Please see article below from AJ Bell received on Thursday afternoon – 14/04/2022.

How much will I get from the state pension?

A reader in their 60s also wants to know about pension credit

Thursday 14 Apr 2022 Author: Daniel Coatsworth

I’m 62 and have worked all my life, what am I likely to receive from the state from age 66 and how does pension credit work?

Sonia

Tom Selby, AJ Bell Head of Retirement Policy says:

The full flat-rate state pension is worth £185.15 in 2022/23 and you will qualify for it when you turn 66. In order to qualify for the full amount, you need a 35-year National Insurance contribution record.

You need at least a 10-year NI record to qualify for any state pension, with a deduction made for every year of missing NI you have. Once you have a 35-year NI record you cannot build up any more state pension entitlement.

The state pension system was reformed in 2016, meaning millions of people built up rights under a combination of the old system and the new system.

Anyone who built up state pension entitlements under the old system and hadn’t reached state pension age before 6 April 2016 has a ‘foundation amount’ calculated.

Anyone with a foundation amount equal to the full flat-rate state pension at 5 April 2016 would not have been able to build up any extra state pension – even if they added more qualifying years to their National Insurance contributions record.

Those with a foundation amount below the full flat-rate state pension could continue to build up qualifying years via NI contributions and boost their state pension entitlement.

People with a foundation amount worth more than the flat-rate state pension would receive the full flat-rate amount plus a ‘protected payment’ to reflect the extra entitlement built up under the old system. They would not gain any extra pension for further qualifying years they accrue.

Use this link to check your state pension entitlement.

Crucially, it is up to you to claim your state pension from the DWP.

Note that the state pension age is scheduled to increase to 67 by 2028 and 68 by 2046 – although a review of the state pension age is underway and due to be completed in 2023.

PENSION CREDIT

Pension credit is another key benefit provided by the state which tends to go unclaimed by lower income retirees.

In 2022/23, if you are over state pension age (66), single and your income is less than less than £182.60 a week then pension credit will top you up to that amount. For a couple, the combined income figure is £287.70.

In relation to pension credit your income includes your state pension, other pensions, employment or self-employment earnings and most social security benefits. As with the state pension, it is up to you to claim pension credit.

Please continue to check back for our latest blog posts and updates.

Please find below, a daily update on markets, received this morning from Brooks Macdonald – 14/04/2022

