of easing macro risks.

Several headwinds that previously dampened sentiment, including geopolitical threats and trade tensions, have subsided or moderated. Markets are embracing a backdrop of measured disinflation, diplomatic progress, and long-term secular tailwinds such as artificial intelligence-led innovation.

The strength of technology stocks was again evident last week, with Nvidia reclaiming its title as the world’s most valuable company. Meanwhile, the U.S. dollar declined, lifting sterling to a four-year high and generating numerous news headlines.

One of the key developments last week was the announcement of a ceasefire between Iran and Israel, alleviating a major geopolitical concern. Although fragile, the ceasefire helped reduce the risk of escalating Middle East tensions or spillover effects and eased concerns about potential oil supply disruptions in the Gulf.

As a result, Brent crude prices declined, more than reversing the gains since the start of the ‘12-day war’. This is a familiar pattern as geopolitical shocks often trigger knee-jerk reactions in oil markets but tend to fade quickly when diplomacy prevails. Importantly, oil market sensitivity appears to be lower than in past cycles, partly due to the U.S.’s role as a major energy producer and the global transition towards energy efficiency.

The market’s reaction also reflects the view that this particular geopolitical shock was largely contained within the oil sector, with limited spillover into broader risk assets. With energy prices stabilising, inflationary pressures may ease further, which supports the case for monetary policy flexibility in the second half of the year.

From trade tensions to trade optimism

Source: Refinitiv Datastream

The broader improvement in market sentiment also stems from developments on the U.S.–China trade front. The U.S. Secretary of Commerce, Howard Lutnick, confirmed a finalised tariff framework with China that would allow rare earths to flow.

This marks a meaningful shift in tone. Rather than escalating trade tensions, both sides appear to be seeking a diplomatic path forward. The move reduces some uncertainty for multinational firms and global supply chains and reinforces the impression that the U.S. is adopting a more pragmatic approach. Ahead of the 9 July tariff deadline, the administration is trying to project a sanguine tone for a change.

Lutnick mentioned 10 potential trade deals are imminent but provided no detail. Typically, comprehensive trade deals are years in the making. But any direction of partial or quick wins would be helpful.

Perhaps less discussed outside of financial media was the proposed removal of Section 899 from the One Big Beautiful Bill Act. Section 899 is considered a ‘reciprocal’ or ‘revenge tax’ on foreign investments for countries whose tax policies the U.S. deems discriminatory. Its removal will bring huge relief to investors who were worried about punitive tax measures on U.S. assets, which have dire consequences of exacerbating the risk of capital outflow.

Overall, the more conciliatory, diplomatic and sanguine tone from the U.S. administration has lowered the temperature around trade and investment risks.

Fed rate-cut case builds

The U.S. dollar extended its slide last week, hitting a three-year low amid improving global risk sentiment and renewed speculation over future leadership at the Fed. Reports that President Trump may pre-announce his preferred Fed Chair nominee raised expectations that a more dovish tilt in monetary policy may lie ahead.

But markets may have got ahead of themselves. Bear in mind, President Trump is the one who nominated Jay Powell in 2017. It means Trump does not always get what he wants. The Fed’s dual mandate (maximum employment and stable prices) should surpass Trump’s influence.

The market derives confidence from the Fed to remain independent and to do the right thing. With no official announcement and several months to go, this remains a speculative narrative, and the market may be overpricing its implications in the short term. For instance, markets are currently pricing in three rate cuts in 2026, as opposed to one cut as indicated by the ‘dot plot’.

Meanwhile, economic data last week added weight to the dovish policy narrative already taking shape. The final Q1 Gross Domestic Product (GDP) shows personal consumption was sharply revised from 1.2% to just 0.5%. Personal spending data in May has contracted which adds to the concern that U.S. consumers are becoming cautious on their spending.

This softening in household spending suggests that underlying demand may be more fragile than previously believed, even as headline inflation continues to moderate. The combination of slower growth and declining inflation is now reinforcing the market’s pricing of two Fed rate cuts by year-end, provided tariff risks remain contained.

At the same time, Fed officials remain divided. While a few members have voiced openness to a July rate cut, the majority maintain a data-dependent, cautious stance. For now, the Fed appears willing to wait for further confirmation before acting. But markets are increasingly confident that the direction of travel of monetary policy is one of gradual easing.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see the below article from EPIC Investment Partners detailing their thoughts on the macro economy and the surgency of the gold market. Received this morning 01/07/2025.

