Please see below the latest market update article from Brewin Dolphin, which was published yesterday (30/06/2020):

As you can see from the above, the virus remains present and its impacts are still being felt globally, with high levels of volatility continuing in markets. These levels of high volatility are likely to continue.

It remains important that you remain invested and focus on your long-term goals until markets recover to more normal levels of volatility.

Please continue to check our Blog content for the latest investment, markets and economic updates from leading investment houses.

Please see below for Royal London’s latest market update received 29/06/2020. They provide an update on the impact of recent market events:

RLAM Economic Viewpoint

Survey data, high frequency data and now increasingly the hard data too, continue to show that developed economies are in the ‘recovery phase’ of this crisis. Albeit this is the somewhat mechanical bit as economies are allowed to open up and you get a bit of pent-up demand set loose as well. Some of the recent data points have shown much stronger than expected improvements. This, however, doesn’t tell us much about the next stage of the recovery that economists generally expect to be much slower. Social distancing, scarring (including permanent job losses, business closures and balance sheet damage) and residual fear of the virus (including as it relates to job security) will all influence the strength of that recovery and government policy still has a crucial role to play in all of them.

June business surveys improve substantially: Data in the past week or two has included several June business surveys and these have mostly seen solid improvements, with some notable upside surprises in European business surveys and US regional business surveys. However, the headline composite PMI business survey indicators for the US, eurozone, Japan and the UK remain below 50. Taken at face value, remaining below 50.0 would normally signal that these economies are still shrinking. However, mapping PMIs accurately to economic activity levels is somewhat hazardous after such a big shock to GDP (the survey asks whether things are better/worse, rather than by how much). Nevertheless, if you look at the commentary in the PMI surveys – social distancing has eased, helping many firms reopen and firms are more optimistic, but many companies also report weak demand as customers remain cautious. That is – so far – consistent with economies taking time (likely, several quarters) to get back to ‘normal’ levels of activity after a sharp initial recovery phase.

US data continue to suggest a strong start to the early stage recovery, but virus data more worrying: May retail sales, durable goods orders and some housing data have bounced significantly more than expected. However, US COVID-19 numbers have, in the meantime, become more worrying. The increase in virus cases in some states is likely to worry consumers, including the prospects of social distancing being reversed and the impact on job security. Meanwhile, Congress and the White House have still not agreed a package of economic support measures to replace those set to roll off this summer. US government policy interventions have so far done a good job in shielding household balance sheets (and therefore spending power) from the crisis. Reduced/disrupted fiscal support and the progression of the virus both have the potential to curb US recovery momentum.

Here in the UK, data also signal a solid start to the recovery phase but also a weak underlying labour market and an economy still in need of policy support: May retail sales were also an upside surprise, rising 12% in May. They are still 13.1% below February levels, but that’s a solid start to the recovery phase, especially since it was only mid-June that saw ‘non-essential’ retail stores reopen. Just as in the US, however, the UK’s early stage recovery has needed – and still needs – plenty of policy support. Government borrowing was also somewhat higher than expected in May and the levels of government debt as a percent of GDP, on the headline measure, moved above 100% for the first time since 1963. PAYE data meanwhile show the number of paid employees fell by 449K March to April. Early May estimates indicate another drop of 163K. Job vacancies in May fell to a record low. The furlough scheme is set to start unwinding from August, but this is a labour market that is far from out of the woods yet. That was recognised by the Bank of England who extended their asset purchase programme, though reduced the pace. They have become more concerned about long-term damage from the crisis. How the labour market evolves from here will be a key driver of their decisions going forward including, potentially, a decision around negative rates.

Market view from Piers Hillier, CIO, RLAM

The upwards trend in global equity markets was met with some resistance this week, resulting in sideways equity trading and moderate credit spread widening. Investors were perturbed by a sharp increase in Covid-19 cases in the US as the country reported a record number of new cases on Thursday. While the coronavirus appears to be under control in most developed countries at this stage, global new case numbers are at record highs; driven by the US, Brazil and India. In an effort to mitigate the damage of a second wave, US regulators gave in to a long-sought demand for a relaxation of the Volcker Rule as they allowed banks to invest in hedge funds and private equity funds.

Markets have also been rocked by increased global trading tensions. There have been signs of further difficulties in the trade negotiations between the US and China. Meanwhile the US threatened to impose tariffs on $3.1bn of European products, prompting an angry response from the European Commission.

On a more positive note, numerous key economic data releases have been far stronger than anticipated recently. There have been strong improvements in US and UK retail sales and in the European and US business surveys. While activity surveys are still consistent with contractions in many economies, possibly reflecting the elevated corporate debt and unemployment levels, they show that businesses are markedly more upbeat as they emerge from the worst of the lockdowns.

Reflecting a perception that the UK economy is somewhat stronger than expected, the Bank of England surprised investors at its latest meeting. While it announced an additional £100bn of bond buying, as had been expected, it slowed the pace of its purchases. The Bank said it would spend the £100bn by the end of the year, rather than by the end of August as the market had hoped. Of course, the very fact that spending was increased reveals the fragile state that the Bank considers the economy to be in, with serious concerns over the unemployment outlook.

The focus for many in the UK has been on further opening of businesses – both non-essential retail in mid June, and with the prospects of pubs, restaurants and others opening from early July. As investors we are pleased to see this – we are under no illusions that we as a society will return to prior habits in terms of spending; many of us will feel differently about being on a train, plane or in a restaurant for some time. And with other countries seeing flare-ups in the virus, it is clear that this road will have a number of bumps in it. However, it does appear that we are now through the first phase of this crisis, and returning to a more normal cycle of data and market reaction.

Royal London is the UK’s largest mutual life, pensions and investment company. This in-depth market outlook by a market leading financial services organisation adds valuable insight to our consensus view of the markets. It is evident that in recent times these views have been dominated by the Coronavirus Pandemic, but we have also now been offered insight into the socio-political tensions that have recently risen, particularly in the US, and how they in turn are effecting the economy. This is an example of how frequently reviewing these updates gives us a better view of the ‘bigger picture’.