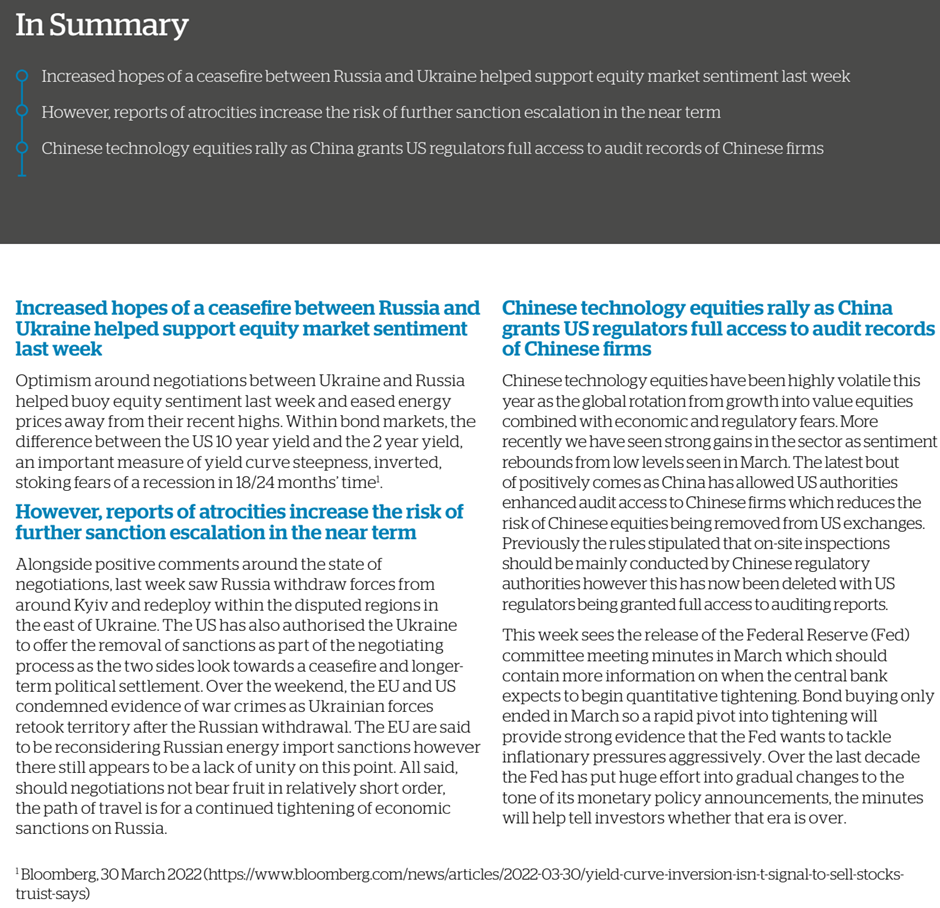

What has happened?

US bond prices continued the recent rally on Wednesday as markets pared back expectations for an aggressive series of interest rate rises from the US Federal Reserve. Following the latest US Consumer Price Index data for March published on Tuesday, which showed a weaker than expected core month-on-month rise in prices, hopes have risen that the near-term inflationary pressures might be at or near a peak. US 2 year bonds, which are more sensitive to monetary policy decisions, have seen yields fall more than 10 year yields this week, with the 10 year-less-2 year yield curve having risen around 40bps since the nadir at the start of the month. In equity markets, the principle of regional proximity to the Ukraine conflict weighed again on Wednesday; while equities were mixed in Europe, US equities were stronger, while across sectors, technology shares outperformed wider equity benchmarks. Overnight, Asia equity markets are broadly higher on reports that China’s policy makers may look to make further cuts in banks’ reserve requirement ratios alongside other policy tools to support the economy. Looking ahead to today the European Central Bank (ECB) holds its latest monetary policy meeting decision, though markets are not expecting much change to the ECB’s recently more hawkish messaging.

US calendar Q1 2022 company results season gets underway

The US bank JP Morgan kicked off the latest calendar Q1 2022 company results season on Wednesday. Seen as a bellwether for the broader US economy, JP Morgan reported profits which fell 42% in Q1 2022 compared to the same quarter period a year ago, and missing analyst EPS estimates amid a more cautious outlook generally. Aside the market impact from Russia’s invasion of Ukraine, investment banking revenue was lower as companies looked to have delayed deal activity in recent months. The US bank also increased reserves saying the possibility of an economic downturn had moved from ‘low’ to ‘slightly less low’. JP Morgan CEO Dimon warned of twin economic uncertainties arising from Ukraine as well as near-term inflationary headwinds. Putting pressure on policy makers, Dimon said “we remain optimistic on the economy, at least for the short term … consumer and business balance sheets as well as consumer spending remain at healthy levels … but see significant geopolitical and economic challenges ahead”. He added that “the Fed needs to try to manage this economy and try to get to a soft landing, if possible.” Asked whether the US could face a recession, Dimon said that “I am not predicting a recession. Is it possible? Absolutely.”

Brooks Macdonald’s Asset Allocation Committee weighs up the investment outlook

Brooks Macdonald’s Asset Allocation Committee held its latest monthly meeting on Wednesday, and as part of discussions, weighed up the latest investment outlook in terms of the twin market drivers of economic growth and inflation. While the broader economic growth outlook remains constructive and above longer-term trend rates of growth, the Committee are mindful that there has been a downward revision of estimates in aggregate. The Committee views a lower economic growth backdrop as likely given the impact that near-term inflationary pressures may have on the cost-of-living squeeze and corporate margins. Whilst it is too early to say whether inflation will slow meaningfully by the end of the year, the base effects mean that headline inflation is likely to slow even if inflationary pressures remain a theme into 2023.