US net investment income has turned negative for the first time since the data series began to be published in 1960. It declined from a recent peak of 1.4% in 2018 to a negative 0.07% of GDP in the four quarters to 3Q24 according to Bureau of Economic Analysis. Previous dailies have noted the rapid decline in America’s net international investment position (NIIP), which represents the difference between US assets abroad and foreign assets in the US. America’s net international investment position deficit has risen from 39.9% of GDP at the end of 2017 to a record 89.9% of GDP at the end of 2024.

Following the Russian invasion of Ukraine, the Group of Seven froze Russia’s foreign exchange reserves held in the Group of Seven currencies. While the Russian economy has not collapsed, Bloomberg recently reported that Russia’s economy is facing a worsening outlook that is far graver than publicly acknowledged. There is a credible risk of a systemic banking crisis in the next 12 months according to Russian banking officials.

The increasing evidence of Russia’s mounting economic problems (due to sanctions) and the seemingly unstoppable decline in America’s financial position have been behind the resurgence of central bank gold bullion purchases. A report issued last week by the European Central Bank highlighted the shifts underway in the portfolios of global central banks.

Central bank reserve managers bought 1,000 metric tons of gold in 2024, double the pace of the previous decade. Interesting both Germany and Italy are reported to be considering repatriating their physical gold reserves currently held in America. At the end of 2024 the dollar accounted for 58% of global foreign exchange reserves compared to 65% a decade earlier. Gold has now replaced the Euro as the second largest component of central bank reserves after the dollar.

There is no evidence that either Japan, China or the Swiss (the countries with the three largest foreign exchange reserves) are reducing their dollar assets but it seems increasingly unlikely that they will add to existing dollar reserves.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Please see below, an article from Tatton Investment Management analysing the key factors currently impacting global investment markets. Received this morning – 30/06/2025:

Markets calibrate to Trump 2.0

We wrote before that US involvement in the Israel-Iran war was ‘priced in’ and therefore unlikely to hurt markets. Quite the understatement. US stocks approached all-time highs and oil prices fell the moment Iran struck a US air base – as traders correctly interpreted the strike as symbolic and ultimately de-escalatory. You could argue the Middle East is no longer as big a concern for western economies (thanks to the US shale boom) but we suspect it’s more that markets have adjusted to Trump 2.0’s extreme “art of the deal”.

The president made his show of strength, and investors think that makes him more inclined to extend the 90 day tariff moratorium when it expires on 9 July.

UK and European stocks lagged, but are still ahead of the US year-to-date. The 5% of GDP defence spending target will mean more fiscal expansion – even if it’s never actually reached. Defence stocks are big winners but the 1.5% allocated to defence-adjacent investment will benefit the broader European economy.

The UK market also got some good news in the form of software company Visma choosing London for its IPO. This is a good sign, given the UK stock market liquidity problem we discussed last week.

The dollar weakened again, despite positivity in US stocks. Its decline in 2025 has hampered returns on US assets for investors outside the US. We’ve put it down to capital outflows before, but that makes less sense given the gain in US capital assets. We can speculate that it might be down to those outside the US converting their dollars (payments for selling to Americans) to local currency, rather than funneling them back into US assets.

Investor optimism is good preparation for the upcoming hurdles: tax cuts in the “Big Beautiful Bill” and the 9 July tariff deadline. The risks are real, but hopefully that optimism pulls us through.

Improving US earnings outlook has a distribution problem

US equity earnings are doing better than expected – and better than elsewhere – despite tariffs weighing on the outlook. Q1 earnings for S&P 500 companies comfortably beat estimates, and recent analyst revisions have been significantly less negative than into “Liberation Day”. But almost all of that positivity comes from the ‘Magnificent Seven’ tech stocks (though perhaps we should say magnificent six, given Tesla’s continued losses). Excluding the Mag7, the rest of the S&P has similar projected 2025 earnings to Europe – and below Japan and China. Expectations for 2026 and 2027 are even worse for the US index.