The opinions of market leaders are key to keeping our understanding of the markets up to date. A wide variety of these views from different sources help us paint a more accurate picture on the events of the world and how they are influencing market behaviours.

Please see the below update from Legal and General posted yesterday (29/06/2020) regarding the current situation in the US.

TheirAsset Allocation teamdiscuss their thoughts on the presidential election, the market’s likely reaction to what could happen, and the ongoing spread of Covid-19 in some states.

The electoral collage

Momentum is clearly with Joe Biden at the moment. Donald Trump’s handling of the pandemic and protests after the death of George Floyd have eroded his approval rating and have led to him losing ground in poll after poll.

Biden has always held a lead in national polls, but that advantage in poll averages has jumped from 4% in May to 10% now. Arguably even more worrying from Trump’s perspective are polls in swing states also shifting significantly towards Biden, and losses of support among both older voters and even his most reliable base of ‘white, no college’ voters.

Nevertheless, don’t count Trump out (again)! Our baseline remains that it will be a tight race to the end. The heat Trump is taking from the dual crises could calm down and the economy may well look stronger by November. Trump’s strategy again seems to be all about turning out his base. If he can get all of the 35-40% of voters that back him no matter what to turn out to vote, then it will take much more excitement about Biden from the rest of the electorate than is evident so far for him to beat Trump.

It should go without saying that it’s still early in the race and a lot can and will happen. To mention only a few wild cards: What will the economy look like in late October? What if there is a second wave of the virus in the autumn? What if a significant number of people get sick after Trump rallies? What if states need lockdowns on election day? What if targeted lockdowns inadvertently favour Democrats or Republicans? What if COVID-19 influences turnout differently among age cohorts? What if Trump or Biden themselves become ill?

Blue wave versus Trump 2.0

We would not expect a big equity market reaction to any type of divided government. If Trump wins, it would be roughly the status quo; under Biden, it would likely prevent many of the most market-moving policies in either direction.

Yet a Biden victory of any flavour could still bring a few market-related policy changes. America’s China policy would largely remain unchanged in substance, but could become less volatile in style. A multilateral approach to China should make an all-out trade war with the EU less likely. Tech regulation should continue to tighten gradually but, unless personnel choices say otherwise, this has not been a policy area Biden about which has shown particular passion. Generally, expect the policy direction to be more social, more green and more redistributive.

On the other hand, a ‘Blue Wave’ in which Democrats control Washington would be the most market-moving outcome, in our view; this has become the single most likely outcome in betting markets. In short, from a market perspective, this would imply higher corporate taxes and more fiscal spending. Even if these two ultimately balance each other out, the market’s gut reaction seems likely to be negative.

And what would Trump 2.0 look like? The desire to be re-elected has arguably been a moderating force on Trump’s policy choices around issues like the trade war. But in a second term this factor disappears. So what does Trump want to achieve with a second term? Money? Power? Policy? Legacy? Dynasty? We don’t have a clear answer for this question yet. Either way, it is unlikely that Trump 2.0 will be calmer than Trump 1.0.

The only two things we are certain of are that the campaign will get very ugly, and that if Trump loses he will not go quietly into that good night.

Houston, we have a problem

The virus continues to spread at an alarming pace in southern states, with the one-week change approaching Italian peak levels in California, Texas and Florida – a risk James highlighted over a month ago. We don’t think this is due to greater testing (which would dilute the share of positive test results). State governors are becoming concerned, with some Texan cities suspending elective (non-urgent) surgeries to free up hospital capacity.

By and large, the re-opening of the local economy is being ‘paused’ rather than ‘reversed’. But new research from the University of Chicago argues that lockdowns only account for 7% of the loss of economic activity. Instead, it is fear that prevents people going out. The study calculated this by examining economic activity in border towns located between different regulatory regimes.

Apple mobility data also suggest Texans are already cutting back on activity, and there appears to be an inflection point with activity levelling off in the median US state.

From a market perspective, there has been a tug-of-war between economic data continuing to paint a V-shaped recovery picture and deteriorating virus newsflow. We would argue that equities are pricing something at the optimistic end of our Scenario 1, implying there will be little market tolerance of signs the virus is significantly slowing down the economic recovery. But at the same time, the starting point for sentiment is already slightly bearish, so it would not take much of a correction to turn our sentiment signals much greener.

As you can see from this update (and from the news!), the situation in the US looks problematic, with no resolution in sight. The run up to a presidential election is always volatile and this one is likely to no different (if not worse due to the Covid-19 situation).

It will be an interesting few months for the US in the run up to November.

Keep an eye out for further updates here on the US and the impact of their Covid-19 and election struggles, and of course general market updates and other content which we continue to post regularly.

Our regulator is working on the advice market and helping to manage risk in this area. We recently completed a return for the FCA that focused on how we are dealing with the pandemic and our business and financial resilience.

I am pleased to say this did not pose a problem for us and we are comfortable with our current position with the focus on keeping ‘business as usual’ for our existing clients while keeping our staff safe.

We have extracted the precis of the FCA’s current views from a third-party compliance business’ blog in an email received on Friday 26/06/2020:

understand firms’ financial resilience so that firms can fail in an orderly manner

markets can function enabling price formation and orderly trading activity

customers are treated fairly

customers are aware of the risk of, and protected from, scams

In her speech earlier this month, The FCAs Executive Director of Supervision, Megan Butler outlined the regulators response to COVID19 and expectations for the rest of 2020.

The speech Highlights:

In operational terms, advisers and wealth managers responded well to the onset of the coronavirus (Covid-19) crisis.

Whilst acting with speed has been the absolute priority, as the industry adapts to the long-term impact of coronavirus, there is a need to transition from the immediate ‘incident response’ towards focusing on longer-term impacts. In her speech to PIMFA’s members, Megan Butler explores the FCA’s priorities and longer-term expectations for the wealth management and advice industry.

Key areas of focus for the FCA include operational resilience in light of coronavirus, financial resilience (and within that the preservation of client assets and money) and acting with integrity.