What does Brooks Macdonald think?

Our Asset Allocation Committee is, in aggregate, presently somewhere between a so-called ‘Soft-Landing’ scenario (describing a low inflation, low economic growth outlook) and a ‘Stagflation’ scenario (high inflation, low growth). Whilst both of these scenarios might favour more growth/defensive investment styles, the Committee is maintaining its equity barbell balance at the current time. There is likely to be continued volatility in markets in the near-term as central banks in particular look to try to thread the policy needle against post-pandemic distortions and the war in Ukraine, and as such, we are keen not to be drawn prematurely in favour of either a growth/defensive or value/cyclical narrative.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please see below this week’s Markets in a Minute article from Brewin Dolphin received yesterday afternoon – 12/04/2022

US markets dip as taper talk returns

US markets dipped last week as Federal Reserve meeting minutes showed rate hikes are again likely, with officials confirming the central bank had to quell inflation.

In the week, the Nasdaq lost 3.86% with the S&P 500 also slipping 1.27% – though the latter was able to recover some of its midweek losses due to consumer staples and tech names which held up.

Across the Atlantic, the picture was more mixed in the UK and Europe. Over the week, the pan-European STOXX Europe 600 index rose 0.57%, with concerns over inflation and the ongoing Ukraine conflict continuing to suppress sentiment. On a country-specific basis, several markets recorded losses – such as the French CAC 40 index, which fell 2.04% due to political uncertainty. The FTSE 100 rose 1.75%, though the more domesticfocused FTSE 250 index better reflected inflationary concerns in the country, falling 0.52%.

In Asia, the Nikkei 225 fell 2.46% with Japan also being impacted by inflationary concerns and US Federal Reserve movements. In China, markets fell as well, with the Shanghai Composite Index slipping 0.94%. Lingering Covid-19 lockdowns across several cities partly caused these falls, as well as investors taking note of monetary policy and inflationary trends around the world.

UK growth stalls

Stocks started the week in the red, with investors around the world starting to price in expected rate hikes from central banks as well as more negative inflation news in the US. By the time markets closed in the US, the S&P 500 and Nasdaq were down 1.69% and 2.18% respectively.

The most notable economic news came from the UK, where growth has stalled. In February, economic growth slowed to just 0.1% which was dragged down by sluggish numbers in production and construction. This was down from the 0.8% GDP growth seen in January. This impacted investor sentiment, causing the FTSE 100 to lose 0.67% by close on Monday, with the FTSE 250 losing 0.28%.

The picture was the same in European and Asian markets. The pan-European Stoxx 600 index closed 0.59% lower, with nearly all regional markets lower as disappointing UK GDP figures were digested. In Asia, the Nikkei closed at 0.61% lower while the Shanghai Composite fell 2.61%.

Fed signals new rate hikes…

Last week, the Federal Reserve published the minutes from its monthly Federal Open Market Committee (FOMC) meeting, which revealed how policymakers are planning to reduce the central bank’s balance sheet. The plan is to reduce the balance sheet by $95bn a month, with officials also preparing to raise rates by 0.50% in May.

FOMC members are focusing on quelling inflation, which hit a 40-year high in March, when US CPI reached 7.9%. Policymakers will feel more confident in raising rates after improving employment statistics were revealed last week. According to the US Bureau of Labor, the US added 431,000 jobs in March, which reduced the country’s unemployment rate from 3.8% to 3.6%. Within this data, the weekly jobless claims tally fell to 166,000, which is the lowest since 1968.

This pushed bond yields higher in the week. By Friday, the US 10-year yield closed the week at 2.7% which is the highest level in three years.

…with ECB also setting hawkish tone

Last week the European Central Bank (ECB) also published minutes of its own meeting in March, ahead of its crucial meeting on Thursday. Policymakers were revealed to be divided, but overall were more hawkish, with many calling for rate hikes to prevent a wage-price spiral.