Of course, taking out the best performers (the Mag7) will always make an index worse – and even then it’s pretty similar to the Eurostoxx 600. Considering the wider index is important, though, because it gives a better indication of the US economy. The Mag7 are fairly isolated from tariffs (barring perhaps Apple) for example, being genuinely global. Tariffs are expected to hurt most other companies – but you might also argue this is too pessimistic. Most expect Trump to delay tariffs past the 9 July suspension deadline, for example, and you could argue that analyst predictions are a little too negative (meaning future earnings beats are likely).

Pessimism itself is bad for US companies, however. It delays business investment and lowers the value of the dollar – reducing the value of equity earnings for international (particularly European) investors. In sterling terms, for example, US earnings look significantly worse than Europe’s.

The currency outlook introduces an extra risk, which threatens price-to-earnings valuations (already more expensive in the US than anywhere else). US stocks have less exceptional profit growth than we are used to, and the risks (including currency) are higher. Without even considering the broader geopolitical risks, it isn’t hard to see why global investors’ love affair with US stocks is waning.

Do androids dream of investment opportunity?

Humanoid robots are one of the more curious investment stories gaining traction. Swiss bank UBS expects the market for human-like robots will reach $1.7tn by 2050, while Morgan Stanley predict $5tn. These estimates are always a little speculative (those most interested in future tech tend to be the most optimistic) but the reports are based on thorough analysis of resource availability, market structures and future regulation. In short, new tech (particularly the AI ‘brains’) will make robots cheaper and more viable, while aging populations will increase the demand.

Take the figures with a pinch of salt, but they show the robot market has potential. Morgan Stanley put together a “Humanoid 100” list of companies that make the “brains” (AI systems), “body” (mechanics) or, the most valuable, “integrators” (putting them together). China could benefit significantly, with lower production costs than anywhere else. China’s overproduction problem has hampered its economy more broadly, but it could be a benefit in the robot race. Many analysts think China is already ahead of the US.

Morgan Stanley’s list of robo-stocks is familiar, if a little underwhelming: Tesla, Amazon, Nvidia, Alphabet, Meta, TSMC, Tencent, Alibaba. You would hope that futuristic innovation would deliver fresh new companies (and it probably will, to some extent) but the big tech names have the best chances. They have the most capital and are already involved in AI.

For example, big tech companies still stand the most to gain from the slow (relative to expectation) rollout of autonomous vehicles (AVs), in part because the lead times are so long and require more investment capital.

The AV story (investment buzz followed by as yet underwhelming impact) shows that technology adoption isn’t a straight line. Not only are there regulatory and social barriers, but short-term cyclical factors (the automotive recession) can delay development. We should track the robot investment theme, but bear in mind these risks.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below, todays Daily Investment Bulletin from Brooks Macdonald covering their thoughts on markets and the ongoing Geopolitical Issues:

What has happened

The US S&P500 equity index edged up +0.80% in US dollar price return terms yesterday, leaving it just 0.05% below its February record. In contrast, the broader MSCI All Country World Index (also in US dollar price return terms) has already got there – hitting another fresh all-time closing high yesterday and in doing so notching up its seventh fresh record high this month. That performance picture however includes a boost from a weaker US dollar currency so far this year – for context, in sterling price return terms, that same global equity index is still below its January record high.

US-China trade deal finalised

US Commerce Secretary Howard Lutnick said last night that the US and China have now finalised a deal codifying the Geneva trade talks back in May – the deal includes a commitment from China to deliver rare earth metals, following which, Lutnick said the US would “take down our countermeasures”. Separately, Lutnick said US President Trump is preparing to finalise a slate of trade deals in the next two weeks and expected to follow the US tax cut bill which is going through Congress currently. On the tax cut bill, there was good news here too, as Section 899, a “revenge tax” provision (which would have hiked taxes on foreign investors and companies from countries deemed to discriminate against US companies) has been scrapped.

US inflation data due

Later today, at 1.30pm UK time, we get the US Personal Consumption Expenditure (PCE) inflation data for May. The Bloomberg median forecast is for a +0.1% month-on-month rise in core PCE (which excludes food and energy prices). If that is the number, it would cap the third month in a row of +0.1% month-on-month prints, and it would equate to a 1-month annualised rate of just +1.21%, well below the US Federal Reserve’s +2% inflation target – in turn, also likely increasing pressure on the US Federal Reserve to cut interest rates.