On the latter, the FCA has identified some firms which have tried to avoid their liabilities to customers by closing down companies and setting up new ones. These practices are unacceptable, and the FCA will continue to take action against firms conducting such activities.

To ensure that firm’s stay on track with risk management, operational and financial resilience and customer focus, the FCA will be focusing on key outcomes:

Client money and custody assets: They see an increase in clients running to cash, so firms are being encouraged to return finances that will not be invested in the short term and/or if firms are facing wind-down.

P and B IFA response: At inception of our business we decided not to hold client money to minimise risk to our clients. This is not an issue for us.

Suitability and advice and discretionary investment decisions are (as always) front and centre of treating customers fairly and in their best interests, but will be scrutinised in particular around firms’ response to the pandemic

P and B IFA response: Our key focus during the pandemic has been servicing our existing clients. Our Due Diligence process on investments has been enhanced with additional criteria. One area of interest is the ESG approach of Fund Managers. ESG stands for Environmental, Social and (Corporate) Governance.

Acting with integrity when it comes to charging appropriate fees is paramount

P and B IFA response: The standard ongoing advice fee for UK IFAs is c 0.79% per annum according to our third party compliance consultants, with many IFAs targeting 1% per annum. We remain competitive against our peers with our ongoing advice fee at 0.50% per annum.

Firms need to continually showcase they have adequate systems and controls to manage Financial crime and market abuse

P and B IFA response: We remain committed to fighting financial crime. At our weekly Team Meetings and monthly Board Meetings we discuss risks, scams and blocking financial crime. We have systems and controls in place to protect our clients and our business.

There is a keen focus on pension transfer activity, with their detailed guidance on advisers providing triage, abridged and defined benefit pension advice.

P and B IFA response: Due to regulatory and compliance input and escalating Professional Indemnity Insurance costs we have withdrawn from Defined Benefit Pension Transfer Advice.

Finally, there is a focus on the future of regulation, with a move to an outcomes based focus with new regulatory principles covering:

Adaptive shift from ‘regulation and forget’ to iterative and responsive approach

Results and performance driven regulation rather than defining a way, thus providing freedom to choose strategies

Risk weighted approach, shifting to data-driven from one size fits all risk evaluation

Finally, a collaborative strategy which aligns regulators nationally and internationally

It is good to see that our regulator, the FCA, is keeping an eye on advice businesses in the UK during this time of heightened risk. We have taken appropriate actions to ensure quality ongoing advice is provided to our existing clients at this time and to lower our business costs for the time being.

We understand clients need to be kept up to date and constantly upload new blogs to keep you informed and email clients when appropriate during this pandemic crisis.

Our resilience and business continuity plans have been tested and we have adapted quickly to providing advice on a Covid-19 risk free basis (from a distance). We will continue to monitor and try to improve our resilience and business continuity plans.

We are not sure how long this will last; it could be a while yet. Personally, I am really looking forward to normal ‘business as usual’ when I can see my clients again!

Please see the below article posted by Jupiter earlier this week from their Global Sustainable Equities Fund Manager, Abbie Llewellyn-Waters:

‘Several sustainable themes have continued to accelerate as a result of the Covid-19 crisis, said Abbie Llewellyn-Waters, Fund Manager, Global Sustainable Equities.

Firstly, momentum for environmental policy has gathered pace, despite the fragile state of the global economy. Policymakers have been quick to draw the link between the coronavirus and the environment – like viruses, greenhouse gases care little for borders. The debate around carbon policy, and specifically carbon tax, has notably accelerated. Abbie remarked on the recent write-downs and substantial price disparities within the oil sector as a further pressure point for tightening carbon policy.

There has also been important research quantifying pollution reduction, one of the few positives from this crisis, said Abbie. As a result of the global measures to combat Covid-19, the IEA expects global CO2 emissions this year to decrease to levels of 10 years ago. This is significant and could support the case for a more agile economic culture that includes more working from home. It is effectively an ‘investment-free’ solution to help deliver the legal commitments of the Paris Agreement.

There also continues to be strong momentum in human capital management within the sustainable companies that Abbie and the team focus on, with an increasing correlation between low staff turnover and high recurring revenue models.

Finally, another interesting new theme is the increasing attention on sustainable supply chain management. For years, efficiency has been the overriding aim in supply chains – “just enough, just in time”. Covid-19 has shifted the focus to security. While this has implications for working capital, it also offers new revenue opportunities. For example, infectious diseases have previously been mischaracterised as an issue mainly for developing markets. But a company Abbie recently spoke with highlighted that R&D investment into non-Covid infectious diseases in developed markets has already increased, which has the potential to create entirely new revenue streams not previously captured by analysts. All in all, Abbie expects the journey ahead to be much more complex than the markets rally suggests.’

Socially responsible investing has now gone mainstream and is a key focus for investors with a ‘put your money where your values are’ approach becoming more and more common.

ESG (Environmental, social and governance), which is a ‘set of standards for a company’s operations that socially conscious investors use to screen potential investments’ is now under the spotlight in this industry.

Keep your eye out for more blog content on this over the next few months as we at People and Business, develop our own ESG processes and scrutinise these criteria within the companies we use for our clients.

Hot off the press, I’ve just come off a webinar update from Prudential notifying us of the following positive Unit Price Adjustments (UPAs):

Series E only

PruFund Growth + 2.58%

PruFund Risk Managed 4 + 3.00%

PruFund Risk Managed 5 + 2.56%

The underlying unsmoothed assets were tested against the smoothed prices, the corridors, at 10.56 this morning.

You might ask why we have different UPAs for the different versions of PruFund? For the following reasons:

Different asset mix

The starting position

Different smoothing limits

The last point, different smoothing limits, doesn’t apply to the three funds we use noted above. The monthly smoothing limits in use for the funds we use is 5%.

Please see this link for details on how ‘smoothing’ works:

Brewin Dolphin’s weekly market update, emailed on 23/06/2020 as below:

Global shares rebounded last week but have still not made up for the losses incurred in the previous week’s sell off. Equity indices in the US rose yesterday and Asian markets were flat or slightly up, while in the UK and Europe, share markets closed down. However, markets got a boost today after President Trump said that the Phase 1 trade agreement with China was still “intact”. As a result, Asian markets closed higher on Tuesday, while equities in the UK and Europe were heading up in early trading.