Though policymakers were split in how to proceed, with some preferring to see how the Russia-Ukraine conflict continues to unfold, inflation has risen since the ECB’s last meeting. Annual inflation in the eurozone is currently 7.5%, a record for the region.

Last week, the EU also imposed more sanctions on Russia off the back of reports of war crimes in Ukraine. These included a proposal to ban imports of Russian coal, and the assets of more Russian oligarchs to be targeted.

France set for close election

French President Emmanuel Macron will now face farright candidate Marine Le Pen in presidential elections, after they both made it through the first round. With 27% and 23% of the vote secured respectively, the race between the two looks tight before voters return to the polls on 24 April.

A few weeks ago, many commentators expected Macron to comfortably secure a second term. However, Le Pen’s early success has now made some investors wary about a potential change of political leadership in the country.

The prospect of a Le Pen presidency has caused concern among some investors, as she has shown sympathies for Russian President Vladimir Putin in the past and been openly sceptical about the European Union. Over the week, the CAC 40 index fell 2.04% in light of these political developments, with French bonds also sliding with 10-year yields hitting their highest peak since 2015.

IMF downgrades Japanese growth

Last week, the International Monetary Fund (IMF) downgraded its forecast for Japanese growth this year, from 3.3% to 2.4%. Uncertainty stemming from Russia’s war with Ukraine was cited as one of the main reasons, with Japan vulnerable to shocks across supply chains, trade networks and commodities.

Japan’s close trade-ties with China were also cited as a risk, with the latter coming under international scrutiny for failing to publicly criticise Russia over its actions in Ukraine. US government spokesmen recently stated if China was found to be supporting Russia, Beijing would also become the target of economic sanctions.

Please continue to check back for our latest blog posts and updates.

Please see below article received from Brooks Macdonald yesterday afternoon, which provides details economic and market news from their in-house research team.

Bond markets continue to drive equity market volatility as investors position for more aggressive monetary tightening

Last week was dominated by the ongoing bond market selloff as investors position for a rapid tightening in US monetary policy. This concern has also filtered into other global bond markets as major central banks, including the ECB, point to decade high inflation levels and an increased willingness to act decisively. Against this backdrop US equities underperformed, falling just over 1% whilst European equities proved more resilient as investors ponder whether the Euro Area has sufficient economic momentum to allow the ECB to tighten meaningfully.

President Macron’s first round electoral results point to strong support however investors keep an eye on the second-round run-off

Sunday saw a strong result from President Macron in the first round of voting with Marine Le Pen now entering the run off against him in two weeks’ time. The French equity market is seeing some mild outperformance today, reflecting the stronger showing from the incumbent versus ingoing expectations. Of course, the critical question now is which candidate will gather the votes from the supporters of candidates eliminated in round one. Polling suggests a tight run-off between the two candidates, but most polls show Macron ahead with a reasonable margin. Given how significantly the polling has changed over the last two weeks however, this will remain a hot topic for European risk assets.

This week’s ECB meeting may not see any major policy change, but markets will pay close attention to the bank’s tone

Thursday’s ECB meeting is likely to be an eventful one given the recent hawkish position from the European Central Bank. At the ECB’s last meeting in March, they announced a faster reduction in asset purchases than the markets had previously expected. The central question will be whether the bank sees the current guidance as sufficient or if it wants to increase the pace given the uncertainties around inflation levels. With the ink still not dry on the plan to reduce asset purchases, a meaningful change in policy this week is unlikely, however the tone of the ECB’s messaging may take another hawkish step which could create bond volatility.

While the market will need to wait until May for the next Fed meeting, the US CPI data released this week will be a factor in whether the Fed hikes by 25bps or 50bps in that meeting. This week also sees the beginning of the US Q1 earnings season which will give the market a good barometer for corporate health and margins given the current inflation pressures.

We endeavour to publish relevant content on a regular basis, so please check in again with us soon.