What does Brooks Macdonald think

It is worth keeping an eye on UK government bond markets in the run-up to the planned government welfare reform vote next Tuesday. The planned savings from the bill were expected to help the Chancellor keep within fiscal rules, however given internal Labour party opposition, that now looks in doubt. How the government’s fiscal maths gets squared later this year in the Autumn budget is not yet clear but higher taxes and/or higher borrowing are likely to adversely impact UK economic growth and gilt yield near-term outlooks.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below article received from Brooks Macdonald this morning, which provides a global market update for your perusal.

What has happened

One-day equity market performance was largely flat to small down yesterday, though a bright spot was US megacap tech stock NVIDIA which notched up a fresh all-time record high. For the most part though, despite Middle East risk moving into the rear-view mirror, investors appeared to be having a hard time finding new reasons to buy stocks. One benefit of the smaller moves yesterday was the market’s “fear-gauge” VIX volatility index (which reflects option-pricing derived annualised 30-day forward-looking implied volatility of the US S&P500 equity index) – that closed on Wednesday at a 4-month low of 16.76 index points – for context, the longer-term VIX average sits at just under 20.

Tax cuts and tariffs centre stage again

With the Israel-Iran ceasefire continuing to hold, markets are focusing back on other things near-term, and top of the list are tax cuts and tariffs. First up, is US President Trump’s tax and spending cut bill currently working its way through Congress, which Trump is pushing to get signed before the 4 July US holiday. Second, the 90-day reciprocal trade tariff pause that Trump put in place back in April with most countries apart from China is due to end on 9 July, less than two weeks away now – Trump’s National Economic Council director, Kevin Hassett, said earlier this week that “we’re very close to a few countries and are waiting to announce after we get [Trump’s tax and spending cut] Big Beautiful Bill closed”.

A new Fed Chair in the wings?

The Wall Street Journal reported yesterday that US President Trump might announce US Federal Reserve (Fed) Chair Jerome Powell’s replacement by September or October this year. If that proves to be the case, it would mark an unusually early appointment (Powell’s term doesn’t end until May next year). Adding to the rumour mill, Trump said yesterday that he had 3 or 4 people in mind as potential replacements.

What does Brooks Macdonald think

US President Trump has made no secret of his desire to see US interest rates lower, characterising Fed Chair Powell as “Too Late Powell”. The risk of an early announcement, however, is that it could effectively create a shadow Fed chair with the power to influence market sentiment and undermine Powell’s authority. Further, just because US interest rates could be cut more easily under a new Trump-friendly Fed chair, it doesn’t necessarily follow that bond markets would play ball, especially in terms of longer-term bond yield interest rates which the Fed has much less control over.

Please check in again with us soon for further relevant content and market news.

Please see this week’s Markets in a Minute update below from Brewin Dolphin, received yesterday afternoon – 24/06/2025.

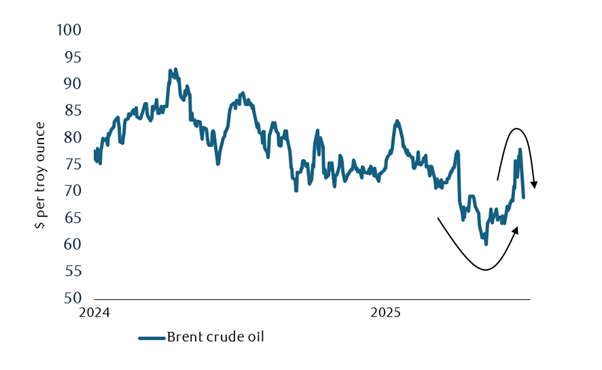

Middle East conflict: oil prices surge, then retreat

Oil prices rose sharply amid heightened tensions, but a ceasefire saw prices return to pre-conflict levels.

Oil reflected the Middle East crisis with prices rising by around $10, but that has largely dissipated

Source: LSEG/Bloomberg

It’s been a dramatic few days in the Middle East with some broadening of participation and targets. Over the weekend the U.S. struck three uranium enrichment facilities in Iran, and we wait to hear how effective those strikes were. Thereafter, Iran retaliated with missiles launched at a U.S. air base in Qatar. Those attacks were easily intercepted, and the base had already been evacuated as a precaution. The event was considered to be stage-managed to allow the Iranian regime to credibly claim they had responded.

