Please see the below article from W1M detailing their views on the current macroeconomic background. Direct from their Global Outlook Report issued on 11/08/2025.

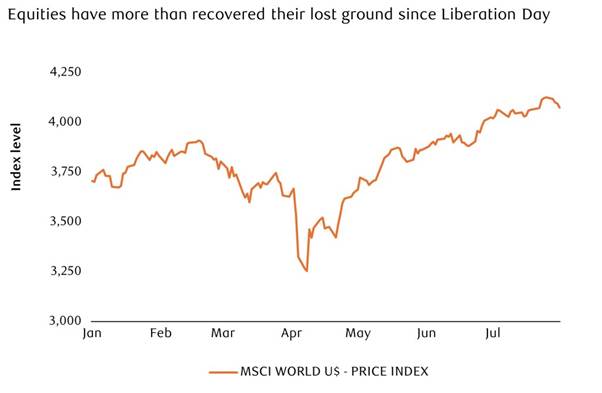

Over the summer there has been surprisingly little market nervousness about the assorted uncertainties relating to US economic policy. Tariffs are generating genuine revenue ($26.6 billion in June alone) but there remains considerable uncertainty about who is paying this new tax. It seems to be a combination of corporates and consumers. But it is very difficult to model how this is going to evolve given that there remains no sign of an agreement with China. And even those agreements that have been made are light on details. For example, does the 15% tariff agreed with the European Union include pharmaceutical exports to the US? That seems unlikely given that President Trump has made it clear that is exactly the sort of thing that he wants to reverse and bring such manufacturing back to the USA. But for now at least the market has decided to not be concerned about these great unknowns.

The other theme that has asserted itself in recent weeks has been the outperformance of the US stock market and within the US the leadership has reverted to the so called “Magnificent 7” (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla). Those stocks now represent a record 32% of the benchmark S&P500 Index. The broadening of market leadership that we saw at the end of last year and the beginning of this has not been maintained. Although the theme of technological innovation and in particular the investment in Artificial Intelligence is very real it would be healthier if stock market leadership reverted to being broader than the current very narrow focus.

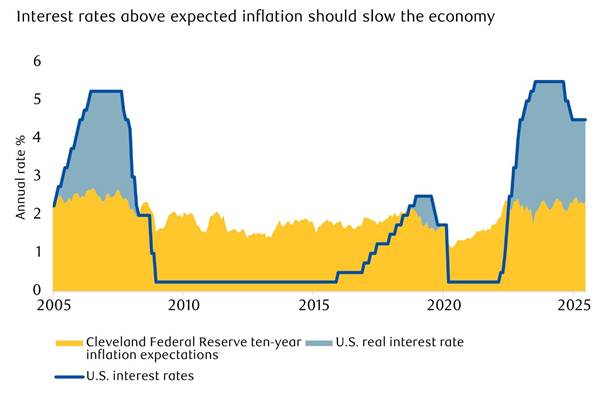

The market is also not showing concern about the political pressure being exerted on the Federal Reserve. There is a long history of President’s being frustrated by the Federal Reserve. Lyndon Johnson famously shoved Fed Chair William McChesney Martin against a wall at his ranch in Texas. Trump has not done that to Jerome Powell, yet. But Trump has appointed his Chair of Economic Advisors, Stephen Miran, as a Governor to serve until January 2026 and will be able to appoint a permanent Governor at that time. The likelihood is that interest rates will be reduced by the Fed in coming months. The market is expecting two rate cuts between now and the end of the year and sees the Fed Funds rate getting to 3.0% by January 2027, down from its current 4.5%.

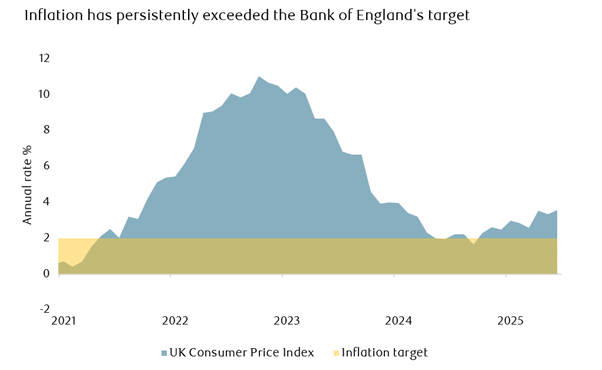

That could happen if the market is correct in thinking that inflation is not going to reassert itself. The five year inflation swap is priced at 2.7% (i.e. that is what the market expects inflation to average over the next five years). A year ago the swap was priced at 2.25% but there has not been an adverse reaction to the repricing. It will be important though for the market not to expect the inflation picture to deteriorate any further.