Please find below, a market update received from Blackfinch Group this morning – 11/04/2022

UK gross domestic product (GDP) rose just 0.1% in February, 0.2% less than economists expected. The UK economy is now around 1.5% larger than just before the UK’s first lockdowns two years ago, according to the Office for National Statistics.

The three storms, Dudley, Eunice and Franklin, which hit the UK in mid-February weighed on the construction sector, leading to a 0.1% drop in output.

UK house prices continued to surge in March, lifting the average house price to a new record high of more than £282,000. Since the first pandemic lockdown began two years ago, the average UK house price has jumped 18%, or £43,577.

UK households and businesses were hit by the biggest monthly jump in motor fuel prices in at least two decades. Average UK petrol and diesel pump prices increased by 11p and 22p per litre respectively in March, according to the RAC’s Fuel Watch.

The number of Americans filing for unemployment benefits fell to just 166,000, the lowest figure since 1968, according to the US Labor Department.

In the US, the total volume of mortgage applications fell another 6% last week, according to the Mortgage Bankers Association’s seasonally-adjusted index. This left mortgage applications 41% lower than one year ago.

In the Republic of Ireland, inflation as measured by the Consumer Price Index (CPI) jumped 6.7% in the year to March 2022, the highest annual inflation rate since November 2000.

German manufacturing orders fell by an unexpected 2.2% in February, in the run-up to Russia’s invasion of Ukraine. The decline, which was led by a drop in overseas orders, was much worse than economist forecasts of a 0.3% fall.

In Turkey, inflation soared to 61.1% in March, its highest reading since 2002 as rising energy and commodity costs intensified Turkey’s cost-of-living crisis.

As the UK Foreign Office joined the US in announcing sanctions on Vladimir Putin’s two adult daughters, it said it expects Russia’s GDP this year to contract by between 8.5% and 15%. Around £275bn, or 60% of Russian foreign currency reserves, are currently frozen, which has hampered Moscow’s ability to support its economy.

Russian consumer prices jumped 7.61% in March alone, the fastest monthly increase in inflation since 1999. Annual CPI inflation rose 16.69% in year-on-year terms in March, sharply up on February’s 9.15%.

The United Nations’ Food and Agriculture Organization (FAO) reported that world food prices reached record highs in March as the war in Ukraine drove up prices. The FAO’s food prices index rose nearly 13% in March, adding to global inflationary pressures.

Global trade fell 2.8% between February and March as Russia’s invasion of Ukraine hit imports and exports, according to the Kiel Institute of the World Economy.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please find below an article on the increase in student loan repayments, received from AJ Bell, yesterday evening – 07/04/2022

Chancellor Rishi Sunak has announced a shake up of the student loan system, which will make it more expensive for people to go to university and mean graduates are paying off their loans for up to 40 years after they leave university.

Graduates and potentially their parents may be left wondering if there’s a case for taking action to pay off borrowings as early as possible in light of these changes.

The modified rules extend the period until your loan is wiped out from the current 30 years up to 40 years. It means someone who graduates when they are 21 could be paying off their loan until they are 61.

The next big change is that the threshold at which you start repaying your loan has reduced from the current £27,295 down to £25,000. However, one help for graduates is that the interest on the loan will be simplified to be just the current rate of RPI inflation, where currently it’s charged at RPI plus up to 3%, varying by your income.

REPAYMENTS GOING UP

However, the combined impact of these changes mean that many graduates will repay more than double what they currently do. For example, someone who graduates with £45,000 of debt on a starting salary of £30,000 a year will currently pay back £30,900 in total, assuming their salary increases by 3% a year. Under the new system they will repay £71,518 – so almost £27,000 more than they borrowed thanks to the impact of interest over the 40-year term of the loan.

Someone who starts on a lower graduate salary of £20,000 will pay back £7,207 under the new system, whereas previously they wouldn’t have repaid any of the loan as they would never have earned enough to get over the income repayment threshold.