Over the course of the crisis, around $10 of risk premium had been incorporated in the prevailing oil price. That had the potential to add 0.3% to 0.4% to U.S. inflation and detract a similar amount from growth. Prior to the incursions, the oil market was over-supplied and prices had been weak. OPEC seemed unwilling to defend the price.

Following the U.S. action and the stage-managed Iranian response, President Trump announced a ceasefire had been agreed. The price fell below the level at which it was trading prior to Israel’s initial attacks. In the short-term, hopes are high that this crisis is resolved however, critically, questions remain over whether the ceasef fire is being observed. Over the longer term it remains to be seen whether the U.S. action is enough to discourage, or ensure the end of, Iran’s nuclear ambitions.

Core inflation has been gradually decreasing despite tariffs (so far)

Source: LSEG Datastream

Despite anxiety over U.S. tariffs in the last few months, the U.S. economy remains in reasonable shape.

The headline U.S. retail sales growth was below expectations, but this seems to be driven by the usual one-off elements. For example, when the weather takes a turn for the worse, consumers delay their buying and that affected the U.S. during May as seen in the weather sensitive building materials and garden equipment sales sector.

However, despite the anxiety, the American economy has continued to function normally. Consumers have yet to be subjected to the burden of tariffs. They can worry about them, but they aren’t changing their spending habits. Going forward, that could change when prices eventually start to rise, not least because now there’s an increase in the all-important gasoline price to contend with.

Uncertainty over this left the Federal Reserve on hold, but they’re still effectively endorsing the markets’ expectations of two more interest rate cuts this year. Beneath the surface though, that level of conviction appears to be dropping and the case for just a single cut grows louder. This declining expectation of interest rate cuts would normally weigh on the dollar, but it hasn’t been trading in line with interest rate expectations recently. Added to which, the dollar remains very overvalued relative to other major currencies, so the case for a weak dollar remains intact.

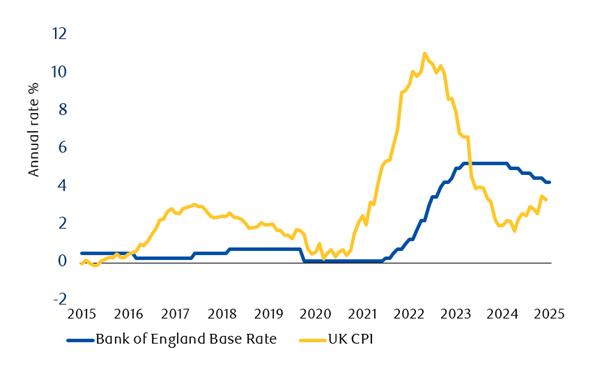

Interest rates have been cut, but inflation remains a problem in the UK

Source: LSEG Datastream

The UK also saw weak retail sales, which adds to a pattern of weaker economic data that has been coming from the UK.

House prices were strong at the start of the year, but now they’re slowing. Employment has been on a downward trend which seems to have accelerated. Added to which, interest rates were raised very sharply between 2022 and 2023. So, there would seem to be ample opportunity to continue cutting rates, and a growing rationale for doing so.

However, the challenge facing the Monetary Policy Committee (MPC) is that core Consumer Price Index (CPI) remains too high at a time when inflation has spent much of the last three years well above the inflation target, a fact which is increasingly becoming enshrined in consumers’ expectations of inflation. As such, it remains the imperative of the Bank of England (BoE) to continue to see validation of its rate cutting stance as it progresses with monetary easing.

The BoE held interest rates this month but is expected to cut them again in August. Lower interest rates would support the UK bond market and lower bond yields would be helpful for the Chancellor, Rachel Reeves. Public finance data suggested that she had some success reining in government expenditure following the Spring Budget, however higher bond yields mean that interest costs are due to eat away at her fiscal headroom and raise the risk of further tax increases in the autumn.

Please continue to check our blog content for advice, planning issues and the latest investment market and economic updates from leading investment houses.

Please see below, an article by Sir John Redwood for EPIC Investment Partners, providing a detailed analysis of the Bank of England’s operations in the bond market. Received yesterday – 23/06/2025

The Bank of England’s legal status and aims

The Bank of England is 100% owned by the state, led by a Governor appointed by the government and ratified by Parliament. The Governor reports to Parliament’s Treasury Committee on his actions and policies. Parliament legislates to reset the Bank’s aims and tasks when it wishes.