Last week’s gains*

FTSE100: 3%

Dow Jones: 1%

S&P500: 1.85%

Dax: 3.2%

Nikkei: 0.77%

Hang Seng: 1.4%

Shanghai Composite: 1.6%

*Data to close on Friday 19 June

Virus treatment breakthrough

The positive news on the virus front was that Dexamethasone, a cheap, widely available corticosteroid significantly reduces death rates in severely sick Covid-19 patients. Sadly, this doesn’t slow transmission and is therefore unlikely to materially affect the willingness of policymakers to allow a full resumption of economic activity.

Cases rising globally

And there wasn’t much more good news on the virus front. The big picture globally has not changed; the trend in new cases remains up, driven by increasing numbers in emerging countries such as Brazil, India, Pakistan, Mexico, Saudi Arabia, Bangladesh, Indonesia and South Africa.

Perhaps the most worrying growth is in the southern states of America where hospitalisations are beginning to put real pressure on ICU capacity in Alabama and Arizona.

A new outbreak in Beijing has hopefully been rapidly suppressed, albeit at the cost of intensified lockdown efforts in one of China’s most important cities.

The trouble with easing lockdowns…

In Europe case numbers have stopped falling and, as efforts have switched towards reopening the economies, there has been a clear failure to decisively suppress the virus.

This is particularly marked in the UK where we are less than two weeks away from the Fourth of July, when bars and restaurants could be allowed to reopen. Boris Johnson is due to make an announcement on the reopening of parts of the hospitality sector this week.

UK case numbers have stopped falling which must make it difficult to proceed with lifting lockdown at anything other than a very cautious pace.

Wall Street not so far from Main Street

Whilst there is a lot of scepticism about how the recent rally in markets is disconnected from the real economy, our research shows that, in the US at least, the retail sector has proven to be freakishly well-aligned with the stock market after rebounding strongly in May. Where it is disconnected is further upstream, with industrial production barely staging any recovery at all.

US Retail sales vs S&P 500 Source: Refinitiv Datastream June 2020

Chinese stimulus

After holding off from their traditional recipe of credit and infrastructure growth, the Chinese authorities have found themselves resorting to that playbook again. Excavator sales have picked up as fixed asset investment by state owned enterprises has begun outperforming private sector investment, just as it did during 2016. Money supply growth has been picking up and the authorities are particularly keen to see funds deployed to Chinese small and medium sized enterprises which account for 80% of Chinese employment.

UK asset purchases to slow down

It is far from clear how the Bank of England would react to supply shock-induced inflation, but for now the policymakers remain in reasonably dovish mood. The Bank kept interest rates unchanged last week but increased its asset purchase target by £100bn. However, it is spreading that out over the remainder of the year, rather than the next three months, marking a marginally more hawkish announcement than had been expected.

That saw a rise in gilt yields as it means net issuance (i.e. bonds not bought by the Bank of England) is likely to be higher over the coming three months, although we don’t yet know how evenly the Bank will spread out its purchases. We think there may be modest upside for yields, notwithstanding the Bank’s generally dovish mindset. Recent movements in commodity prices, the rally in oil and a slight pickup in economic activity would all be consistent with rising gilt yields.

Pull out quote suggestion “UK case numbers have stopped falling which must make it difficult to proceed with lifting lockdown at anything other than a very cautious pace.”

Capital and income from it is at risk.

Neither simulated nor actual past performance are reliable indicators of future performance.

Performance is quoted before charges which will reduce illustrated performance.

Investment values may increase or decrease as a result of currency fluctuations.

The information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness.

A good input from Brewin Dolphin with regards to the global shares rebounding last week. The weekly market updates from Brewin Dolphin are useful given the current volatility we are experiencing.

Keep checking back for regular up to date blog posts.

Please see the below investment outlook received from J.P. Morgan today (Tuesday 23rd June):

In Brief

In early June the market was pricing in a V-shaped recovery from the pandemic-driven economic contraction. We expect the recovery to be more gradual, with a few stop-starts along the way. Extremely low interest rates will help, but unemployment and corporate deleveraging could be a drag on growth.

The extent of near-term uncertainty, as well as the potential for political risk to mount as we approach the US election, could generate more market volatility.

For individual market sectors, the outlook depends on the path of the pandemic. If a full and sustainable reopening of the economy becomes possible, we may see a further rally for the most beaten-up sectors, coupled with a style rotation. For now, we believe it makes sense to maintain a nimble approach, with a focus on quality and an eye to ESG risks.

Low-risk options for income seekers are increasingly scarce. Rather than stretching for yield, investors may be better off being selective within fixed income and using a wider range of income-providing asset classes, including real assets for those who can accept lower liquidity.

Developed market government bonds look less and less likely to play their traditional roles of providing income and protecting portfolios in periods of market stress. Investors may need to look beyond the traditional 60:40 portfolio, with a greater role for alternatives and flexible fixed income strategies.

No one predicted that in the first half of 2020 the world’s economies would be brought to a virtual standstill by a global pandemic. Even had we have known the virus was coming, we would not have predicted that by mid-year the S&P 500 would have managed to climb back above 3000 (EXHIBIT 1).

We have global policymakers to thank for the market’s resilience. According to current analysts’ expectations, the policy response has helped one-year forward earnings expectations to find a floor and start to improve. In the sharp rally since 23 March, markets looked to be pricing that the combined actions of governments and central banks in recent months will have successfully absorbed the economic losses of Covid-19 to engineer the perfect V-shaped recovery (EXHIBIT 2).

While the policy response has been commendable, we believe the market’s expectation of the recovery in early June was too optimistic. It’s not that we believe people will permanently change their behaviour – we are social animals, after all. We just think it will take a little longer to get back to full normality.