However, the changes do benefit higher earners, who will pay off their loan faster and so incur less interest over the term of the loan, but also benefit from the lower, flat-rate interest under the new system. For example, someone on a starting salary of £50,000 (on the same debt and salary increase basis as above) would pay off almost £117,000 under the current system, but only £62,000 under the new system. Of course, few graduates will start on such a high salary.

SO IS IT BETTER TO PAY OFF THE LOAN STRAIGHT AWAY?

Parents who have a lump sum they could use to pay off the debt will now be wondering whether it’s better to pay off the loan as soon as their child graduates (or just not take out the loan in the first place and use that pot of money to pay for their child’s university education) or whether they leave their child to pay off the loan through their salary. However, it’s not an easy calculation and relies on some big assumptions about your child’s future earning potential.

The first thing to note is that student loan debt is not the same as other debt – you don’t have to pay it if you have no income, or your income falls below the new £25,000 a year threshold. So, if you take time out, a career break or work part-time on a lower salary, you wouldn’t be liable to pay it. It also doesn’t count on your credit file as debt like that volume of credit card debt would, for example.

Regardless, many graduates won’t want their university debt following them around for 40 years if they can help it. And, as you repay your debt at a rate of 9% of any income over the £25,000 threshold it means that graduates have a 42.25% effective tax rate over this income level (20% basic rate tax, 13.25% National Insurance and 9% student loan repayments). That could significantly impact their ability to save money for a house deposit, for example, or to live the lifestyle they want.

However, whether it’s worth paying off the loan hinges on what your child is likely to earn. Someone with £45,000 of debt on a starting salary of £25,000 who sees a steady 3% a year increase in their salary will repay just over £36,000 in total over the 40 years. That’s obviously much less than the amount they initially borrowed and so means it wouldn’t be worth paying off the debt when they graduate. However, a small increase in their starting salary to £30,000 changes the figures entirely, as they would pay off just over £71,500, far more than the initial debt.

ACCOUNTING FOR PERSONAL CIRCUMSTANCES

These scenarios don’t account for any career breaks, due to having children, going back into education or travelling, where the graduate would make no repayments. And nor do they account for big increases in salary, due to promotions or switching jobs. And both these factors can dramatically impact the sums.

Let’s take that person starting on £30,000, with £45,000 of debt and a gradually rising salary. If they took a five-year career break early on in their career and then resumed work on their previous salary their repayments will reduce to just more than £40,000.

Now take that same individual starting on £30,000 with no career break but instead they get three pay rises of £5,000 each in years five, 10 and 15 of their career – now their repayments rocket to almost £104,000 – meaning that it would have made financial sense to pay off the loan when they graduated.

As these figures highlight, there’s no easy answer. Some of it will come down to the career your child picks and their likely future choices around career breaks, and some may come down to whether that’s the best use of the lump sum you have sitting around.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses

Please see the below article from Brewin Dolphin, detailing the key stories from economies around the world, as well as global market performance over the past week – received yesterday evening – 05/04/2022

S&P 500 sees worst quarter since early 2020

US stocks gave a lacklustre performance last week to cap their worst quarter since the start of the pandemic in early 2020.

The S&P 500 ended the week largely flat, taking its loss for the quarter to nearly 5%, as the ongoing war in Ukraine weighed on investor sentiment. Bond yields were in focus after an often-cited recession indicator was triggered when the two-year and ten-year Treasury yields inverted for the first time since 2019.

After a volatile few days of trading, UK and European indices finished the week mostly higher despite concerns about the macroeconomic outlook. The pan-European STOXX 600 added 1.1%, Germany’s Dax gained 1.0% and the FTSE 100 rose 0.7%.

Over in Asia, Japan’s Nikkei 225 declined 1.7% as sentiment among Japanese manufacturers fell in the first quarter for the first time since the start of the pandemic. China’s Shanghai Composite advanced 2.2% after the government indicated it would provide support for the economy and markets.