The Bank has under its current legislation an independent status to set the key base short term rate and to publish its own economic forecasts. It made large purchases of bonds (£895bn at peak) in response to the banking crash of 2008, briefly after the Brexit vote, and on a large scale during Covid. This was a joint policy of government and the Bank. All purchase programmes required Chancellor sign off with the grant of full Treasury indemnity against any losses the Bank might incur on the bonds.

The main aims of the Bank are to keep inflation at around 2% and to ensure financial stability in the UK markets and banking system. It had a good record on inflation in the decade following the banking crash of 2008, against a benign deflationary world background and with plenty of Chinese competition in goods helping keep prices down. Like the Fed and ECB, but unlike the Swiss, Japanese and Chinese central banks, the Bank of England presided over a surge in inflation this decade, hitting a peak of 11% in late 2022 against the 2% target.

The Bank did not keep markets stable in 2007-9, when there were violent convulsions in the banking system, as in the US as well. There was a short crisis in the UK in late 2022. Markets were driven down by rises in official rates here and in the US, an expansionary budget which was reversed, the Bank’s announcement of a major sales programme of gilts and the plight of pension fund investments in geared bond funds. Pension funds had to sell bonds to cover losses and meet calls on their leveraged positions. This forced the Bank to temporarily reverse its bond sales plans and to buy bonds again to stabilise the market.

The Bank and the Asset Purchase Facility

The joint government/Bank bond portfolio was acquired by the Asset Purchase Facility (APF) at the Bank. As it bought bonds from the market, more cash was deposited with the commercial banks, who in turn increased their deposits with the Bank of England. In the early years of the APF, with interest rates falling, the Bank made money on the difference between the amount of interest it earned on the bonds and the lesser amount it paid out for the deposits. Up to mid 2022 the Bank was paying its profits (£123bn) on this over to the Treasury, who spent the cash. When rates started to rise the Bank moved into loss on the portfolio, as the low interest rates it had locked in by buying the longer term bonds were below the higher and rising level of interest on the deposits it held from the commercial banks. The Treasury had to start paying out for the losses.

The Bank added to the losses by proceeding with a programme of bond sales into the market. The bonds were well below the purchase price they had paid, as interest rates had gone up a lot, depressing the price of the bonds. The long dated bonds were often more than 50% down on purchase price and recorded large losses which the Treasury is now paying. No other central bank that had bought up bonds to provide stimulus during Covid lockdowns has been selling bonds at a loss. They wait for the bonds to mature, when they get back the original issue price of the bonds. The closer a bond gets to maturity the closer the market price will move to the original issue price, reducing the losses at a time of higher interest rates.

In 2023-24 the UK Treasury paid £44.5bn to the Bank for bond losses in the APF. The Office of Budget Responsibility is forecasting losses of £257bn from mid 2022 to mid 2033 when they expect the portfolio to be wound up. These losses are now becoming a matter of public debate, with some urging the Bank and government to take action to reduce them and save the Treasury some money. The other trading profits and losses of the divisions of the Bank are very small in comparison to the APF losses.

The Bank deliberately paid too much for the government debt or bonds it bought to drive their prices higher, often paying well above the repayment value of the bond in order to get interest rates well down.

What are the Bank’s options on bond losses?

The Bank is currently incurring three types of loss. There is the loss on sales in the market at depressed prices. There is the lesser loss on maturity on bonds bought above issue value. There is the running loss on the interest differentials.

There is nothing the Bank can do to avoid losses on maturity. The private sector is the winner as they sold the bonds to the Bank at a high price and can buy them back at a lower price when new replacement bonds are issued for the maturing ones.

The Bank can suspend or cancel its bond sales at a loss. It does not argue there is a necessary monetary purpose for the sales and is out of line with other central banks. Holding them for longer means continuing revenue losses on the interest differences, but avoids large one off up front losses. Future interest differential losses may reduce as interest rates fall. Capital losses will be much reduced by holding.

The Bank can change the amount of interest paid to commercial banks on their deposits. The European Central Bank (ECB) changed its policy in 2023. It pays no interest on a specified minimum level of reserves a commercial bank has to keep with the Central Bank. It has a lower deposit rate from its lending rates to reduce its losses. The markets accepted this meaner treatment of commercial banks in its system.