Chief among our concerns is that the virus itself may linger and some need for social distancing will remain, in countries such as the US and UK, at least. In addition, high unemployment and a dramatic increase in public and private debt may serve to restrain spending in the recovery. We may also be at the beginning of a period of difficult political fallout as politicians seek to apportion blame for the crisis. The US election of 3 November could have important market implications. With the UK having left the EU but not yet having secured a new trade deal, Brexit might also – once again – generate volatility.

In summary, we acknowledge that the commitment from governments and central banks shouldn’t be underestimated. And, if more stimulus is needed, it will come. This makes us cautious about being underweight risk assets. But we need to see that policy action is influencing fundamentals. Valuations and uncertainty around the economic and earnings outlook make us cautious about advocating an overweight position in equities. We therefore think investors may benefit from having more than one toe in this rally, but not from jumping in with two feet.

In what follows, we provide greater information on our view of the shape of the recovery. We then consider three investment themes for the second half of the year:

1) Considerations for investors in the near term, given uncertainties and potential volatility

2) Options for investors in need of income

3) Rethinking a 60:40 portfolio in a world of zero bond yields

WHAT SHAPE WILL THE RECOVERY TAKE?

As shutdowns are eased around the world, forecasters are debating the likely shape of the recovery. The optimists point to a V-shaped recovery, the pessimists L-shaped, and the cautious look for something less linear, such as W, U or √.

In truth, it is very difficult to know at this stage. The risks aren’t black swans, they are known unknowns, but we simply don’t have enough information at this stage to form our judgment.

The first set of known unknowns relates to the virus itself. As the economic and fiscal costs have become apparent, politicians have hurried to ease shutdowns, whether the infection is under control or not. It is possible that the combination of a degree of ongoing social distancing, track and trace systems, and better hygiene practices will mean that the reopening happens without a reacceleration in infections. But there is also a risk that the infection rate will pick back up. Governments may be reluctant to re-impose shutdowns in such a scenario, but there will still be economic costs if people choose to socially distance voluntarily (EXHIBIT 3).

We are closely tracking how the virus progresses as well as using high frequency data to gauge the extent to which economic activity is normalising (EXHIBIT 4). To find the latest statistics on these, please refer to our On the Minds of Investors piece, Monitoring the global impact of Covid-19, which is updated twice a week.

As the weeks and months drag on, the more lasting consequences of the recession will become more evident. Policymakers globally have made a gallant attempt to limit the impact and absorb the losses of Covid-19. Grants and subsidies aimed to shift the losses on to government balance sheets. These, in turn, were shifted to central bank balance sheets as asset purchase programmes were expanded to absorb the additional issuance. Governments have been able to issue record high levels of government bonds, at record low interest rates.

Furlough, or short-shift schemes have been the cornerstone of the policy response in Europe (EXHIBIT 5). However, unemployment has still risen in the UK. The moves on the continent of Europe have been more moderate, but we suspect this is flattered by people not categorising themselves as unemployed because they are not actively looking for work due to either a need to look after children or a choice to remain socially isolated.

In the US – which hasn’t adopted widespread furlough schemes – unemployment rose to 14.7% in April though came down slightly in May to 13.3%. We would be considerably more worried about a double-digit unemployment rate were it not for the fact that the US social safety net has been made considerably more generous. Indeed, estimates suggest that 75% of those that have lost work are in fact better off given the additional USD 600 a week that has been added to unemployment benefits. This boost to benefits is set to expire on 31 July and, though an extension of some sort looks likely, it is likely to be less generous. We are therefore monitoring labour market data closely to gauge any shift in unemployment from those currently classified as temporary to permanent (EXHIBIT 5).

What will be the lasting consequence of higher levels of public debt? Is a new wave of austerity ahead? Public sector pay and benefit freezes – which were an important component of the spending restraint in the last expansion – seem unlikely given the degree of austerity fatigue in the population. Wealth taxes may be appealing given the resilience of asset prices, but these policies run into the practical problem that much of people’s wealth is stored in housing assets and held by individuals that are asset rich and income poor. One off ‘Pigouvian’ income taxes on higher earners are also being touted. We see it as more likely that finance ministers will forge ahead with plans to tax the large multi-nationals that obtain tax advantages by choosing favourable domiciles.

There is one global debt-reducing strategy we see as almost inevitable: interest rates will be held down for the foreseeable future. One suspects that policymakers are hoping for a repeat of the post-war period, in which a combination of yield curve control and financial repression kept the interest rate below nominal growth and helped erode government debt as a percent of GDP (EXHIBIT 6).

Lower interest rates will help corporates, which, on aggregate, have also experienced a significant rise in debt as a result of Covid-19. While we don’t expect governments to focus on deleveraging, the same may not be said for the corporate sector. Corporate deleveraging may constrain investment spending and employment growth and, in turn, the economic recovery.

So what is the letter most apt to describe the economic recovery? Our standard alphabet might not suffice but, in our view, expecting a symmetrical V is too optimistic. The recovery is likely to be more gradual, with a few stop-starts along the way. All the while, investors should be mindful of some sizeable tail risks lurking.

One such risk is China’s relationship with the world in the wake of Covid-19. Our opinion is that de-globalisation is easier (politically) said than done. China is highly integrated in global supply chains. As the 2019 trade war demonstrated, it is very hard to reduce trade links without causing significant economic harm in western economies. However, it does seem likely that China will come under scrutiny for regulatory standards, which may in turn raise inflationary pressures. Despite the economic realities, rhetoric towards China may intensify for short-term political reasons.

Nowhere is this more evident than in the US, which enters full election mode in the coming months. At this stage it is still difficult to say anything definitive about who will win, whether the victor will have full control of Congress, or the impact on markets.

The top priority for whoever emerges successful will be to manage the recovery as the economy restarts in earnest in 2021. Tough choices will need to be made about whether to push on with further stimulus or to try to tighten the purse strings as the recovery takes hold. President Trump had already flagged his desire for a second round of tax cuts prior to Covid19, but with US national debt-to-GDP now set to rise above 100% this year, further corporate tax cuts could face greater opposition. While Trump is yet to lay out a clear agenda for a second term, the tough-on-China and tough-on-trade stances that were at the core of the 2016 Republican campaign will remain a key tenet of his approach.