UK consumer confidence plummets

Stocks started this week in the green, with the FTSE 100 edging up 0.3% on Monday (4 April) despite data showing UK consumer confidence suffered its biggest fall in March since 2008. PwC’s consumer sentiment index fell to -20 after peaking at +10 in June last year. The 30-point drop in nine months was the biggest sustained fall since the global financial crisis. PwC said the cost-of living crisis was causing post-pandemic pent-up demand in discretionary spending to “all but evaporate”.

The pan-European STOXX 600 added 0.9% on Monday as investors digested news that Western nations might impose further sanctions on Russia. US indices also rose, with the S&P 500 and the Nasdaq up 0.8% and 1.9%, respectively.

UK and European stock markets were down at the start of trading on Tuesday ahead of the latest UK services purchasing managers’ index.

Households hit with surge in energy costs

Dubbed “Bleak Friday” by several newspapers, 1 April marked the day that price rises for many UK household bills came into effect. The most notable of these was a 54% rise in the price cap on energy bills. A household using a typical amount of gas and electricity will now pay almost £700 a year more than they did last year. Council tax, water bills and car tax have also increased for some households.

It isn’t just consumer confidence that is being affected by soaring prices. A closely watched gauge of business sentiment showed economic confidence collapsed in March. The index from the Institute of Directors (IoD) plunged from -4 in February to -34 in March, the lowest since October 2020. Over half (53%) of business leaders said the cost of energy is exerting a negative impact on their organisation, three times as many as a year ago. Business leaders’ expectations of inflation continued to rise.

Kitty Ussher, chief economist at the IoD, said: “Business has experienced a dramatic collapse in confidence following the invasion of Ukraine, leading to many firms putting investment plans on hold. The reality of higher energy and commodity prices, plus the hike in employment taxes, all overlaid with a general climate of deep uncertainty, is now having a real economic impact.”

Eurozone inflation soars to 7.5%

The eurozone is also witnessing surging consumer prices. According to Eurostat’s latest flash estimate, the annual rate of inflation reached a record 7.5% in March, accelerating from the previous record of 5.9% in February. This was far higher than the expected 6.6% increase.

Energy was the main contributor to the increase, as the war in Ukraine and sanctions on Russia pushed fuel and natural gas prices to record highs. There were also increases in the prices of food, services and durable goods.

According to the Financial Times, the figures have prompted some European Central Bank (ECB) policymakers to call for the central bank to bring forward its plan to end net asset purchases and to raise interest rates for the first time in more than a decade. So far, the ECB has only announced plans to stop net bond purchases by September, when it will decide if inflation will stay high enough to justify a rate increase.

US nonfarm payrolls lower than expected

The US economy added 431,000 jobs in March, down from 750,000 the previous month and below the expected 490,000. Despite missing forecasts, the figures are still considered strong and show the tight labour market is persisting. Jobs growth averaged 562,000 per month in the first quarter of 2022, the same as the average monthly gain for 2021, as the lifting of Covid-19 restrictions and strong consumer demand kept labour demand high.

The data from the Bureau of Labor Statistics also showed the unemployment rate fell by 0.2 percentage points to 3.6%, the lowest level since before the pandemic. Average hourly earnings rose by 0.4% from the previous month, or by 5.6% from a year ago, as businesses competed for talent and rushed to fill a near-record number of job vacancies.

In other US economic news, personal spending, which accounts for more than two-thirds of US economic activity, rose by only 0.2% in February after an upwardly revised 2.7% gain the previous month. Spending on services rose by 0.9%, the most in seven months, whereas spending on goods fell 1.0% led by a slump in purchases of motor vehicles.

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below Brooks MacDonald’s summary of what happened in markets last week:

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Please see below weekly news update received from Blackfinch this morning, which provides a summary of global events from their multi-asset portfolio managers.

UK COMMENTARY

Reuters reported that the UK government had sanctioned 14 more Russian entities and individuals, including the state media organisations behind Rossiya Television and Sputnik, and some of their senior figures, for pushing out “Putin’s fake news and narratives”

According to Nationwide, UK house prices rose 14.3% in the year to March. This was the strongest increase since November 2004, when the UK experienced a housing boom that preceded the financial crisis.