Some Bank of England critics think it should return to the older system when it did not pay interest on reserves. This would be a much tougher policy on the banks than the ECB one, cutting bank profits and income considerably, much as a bank tax would. This might have adverse market consequences and could have an impact on credit growth and general economic growth. Banks would need to balance the wish to withdraw reserve deposits and make better use of them with the impaired profit and cashflow which could affect their capacity to lend.

What might the Bank do?

It seems unlikely the Bank will suddenly remove all interest on reserves, as they tend to move cautiously and would not wish to be seen to be following Reform party policy. The Bank may, with behind the scenes government encouragement, take more limited action to reduce some of the losses. This they could most easily do by postponing long bond sales. The Bank will be concerned at how longer rates have risen this year and are now consistently higher than in the late 2022 period of bond volatility. They are less likely to create a minimum reserve requirement with no interest, as they have written about how they find it difficult to judge what the correct level of reserves should be.

Markets will be watching carefully the increases in spending announced as part of the Spending Statement and considering what budget action will be taken later this year to ensure conformity with the Chancellor’s fiscal rules. There is general agreement that more tax revenue will be needed to keep to the requirement to balance the revenue account later this Parliament. For the time being the UK offers higher rates than the US, Euro area and Japanese bond markets provide, whilst we await clearer news on the trajectory of future spending and borrowing. There is likely to be more negative speculation before the budget reveals more about how the revenue side could get closer to matching the increased spending.

The Bank has allowed too much inflation and is now keeping longer term interest rates higher for longer as it continues to sell so many government bonds. Its large losses invade the budget arithmetic and add to the fiscal pressures which are impeding better UK growth.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Below are the latest insights from the De Lisle Partners investment team regarding the recent developments in Iran. Received today – 23/06/2025:

Despite weekend commentators gaming out a range of negative scenarios for an Iranian response to US strikes, we – and the markets – remain calm. In early futures trading on Monday, the Dow Jones, S&P 500 and Nasdaq indices are all slightly positive, while the larger initial move in crude oil was sold.

This is not without precedent, as markets have previously strengthened on US interventions in the Gulf. For example, the S&P 500 rose 4% in early 1991 at the start of the First Gulf War, ending the 1990/1 recession, and went straight on up in a surge of nationalism to trade 16% higher by February 11. Even energy stocks kept pace although the oil price went down.

Today Monday June 23 the market is not so depressed, having already surged since April. But we have clues from this morning’s futures markets and from the rise in the Tel Aviv, Egypt and UAE stock markets yesterday that there is plenty of support for the US strikes. Gold is down and the dollar is up as a further show of confidence in American exceptionalism. Trump’s display of decisive power seems well liked in these politically fractious times.

The reaction today is muted because there is little current concern. The Houthi threat to the Strait of Hormuz is not credible and China and Russia have looked on. American confidence is shown in the 0.6% rise in the dollar and longer-term oil futures reflect little concern of supply disruption. Gold, as a proxy for fear, is not moving much this morning.

For us, our themes are unchanged. Our portfolio is steadfast in long-term secular themes in re-industrialisation and power infrastructure while being counterbalanced by exposure in oil service that strengthens on geopolitical uncertainty. We remain at low levels of liquidity and would add to existing holdings selectively on weakness.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.

Please see below, an article from Tatton Investment Management analysing the key factors currently impacting global investment markets. Received this morning – 23/06/2025:

The risks are real – but priced in – up to this point of escalation

Last week’s Israel-Iran escalation ended with higher oil prices, a slight knock to equities and a slightly stronger dollar. Even if that seemed a relatively muted reaction to an historic event, it did nevertheless suggest that markets thought the US would join Israel’s attack. This explains why oil is up by only $1 following the US’ attack over the weekend and that should mean oil continues to stay within ‘normal’ ranges – but that depends on the nature of Iran’s reaction, namely whether it will indeed try to block the Strait of Hormuz as voted for by its parliament on Sunday.

Last week, potential US involvement created internal tensions between Trump’s MAGA isolationists and old-school Republican war hawks. But his move to action appeared to have rallied and consolidated the factions which could further embolden the president in his aggressive policies, which has the potential to cause market volatility to increase after all.