For the Democrats, as the most left-leaning candidates exited the primary race, so did their policies. Yet it is clear that presumptive nominee Joe Biden’s vision for corporate America is still very different to that of President Trump. Two topics that investors will need to monitor closely are a proposal to use anti-trust legislation to clamp down on ‘Big Tech’ and plans for corporate tax changes. Biden’s campaign team has also been keen to emphasise its candidate’s tough-on-China credentials. Historically, escalating trade tensions have favoured the higherquality US stock market relative to other regions, but a ramp-up in pressure on the tech titans would pose risks to US market leadership given the high weights to the technology and communication services sectors in US indices.

The second half of the year may therefore put us in the unusual position in which the political risk premium may be higher on US assets than on those of continental Europe, where the signs look increasingly positive. Though it still needs to be ratified by all EU member states, the European Recovery Fund is a significant step forward. Not only will it provide invaluable short-term help for countries like Italy but it provides a strong signal for the long term with regards to the fiscal integration that is much needed to complement the monetary union.

If the recovery in the US lags due to lingering Covid risks, and perceptions of political risk change, we could see downward pressure on the dollar.

CONSIDERATIONS FOR INVESTORS IN THE NEAR-TERM GIVEN UNCERTAINTIES

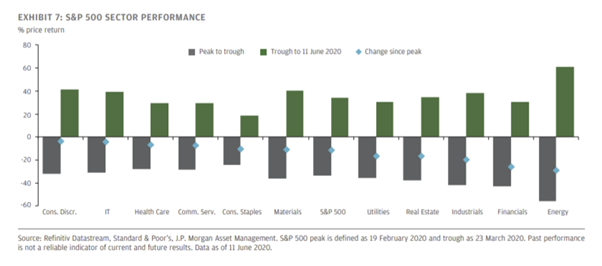

While the S&P 500 suggests a V-shaped recovery is priced in, at the sector level the narrative is more nuanced. From the start of the year to the S&P 500 trough in March, some of the most obviously affected sectors were hardest hit. Meanwhile, the likely winners from people remaining at home, other than for their food shop, outperformed.

The bounce-back since March has included some of the worst performers during the sell-off (EXHIBIT 7). For example, energy, autos, clothing retailers and restaurants have all outperformed during the rally, presumably on hopes of a partial rebound in activity as the economy starts to reopen. But some of the perceived beneficiaries of a world with more working and shopping from home, such as home improvement retailers, tech companies and industrial (including warehouse) properties have also rallied strongly. Meanwhile, despite improvement from their lows, airlines, hotels, department stores and retail properties remain among the weakest performers year to date.

What are the risks and opportunities from here under different potential scenarios:

Scenario 1: A full and sustainable reopening of the economy with social distancing no longer required. The most beaten-up sectors could rally further, while the sectors that have gained the most could be vulnerable to profit taking and rotation into cheaper companies as it becomes clear we won’t all work and shop from home forever. This would also likely coincide with a style rotation from large cap to small.

Scenario 2: An acceleration in infection rates leading to renewed shutdowns. At least part of the rally since March could reverse for most sectors, but those most exposed to further shutdowns could suffer the most as solvency concerns increase.

Scenario 3: Partial reopening of the economy but with some social distancing remaining in place. Sectors that might be able to reopen with some social distancing, such as department stores, autos and energy, could benefit further. Airlines, hotels and dine-in restaurants could struggle as solvency concerns increase. The most expensive stocks among the current winners could also suffer from valuation deratings and earnings disappointments, as unemployment remains elevated.

Which scenario plays out depends largely on the path of the virus itself, which is unknown. Given this uncertainty, we think it makes sense to avoid potential value traps, where solvency concerns could increase further. But we also think it makes sense to avoid the most expensive companies, where there is a lot of good news already in the price.

We also think this recession will increase the momentum behind sustainable investing. Robust ESG screening processes should capture the risks to corporate earnings from potential changes to taxes and other political interventions. The crisis has underscored the benefits of screening companies on nonfinancial metrics such as corporate governance and human capital management. We believe companies will increasingly be rewarded for demonstrating responsible capitalism given that there are, unfortunately, likely to be more lasting consequences of this recession for lower income and minority groups. Finally, although governments will be strapped for cash coming out of this recession they will also been keen to support infrastructure projects that can fuel the recovery. We expect these projects to be focused on the shift to a zero-carbon economy. The European Green deal is one such example.

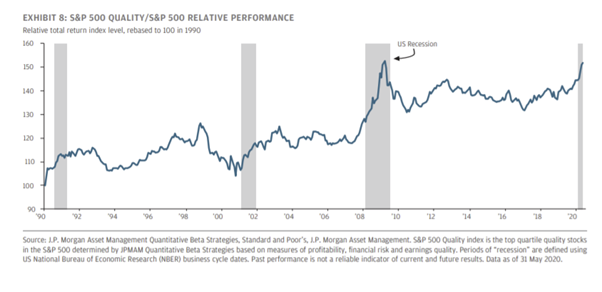

An active, nimble approach, with a current focus on quality companies (EXHIBIT 8), a keen eye on valuations, and consideration of ESG risks, therefore appears the best way of navigating the uncertainty facing investors.

SEEKING SUSTAINABLE INCOME

Central bank actions so far this year have performed the essential role of keeping government borrowing costs low but, for those seeking income, the negative side effect is that lowrisk income options are increasingly scarce.

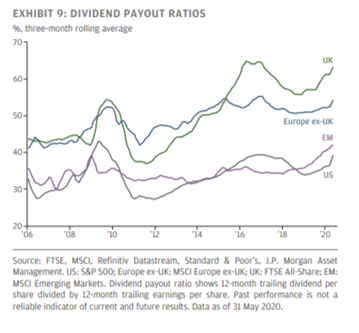

Investors have been turning to higher risk asset classes, including equities, for income over recent years, yet dividend cuts have become a hot topic as companies look to shore up balance sheets against the shock from Covid-19. While we acknowledge that many companies – particularly those who are receiving government support – may find it difficult to maintain payouts over the coming months, it is essential not to mistake what, for many firms, will be a cyclical issue for a structural one. On a regional basis, we see US dividends as most resilient. The lower dividend payout ratio of the US market provides companies with more flexibility to maintain dividends in periods of weaker earnings. Higher use of buybacks provides a buffer for companies to cut before dividends are hit. Regulatory pressure on banks, in particular, has also been lower so far in the US than in Europe.