The Office for National Statistics (ONS) reported that UK gross domestic product (GDP) rose by 1.3% in the fourth quarter of 2021, stronger than a preliminary quarterly growth estimate of 1.0%.

According to an extensive ONS survey of more than 13,000 UK, 83% saw an increase in their cost of living in March, up from 62% in November.

NORTH AMERICA COMMENTARY

The US unemployment rate fell from 3.8% to 3.6%. The largest job gains were in leisure and hospitality, which added 112,000 new jobs in March. This was the 11th consecutive month of job gains of more than 400,000, the longest stretch of jobs growth on record.

Over the past 12 months, average US hourly earnings have increased by 5.6%.

US GDP growth in the fourth quarter was reported as lower than forecast. The annualised growth rate was revised slightly from 7.0% to 6.9%.

EUROPE COMMENTARY

Soaring energy prices pushed inflation in the Eurozone to 7.5% in March, according to the preliminary estimate from the European Union’s statistical office Eurostat. This was the highest inflation rate since the single currency was created.

In Italy, inflation rose to an annual rate of 6.7% in March, according to a preliminary estimate from Istat, Italy’s statistics office.

Eurostat reported that the unemployment rate in the Eurozone fell to a record low of 6.8% in February, from 6.9% in January.

In Germany, the number of unemployed in February fell by 20,400 from January to 1.34 million, according to official figures. The unemployment rate stayed at 3.1%.

In Spain, rocketing energy prices meant inflation reached 9.8% in March, the highest annual rate since 1985.

ASIA COMMENTARY

China’s National Bureau of Statistics reported that the official Chinese Manufacturing Purchasing Managers’ Index (PMI) fell to 49.5 in March from 50.2 in February, , while the non-manufacturing PMI dropped from 51.6 in February to 48.4 in March, its lowest level since August 2021.

Please check in again with us shortly for further relevant content and news.

Please see below article received from AJ Bell yesterday afternoon, which provides insight into global emerging markets from the Franklin Templeton Emerging Markets Equity team.

The Russia-Ukraine conflict dominated global headlines and rattled financial markets after Russia invaded Ukraine. Aside from the tragic humanitarian impact, a major consequence of the conflict has been a surge in commodity prices on expectations of weaker supplies, as both countries are major exporters of energy and agricultural commodities. The longer-term impact of the energy shortage could also result in an acceleration in the pace of decarbonisation, especially in Europe as it may work toward reducing its dependence on Russian gas. Markets are entering uncharted territory in terms of the implications of a war on Europe’s borders.

We expect to see different outcomes for different regions and believe that markets in Asia and Latin America could be relatively more insulated from the heightened geopolitical risk in Europe. Oil producers in the Middle East are also beneficiaries of higher oil prices. As energy costs rise, we could also see a faster shift to renewables and electrification. Apart from China and to a lesser extent South Korea, emerging Asia has limited direct trade exposure to Russia and Ukraine. Higher commodity prices could, however, impact the region which, except for Malaysia and Indonesia, is a net energy importer. In resource-rich Latin America, energy and mining companies stand to benefit from higher prices and supply shortages. With limited direct trade with Russia and Ukraine, the impact on corporate earnings generally across the region could also to be limited as these countries account for a marginal part of their revenues.

Brazil defied the global market rout in February to end the month higher. The MSCI Brazil Index rose 18% in the first two months of the year, outperforming the MSCI Emerging Markets Index and the MSCI World Index. As the world’s fourth-largest commodity exporter, the continuation of last year’s commodity price surge amid global supply concerns from the Russia-Ukraine conflict has been good news for Brazil’s commodity exports, economy and market. The country is the biggest exporter of soybeans and coffee, and the second-biggest exporter of corn and iron ore. Surging commodity prices are leading analysts to raise earnings forecasts in Brazil. The consensus estimate for 12-month forward earnings per share in Brazil is up 6% year-to-date. Despite the stock market’s recent climb, valuations look appealing.

We will continue to publish relevant content and news, so please check in again with us shortly.