Trump also called Federal Reserve chair Powell “stupid” for not cutting interest rates. He’s right that the slowing US economic could do with lower rates, but it’s his tariffs, deportations and general chaos that’s preventing the Fed from doing so. The Fed recognises that the medium-term trend is towards lower rates, but Trump has them in purgatory. It’s heartening, at least, that Powell and co are staying level-headed.

The Bank of England also held steady but is in a different situation (with a stabler government). It signalled an August cut and will be helped by sterling’s strength.

Conversely, dollar weakness is a problem for the Fed. The dollar has stayed low despite the US stock market recovery, and the currency effects make middling US company earnings look worse for international investors. This is especially when considering that virtually all the earnings positivity comes from the globally focussed Magnificent Seven.

Dollar weakness this year reflects stronger growth elsewhere (the FTSE 100 hit a new all-time high) so it’s fitting that ECB president Christine Lagarde wrote about the need for a “global euro”. Currently, US capital markets are joining the Fed in purgatory. Investors now await not just the Israel/US-Iran war but the 9 July tariff deadline.

The UK equity liquidity problem

The FCA has just launched its Private Intermittent Securities and Capital Exchange System (PISCES) to boost investment in UK companies. It opens up more companies to private investment, but we think the main problem with UK capital markets is the lack of trading liquidity. This illiquidity comes from high transaction costs and a post-Brexit exodus of market makers, and it has resulted in Britain having one of the lowest domestic ownership rates of its stock market (just 31%). Illiquid markets are more prone to sudden price drops – increasing risks for investors and hence decreasing equity valuations. PISCES opens up more saleable assets, but doesn’t encourage more buyers and market makers.

The EU has similar liquidity problems – owing largely to the lack of retail investors (relative to the US boom in retail investing). European markets are dominated by large institutional investors, whereas from a ‘gap risk’ perspective you would rather have many small buyers and sellers. Big institutions also prefer to keep their trades away from public order books, so that others can’t copy their trades and move the price before the large orders are fulfilled. That lack of transparency decreases the perception of liquidity.

Europe’s problems are compounded by a lack of common regulation (as ECB president Lagarde argued in a Financial Times op-ed), which discourages investment banks from acting as market makers. But the bigger problem – as in the UK – is high transaction costs. The US has much lower transaction costs and an integrated market, increasing liquidity and benefitting American companies.

Reducing UK stamp duty on share trading would therefore help bring back liquidity, but so would greater regulatory alignment with Europe. With London’s financial expertise, Britain has a real opportunity to capitalise on Europe’s investment drive. But reforms need to make it easier for buyers too – not just open more assets for sale.

Yield breakup?

UK and US government bond yields are tightly correlated. To understand why, it helps to look at historical bond trends: global yields used to be high and fairly independent, but came down together after 1997, thanks to the freer movement of global capital and the advent of independent but often coordinated central banks. Yields dispersed somewhat after the 2008 financial crisis – and again post-pandemic – partly due to regional factors (e.g. the euro crisis) but largely due to slower economic growth in Europe and the UK, compared to the US.

There are a couple interesting trends to note here. First, Japan and China don’t follow the same pattern as the rest of the world, due to their different growth profiles. Second, UK yields used to be more tightly linked to Europe than the US – but this changed after the Liz Truss bond market crash.

Does the current UK-US correlation mean UK growth and inflation is more similar to the US than Europe? Perhaps on the inflation front, as we do have a tighter labour market than the EU, post-Brexit. But the growth comparison makes less sense: the US economy has raced ahead, but Britain has been sluggish. The relationship makes even less sense when you consider that Trump’s current fiscal expansion (from tax cuts) is starkly different from Downing Street’s fairly stringent fiscal rules.

It’s possible that US and UK yields are connected because the traders of those bonds are themselves linked. If so, the relationship seems fragile, especially if Trump keeps breaking trade links. Currency movements – like sterling’s gains against the dollar this year – could be the thing to break it, as that would mean capital flows into UK bonds and out of US bonds. Indeed, further declines in the world’s reserve currency – coupled with growing government debts – could see yields break apart globally. It will pay for investors to stay alert to the risks and opportunities this changing landscape presents of the coming months.

Please continue to check our blog content for the latest advice and planning issues from leading investment management firms.