Riskier parts of fixed income, such as corporate credit and emerging market debt, are other areas that may warrant attention when hunting for income. The Federal Reserve’s decision to buy both investment grade and high yield credit for the first time helped to pull spreads back from their widest levels in March, but credit spreads still sit significantly above their levels of the start of 2020. Central bank purchases in both the US and Europe should provide something of a backstop for corporate bond prices in the second half of the year, although we advocate an increasingly selective approach as investors move further down the quality spectrum and the need to differentiate between (more temporary) liquidity issues and (more permanent) solvency issues becomes more important.

Outside of fixed income, real assets may also have a larger role to play in portfolios as an alternative income source. While asset prices in areas such as infrastructure have not been immune to the pressures seen in public markets so far this year, income streams have broadly remained stable. But, of course, investors will need to be able to accept lower liquidity as the trade-off for moving into these types of asset classes.

The risks of overstretching for yield when hunting for income have been made very clear by the market volatility so far in 2020. Higher levels of income can only be achieved via higher levels of risk in some shape or form. Rather than ramping up risk to achieve a fixed yield target, income-seeking investors may be better off using a wide range of asset classes to build well-diversified portfolios that are in line with their risk appetite, and accepting the level of yield available as a result.

60:40 WHEN BOND YIELDS ARE NEAR ZERO

Perhaps the clearest investment challenge that will endure well beyond Covid-19 is that of how to construct a portfolio in a world of very low government bond yields.

Government bonds have traditionally played two roles in a portfolio. One is to provide a steady and stable source of income. The other is to protect a portfolio in times of market stress. Traditionally, recessions would coincide with central banks cutting interest rates, sending bond prices higher at a time when stock prices were falling. This reduced the overall scale of capital loss in bear markets.

As we look ahead, developed world government bonds don’t look like they will serve either purpose. Even long-duration government bonds provide very little – if any – income in much of Europe. And unless central banks entertain the idea of taking interest rates into negative territory (or deeper negative territory, for those already deploying negative interest rates) then bond prices cannot rise much in periods of market stress.

Meanwhile, shifting to, say, a 90:10 allocation or substituting government bonds for high yield bonds would help boost return prospects but result in a portfolio that was far less able to weather bouts of volatility.

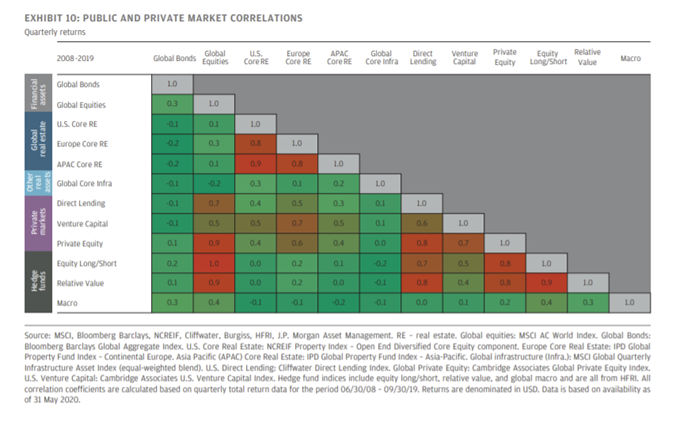

The challenge is therefore to find assets that have low correlation to stocks and ideally provide income along the way. While there are still highly rated government bonds – such as Chinese government bonds – that offer modest positive yields, in our view it may be better to look to the alternative markets. EXHIBIT 10, taken from our Guide to Alternatives, shows the asset correlations. Within liquid strategies, macro funds have tended to do a good job of providing downside protection. Less liquid options include direct real estate and core infrastructure, which both have relatively low correlations to stock markets and offer relatively strong income.

J.P. Morgan is a global leader in financial services, offering solutions to the world’s most important corporations, governments, and institutions in more than 100 countries. This in-depth analysis of markets by a world leading financial services organisation can prove valuable as we venture into the unknown as Coronavirus restrictions are gradually loosened and we attempt to return to ‘normal’.

We still believe now as much as ever that gaining a consensus view of the markets by reviewing the opinions of a variety of market leaders is key. Market behaviour is very much on a knife edge right now, and it is important that we frequently review these views so that we are well informed and in turn can keep you up to date.

Please see below a blog received yesterday from Legal & General Investment Manager’s (LGIM) Asset Allocation Team, which outlines their team’s key beliefs within the markets at the moment.

As you can see from the above, global economic stimulus is expected and this will present some medium to long-term opportunities for investing. It remains important to stay invested in order to benefit from the economic impact of the proposed stimulus measures.

Please continue to check our Blog content for the latest investment, markets and economic updates from leading investment houses.

Please see the below article by AJ Bell received yesterday (Sunday 21st June):

This week’s online meeting of the European Union’s members to debate the proposed €750 billion COVID-19 recovery plan is vitally important economically and politically. For progress to be achieved and help offered to those who need it, amid predictions that EU GDP will drop by 8–12% in 2020, all 27 nations must agree on:

the amount of money to be spent, on top of an EU budget of some €1.1 trillion (itself a matter of some friction between member states);

the conditions for awards of the capital available, which appear to include both green and digital criteria for would-be recipients;

how the money is to be spent, and the mix between loans and grants; and

how and when the money is to be repaid and over what time period, starting in 2027.

The discussions are therefore an opportunity to present a united front, tackle the viral outbreak and shore up the EU edifice at the same time, just as the Brexit negotiations with the UK start to heat up again.