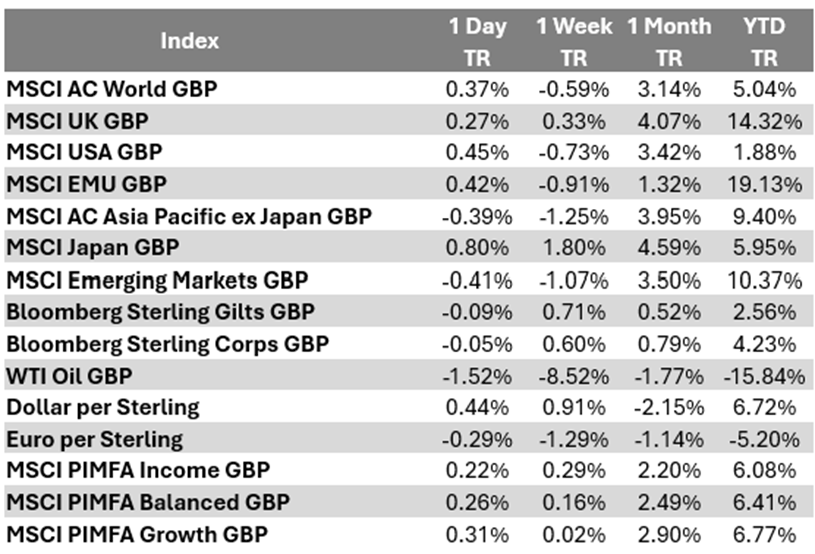

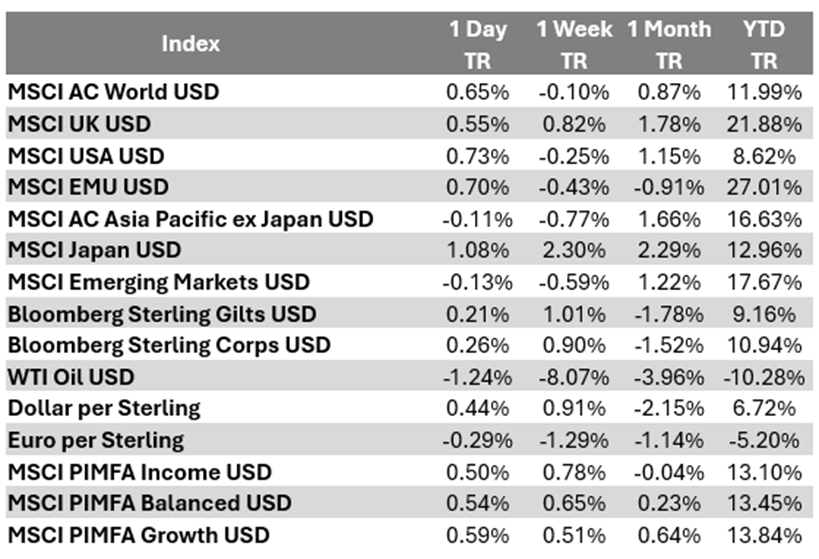

As the investment team highlighted this week, with 90% of S&P 500 companies reporting quarterly results, corporate earnings season is winding down. Earnings results have been stronger than expected, as 82% of S&P 500 companies have beaten analyst estimates, with an average upside surprise of 8.5%. As a result, forecasts for earnings growth have been revised sharply higher to 9.7%, from 3.8% at the end of 2Q, showing that prior downgrades appear to have been overdone.

The Mag 7 continued to generate an unusually big share of overall 2Q earnings growth. In aggregate Mag 7 are forecast to report average growth of 25.7% as of August 5, according to FactSet. Excluding those big tech firms, the S&P 500’s other 493 stocks were expected to post much slower growth of 6.3%. But the health of the US corporate sector remains rude, a helpful backdrop given the uncertainty around tariffs.

Risk warning: The above should be used as a guide only. It is based on our current view of markets and is subject to change. As at 11.08.25

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Alex Clare

14/08/2025