Coming of age

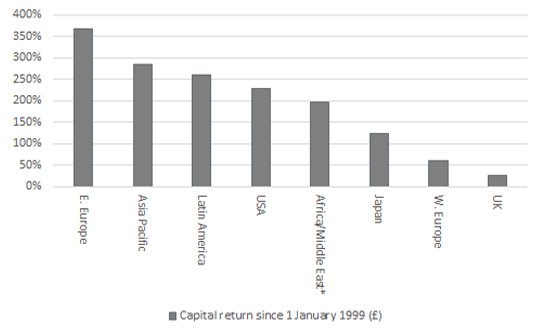

“From the narrow perspective of investing in stock markets, it seems that global capital is yet to be fully convinced by the merits of the European project.”

From the narrow perspective of investing in stock markets, it seems that global capital is yet to be fully convinced by the merits of the European project. The sterling-denominated performance of the Stoxx Europe 600 index ranks it seventh out of eight in capital terms since the euro came into being on 1 January 1999.

This poor performance may reflect the lingering effects of the debt crisis that first boiled over a decade ago, as well as the difficulties of providing a solid financial platform with which to support political union, in the absence of fiscal and banking union to support a single currency and unified monetary policy.

EU stock markets have lagged badly since 1 January 1999

Source: Refinitiv data. Capital return in sterling terms. *MSCI Africa/Middle East since inception in September 2003.

It may also reflect the different aims and needs of the 27 member states which are again becoming apparent as the recovery plan and budget come up for discussion.

The most serious questions of the plan are being asked by the so-called Frugal Four of Germany, Denmark, Austria and Sweden.

Failure to agree, in the twenty-first year of the existence of the single currency, would raise existential questions about the euro and the EU’s purpose and usefulness. Government is there to provide assistance in times of crisis above all others and, were the EU to fail to offer help to those nations which COVID-19 has treated most cruelly – notably Italy and Spain – then scope for further local disaffection with the supra-national powers in Brussels is considerable.

“Those nations which COVID-19 has treated most cruelly – notably Italy and Spain – suffered the most in the wake of the debt crisis that started in earnest just under a decade ago. Stock markets clearly believe they have not enjoyed anything like the same degree of economic benefits from monetary union as Germany.”

After all, these countries suffered the most in the wake of the debt crisis that started in earnest just under a decade ago. Stock markets clearly believe they have not enjoyed anything like the same degree of economic benefits from monetary union as Germany. (Eagle-eyed investors will note that two of the three best-performing developed European stock markets since the euro’s launch do not even use the single currency).

In stock market terms, the north looks like a clear winner under the euro compared to the south

Source: Refinitiv data. Capital return in local currency terms.

Great divide

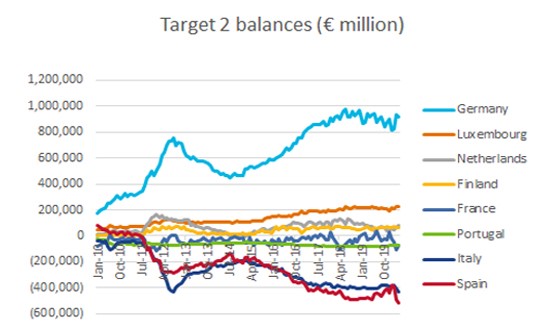

This north-south divide can be seen in another way, via the TARGET2 payments mechanism.

TARGET stands for ‘Trans-European Automated Real-time Gross Settlement Express Transfer’ system. In essence, the system is there to help balance trade flows but it could also reflect capital flows. Supporters argue that the TARGET2’s smooth functioning shows that it balances out the capital needs of the EU’s member nations. Sceptics assert that TARGET2 merely highlights huge capital flight from the south to the north and Germany in particular.

Germany’s TARGET2 surplus is still swelling even as French, Spanish and Italian deficits grow

Source: European Central Bank

No harm is done – unless an EU member defaults or drops out of the monetary union. Then those which have a positive balance are on the hook for the deficits of the member in the red. This may be why the €750 billion recovery plan alarms the Frugal Four, as they fear it could be the first step to debts being aggregated and funded at EU level, potentially leaving them to subsidise what they see as the spendthrift southern members.

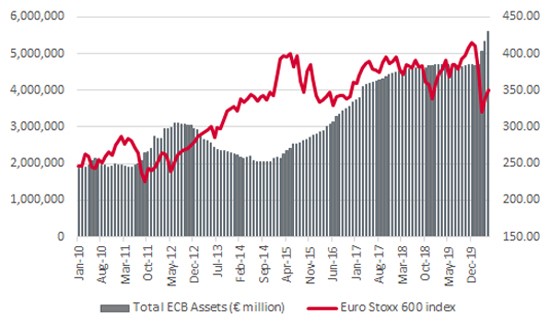

“The European Central Bank is doing its bit to keep the plates spinning and, as is the case elsewhere, quantitative easing (QE) is boosting equity and bond markets to at least create some kind of feel-good factor.”

The European Central Bank is doing its bit to keep the plates spinning, as it holds headline interest rates at zero and its €650 billion expansion of the Pandemic Emergency Purchase Programme (PEPP) to take the total to €1.35 trillion. As elsewhere, that quantitative easing (QE) largesse is boosting equity and bond markets to create some kind of feel-good factor.

More QE from the ECB boosts European equities

Source: European Central Bank, FRED – St. Louis Federal Reserve database, Refinitiv data

But whether QE provides a lasting solution is unclear. The cost of meeting each crisis – 2007–09, 2011–15 and now COVID-19 – is becoming ever greater each time. The euro is under less scrutiny than it would be, even if has lost 84% of its value against gold since its launch, because sterling, the yen and the dollar are also at the mercy of identical monetary policies (and all are down by more than 80% against the metal, too). Investors may not welcome another round of patch fixes and last-minute fudges from the latest series of talks, especially if they only serve to stoke further support for anti-EU parties in the south, should those nations start to feel neglected again.

This article was written by AJ Bell Investment Director, Russ Mould, who has been in that role since 2013. Prior to that he was a Fund Manager from 1991.

Views from experts in this industry help give us a view of the ever-changing landscape.

Keep checking back for our regular blog posts and updates.

Source: Refinitiv Datastream June 2020

Source: Refinitiv Datastream June 2020